This is behind Pay wall. It is better you list out salient points if it is not infringing on the copyright issues. If there are copyright issues , then posting the link is not advisable.

3 Likes

Details about EV Plans at Global stage

5 Likes

What is the head winds in this stock

1 Like

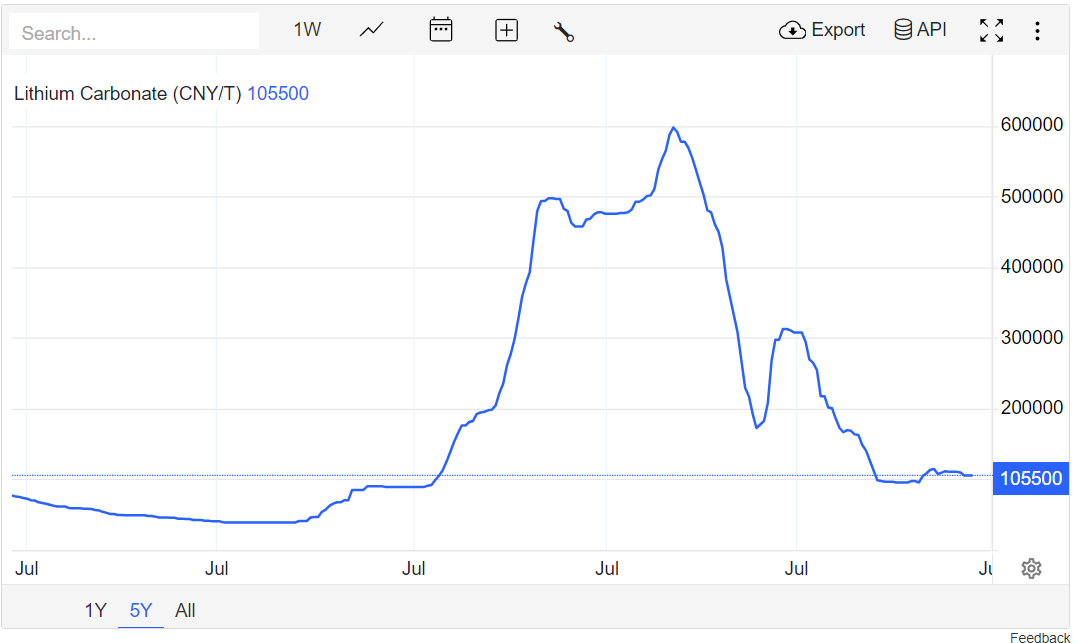

US recently announced heavy duties to be imposed on Chinese imports into US viz . EV batteries, cars, solar cells, aluminium among others . With these duties the export to US will be impacted so the next big market for chinese to dump the extra production will be india .

EV and batteries uses shunts, so if cheap producta from china are getting flooded into the market than domestic demand for shunts will be affected unless India also announces similar duties like US or YS lifts these duties, both look unlikely at the moment. This is one of the main reasons i think SBCL is see a price correction

Shivalik has had a tremendous run and the long term prospects look good, not to forget that shunts are also used in electric meters and many cities are looking to adapt these smart meters

Disc : not sebi registered . Not a buy/sell recommendation

8 Likes

I think when Elon Musk went to China Before India , he was intimidated by Chinese since 40% of raw Material to Built Tesla batteries comes from China. If Tesla Moves Production to India His Cars will be more competitive with Chinese Car makers . In Response US Govt Imposed tariffs and EU is in process to do so.

Now Tesla coming to India would have been great trigger for companies like Shivalik Bimetal.

Alas ! now it might hurt from opposite end as you mentioned about Chinese dumping their product elsewhere where Shivalik might be a supplier. Indian EV market is still in nascent stage.

Only after New Govt is formed and we start commercial mining of Lithium , we might have a shot.

Just sharing my thoughts might be wrong

10 Likes

Disc: invested

As a long-term investor, I see significant potential in SBCL providing impressive returns. However, the substantial increase in “other income” raises some questions. I haven’t come across any news regarding the sale of large assets that could justify this unusually high figure. When examining the revenue, it appears to be flat. This might be due to a typical yearly cycle, but as I am still in the process of understanding the company’s patterns, this warrants further investigation.

Additionally, the 8% increase in expenses is concerning. A notable rise in raw material costs could be a contributing factor, possibly due to a surge in copper prices or other similar inputs. Given these factors, the flat sales figures are somewhat disconcerting.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/e9fd5a10-97eb-492b-a84e-c3dd95fcbe63.pdf

1 Like

I dont see any negative in this type of other income which is related to PLI which will help SBCL to invest more and expand. these type of PLI incomes usually realised in Q4.

1 Like

Why is the comapny doing CAPEX in electrical contacts if the space is highly competitive and even after CAPEX they will get a maximum 14% EBIDTA margin as mentioned in Q3FY24 concall

Yesterday the promoter group “TSL Holdings Private Limited” bought 4800 shares as per the BSE disclosure:

This increases their holding by 0.01% from 5.85% to 5.86%. However, the same promoter group sold their stake during last August, on 07/08/2023, which reduced their stake from 14.53% to 5.85%. Essentially they sold 8.68% of their stake and now they bought 0.01% stake.

As an investor this makes me very uncomfortable. How do you interpret this?

Disclosure: Invested.

2 Likes

on 4th June, they further bought 4000 shares from the open market

the promoters also sold millions of shares few months back ![]()

Was it open market or block deal? I think FIIs bought and some of the names in public holding. how can we see that data?

https://www.screener.in/company/SBCL/#shareholding

Jun 23: Promoters: 60.60%, FII: 0.46% Public: 38.77%

Mar 24: Promoters: 51.13%,FII: 3.26% Public: 43.70%

Maybe this dilution helps in increasing floating shares, however, 0.01% increase makes me worried about possible future dilution if any when revenue is flat for past 6 quarters.

Disclosure: Invested.

5 Likes

7 Likes

Been reading up on the company. Lot of strengths and I think the medium term prospects look exceptionally strong. Near term may vary on how EVs pick up.

My key doubts from a long-term standpoint are:

-

Is there a threat to their business from alternate technology or design – Forum had a discussion on Hall effect sensors. I also came across a thread on twitter raising concerns around long term prospects for bimetals

x.com -

Is there a threat of more competition in the longer term (from Chinese suppliers or backward integration of biggies). I feel “this is too small” for someone to bother isn’t a good enough moat pointer. That in itself means that the market or size of the company cannot be large enough.

Great company and prospects but trying to find satisfactory answers on these two longer term concerns.

5 Likes

Poor results. I am not actively following this so I’m not sure if this was expected.

- Revenue - Down 4% YoY

- PAT and EPS - Down 19% YoY

Not the numbers expected for a company trading at 40 PE. Also, they had given a guidance of 1600 Cr by 2028-29 which now looks too aggressive

2 Likes

If you listen their last 2 con calls they cleared informed that 2025 is very nominal growth or slow growth, we can expect good numbers from 2026 onwards

6 Likes

CFO, Mr. Rajeev Ranjan added:

"Our financial performance in Q1FY25 demonstrates the robustness of our business model

amidst a challenging market environment. Despite a 5.18% decrease in total income to ₹107.22

Crore, our strategic focus on volume growth yielded an 8.58% increase in product volumes,

underscoring the resilient demand for our products. This growth is a testament to our market

positioning and the effectiveness of our expansion strategies in Europe, Asia, and India.

The decline in profitability, with PBT falling by 18.75% to ₹21.75 Crore and PAT reducing by

19.41% to ₹16.30 Crore, reflects the impact of increased COGS also affecting our margins.

Looking forward, we are enhancing our R&D capabilities and operational efficiencies,

positioning us for long-term growth. We are implementing manufacturing cost management to

improve our margins.

Looking to the future, our market diversification strategy is yielding positive results, particularly

in the European market, where shunt resistor sales improved by 134.40% off a modest base.

This growth, along with significant gains in Asia, demonstrates our ability to capture highgrowth segments and adapt to regional market dynamics. While sales in the Americas faced

challenges, we are optimistic about a gradual recovery as the EV market stabilises and demand

picks up.”

6 Likes