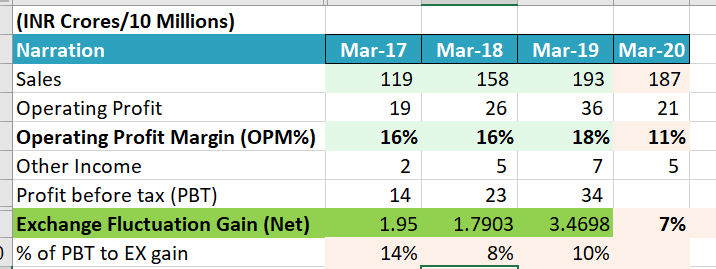

yes why not without hedge you can also book fe gain/loss.

for fair valuation, o/s foreign currency receiable/ payable needs to reinstate to month end or balance sheet date closing rate.

There is a new corporate video posted on YouTube a couple of days back which might be useful here to this discussion.

They also make a mention of two joint ventures with foreign partners namely Checon Shivalik contact solutions and Innovative Clad solutions pvt. ltd. They also mention their customers to whom they supply.

There were no salary cuts in the company. Even during shutdown and slowdown period we paid full salary all across the company.

We have not finalized any future capex as the current capex is delayed due to coivd.

The capex plan on land adjacent to the current plant is delayed by 3 months. 1st slab was laid a day before AGM 2020.

Intend to use GOI scheme on manufacturing and waiting for GOI approval expect to get same in October.

We expect to reach pre-covid levels of operations from October. Gradually many customers are already back to the pre-covid levels.

Expect a good H2FY21.

We have 90% market share in domestic shunts industry.

Globally, 70% of our exports are direct to end customers and only 30% through channel partners. On the domestic entire 100% sales is to direct customers.

Mr Ghumman spends 95% of his time on new product developments

In the last 3 years 30% of revenue came from new products.

In bimetal segment we are ran at 80% utilization and with the new capex the capacity will be more than 3x in new plant.

In Shunt we are the largest in world in electro welding under single location.

Innovative JV was focusing on export market. But, US customs issue affected this entity’s performance.

Our key client for shunts is getting back to normal and off-take from them is expected to be good.

We expect a new set of products to be dispatched from next year.

There is good traction in auto sector i.e… electric vehicles the segment we cater to.

May have missed some other points as the quality of connection was poor and interaction was interrupted. Personally - the big positive for me was the validation and positive undertone of the management around the large customer and scale up on new relationships which they have been seeding for last few years going forward. Given the low market cap and potential, it remains interesting to my mind.

Concern remains the way management wants to remain low profile and not open up or adopt modern practices of interaction with investors/shareholders. Few other issues like high salary remain.

Disc: Invested in family accounts and clients in PMS.

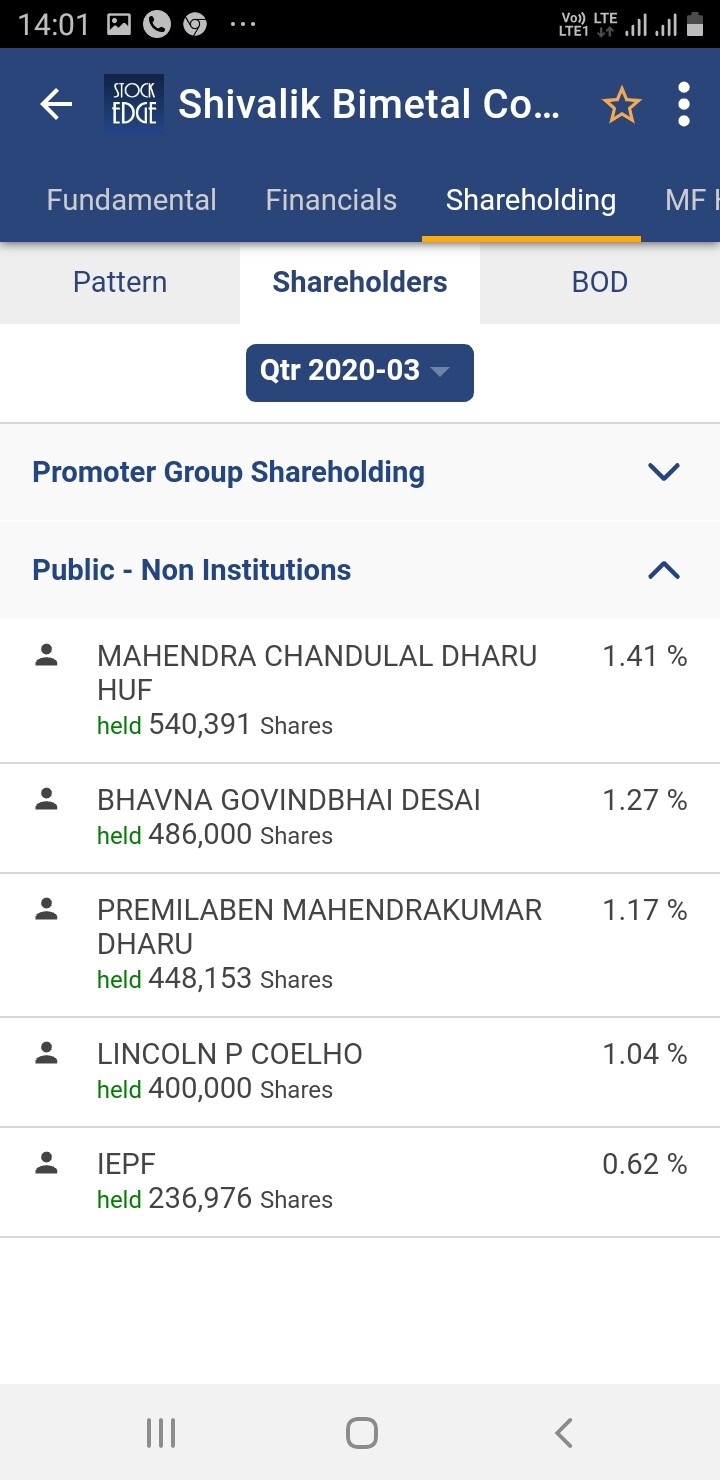

Continuous buying since last three quarters from dharu family…

Is there any update regarding adjacent plant which is supposed to be commissioned during last quarter.

There has been interesting developments on manufacturing front recently as Govt launched PLI scheme for various industries. Overall value add by PLI scheme would add value of 1.7% of GDP by 2027.Mobile phone manufacturing gets biggest share but if we see other industries Auto, Battery and Telecom would also enable huge Electronics Manufacturing in India. Please see below chart.

As per IT Minister Electronics and Smartphone Manufacturing alone would contribute $1 Trillion by 2025.

Electronic and smartphone manufacturing alone will contribute $ 1 trillion by 2025: Union Minister Ravi Shankar Prasad

Our existing Electronic Manufacturers are grabbing this opportunity with open hands and would grow manifold going forward.

Dixon forays into ICT hardware; set to open factory in southern India

This push in electronics manufacturing would open full scale electronic manufacturing ecosystem which doesn’t exist in India as of now. All the Mobile manufacturing units in India are currently more of assembly lines than downstream electronics component manufacturing and assembly. This is mainly due to lack of electronic component manufacturing ecosystem currently. As per above snapshot in Economic times recently these manufacturers are also looking for local value add rather than just assembly. This shall evolve a new area for growth in ELECTRONIC COMPONENT MANUFACTURING going forward. The full ecosystem requires Semiconductor Component Manufacturing along with PCB manufacturing and assembly. PCB is bare motherboard in lay man language where electronic components are soldered together to build required circuit aka hardware. Any electronics PCB has semiconductor chip, registers and capacitors as main building blocks. This is true not just mobiles but also for laptops, Auto electronic controls, battery management systems etc.

Out of all the above building blocks manufacturing semiconductor chips is capital intensive and required huge investment. Next stage of electronics manufacturing that unfolds after current assembly lines is component manufacturing eco system to do downstream value addition. Looking at this opportunity Govt of India is already inviting expression of interest from interested parties to build semiconductor chip manufacturing fab in India.

India’s Big Push For Small Chips: Union Government Invites Companies To Submit EoI By Jan 21 For Setting up Semiconductor Fabrication (FAB) Plants In India

While semiconductor FABs would take time to build we already have fragmented PCB manufacturing factories and register and capacitor manufacturers in India, some of which would grab this opportunity to scale and improve their capability to support in building this eco system.

Shivalik manufactures, shunts, SMD registers along with some capacity to manufacture PCBs for defense.

Their Shunt and SMD register quality is world class and auto grade. The capability required to manufacture consumer grade components is much less than auto grade. I am sure they would be part of this opportunity looking at their relationship with top quality conscious customers they supply already.

Only thing we need is management to grab this and they are just a tiny fish in big opportunity ocean.

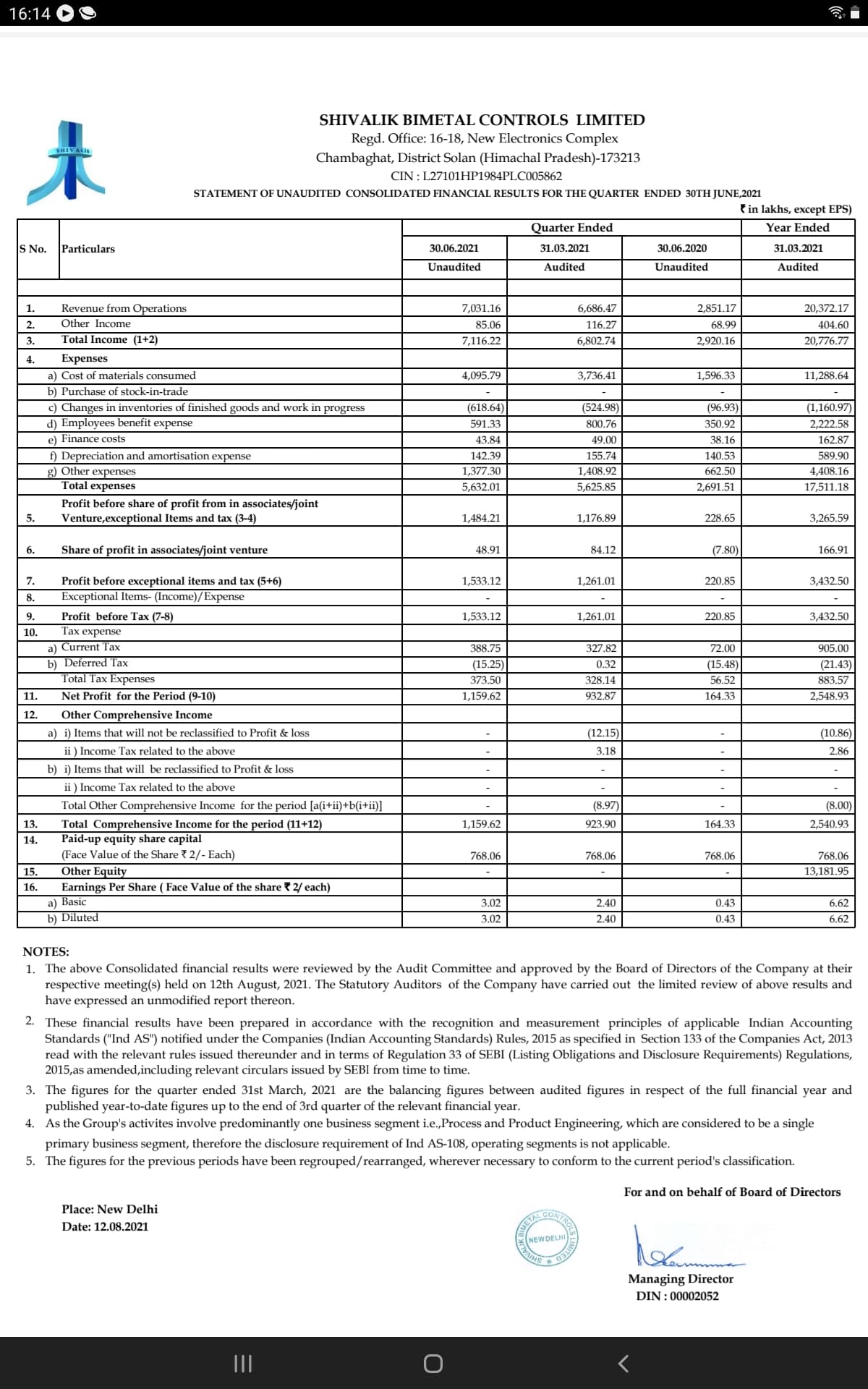

Qtrly EPS at 2.4 with YoY topline growth of 30%( 44 cr to 59cr) and profit over 125%(4.1cr to 9.1cr), QoQ numbers impressive too

9mo EPS at 4.2 - profit at 16cr+

9Mo finance cost have halved, (2.3 cr to 1.1 cr)

Dividend declared as well

Annualized can do eps in vicinity of 6.5 -7… PAT around 24-26 Cr - current market cap is 280Cr

ATH for stock was in Apr 2019 with price of 140 with annual profit at 23 Cr in year ending Mar 19( highest yearly profit till date) - likely to end this year there about or slightly better profitability and much leaner balance sheet, better operating margins, low interest cost scenario

I personally feel that this article has used semiconductor as a loose term…and it also covers passive components…as they have given example of usage in auto & home appliances. So, last time when we had such a shortage in semiconductors & passive components…we saw 2-3 Qtrs of good numbers & margins in Shivalik…can this Qtr be on the back of a similar scenario…?

PS- Above assumption is more of a thought experiment and may be other senior members and industry experts can guide us if we are on the right track or not.

Being one of the few manufacturers of bimetal parts and shunt resistors in India, SBCL faces limited competition. The company caters to a broad spectrum of applications, including switchgears, energy meters, and electrical applications, and automotive and electronic devices. Thus, growth remains correlated with the performance of the electrical, electronics, and automotive industries.

With metals such as nickel and copper forming around 50% of overall cost, operating margin remains susceptible to volatility in commodity prices. Though metal prices may continue to fluctuate, this risk is mitigated by order-backed processing undertaken by SBCL on highly customised products .

Gross current assets stood at 168 days as on March 31, 2020, because of sizeable inventory and large receivables. Raw materials inventory of around 120 days is maintained as procurement is imported, and includes a variety of alloys.

Net cash accrual, estimated at Rs 24.9-30.5 crore in fiscal 2021 and expected around similar levels in fiscal 2022 should comfortably cover maturing debt of Rs 1.78-4.77 crore and the surplus will support liquidity.

‘Pursuant to Regulation 30 of the SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015 (‘the Regulations’), we would like to inform you that the Company has received an approval for listing of equity shares of the Company on the NSE. The Equity Shares of the Company shall be listed and admitted to dealings on the NSE w.e.f. 24th June, 2021.’

Shivalik’s largest client, Vishay Dale seems to be doing quite well. Some insights from Vishay Dale’s May 21 Update:

• Total order book to bill increased to 1.67 vs 1.44 sequentially, with total backlog extending to 6.8 months (2x above historical average of ~3 months).

• Current demand environment is best in 40-year career on account of overwhelming book-to-bills and historically low distribution inventory.

• Strength seen across the business with each product category and end market performing well but constrained by manufacturing capacity.

• The core theme of electrification has a long runway for growth - auto accounts for 34% of business; the content per vehicle for Vishay Dale should increase from $200/vehicle to $700/vehicle.

• Improving mix and volume is driving gross margin expansion with additional room to expand as the demand momentum continues.

• Multiple capacity expansion projects are ongoing with an incremental $400-$500M planned to be online by the end of CY22.

Can someone please help me understand the key growth drivers for Shivalik going forward. Especially in context of the valuation at current market price of Rs.127 odd…thanks!

The semiconductor shortage is hitting developed and developing markets. This is going to add to the bottom line in the short term in all alied products. Indian context to be found in the Page 28 of the magazine https://lnkd.in/dkvuASB

70 cr revenue, 11.6 cr PAT, 3.02 EPS. Annualized can do 280 to 300 cr revenue, 45-50cr PAT, current mkt cap is 640 cr I.e. a PE ratio of 13. IMO deserves a further rerating likely with 23+PE as median for last five years period, last 4 quarters there is consistency in performance improvement - mkt typically rewards it well

Q4 to Q1 employee expenses down from 8 cr to 6 cr, need to understand on it, best guess would be some year end payout, typically emp cost has been around 10% and higher utilization will help with op leverage.

Overall resilience visible, market knew and reflected in stock price movement. pricing power visible as company operates in a niche with customized orders for clients, and has been able to deliver superior profits in the current situations of very high commodity ( metal etc) cost.