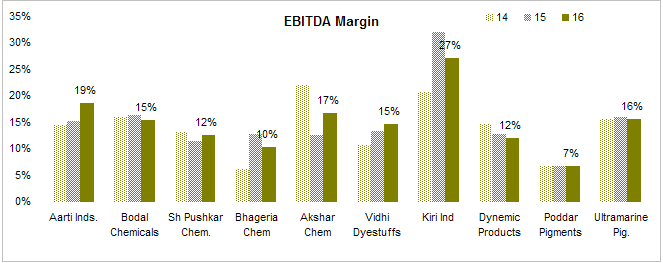

Shree pushkar – specialty chemicals

Mcap= 511 cr.; P/E= 19 ; ROCE= 21.86% ; ROE= 17.72% , promoter holding is around 60 percent.

Single Plant located in Lote Parshuram , Maharashtra

Manufacturer of dye intermediates, reactive dyes, cattle feed , fertilisers, acid complex .

In 1993 company was engaged in trading of chemicals. It switched to manufacturing of dye intermediates from 2000 .Over the last 15 years company has done backward integration by putting up capacities for manufacturing RMs used in dye intermediates. It has a capacity of 8000 MTPA for dye intermediates. Main dye intermediates compounds involve Gamma Acid, K-Acid, Vinyl sulphone, R-Salt, Meta Ureido, etc. The company is the worlds largest manufacturer for K Acid. Dye intermediates are used for making dyes which are further used for colouring textiles.

In H1 FY 2017 this dye intermediate division contributed to 72 percent of revenues of the company. The clients of the company include big companies Huntsman Corporation USA, Arochroma Switzerland. Its operated currently at an utilization level of around 70 percent. The realisations of vinyl sulphone is Rs. 400/ kg and of Hacid is Rs. 425/kg. Vinyl sulphone is a product which is in great demand, due to the closure of factories in China(environemental concerns) and price of this product is expected to remain high., as per the guidance given in the Q2 concall. (http://www.moneycontrol.com/news/business/what-risevinyl-sulphone-price-means-for-indian-dye-makers_7459061.html) http://www.textileexcellence.com/news/details/1081/dyestuff-makers-will-see-revenues-rise-of-40-50--this-year

Since the major focus has shifted from China to India for the manufacture of these products many Indian companies like Kiri Industries have been putting up huge capacities for the manufacture of these products. However given the fact that Shree Pushkar is completely backward integrated it should be able to fight competition on a price basis. The world market for dye intermediates and the amount produced in the factories of China need to be studied to get a better picture.

The company has decided to forward integrate by starting the manufacturing of reactive dyes. Reactive dyes is a special type of dye which makes covalent bond with the fiber and become a part if it. It has put up a plant of capacity 3000 MTPA which started its commercial production from May 2016. The capacity will be increased to 6000 MTPA by Q3 2017 with a marginal capex of 5 cr. According to latest concall the management says achieving a capacity utilsation of 35- 40 % will break even this project. The amount of capital involved in this expansion and forward integration plan will be around 60 cr. The money for this expansion plan was raised via an IPO in August 2015. (61 cr was raised).

One of the great features about this company is that it has a zero waste discharge factory. Effleunts generated from one product manufactured are used to make other products. Products like fertilisers , soil conditioners and cattle feed are made by these waste effleunts.

Fertiliser

SSP , NPK , SOP , Soil conditioners are some of the products made in this division. FY 16 sales of fertilizer volume was 55606 MT and revenue was 48cr.( 20 % of total). The capacity utilization of the division was 48 percent implying a capacity of 1.16 lakh MT. The sales were a bit low last year due to delay in monsoons. The company obtained a NPK fertilizer license after a struggle of 2 years. 20000 MTPA capacity was put up which got commissioned in Feb 2016.

10,000 MTPA capacity of SOP is put by the company whose commercial production has started from Sept 2016. HCl is generated as an effluent during manufacture of SOP. Hence to follow zero discharge policy the company will be using that HCl to make calcium chloride granules. 6500 MTPA capacity is planned of calcium chloride whose commercial production has started in November.

They have an exclusive marketing arrangement with DCM Shriiram in the fertilizer segment for SSP in Karnataka and Maharashtra. They have launched its own brand Dharti Ratna in Western Maharashtra for soil conditioner.

Acid Division

The products of this division are mostly captively consumed and they include Oleum, Sulphuric Acid , CSA . This division contributed only 4 percent to the revnues in H1 FY17.

Key Strengths of the Company –

It is backwardly integrated hence making the products more cost efficient.

Has zero debt on its balance sheet.

Its becoming a one stop shop for the textile industry. The management plans to go into textile chemicals next year, they have already purchased land for it( as said in the latest concall)

It is a zero waste company. In fact the effluents are used to make new products making the company more cost efficient. It also saves the cost to treat the effluents.

The company has delivered a strong financial performance over the last 5 years.

Revenue CAGR – 14 % ; consistently increasing capacities by the cash flows generated from the business

EBITDA CAGR- 18% ; as the OPM has improved over the years. The management believes the OPM is going to be around 20 prcent for the year owing to more value added products and also higher realisations on dye intermediates

PAT CAGR – 43% ; due to financial leverage as the company has paid down its debt over the years.

The manangement has given a guidance of revenue of 350 cr this year followed by 450 cr next year, based on the expansion plans. ( Revenue was 250 cr in FY 17)Also the prices of some of the products are commanding a higher realisations due to higher demand, the company is venturing into forward integrated products, an EBITDA of 20 percent will be achievable.

Key Risks –

Competetion . Since the focus has shifted to India from China , many companies are putting up capacities to manufacture dye intermediates. The market for this segment, the growth expected in the market and the capacities being put up by the cos need to be studied in order to understand this point better.

The revival of the factories in China which were shut down for dye intermediates.

Unpredicatble monsoons is always a risk but that was not the case this year .

The management has given a guidance of revenue of 350 cr this year followed by 450 cr next year, based on the expansion plans. ( Revenue was 250 cr in FY 17)

Right… i went through the concall transcript. Somehow missed it earlier. Went through again and guess what, you are absolutely right. 325-350 cr for this fiscal, and 450 cr for next fiscal. 18-20% margin guidance.

As far as valuation is concerned, where do you see Pushkar at the moment? Currently trading at 22 trailing p/e…If we take the above numbers into account (450 cr topline/40 odd cr bottomline), 2018 forward p/e comes around 14-15.

What does in your opinion a zero debt company with mgmt as good as Pushkar’s deserve in bull market?

450 cr at 20 percent OPM , EBITDA = 90 cr.

Depreciation can be estimated max to be around 10 cr.

Hence PBT = 80 cr.

PAT will be around 55- 60 cr ( effective tax rate < 30 ) .

Hence its at a forward pe of 10 - 11.

I believe if its such a high growing company with zero debt, good management , decent return ratios , completely vertically intergrated company it deserves a forward pe of 17- 18 atleast.

Q3 results

Topline: 76 cr vr 49.6 cr up 53%, PBT at 11.07 cr vs 5.96 cr up 85%, PAT 7.23 cr vs 5.96 cr up 21%. No tax expense with deferred tax in last year nos.

350 Cr this fiscal sounds optimistic. 9M revenue is 220 Cr so they have to generate 130 Cr in Q4 to hit the 350 Cr mark. That wil be 60% jump from Q4 of last year. I know that many new capacities are ramping up but this target looks optimistic.

450 Cr next fiscal is also little too optimistic. My conservative estimate would be 400 Cr top line and 40 Cr bottom line giving a forward p/e of 14. There is some upside potential but not much.

They said 325-350 cr. I think they were expecting 90-95 odd cr sales in q3-q4. Demonetization might have impacted them a bit. I have not gone through the recent concall, which will throw some light on this. Anyone, who attended concall, can you please share the notes?

They in recent concall said (read a comment on mmb) that q4 will be much much better than q3. May be they are expecting some sales to flow into q4, which were to happen in q3. If they can manage 100 odd cr, they can still manage to almost hit the target.

This company came public at 65 Rs about 18 months ago. Its a 3 bagger already. Its hard to say that there is still some value left in this investment. As a business it will do well but as an investment, I am not too sure.

it is alright to make future projection and value a stock, but i think that is like missing the stock story. Qualitative factors are pretty much missed. Shree Pushkar seems like an interesting story because the company is trying to capture the complete value chain of the products. From trading to manufacturing to backward integration to forward integration the stock story has been pretty impressive. Also the management talks about going into textile chemicals from next year which will be followed by going into more specialty dyes. This can turn out to be interesting as these products will definitely give a better OPM margin, and good growth. So if it does well as a business i dont see why it wont do well as an investment.

Also it would be nice if someone can share their notes from the recent concall.

In the con-call the management has given a guidance of 100 Cr in top line for Q4 and said + or - 5% from that number. They have also said that tax will go down from next quarterly result from 38% to around 21% as capex will be capitalized. The top line for the previous quarter was decent and in fact better considering that the price realization from vinyl sulphone and h acid have come down from short term unrealistic prices which prevailed for some time due to the China issue. All above from the conf call.

Disc-invested.

Current price of H-acid stablized to 350 per kg and Vinyl Sulphone to 275 per kg. The prices have come down from earlier levels but as per company, even these are sustainable prices.

Expansions plan are on track.

Q4 revenue expected is ~100 crs.

Possibility of MAT to reduce the tax margins by 10-11% in Q4

Foray into textile chemicals being discussed. Building work almost completed. Machinery on its way. Management will provide a more granular update in next quarter.

Some Chinese manufacturers have started shop wrt dye intermediates. However the company doesn’t see this as a major threat as they feel that building a sustainable business model in this industry is difficult.

Confident of maintaining EBDITA of 16% and above. Confident of having CAGR of 25% plus in FY 17-18

Sales have picked up drastically post december16, Effect of demonetization will not be visible Q4 onward.

The management commentary was positive and they seem to be working to build a long lasting sustainable business model with good expansion plans.

At 18-20% they will be one of the most profitable company in the industry. In fact historically they are not the most profitable among the peers despite generating by-products from effluent treatment. 16% sounds more reasonable. That puts the PAT for FY2018 at 40 Cr.

They said that any sustainable business needs 16-17% margins.

Their current quarter margins were 17.9.

They said they ll always strive to do above 16-17.