Had anyone attended Shivalik Rasayan’s AGM on 29 Sept? If so, any notes/key takeaways?

Disc- no holdings as of now, tracking closely

Had anyone attended Shivalik Rasayan’s AGM on 29 Sept? If so, any notes/key takeaways?

Disc- no holdings as of now, tracking closely

Company has not been able to convert expensive capex plans to Sales. Any news on when this could happen? Clearly timing is of essence in this stock.

cheers for the great work.

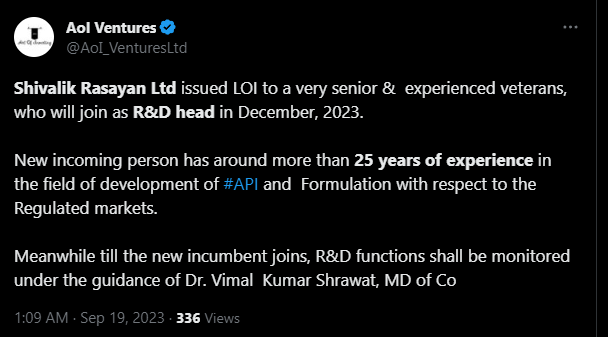

Anyone knows name of the veteran who will join the company’s R&D section ?

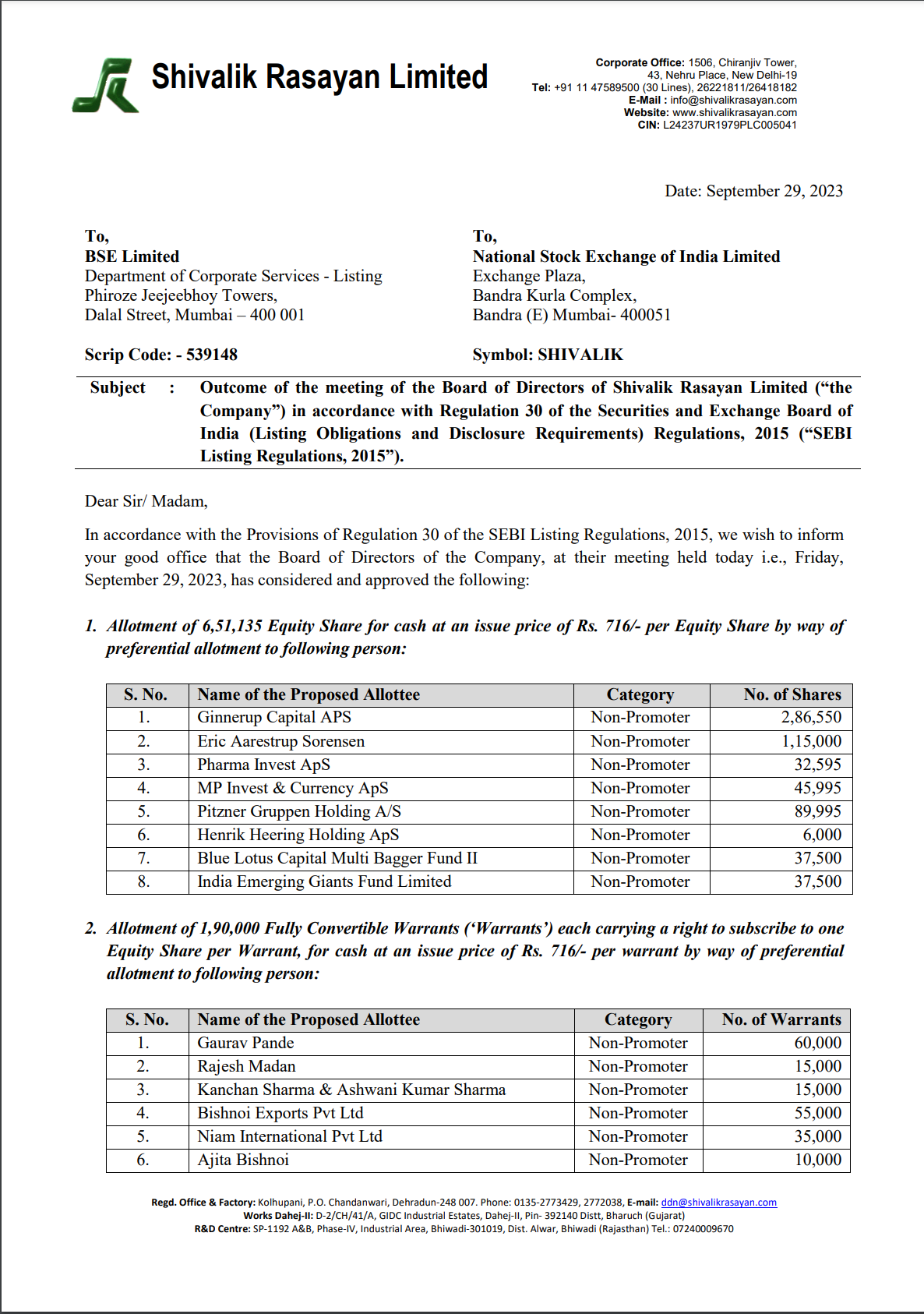

Allotment of 6,51,135 Equity Share for cash at an issue price of Rs. 716/- per Equity Share

Allotment of 1,90,000 Fully Convertible Warrants (‘Warrants’) each carrying a right to subscribe to one

Equity Share per Warrant, for cash at an issue price of Rs. 716/- per warrant

Shivalik AGM FY23

** Management Commentary**

Agro:

Filed 2 patents in the US which are already granted. Dehradun plant was working for 90% capacity. Last year couldn’t do well due to uneven rainfall.

New facility has almost commenced, last approval of GPCV consent to start is pending, which is expected to happen in Oct’23. Product sold be sold post this right away.

By 2030, approx 14 agro chemicals are going to go off patent and considering the strength of RD, Shivalik is planning to work on 3-4 molecules and Rahul Bishnoi expressed confidence that future looks bright on this front as well.

Asset turnover ratio is 1:2 in agro chemical and it will be gradually ramped upto full utilization in 2-3 years time. Expecting 22-23% of margins from these.

API:

Customer whoever buys the product waits for stability data, which may take 2-3 years of time, which Shivalik has now almost crossed. Revenue from API plant will start after audit of DMF and Europe inspection which is supposed to happen max by the end of Dec’23, which provides more confidence to the potential buyer.

All other countries accept the approval of USFDA, which will really open the market. Company is currently focused on preparing for this audit.

Q & A Agro

Invested 130cr in Agro chemical plant, which will be the asset turnover ration and can you give us a ramp up plan year 1, 2, 3 ?

Normally for agro chemicals it is 1:2. Total potential is 250cr and this will be achieved gradually. 25-30% in year 1, 50-60% in year 2 and year 3 100%.

What is the revenue potential that can be generated from this plant given current and future molecules pipeline?

Peak revenue is 250cr.

What are the margins from these new Products?

EBITA currently is 13-15%, expecting more of 22-25% going forward because products are going to be new.

Any capacity bookings already done by customers?

Tied a part of revenues with a regular customer.

when does the inventory recorded in the AR gets liquidated to revenues?

. 57cr inventory will be capitalized this year from the agro plant.

New hiring of 60 ppl new hiring was done in agro plant operator sort of roles.

Q & A API

Annual report mentions about 12 molecules in R&D, out of which 1 with DMF and 4 with EDBF. Can you throw some some colour on size of these molecules, competitor landscape etc?

Products chosen based on Market size of not less that USD 1bn. Now, needs to see how much of that can be captured.

Chinese company is partnered with us for API. At what stage we are and by when we can see commercial.

Tied up on 1-2 molecules. Offered 2 molecules to a Japenese company as well. Normal period for product registration is 18-24 months which was started 6 months ago.

Normal asset turnover for APIs in 1:1.

How much will be ration of external to Medicamen?

30% material utilization with Medicamen and the rest externally.

Any capacity bookings already done by customers?

No response

Company has raised 104cr, how was the price decided?

Rates are fixed by ICTR rules and sebi norms

Overall

Any guidance on revenue and profitability for the next 1-2 years?

Min revenue will be double in the next 3 years

Thank you for putting in the effort to share the AGM highlights.

Tried to simplify using Bard

Invested

I am just sharing the views of Sajal Kapoor on Shivalik Rasayan

Please watch the timeline for 1 hour and 6 minutes.

Invested and Biased.

dr.vikas