https://www.qulectra.com/industries

A simple explainer on applications of a Current Sensing Module.

https://www.qulectra.com/industries

A simple explainer on applications of a Current Sensing Module.

Good Article on the company and its future prospects.

Moneycontrol are too late to discover it, it’s trading at high valuations, most of the future gains are already factored in.

Pl don’t take offence but if you trust the judgement of Trendyline you will never be able to catch a multibagger.

I have monitored some of my portfolio stocks including Shivalik Bimetal over last 2 years. It was always shown as an expensive star after it crossed 150 levels(pre bonus price).

So pl be informed about the value of these platforms. Their data is very quantitative and lacks quality of analysis which only a human mind can do.

Disc: Invested

Some of the largest traditional automakers are experiencing electric vehicle growing pains and pulling back on production.

Why it matters: Consumer demand is falling behind lofty projections drummed up by manufacturers and other car-industry stalwarts.

https://www.axios.com/2024/01/19/ev-cars-ford-lightning-gm-chevy-blazer-cuts

Couple of questions:

May be I missed in the thread, but is there any thing which stops SBCL to provide its Shunt Resistor to 2W EV? across the thread could only find mention of 4W EV (per vehicle volume high) nothing on 2W (base volume is high). if nothing stops its, do we have a sense where its with the likes of EV OEMs like Ola, Ather, Bajaj etc?

Additionally, read in the thread that SBCL got PLI first stage approval, so does it mean that if it does end up getting the final PLI approval, then more capex may happen?

For Smart Meters, say Made in China is not promoted in India (for purely technical reason for Smart Meters can be controlled remotely and can affect power grids), how will it be possible for SBCL will be to provide shunt resistors and relay/contact material for smart meter opportunities in non-Indian markets (unless its driven by political alignments between Indian and other countries) ?

While they have explained why they maintain 4 months of inventory (1 month each across shipping, custom, manufacturing, inventory/FG) the actual inventory days are trending more in the 6-8 months, why would that be?

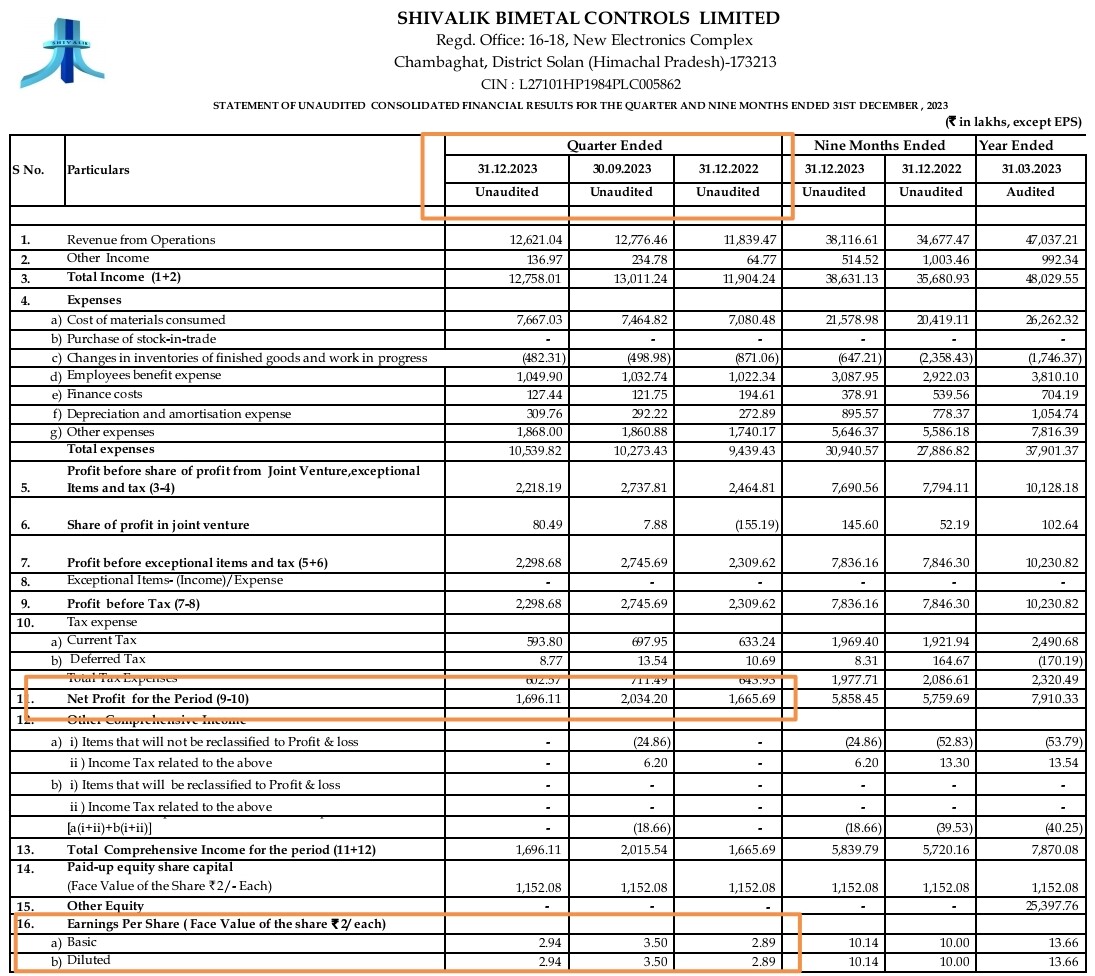

Results are out. Big YoY and QoQ drop. This will correct further I think

Please check consolidated numbers, YoY bottom line is actually up!

QoQ material costs have gone up, seems biggest contributor to lower PAT, together with slight decline in sales. Also ‘other income’ decreased.

Disc: invested, smallest holding

Valuations wise the flat profit and single digit revenue growth is pretty bad optically.

Was this as per expectation or came out of the blue?

Looking at stock price action for last few weeks, I would guess market has seen it coming. Now concall commentary would be important.

If I remember correctly, during Q2 concall, the Management did indicate next 2 quarters (not sure 1 or 2) would be muted and these results surely do appear on the expected lines.

True… earnings expected to pick up from q1-25

During concall, promoters have clarified that no further stake sale is planned in near future. This should take away investor concerns

SBCL_Q3_Conncall Highlights (Source :Screener Notes)

• Q3 FY24 total income increased by 4.31% to Rs.112.17 crore

• EBITDA for nine months rose by 4.74% to Rs.81.03 crore

• Profit after tax improved by 3.56% to Rs.55.64 crore

• Declared an interim dividend of 35%, Rs.0.70 per equity share

• Significant growth in Thermostatic, Bimetal, Trimetal segments in Q3 and nine months FY24

• Positioning well in Asia region for global electrification landscape

• Challenges in America, particularly in Shunt Register category

• Shunt sales split: 65-70% automotive, 13-14% energy meters, 8% energy storage

• Confident in ability to navigate market dynamics and deliver value with solid cash position of Rs.25 crore

• Working on business plans and feasibility study for Metalor MOU for Bimetal JV

• Contact business EBITDA margin at 11-12%, expected to improve with new plant and higher volumes

• Capacity utilization for Shunt and Bimetal at 35-38%

• Bimetal gross margin: 44-46%, Shunt gross margin: 48-52%

• EBITDA margin for both products combined in the range of 22-26%

Hi Friends,

I see promoters remuneration is in higher side compared to other big companies

Does this is normal,please educate me…Thank you

Any indications when will growth start again?

Shivalik Bimetal Controls -

Q3 FY 24 results and concall highlights -

Revenues - 112 vs 108 cr ( up 4.3 pc )

EBITDA - 24 vs 28 cr ( margins @ 22 vs 26 pc )

PAT - 16 vs 18 cr

Company has 03 manufacturing capacities - all three located at Solan ( HP )

Plant - 1 - makes Shunt resistors using Electron Beam Welding technique ( difficult to master ). Shunt resistors are used to measure and regulate the flow of current in an electrical circuit. Find application in - EVs, smart meters, energy storage, power storage modules. Peak sales potential of this plant @ 700 cr

Plant -2 - makes Bimetal strips. Metals are joined post heating, taking advantage of their different coefficients of expansion as they respond to heating. Post bonding finishing is also done in-house. These are critical components used in overload protection devices. Find applications in - Switchgears, Medical devices, electrical appliances etc. Peak sales potential of this plant @ 600 cr

Plant -3 - makes electrical contacts. Contact materials used in such components are alloys of precious metals joined on to copper or copper alloys. These are the critical connecting points when a switch is turned on/off. Find applications in - smart meters, switchgears, wires and accessories etc. Peak sales potential of this plant @ 300 cr

Segment wise revenues -

Shunts - 51 vs 57 cr ( 50 pc of this is from the EV segment applications, around 20 pc from smart meters applications , 10 pc from energy storage applications and rest from Misc applications )

Bimetals ( includes electrical contacts ) - 61 vs 50 cr ( 65 pc from switch gears and circuit breaker applications, 15 pc from electrical appliances, 10 pc into metering apps and rest from misc applications )

Avg value of Shunts per EV varies from as low as Rs 20-30 to as high as Rs 2000 per EV , basically depending on EV to EV

Expect North American mkts for Shunt Resistors to start picking up from second half of this CY as the over stocking / inventory problems are likely to be behind by then

Smart meters demand from GoI’s initiatives is definitely an exiting opportunity. Company sees good demand from these initiatives going fwd

Company is in the process of forming a JV with Metalor Technologies. Metalor is the global leader in Bimetals and Contacts business. Exact modalities of the JV are yet to be formalised. Due diligence in progress

New facility for making Silver contacts is under construction ( 10 Km from Solan - towards Shimla ). This plant should be functional in next 4-5 months. Peak revenue potential of this plant should be around 250 cr

Base growth for next FY should be > 10 pc. However, if the EV mkt in US revives, this growth can be as high as 30 pc. Actually, all the company’s product segments are growing @ rates > 20 pc except the Shunt resistors for EVs due to the over-stocking and slowdown in North American EV mkts

Company’s revenue per smart meter should be aprox Rs 60-70 ( including both shunts and contacts )

Promoter do not have plans for further stake sale in the company

Present EBITDA margins for the contact business are around 11 pc. With new plant going on stream, margins should improve. Aiming at 1-2 pc margin expansion

EBITDA margins in the Shunts business are double or more vs the contacts business

Disc: holding, biased, not SEBI registered

Q3FY24 update from Dalal & Broacha.

Shivalik Bimetals_Q3FY24_Dalal&Broacha.pdf (481.7 KB)

Disc: Invested