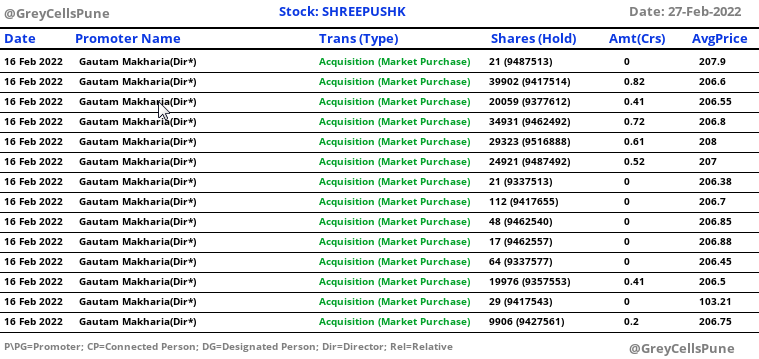

Including the latest warrants, they will have issued a total of 1,406,445 shares since IPO in 2015, representing equity dilution of ~4% as against an increase in PAT by ~120% from March 2016 to March 2022 (assuming PAT of 50 cr for current FY). It’s not that significant here - definitely a problem in many other small caps.

3 Likes

How does this impact company ? can you please explain

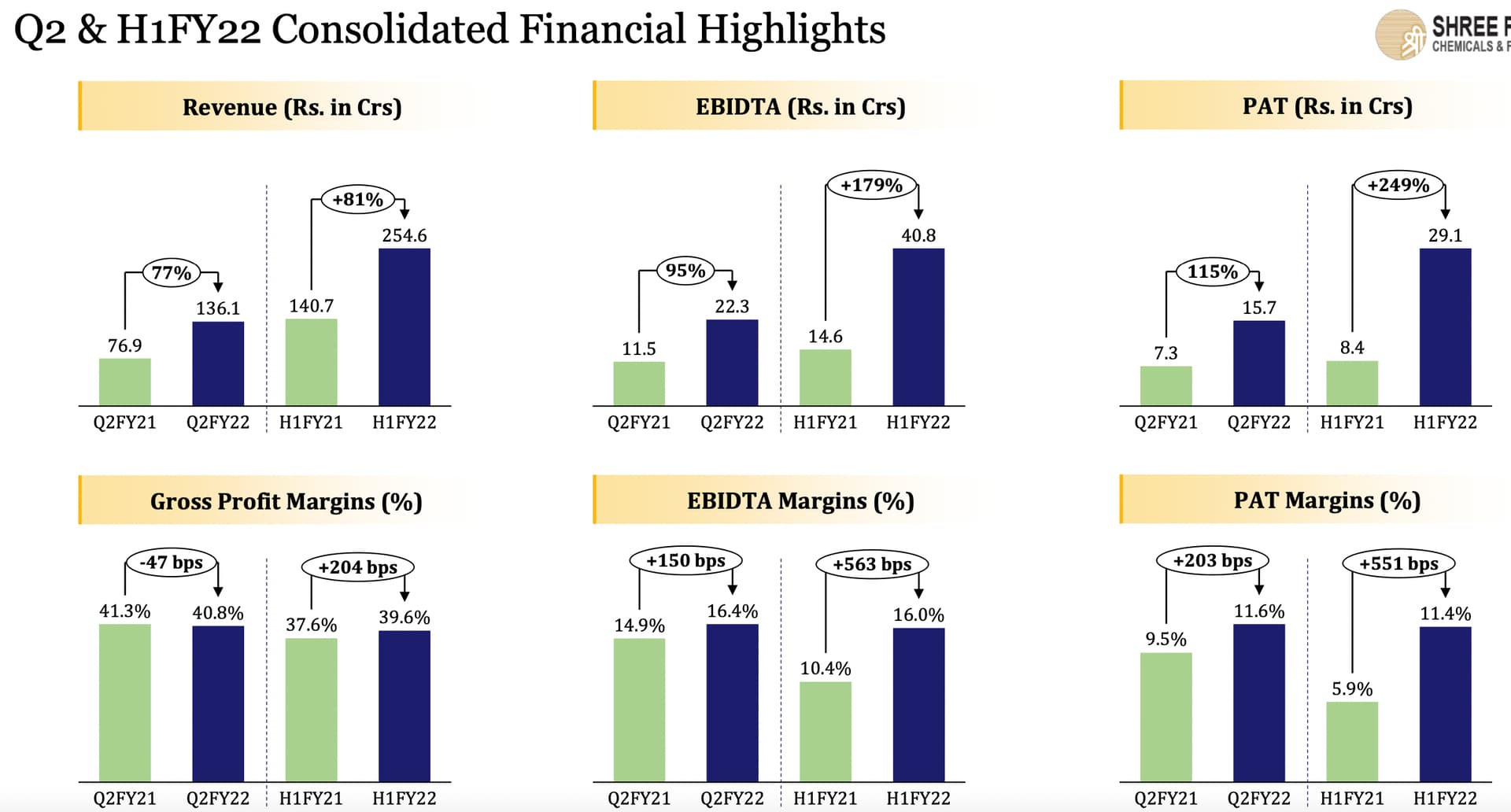

Strong numbers again from Shree Pushkar.

- All time high quarterly revenue, EBITDA and PAT

- YoY 77% revenue & 115% PAT growth. Good QoQ growth as well. Very impressive margin performance in a quarter where most companies have struggled with input and logistics costs

- Capex update: Solar project and Unit 5 will be commissioned in FY22 - not clear whether Unit 5 is partially contributing already or not. If these are the numbers without Unit 5 then it is doubly impressive. In the last call, they had mentioned new expansion plans would be shared post-Diwali.

- With Unit 5 coming online, we should expect H2 to be better than H1. 150cr+ quarterly topline is attainable, given sufficient headroom to sweat existing capacities

- Valuations remain very reasonable. If we annualise this quarter’s performance, the stock is trading at ~11x P/E and ~8x EV/EBITDA. Remains net-debt free

Disc. Invested

4 Likes

Q2 FY22 Con Call highlights

-

Unit 5 commissioning - Out of the total planned Capex of INR 90 crores, INR 86 crores incurred, from the internal accruals. Dry trial runs in December and the commercial production by the end of December or maybe the first week of January. Can expect 1-2 months of contribution in FY22.

-

Installation of 2 solar power projects - Total planned Capex of these 2 solar plants would be INR 21 crores, funded through internal accruals. We have already incurred approximately INR 10 crores till date. We anticipate these power plants will go online in FY '22 itself, and hence anticipate power cost savings of INR 6 cr/year from FY '23 onwards.

-

Future expansion - Will be announced only after Unit 5 is commissioned. Company is keen to consolidate and stabilise the recent Capex program of ~150cr before announcing new plans

-

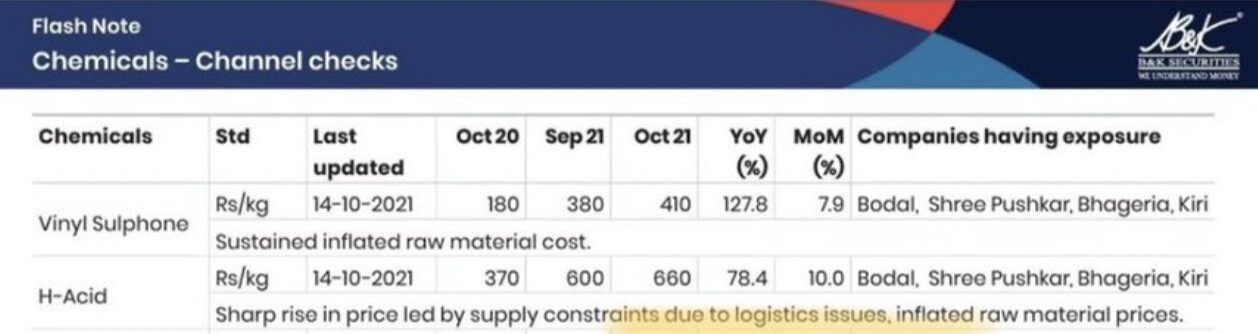

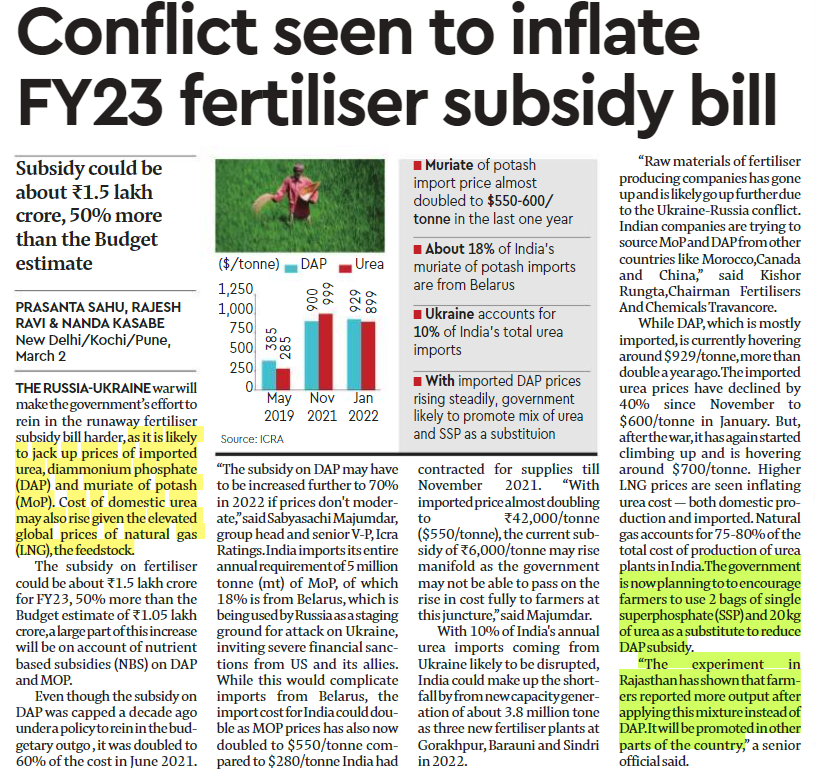

Increase in prices of Vinyl Sulphone & H-Acid - Should be visible in Q3. Company is holding inventories and is easily able to pass on the price increase of raw materials to the customers. Vinyl Sulphone price is somewhere prevailing around INR 400, and H-Acid is around INR 600 to INR 635 a kg. Note - corroborated this with a recent report →

-

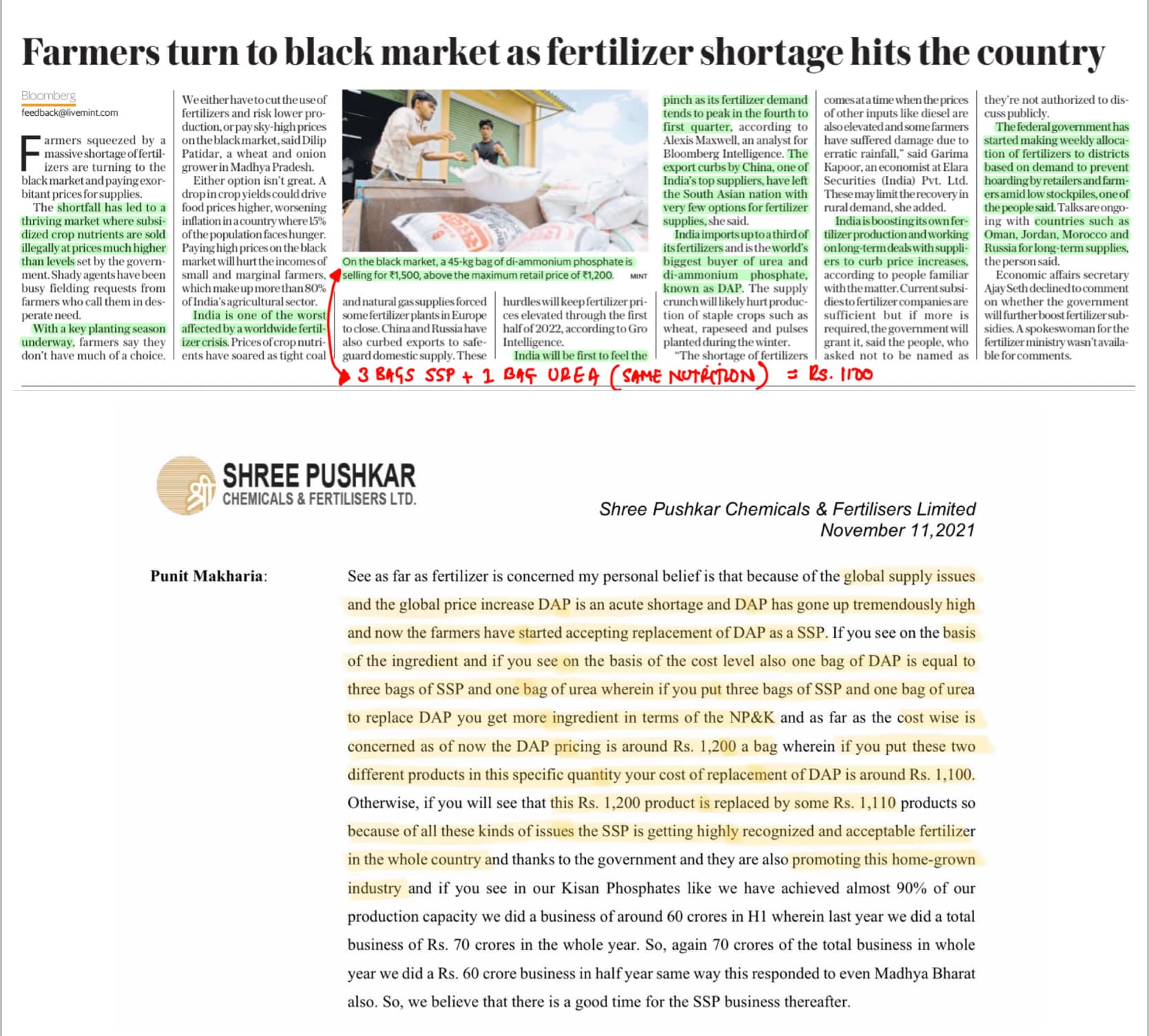

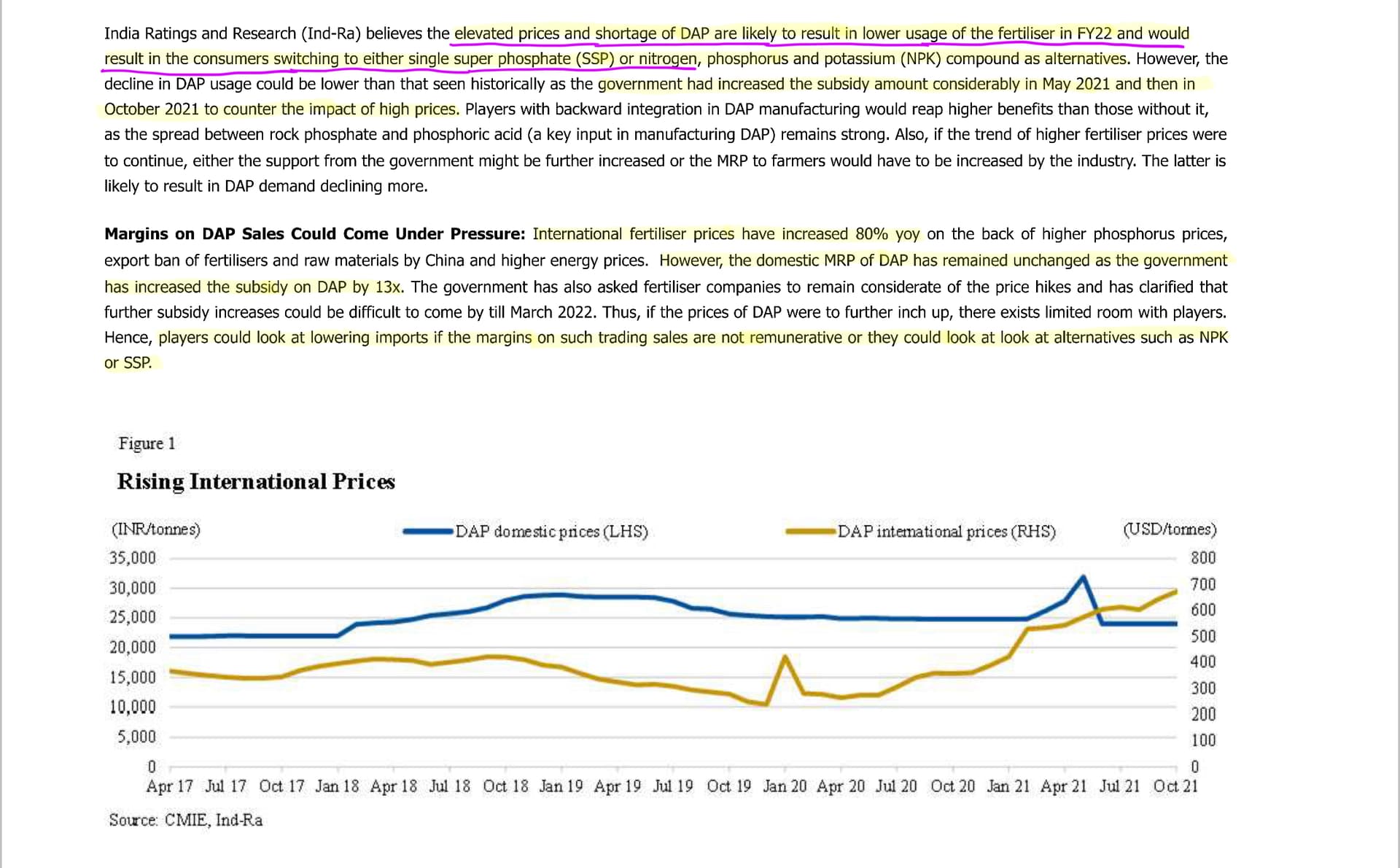

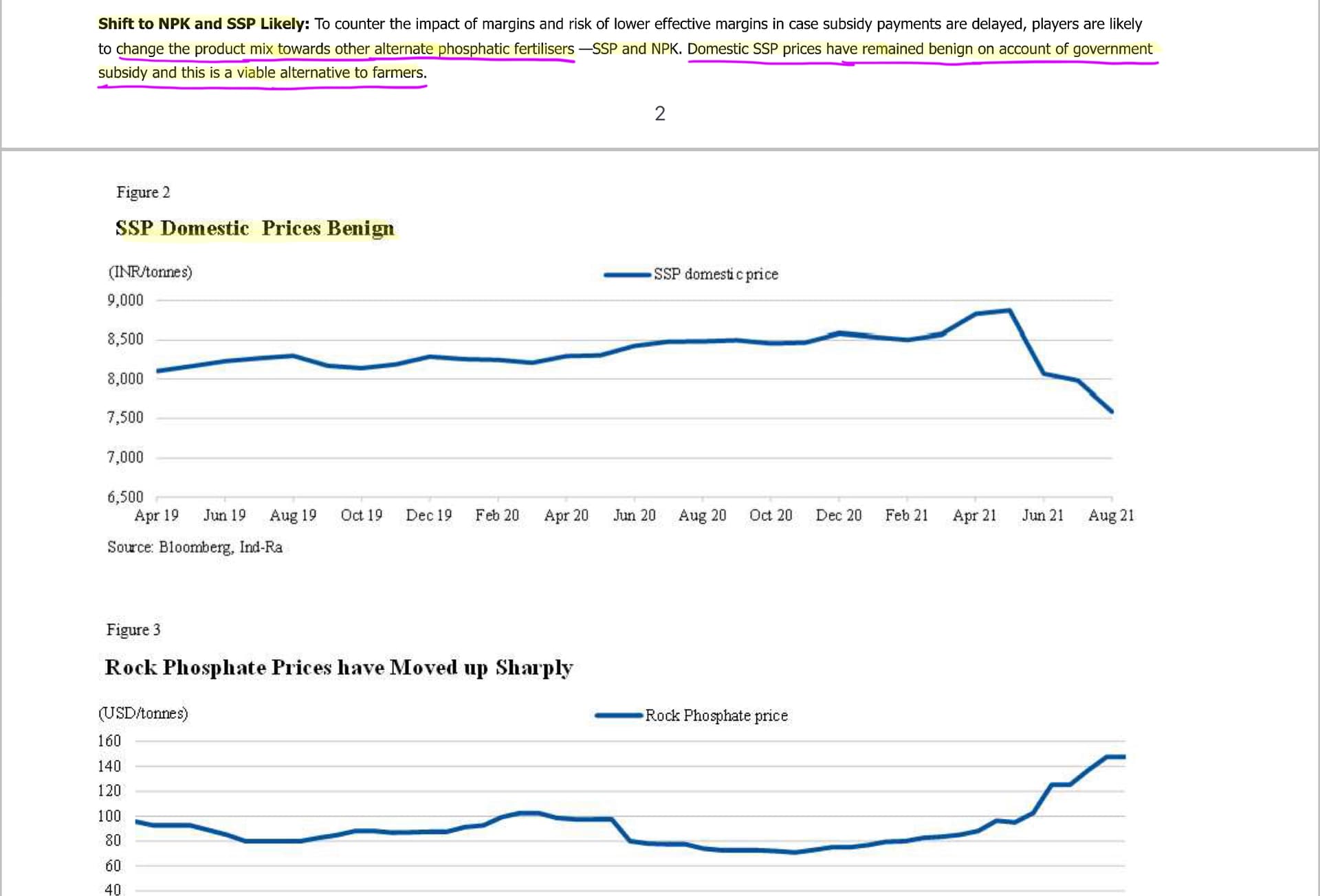

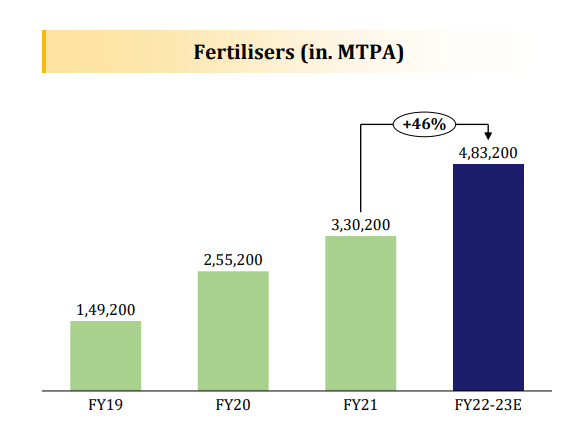

Increased acceptance of SSP fertiliser in India: Due to global supply issues and the global price increase, DAP is an acute shortage and prices have increased. Now the farmers have started accepting replacement of DAP with SSP. Reason → If you see on the basis of the ingredients and if you see on the basis of the cost level also, 1 bag of DAP is equal to 3 bags of SSP + 1 bag of Urea, wherein if you put 3 bags of SSP and 1 bag of urea, to replace DAP, you get more ingredients in terms of the N, P and K. DAP pricing is around INR 1,200 a bag, wherein if we put SSP + Urea, your cost of replacement of DAP is around INR 1,100. So otherwise, if you see that this INR 1,200 product is replaced by INR 1,100 product. Government is also promoting SSP as a home grown industry vs DAP which is majorly served through imports

-

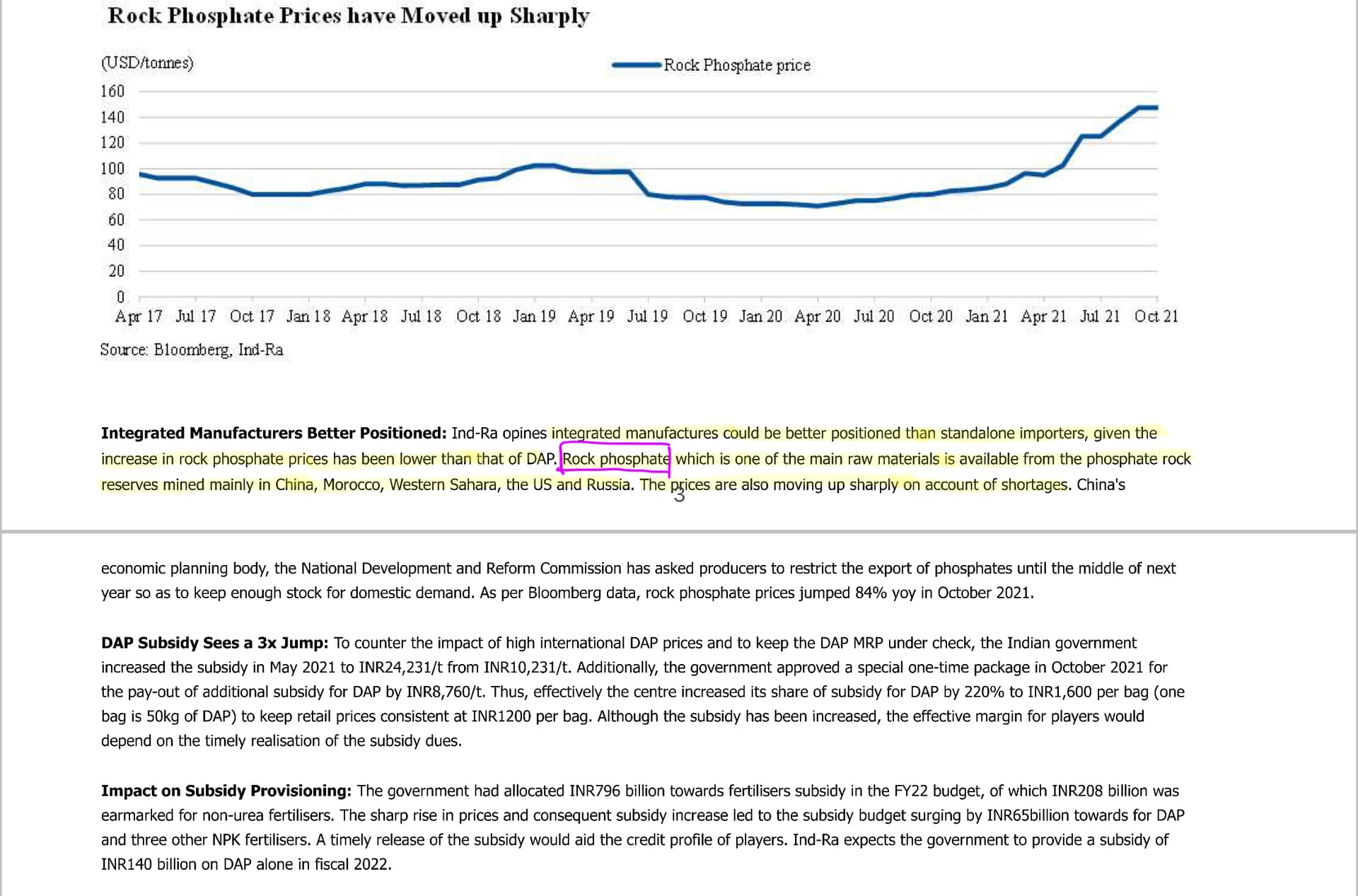

Supply chain - Not a major issue. We have stocked rock phosphate till March 2022, due to which inventory levels have gone up and there was pressure on the cash flows because majority of the money is locked into inventory. Company has also opened some LCs for raw material purchase

-

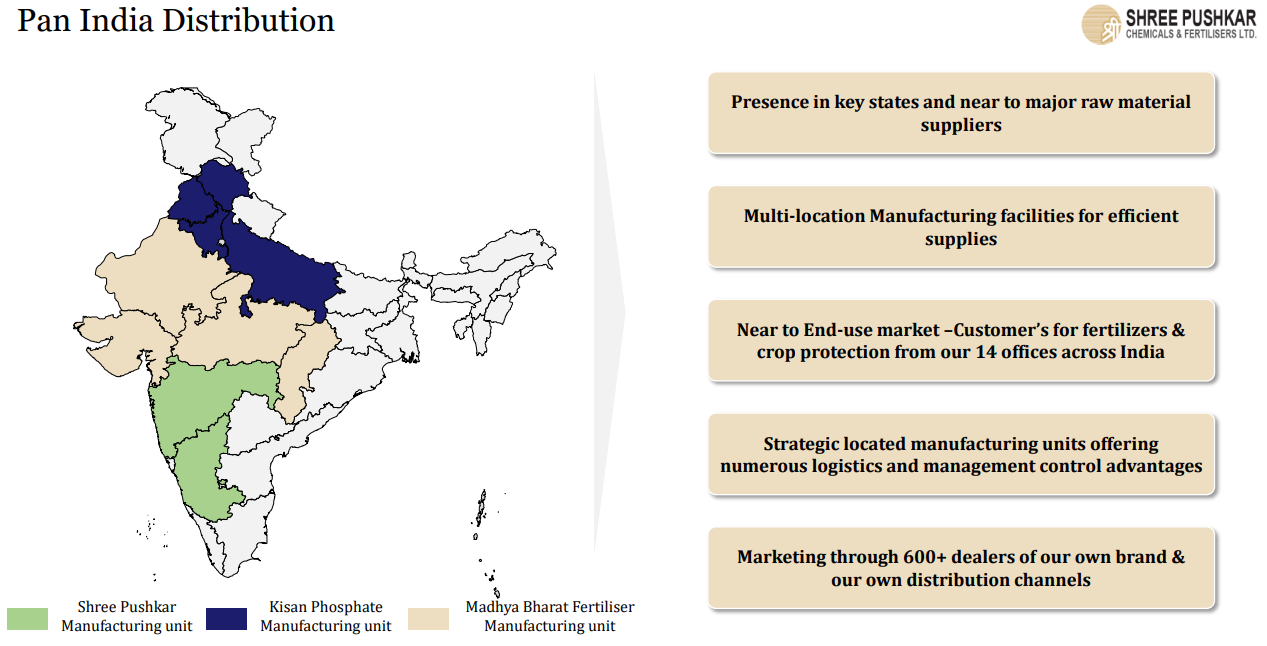

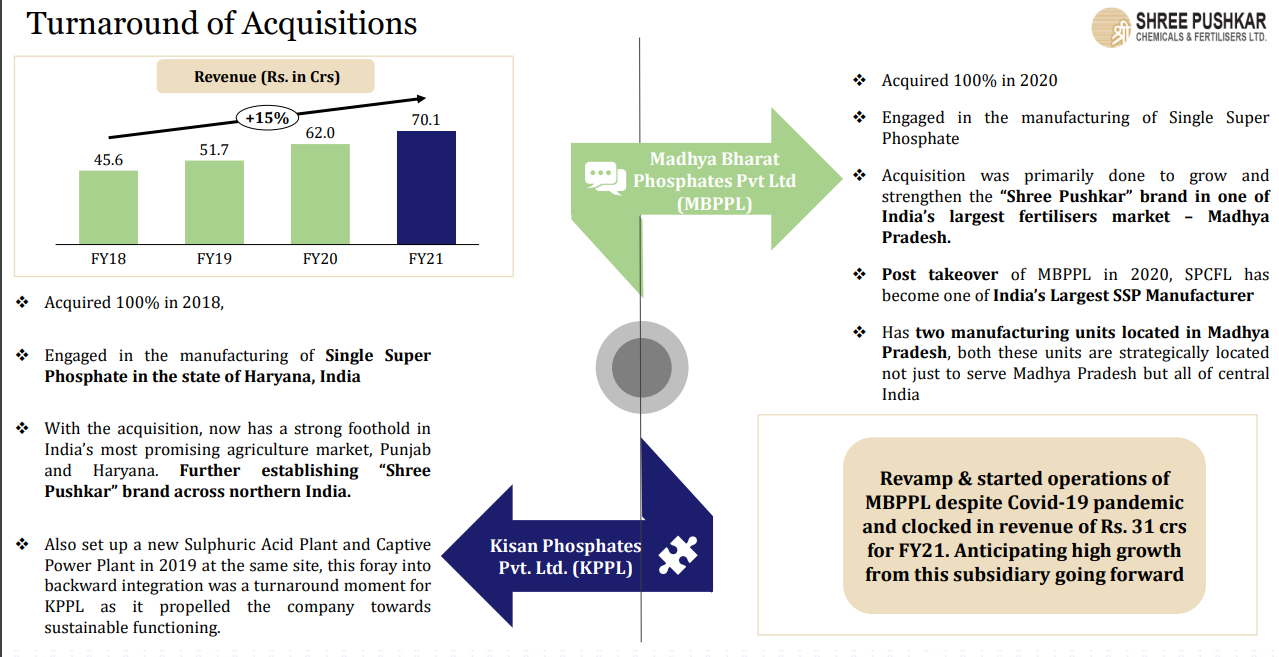

Guidance for FY22 - Total sales - 525 cr, of which Madhya Bharat will be 100 cr and Kisan Phosphates will be close to 120 cr. Margins will be similar or better than H1. Sticking to earlier guidance despite losing Unit 5 contribution

-

Guidance for FY23 - Total sales - 775 cr, with Unit 5 contributing for the full year. This is up from earlier guidance of 650-700 cr given in Q1

-

Demerger - No plans for next 2-3 years

7 Likes

Very informative thread

With increasing product prices, upcoming capacity, the co looks to be at very reasonable valuation

5 Likes

60% yoy increase in SSP sales in Oct-Nov period due to DAP shortage.

6 Likes

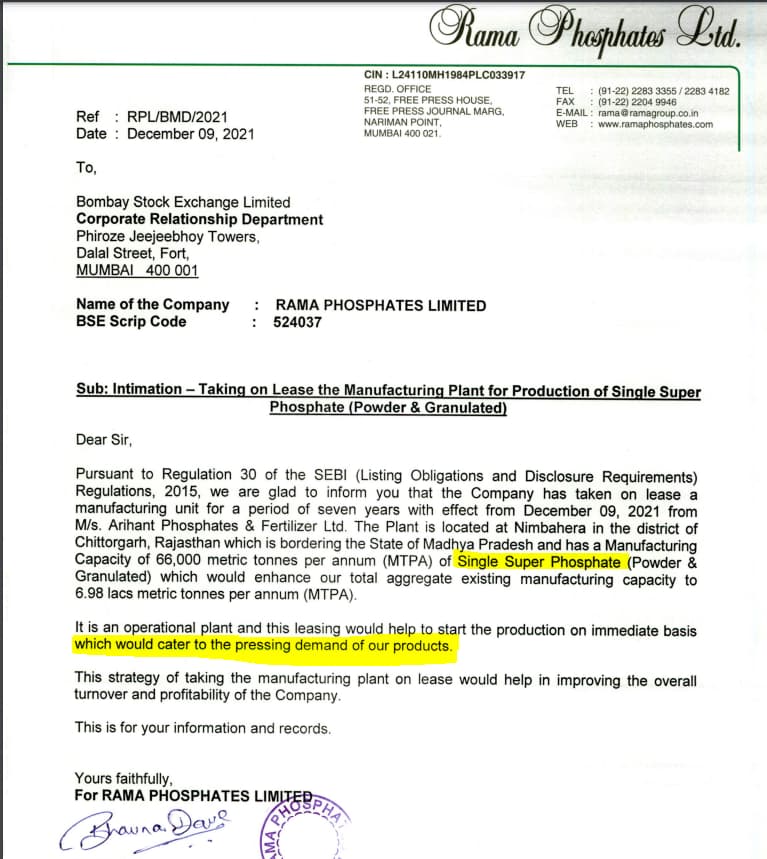

Rama Phosphates leasing plant for SSP production due to pressing demand for the fertilizer…

Next few quarters should be excellent for Pushkar with KP and MB in play as well.

4 Likes

Q3FY22 results look flattish at first glance - however accounting for increased inventory gross margins improved substantially sequentially. This is most likely due to improving realizations for Dye Intermediates and possibly Dyes. We will know after the concal next week once they share the volumes. So good news is that they seem to be able to pass on input cost increases. This while Unit 5 is sucking up cost but not yet contributing to top-line.

| FY19 | FY20 | FY21 | Q1FY22 | Q2FY22 | Q3FY22 | |

|---|---|---|---|---|---|---|

| Sales | 452 | 347 | 355 | 119 | 136 | 137 |

| GP | 149 | 132 | 143 | 45 | 55 | 60 |

| GP% | 33% | 38% | 40% | 38% | 40% | 44% |

| EBITDA | 67 | 50 | 43 | 18.4 | 21.8 | 22 |

| EBITDA % | 14.8% | 14.4% | 12.1% | 15.5% | 16.0% | 16.1% |

| EBIT | 60 | 42 | 37 | 16.9 | 20.7 | 20 |

| EBIT % | 13.3% | 12.1% | 10.4% | 14.2% | 15.2% | 14.6% |

| PAT | 41 | 36 | 29 | 13.4 | 15.7 | 12.4 |

| PAT% | 9.1% | 10.4% | 8.2% | 11.3% | 11.5% | 9.1% |

| EPS | 13.3 | 11.6 | 9.3 | 4.34 | 5.05 | 3.85 |

One question would be that why no revenue growth sequentially QoQ? CEO indicated good demand scenario for DI+Dyes as well as SSP in Q2 call.

Another question would behow much of HA and VS price increase is already captured in realizations versus how much will kick in into Q4. CEO had indicated spot prices for HA and VS to be trending around Rs 600 and 400/kg resp. in November call. Meanwhile, below excerpt from Bodal Q3 results (they seem to have swapped HA and VS prices though)

3 Likes

Company has upped its revenue guidance for FY22 to 550 cr and FY23 to 900-1000 cr.

Basis for FY23 guidance is 550 cr (base) + 250 cr (Unit 5) + 100 cr (Deewanganj, Kisan, cattle feed expansion) + X (to be announced organic/inorganic growth)

Unit 5 dry runs have commenced and they don’t see any reason for further delay beyond a March commissioning date. Will be important to see if they deliver on this given the extended delays so far.

disc. Invested

6 Likes

The 250 cr projection for Unit 5 is a bit difficult to understand. The stated capacity increase is around 24,000 MT. In Q3 call, it was stated that Q2 DI sales (net of internal consumption) was 800 MT. In Q2 they had stated that DI sales were 29 cr. That works out to Rs. 400/kg in realization. Even if we take FY20 or 21 lower realizations for Rs 300/kg, 24,000 MT additionall capacity at 70% CU should translate to annual sales of 24,000 MT * 1000 * 70% * 300 => 500 cr. I am assuming that all new DI capacity is for external sales as there is no capacity increase in Dye manufacturing.

So why is management guiding for 250 cr sales increase from DI only?

1 Like

Here’s the responses I recvd frm company on my questions:

1)Can you please share the detailed breakdown per site of products made (SSP, SOP, DI, etc.), current capacity, target capacity per ongoing CAPEX and estimated completion month-year for that CPAEX. This was something Mr. Makharia promised to make available afterwards due to confusion around capacity.

> The capacity details have been attached with this email. Unit V would be starting commercial production by March 2022. Solar plant is ready. MBPPL and KPPL new capacity will be potentially active by Q1 of FY 2022-23

- What was the average pricing for H-Acid and V-Sulphone during Q3 and what is the rough current market price?

> H Acid- Rs. 525/- and VS- Rs. 300/- . Current rough price- H Acid- Rs. 490-500/- and VS- Rs. 300/-

- Mr. Makharia guided for around ~250 Cr additional revenue run rate once Unit 5 comes onstream in FY23. I understand that additional capacity will be 24,000 MT in Dye Intermediates. How does this translate to 250 cr revenue only as per my rough estimation it should be much much higher? Please see below and point out what I may be doing wrong in my assumptions.

In Q3 call, it was stated that Q2 DI sales (net of internal consumption) was 800 MT. In Q2 it was stated that DI sales were 29 cr. That works out to Rs. 400/kg in realization. Even if we take FY20 or 21 lower realizations for Rs 300/kg, 24,000 MT additionall capacity at 70% utilization should translate to annual sales of 24,000 MT * 1000 * 70% * 300 => 500 cr. I am assuming that all new DI capacity is for external sales as there is no capacity increase in Dye manufacturing.

> The Capacity of 24000 MT includes different product mix with different capacity utilisation for each of those products at different price so we can’t take Rs. 300/- , Target turnover will be Rs. 250 Crs

Capacity Details_Feb22.xlsx (10.7 KB)

10 Likes

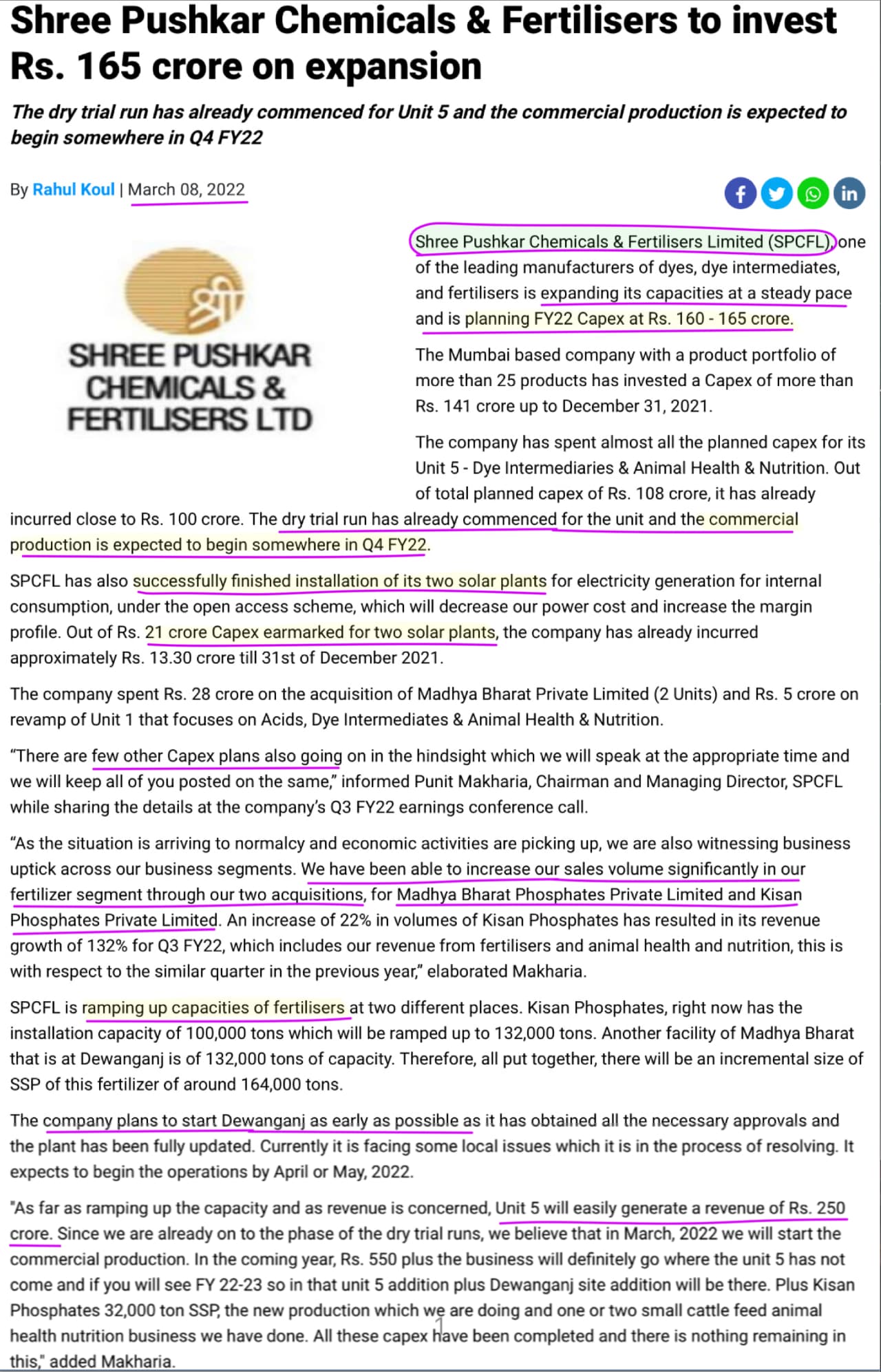

Nothing new in this article versus what was shared in the Q3 concal - but thanks for sharing.

1 Like

Dr. Mansukh Mandaviya assures to take steps to support Single Super Phosphate industry

Mandaviya asks countries to fix fertiliser prices responsively

1 Like