Waiting eagerly for Annual report for update on API plant. Also interest fact that Shivalik holds 39% stake in medicamen biotech which also looking to acquire company in Australia… in addition to oncology formulation plant expansion at Haridwar which will be ready this year end

Shivalik AGM Notes, 30Sept’19

Acquired Oz trading/distribution company through Medicamen, would help in entering the market there(3-5m expected revenue by next year)

Focus on upgrading the facilities to US FDA standards

Want to shift from low margin markets(Africa & ROW) to high margin ones (US,Japan, Au’s, Europe)

Targeting to file 5 DMF by Dec-2020

Oncology unit of Medicamen and 2 blocks of dahej plant are in final stages of completion, would be operational by Dec’19

First 6-9 months of operations would mostly deal with testing, getting approvals for APIs, so API revenue wouldn’t start anytime before Q4-'21

My overall view,Management seems committed and is making lot of efforts to establish themselves as a strong API player in the market. But actual impact on financials is still some time away

Great to see Shivalik holding its ground in current market conditions. Continuous Promoter buying even after 15-20% rally seen in last month also gives lot of confidence. Promoters have raised stake by around 0.35% in last couple of months

Right Puneet, API revenues are still some time away. But they are focusing also on CRAMS for APIs and also on selling APIs for lesser regulated markets. Are you tracking this company closely, any info. on the revenue potential this year for the above ones?

These are the APIs already in production by Shilpa Medicare. Why not buy Shilpa instead of Shivalik. Shilpa has entered into formulation too and has many USFDA approvals too.

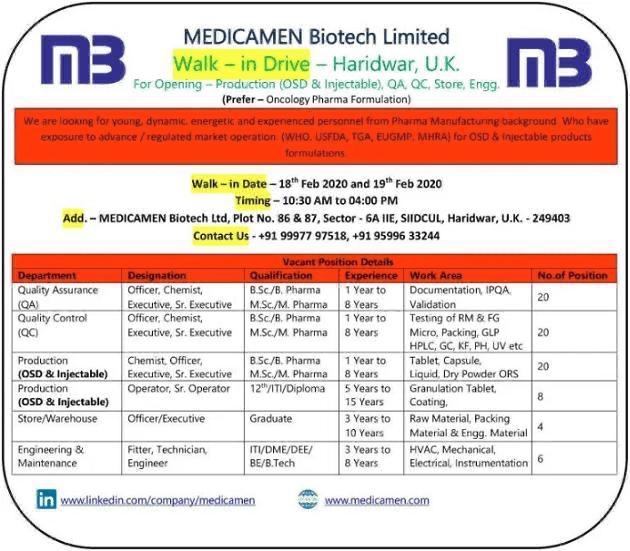

Just before the lockdown, Medicamen Biotech advertised for a large number of fresh recruitement for their new plant.

Shivalik includes Medicamen results as well as will probably supply to Medicament when its own plant is ready but for now Medicament probably will have to source raw materials

Probably the plant is live or going just live immediately after lockdown.

The Danish company that is one of the shareholders usually supplies huge quantities to WHO

I think at the moment medicamen looks more promising over the immediate future

What is the revenue potential of the oncology products the company is planning to manufacture? Medicamen has gotten the required license to manufacture products which will in turn affect Shivalik’s revenue positively. But to what extent?

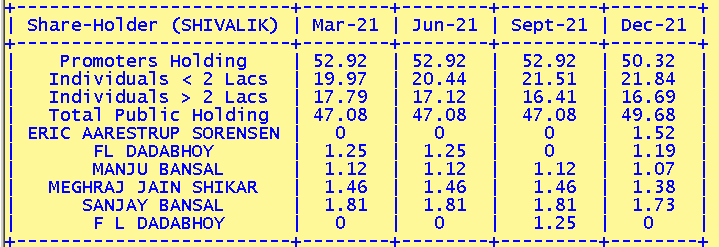

The promoter did not sell. The reduction in the percent holding is due to preferential allotment at Rs 921 to Kim Gennerup Aps, Eric Aarestrup Sorensen and others. It can be seen that the promoter Growel Remedies is also an allottee for new shares. The number of shares has increased from approx 1.38 crores to approx 1.45 crores after the allotment (1.49 crores diluted shares).