Shivalik Rasayan Ltd

Disclosure: Invested small quantity

I searched and although Shivalik was a great wealth generator, the company doesnt seem to be discussed here. I wish to put some figures for consideration from what looks like a good value play. I have taken a small tracking quantity.

Shivalik is undergoing an expansion

For the purpose of expansion they issued preferential shares of 44 lakhs at the price of Rs.326 each which brought in a capital of Rs.143 crore

Current Shivalik market cap (after the 143 crore funds raised) is 370 crore.

If you set aside the new money raised as I assume that money is still not put to use to generate profits as yet, the remainder market cap of Shivalik is 227 crore

Shivalik as per annual report also owns 39% of Medicamen Biotech.

Medicamen is valued at 599 cr.

39% of 599 crore is 233.6 crore

Usually holding companies are traded at a discount of 30pc the assumption being if they were to sell their investments and distribute the capital it will attract a tax of roughly 30pc. So if Shivalik was only holding Medicamen and nothing else, the market cap would be roughly 163.5 crore

Deducting 163.5 crore from the 227 crore we got earlier, for the current business the market cap is 63.5 crore (Their expansion is 185 crore as you would see below but lets deduct just the new capital for now and 70% of medicamen)

The current standalone profit of 1.18cr per quarter equates to roughly 4.73 per year. This equates to a rate of 7% on 63.5 crore or a PE of 13.

Medicamen risk

Major calculations above include the value of Medicamen. If this is inflated then eventually Medicamen market cap would come down so its essential to look at Medicamen a bit to understand if we are dealing with highly inflated market cap.

11pc of Medicamen is owned by Parmadanica. Parmadanica is a subsidiary of MissionPharma.

KLAUS SNEJ JENSEN is the COO of MissionPharma as well as MissionPharma’s chief Pharmacist. Mr Klaus is also on the board of Medicamen. Mr klaus is not on the board of any other listed company so he must be working quite closely with Medicamen

MissionPharma does not manufacture any medicines as per the below excerpts from their annual report:

Missionpharma supplies generic pharmaceuticals, medical devices, medical kits and hospital equipment to countries outside the EU – primarily in Africa and Asia. Customers include ministries of health, central medical stores and public procurement agencies as well as NGOs, funders and private wholesalers. The

products are both sold in bulk and kits. Missionpharma is not a manufacturer itself whereas all products are sourced globally from manufacturers.

So looking at the “possible” value of Medicamen future sales it’s good idea to check what MissionPharma’s cost of goods/material is. As Medicamen is likely to get a slice of that pie. Missionpharma material purchases for resale in 2017 as per their annual report - converted to today’s exchange rate - is in the region of INR 440 crore.

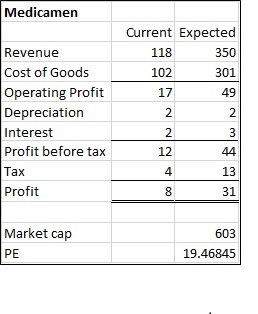

Medicamen sales is 118 crore, profit of 10 crore, pe of 57. Lets say normal pe for generics business is 20 like Cadila. So back of envelop calculation, market is expecting medicamen to have revenue of around 350cr as below

Its unlikely Medicamen will be able to procure a big part of MissionPharma’s yearly requirement of 440crore however they do have the capacity as per their 2016 annual report so depreciation is likely to remain at current level and because of MissionPharma being on board probably new generic drugs development is targeted at higher margin products. MissionPharma is growing as well and as part of a listed company they would have growth plans. I am not sure how Medicamen fits into it but I assume with board, shareholding, etc they have plans to use the underutilised Medicamen plant

Shivalik Expansion

Looking at the expansion, Shivalik initially took an approval (board,shareholders, environment,etc) for expanding their existing products. The expansion of existing products was in the region of roughly 5 times their current capacity

Expansion plans - reviewed and changed

It appears that once Shivalik management had an understanding of Medicamen business they realised that

- There is more money to be made in API intermediates

- They have almost ready market in Medicamen as Medicamen is growing and have used roughly 60+ crore of raw material last year.

- As per Annual report, India does not currently have capacity and a lot of it is imported from China

They have now changed their expansion project from old business to API intermediates business

Live date for expansion

They have received all approvals for the change of plan with an expected production commencement date of December 2019.

shivalik/medicamen intergroup sales

Medicamen cost of raw material is around 59pc. Lets say Shivalik fulfils roughly half of it. So Shivalik is looking to generate a revenue of 150 crore, which is roughly 3 times current revenue. Their last expansion plans for their old products was 5 times capacity. So 3 times probably sounds very conservative. They also said the raw materials currently have to be imported from China and their new plant is state of art which would make them more competitive. So on the expansion capital of 143 crore they will most likely make 14 crore (150 crore / 44.82 * (5.79 - 0.73) x .70 after taxes

14 crore over 143 crore is an excellent return of 10pc per annum or a pe of 10

The expansion so far has been without debt other than recently raised more capital. Their annual report says their proposed investment for new plant is shown as 185 lakhs. I am assuming this is due to oversight. No one will talk a lot on an investment of 1.85crore. They probably mean 185 crore which ties in with the recent capital raised.

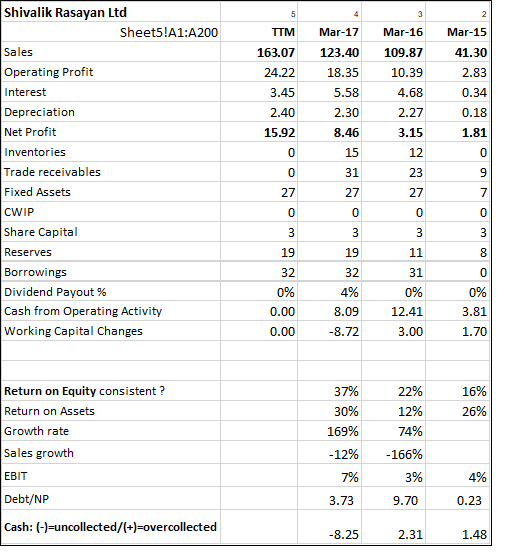

Shivalik standalone historic figures:

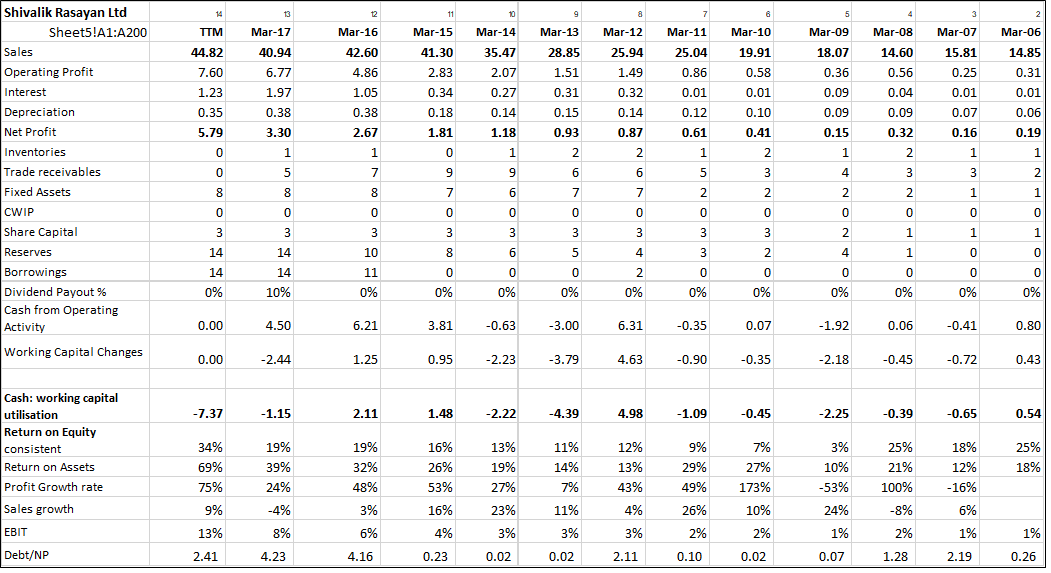

Shivalik consolidated snapshot key figures

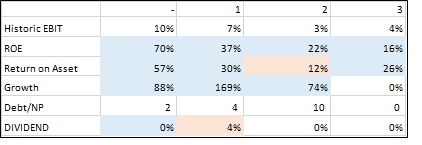

Shivalik consolidated figures