Good analysis. While it is possible, given the past track record, there has been volatility in revenue over last 5-6 years. Hence, market would look at next 3-5 quarters, to ensure that revenue is sustainable. In Past also we have spurt in revenue and profit followed with major slump which continued for 5-6 quarters. Enclosing same from Screener

Just look at Sep 2018 to June 2019 results on Sales and Net profit. Despite no major change in revenue, the net profit declined from Rs 6 Cr in March 2019 to Rs 3 Cr in June 2019. Subsequently,Revenue and Net profit crossed previous high of Rs 51 Cr in June 2019 only in December 2020 quarter,

In nutshell, I would suggest investors to look into cyclicality in the business of company and does not consider as a stable and steady compounder. It has demand volatility as well as raw material volatility. However, the current bullishness in Small cap market can definitively take valuation in different orbit which no one can project. We need to differentiate compounder from cyclical/industrial company and look in valuation over cycle when we look at investing for long period (5 years+)

Disclosure: Among my Top 6 holding. My view may be biased due to my investment. I am not SEBI Registered advisor. I am not suggesting any investment action in the company… No trade in last 6 months.

Point taken @dd1474 on sustainability of margins to take some more time given history, would you not think that annual numbers may give better performance track record, if we were to look at same the only outlier year that stands out is FY 20( reasons below). Outside this year, margins are on upward trajectory across last 11 years and these are further reflected in profit growth CAGR numbers.

Given that performance is being delivered now and market itself are in a rewarding mode, thus the current performance. These can never be compounders but not sure cyclical either, party may still go on as long as performance is good and numbers speak for itself. Key here will be to keep exit plan need to be in place.

All said mgmt still deserves the credit for good performance in toughest year in the history.( last high price was 140 and approx mkt cap of 500 cr+ in April 2019 when revenue were 193 cr with OPM 18% and net profit 25 Cr and peak debt, TTM they are at 246 cr with OPM of 20% and profit of 35 cr with negligible debt and at market cap of approx 600 cr+)

What stands out IMO is QoQ performance in Q1 22 inspite of Covid 2 impact, makes believe that time ahead may be better if it is not one off.

EV a key growth driver - both vehicles and charging stations

Smart meters initiatives & PLI schemes for consumer goods and switchgear industry as tailwinds

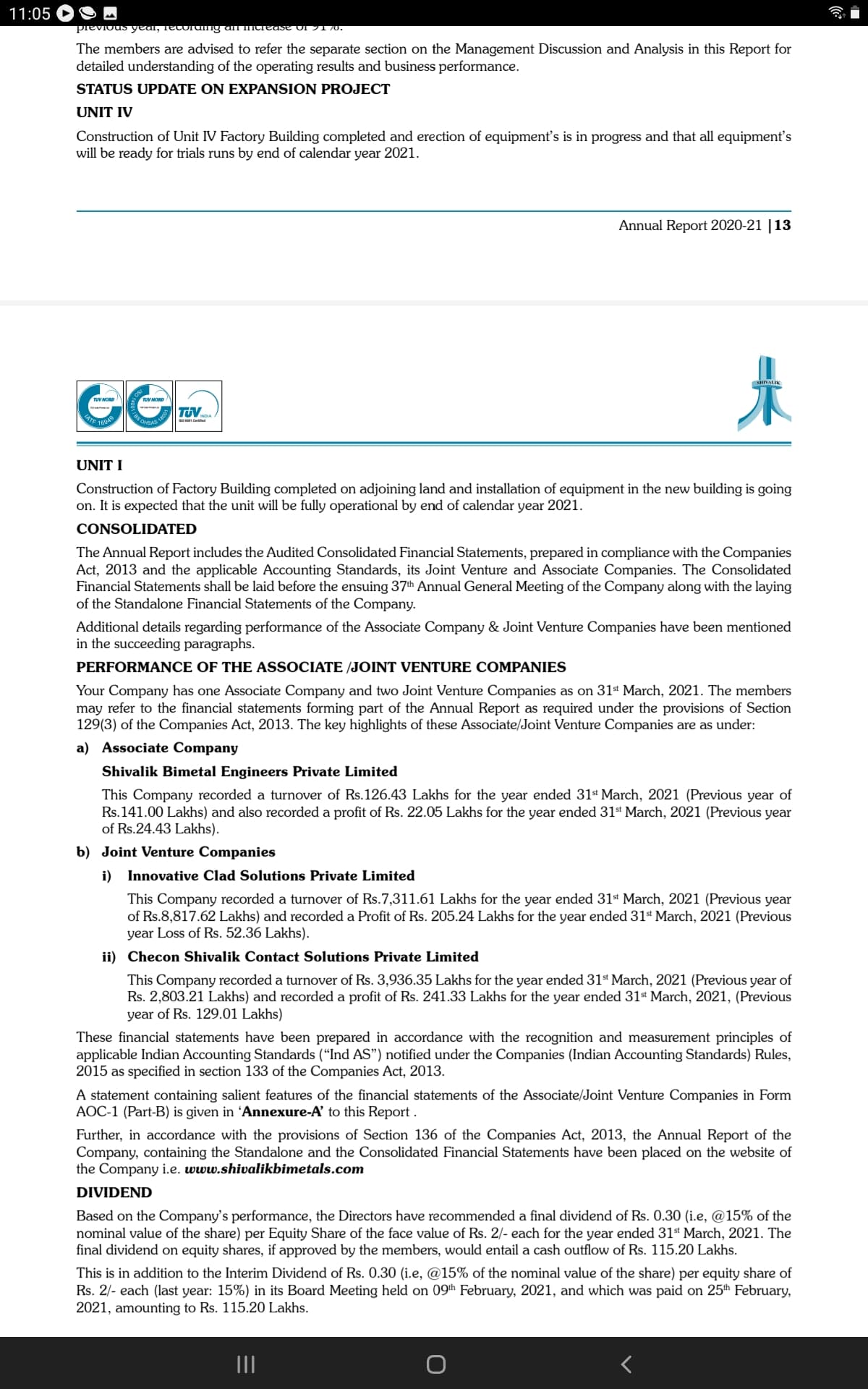

Associate and Joint ventures back to good profits YoY

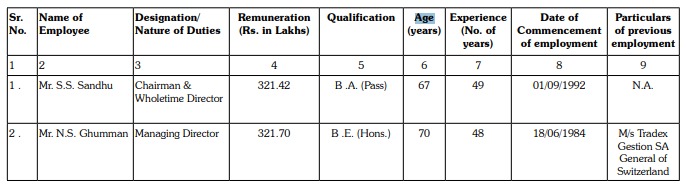

Mgmt team didn’t take hike in remuneration this year

Expansion in Unit 1 and 4 to come online by end of CY ( couldn’t gauge capacity addition in quick read through)

With growth outlook and pricing power visible ( customized solutions per customer), expanding margins and end customers industry tailwinds, Valuations attractive per post above

Stock continues to do well with sustained buying interest and strong on charts, some interesting stake increase and additions in public share holding patterns in last 2 qtrs for those holding >1% .

Came across Another interesting set of info on shivalik shipments to Vishay Dale, shunt resistors primarily, Qty/Weight much higher in recent shipments.

Hi…The Image you posted , which shows historical data ,is it available to paid subscribers only?

As I can see data for latest shipment only(in free version)

Co. does say that they produce war head assemblies and other defense products on their website. Anyone know how important this segment is to company since there is lot of buzz in the defense sector now because of heavy investments coming in from the govt. which could be a long tailwind for the company.

They assemble electronic circuits on a PCB for defence. As for as I know they have capability to build PCB and assemble it. Assuming they have PCB manufacturing & assembly capability this would not open just the opportunity on defence but also on other electronic assembly opportunities. They can assemble even mobile phone motherboards tomorrow by upgrading their infra. I feel jumping from manufacturing shunts to PCB assembly is natural for companies like Shivalik. This is upstream for them. Today we import Mobile phone motherboards from China, next level is assemble those motherboards in India. Those who have the capability would have early mover advantage. The kind of work they are doing today, shall be natural progression for tomorrow. If someone has this capability they must supply to defence as thats where import option is not there.

They make pbc which In reality are microchips

There is an ongoing worldwide shortage of microchips

Many car companies are affected

Even if they don’t make for the car industry, when companies that make car chips try to fill up the shortage, some of the work they forgo will be picked by others

I think shivalik also makes chips for car industry hence it’s been doing upper circuit in anticipation of a good quarter

The chip shortage will likely continue for a year atleast

Intel are only now building a new factory to address it and the earliest is around 2 years for that to go live !

No, Shivalik or for that matter any company in India doesn’t manufacture semiconductor chips. However every circuit that uses semiconductors needs shunts and SMD registers that Shivalik manufacture.

Has not been easy to find information about Shivalik Bimetal. Considering this, here is a titbit. The two pdf illustrates that Shivalik has been one of the four approved/recommended player for “Shunt” component in electric/energy meter spec by UPPCL(UP) and PGVCL(Guj). In fact, the only domestic player; the other three are international players.

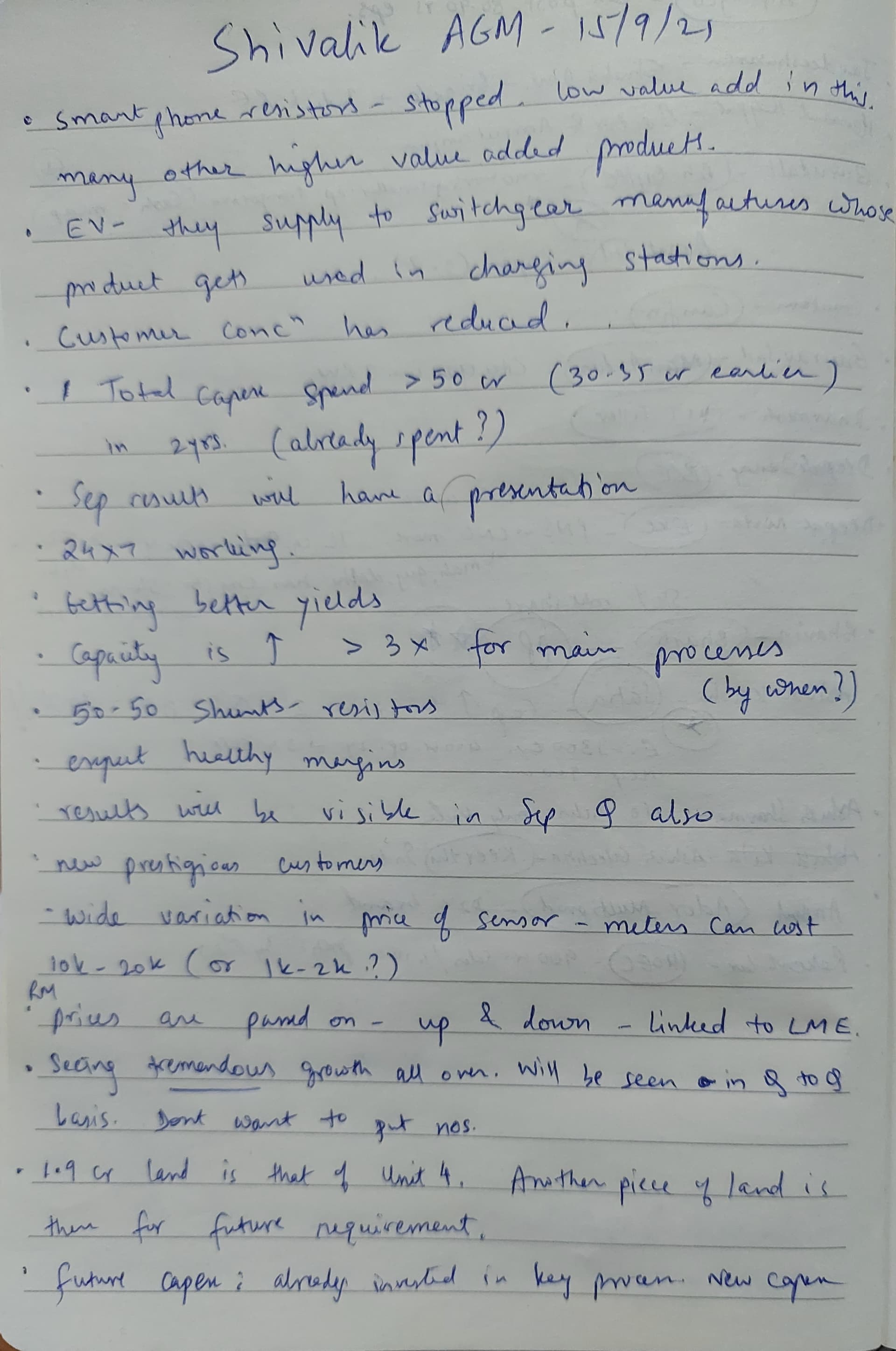

-Company is on the right track. And we are seeing good demand traction for our products.

-Have asked customers for advanced payments.

-We are no longer focusing on Smart Phone resistors as there is more demand from other value added products…which we feel have comparatively higher potential.

-Our switch gears will be used in charging stations…we supply our products to switch gear manufacturers who in turn will supply to charging stations. This has long term demand.

-Capex of roughly 50 Cr over a period of 2 years…we are close to completion. It will help us expand our capacity by 2-3X. We will not need any more capex in near term only may be few finishing equipment that too depending on the order.

-We have added prestigious customers. On the previous risk of client concentration…we have now diversified it fairly and we are in a comfortable spot.

-Overall seeing robust demand and growth in our core markets.

-Revenue split between shunt & bimetal is roughly 50-50.

-We are seeing good demand traction in our bimetal segment as well.

-Overall we should see good growth H2 onwards.

-Company is contemplating on giving an investor presentation along with Q2FY22 results.

-Automotive is around 30% of sales and meter is 18%

Shivalik Bimetals - Questions we want answered from Automotive/EV Domain Experts

Shivalik Bimetals is a supplier of low-ohmic, high precision shunts for Battery Management Systems used in EVs for Global OEMs, Smart Meters, and other application areas.

BMS for EV is our primary area of interest. We are looking to nailing down the industry structure/growth, competitive position, supply chain relationships, production capacities, supply demand inventory situation/monitoring, and the like.

Looking to source 5-6 (hands-dirty) domain experts from the Automotive EV Industry to nail down answers to questions as below:

A. Global BMS Industry for EV

Tier 1 suppliers mapping with rough market shares for - like Continental, Hella, Marquardt, Denso - supplying BMS to OEMS

Tier 2 suppliers mapping rough market shares like Vishay, Isabellen Hutte, Rohm, Panasonic, Yageo, Koa, Ohmite, SEI - supplying PCB for BMS with shunts and other passives

Tier 3 suppliers mapping rough market shares like - Isabellenhutte, vishal, Shivalik supplying the shunt/strips

Tier3-Tier2-Tier1 - Supply chain Relationships.

Entrenched relationship chains where a new supplier like Shivalik Bimetals might break in, and where it might find too difficult to break in. And why?

Above should be leading us to establishing Addressable Market for Shivalik Bimetals

Breakdown by 4 wheelers, 3 wheelers, 2 wheelers - as these might be non-overlapping markets (?), as well

B. Technology/Disruption Risks

Shunt Resistors vs Hall Effect Sensors - technology share uptake in EV BMS systems. Trends past few years, and expected going forward

Advanced manufacturing technologies in use

Any others?

C. Capacities/ Expansion plans

Rough capacities as existing today for the major players/competition identified for Shivalik Bimetals. Expansion plans, as available in public domain

D. Inventory/Supply/Demand mapping

Why/how of the last glut in 2018/19

Sources to track and be top of inventory/supply situation

Current situation - inventory de-stocking over, shortages (?)

Acceleration in demand drivers/new demand drivers in Market

Projections for 2021-2025

Please help us refine this top-of-mind wishlist of queries we need answered to nail down this opportunity properly. Please share this wishlist with your friends from Automotive EV/BMS Industry and/or invite them in to this discussion here. @desaidhwanil@ankitgupta@ayushmit - please help refine/structure the questions better so that we can extract more - should we reach the right experts this time round.

@Vpayasam@wandering@rambaranwal and other guys who might have worked on this before, let’s give this another serious go. Please don’t beat me up with the usual “Why now, Donald” - better late than never

Last but not the least - hidden automotive/EV domain professionals in VP - please wake up if you see this post (update your profile so we can catch you when needed like this) and put your hands up to sourcing the right experts to talk to

I think you have prepared the summary well. Not sure what I can add.

Few questions/observations from my side:

If we observe the financials of Shivalik or Permanent magnet, both the cos fortunes changed since they started dealing in shunts. Both cos are having very good profitability and now it’s been 5-7 years. So why has the competition not been able to come in and disrupt these?

If one looks at the nos of Shivalik - they are doing about 40-50 Cr profit now on a net block of 40 Cr! This is a highly profitable activity and should have invited competition?

Vishay talks about patents in shunt strips and sources the same from Shivalik (a small tiny co based out of Solan…and it’s tough to reach this place) Why? Why will a multi-billion dollar co take so much headache?

Can we find connections in Vishay or related cos to understand the above?

What could be the other related areas to shunts for these cos to expand into?

Can we find more about global competitors in this area and understand their financials etc?

What we understand from interaction with Permanent Magnet management is that current sensing technology is still in the evolution stage and tier 1/tier 2 suppliers and OEMs are still experimenting with which technology to use. Can we get some sense on how this technology is evolving at various supply chain levels? Have we reached a stage where a particular technology has been established as the best one to use for current sensing?

The qualification process for the shunt suppliers seems to be very vigorous and it takes years to penetrate into a particular customer and model. Can you please elaborate a bit on the qualification process?

Shivalik is forward integrating from shunt strip manufacturer to shunt resistor manufacturer while Permanent Magnets has plan to forward integrate into module manufacturer. How easy/difficult is to forward integrate in these industry?

Apart from EVs, smart meter opportunity also seems to be big for shunt manufacturing companies. Can you throw some light on these opportunities?

Very well articulated questions. If we can get answers for these it would be pretty clear. However as EV in itself is in diapers I feel it would keep evolving.

I have following inputs to some of the above questions

We need to treat Shivalik as a technology company where capacity is not the only criteria but capability plays key role. Capability in terms of value adding to bi metals to create electronic components such as shunts or bimetal coils for switch gears,

*This value add requires lot of technical experience and skills.

We can treat these skills much more difficult to attain than software skills for example, as we have less of these in India Vs software.

The Semiconductor fabs are also converting Silicon/Germanium to electronic circuits and shunt manufacturing requires technical skills to convert bimetals into parts with required electrical properties.

After manufacturing, need to optimize yields and avoid wastage to achieve high Gross margins.

The Qualification for auto grade is a niche skill as they need to validate parts not just for electrical properties but also it’s reliability and its 10-15 years reliable operation.

I would like to add below questions if we can get answers from market experts or management it would clarify the dynamics of this business

*What kind of current sensing technology big EV players like Tesla are using?

*Is current sensing shunt nos per BMS system are increasing ?

*Skilled Labour cost differences in Europe/US Vs India for shunt manufacturing Industries.

*Is there any forward integration being planned by Shivalik for BMS manufacturing ? They have the capability as they used to manufacture PCBs for defence earlier.

*Where are we on samples sent to OEMs some time back by Shivalik to Global Automotive OEMs.

As they are exiting Mobile phone market due to low margin, looks like they are overloaded by high margin business of EV OEMs.

Disclosure: Invested

Q2 22 - good performance continues( good QoQ, multifold YoY, management came up with presentation for first time,

At annualized Q 2 they will do at 300-325cr revenue, EBDITA is around 25%, one of very few companies with QoQ margin expansion, evidence of pricing power and tail winds, there is sizable capacity addition coming online from Q3, available at 3X sales and 15x EBDITA. This is not considering CWIP.

Only challenge seems to be on cash flow front, seems the case for pretty much most of companies.