My understandign was that they have always said that material costs are passed on to the customer. Thus this seems a bit odd.

1 Like

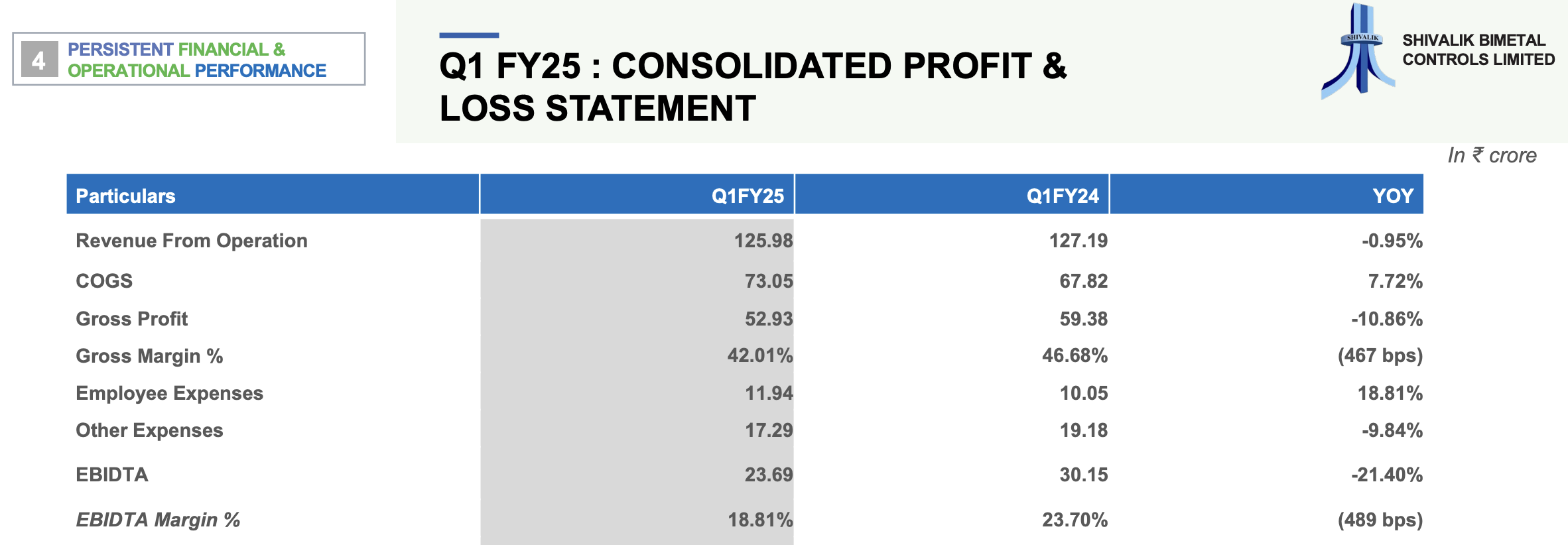

The CFO says, “Despite a 5.18% decrease in total income to ₹107.22 Crore, our strategic focus on volume growth yielded an 8.58% increase in product volumes, underscoring the resilient demand for our products.”

This is a dumb statement! It’s like saying “I made less money, but on the other hand I am proud I sold more quantity”. Well, as even a fourth grader will tell you, if you reduce prices you will sell more! It is not “…underscoring resilient demand for our products”.

An decrease in Income of 5.18% against a volume growth of 8.58% means a price drop of 12.7% per unit volume, in an inflationary environment.

17 Likes

Promoters really pumped up expectations with a long term guidance and then did a block deal in Q2FY24 and sold down stake.

A cautionary tale for everyone, “Dont trust the promoters when they spin stories especially when they want to sell their own stake”

10 Likes

Also puzzling is the fact that they say margin is hit due to increase in raw material costs. In the face of increase in raw material costs they had to reduce finished goods prices.

3 Likes

COGS has gone up by 7%!

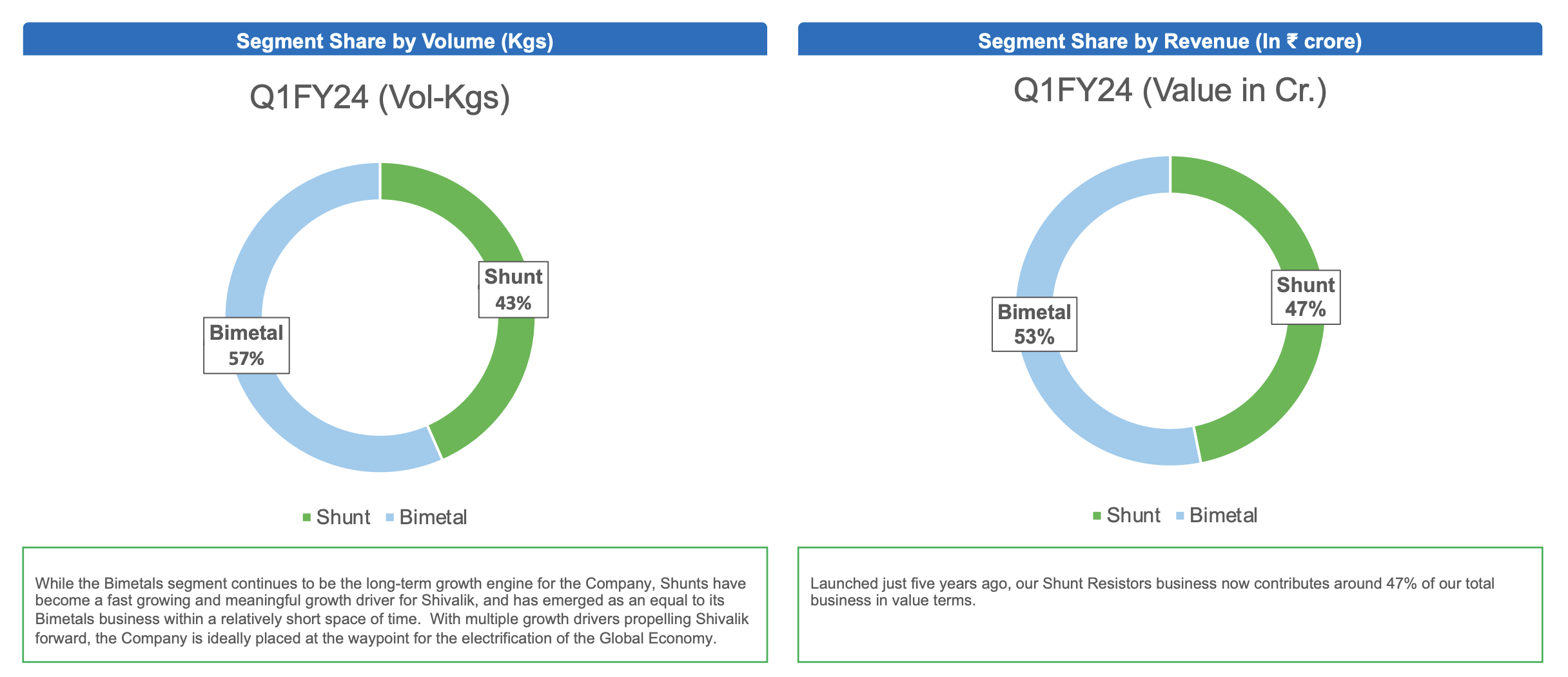

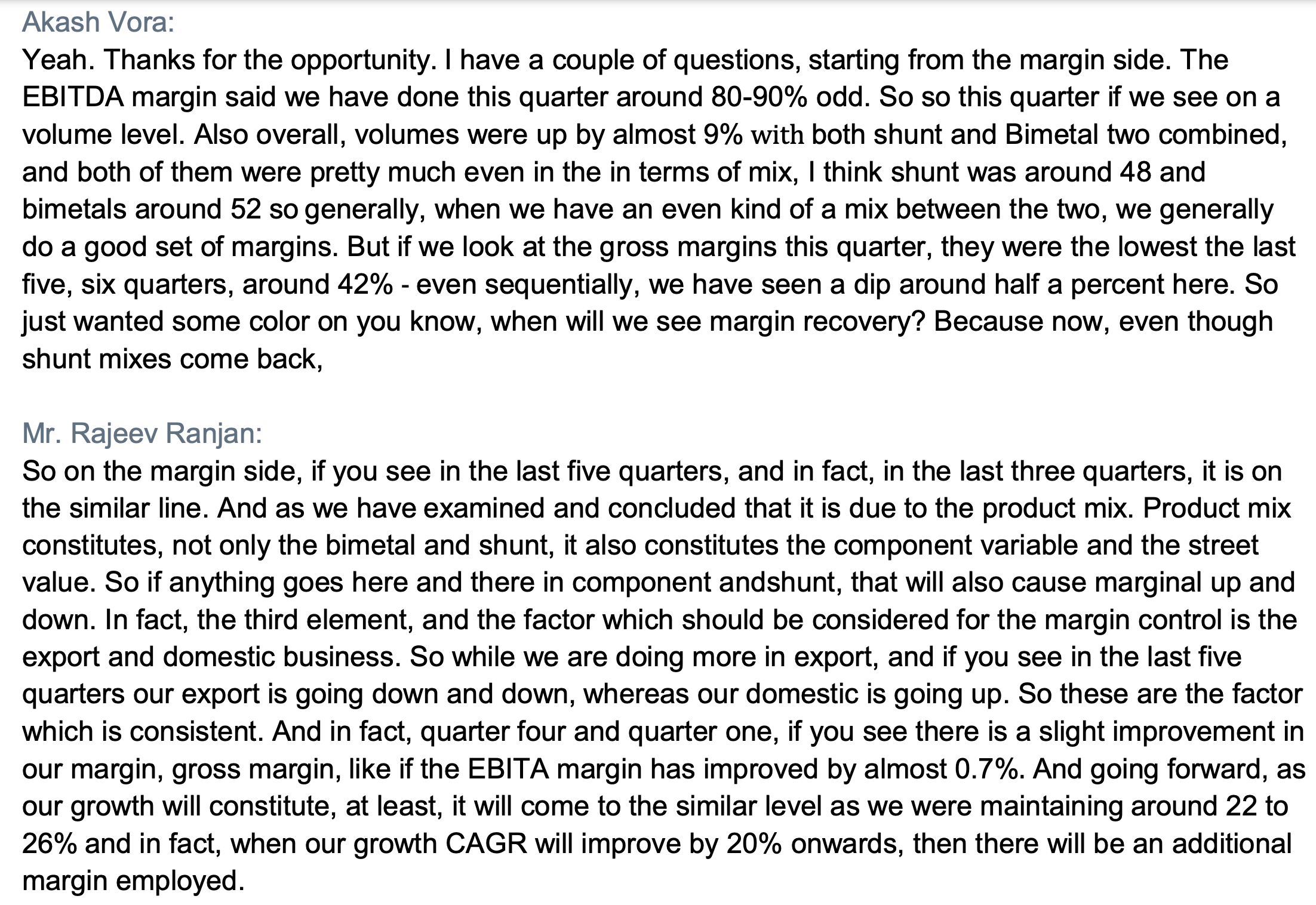

Rather I think this result has to do with the change in product mix. Look at the volume and value for the 2 segments in Q1FY24 and Q1FY25. A drop in volume of 5% (57% to 52%) has resulted in drop in value of 2% (53% to 51%). This indicates bimetals is a higher margin division and change in product mix is affecting the margins. Can this be the right conclusion (Bimetal having higher margin than Shunts)? It would be great if this is corroborated elsewhere.

In any case, looking forward to the concall for management insights beyond this press release commentary.

8 Likes

The law of lower price => higher volumes has nothing to do with product mix. And if I get paid less while I sold more (whether 1 product or a basket); price / unit (single or blended) was reduced. That cannot happen if demand was “resilient”.

If share of one of the two reduces from 57% to 52%, it does not mean volume has dropped by 5%. Volumes could also have gone up, and the volume for the other went up faster. Similarly drop in share of value is not drop in value.

Revenues / Volumes do indicate nothing about margins. So you cannot conclude the above.

5 Likes

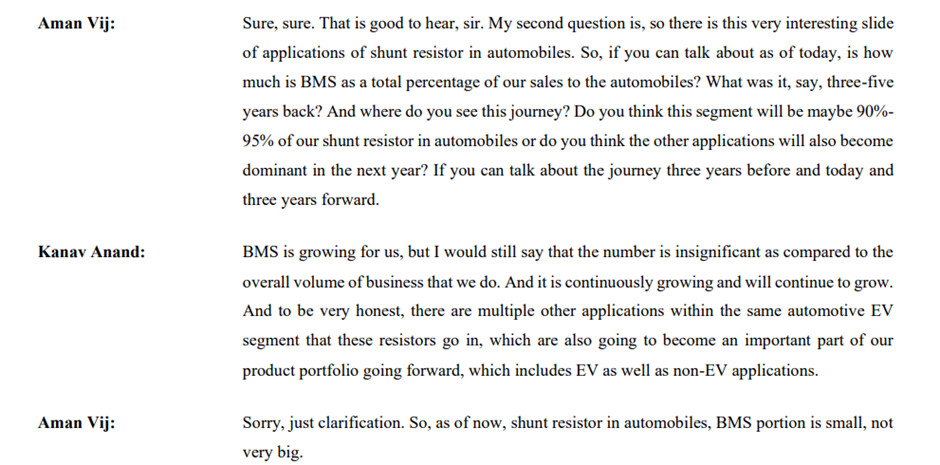

A quick question here: company in some of the earlier calls had mentioned that Shunts revenue coming from BMS applications is quite small (from Mar-23 call) but since then some of the posts had mentioned that BMS’s contribution within shunts revenue is quite high. any one can please clarify this anamoly?

2 Likes

After some more reading and speaking to some-people involved in the value chain, the understanding I have is that:

- There is a tech-edge and barriers to entry when it comes to the Auto business (as there is a long approval process and products are also more sophisticated)

- Same true for their bimetal business esp when they are supplying to the likes of Scheider etc

Though, when it comes to enery meters (and smart meters) it seems that there could be some local competition that may emerge. Also companies might still import from China as it works out to be cheaper even after duties.

Would be keen to gather thoughts from others on these.

3 Likes

One promoter group (Ghumman) have transferred their shares to another promoter group (Sandhu). Is it bad or good news for the company and its shareholders?

it is irrelevant to investors…

So, management commentary indicates the Q1 margins pressure is mainly due to product mix change and lower exports. That partially confirms the above reasoning. This also indicates that the shunts business requires lot more material than bimetals hence the increased COGS. @diffsoft , What is your reading?

2 Likes

Further, the geography mix is probably important to track. Exports has higher margins than domestic business in bimetals business.

Below is the snippet regarding the pricing and margins question. Evidence that bimetal business is more profitable than shunts due to consistent end consumers and not having to deal with Chinese competition which is there in shunts. On top of that, within shunts segment, there is better margin with automotive customers due to technology (slightly specialty business in shunts) vs smart meter (more like commodity business). So, another metric to track would be growth of shunts in smart meters vs automotive & other segments - this can be slightly difficult.

Overall, track exports v domestic (exports is higher margin) and product mix + growth for shunts with respect to end consumer (automotive is higher margin v smart meters)

4 Likes

I don’t have any reading. My point was limited to Econ 101. If you lower prices, you will sell more quantity. Also note that my point has nothing to say on margins. It’s just a simple relationship between price and volumes. To repeat, if you lower prices you will sell more quantity.

So you can’t call that an achievement; whatever words may be used to describe it, as the CFO did - “strategic focus” / “resilient demand (really!!)” .

Everything else; like ‘we sold more in domestic’, ‘we sold more shunt / less bimetal’ etc etc are explanations for the outcome. I don’t have much to say except that we should be very careful not to mix up cause and affect / stimulus and response. For instance if my employee comes and tells me that he sold more in domestic and less as exports; then was selling more in domestic which fetches less, a stimulus (i.e. did we purposely do it to make less money? wouldn’t that be dumb) or was it a response (export demand was weak so we responded by selling more domestic to keep utilisation going). He may cloud his reasoning as well as ours by saying - “I sold more domestic because demand was high”, “this is my strategic focus” etc etc; but the real reason is that he could not sell in the export market.

17 Likes

The latest Annual Report is delightful. The AI and data centre boom is a positive development for the company.

3 Likes

Please explain what is their contribution to data centres?. Its fashionable to add data centre, AI, ML, hyperscaler etc in your annual report to get a higher valuations.

Looks like with EVs having fizzled out a new game is being played now.

11 Likes

It’s about their contribution to switchgear, silver contacts etc. Just see the Jun 24 concall.

I’m very sure that an honest management will not fool investors by painting a rosy picture.

1 Like

And the latest FAME 3 is on the cards.

1 Like

Questions for Shivalik Bimetal AGM Sep 26, 2024

It’s time to get back our focus on questioning SBCL Management to extract more out of the interactions at AGM 2024. My natural bent is to focus primarily on the medium to longer term issues (even as near-term might be a bit disconcerting to some; to others it may seem like more of an opportunity ![]() ). So let me get to try and probe if the medium to long-term view/strategic intent of SBCL is intact.

). So let me get to try and probe if the medium to long-term view/strategic intent of SBCL is intact.

- Bimetal segment constitutes ~ 50% of total sales, with motor starters accounting for 8-10% of bimetal sales. In Exports, some customers like Cutler Hammer (primarily motor-starter sales?) had scaled up significantly since 2021 and even overshot Siemens (hitherto the primary customer in bi/tri metals). Bimetal Sales thus were a safeguard against fluctuating Shunts Market.

- We are hearing of-late demand first peaking, and then plateauing and coming off in this segment (quite majorly for some customers if not all). Could you please throw some light on the demand drivers, extent of stocking-destocking, and medium term outlkook for this segment. What were the main pillars of demand spurts in 2022 and 2023 and how does it look now for the Industry and SBCL specifically?

- MoU with Metalor Technologies International SA (Swiss Corporation) for setting up a Joint Venture in India to manufacture and sale of electrical contacts. This is expected to establish SBCL again as a global supplier in Contacts segment, boost volumes hugely albeit at considerably lower margins.

-

With the JV now signed, can you please throw some light on when commercial supplies is likely starting and what will be the segment contribution to sales/margins within 2-3 years> What kind of projections visibility are we working with now - is it 6-7 years, or more like annual?

-

Buyout of Checon Corp 50% stake in Checon Shivalik Contact Solutions in Apr 2022 This was supposed to have lifted the shackles on the Contacts business as SBCL was now free to market it’s products in the biggest market for contacts in the US. Can you explain why Sales have not accelerated even after more tahn 2 years. Is this a Marketing Challenge, or it’s Tech specifications challenge that SBCL has been unable to step up to, so far. If yes, are we hoping that the Metalor JV will solve issues on both fronts

- Capacity in-place for 1600 Cr in annual sales since 2023. SBCL had mentioned then that the confidence in setting this up much ahead of time was based on 6-7 years forward visibility from strategic clients and the ramp up envisaged by them. EV market dynamics and geopolitics might have led to a significant pause.

- Please throw some light on how have these projections been revised/deferred by major Clients like Vishay. Also Continental and Hella were expected among major growth drivers but they have stayed where they were (last 2 years) while others like Gruner and Dooyoun have spurted much ahead in the same timeframe. Will be good if you can share anything on these new relationships.

- New Capacity being set up. We understand that this is ostensibly to take more advantage of PLI Schemes and forward integration projects being undertaken. At the same time we actually have 3x more capacity in-place lying under-utilised. Currently PLI scheme earnings are at 12 Cr

- Please throw some light on what are the expectations from PLI scheme accruals in 2-3 years. Also please throw some light on why decision on forward integration projects/capacities were NOT taken in existing factory set-ups where SBCL is sup[posed to have the largest EBW/Bonding/Stamping in-house facilities in the world?

- Forward Integration projects. As we understand logically there are 2 significant areas of great value-migration. Current-sensing & BMS, as also Smart meter Relays. BMS R&D projects have been mentioned a couple oi times in Concalls too.

- Kindly let us know where we are on these projects. Why is this NOT a good time/idea to focus and speed up commercial products entry given the current stagnation in revenues for almost 3 years now, especially in the light of severely under-utilised capacities?

- Sustainability of Competitive Advantage. We have talked about global market share in EBW Shunts as over 10% and less than 15% in last AGM. We had the largest capacity globally already in EBW Shunts.

- Please educate us on the competitive space, older incumbents as well as new challengers. Of late we have seen SBCL mentioning impact of Chinese competition. Which are these segments and please educate us on the nature of the impact, and how it looks going forward.

- China Market for EVs. This is the homeground of the biggest players in the EV space today. BYD and even new players like Xiomi. Vishay has mentioned several times that BYD is a big customer (not sure whether for China market as well).

- Kindly educate us on SBCL efforts in China - we have a Sales Office there, what is its role? Given that China EV market is the largest and still growing (while every other EV market globally has probably paused/slowed down), what is SBCL trying to do there? Are we present in the Chinese EV/ICE ecosystem? As a Tier 3 supplier to what kind of Tier2 players? BYD was a development customer for SBCL, what is the progress on that? What about Sales through Vishay’s customer base in China?

-

Battery Gigafactories being set up in India under PLI schemes and even independently by 8-9 deep pocketed players. By 2030 targeted capacities are like 300 GW. Do we have customer inroads already into that space. What about Energy Storage systems - that should be a big growth driver in next 3-5 years?

-

Growth in Defence and Medical Devices segments. SBCL has mentioned harnessing potential growth in diverse segments such as Defence and Medical devices.

- What is the traction we have seen. Do we have any development projects going on?. Would be great if you can throw some light on that.

- ABB and Schneider relationships

- When do we see scale up?

- Hella and Continental relationships? Was supposed tp scale up majorly in another year or so

- Where are we? is this paused, deferred, what?

12 Most promising growth segment in next 2-3 years.

- Apart from BMS Shunts, where is the excitement in SBCL as a major growth driver rivalling BMS Shunts potential in next 3-5 years. Contacts segment, Smart Relays, BMS, Smart Meters

42 Likes

The italicized text is taken from Vishay Q2 2024 earnings call transcript that took place on Aug 7, 2024.

-

“Based on input from our customers in Europe and the Americas, we’re seeing flat automotive demand tied to persistent high interest rates, driving consumers to look towards purchasing less expensive compact cars, containing less electronic content.”

[Q] Are there indications that the worst of the demand decline has passed now that the Fed, ECB, and China have started reducing interest rates? -

“Even though sales were lower, design activity continued on all automotive electronics, including BMS, ADAS and with the increasing discussion around AI chipsets. We also stepped up our engagement with automotive OEMs and Tier 1s.”

[Q] Could you provide some insights into the trend regarding the level of design activity for automotive electronics related to the customer programs planned for launches in 2026 and 2027 and beyond? -

“We have decided to guide it flat even though we see scheduling agreements with increasing demand in Q3. We saw what happened in Q2. We had Q2 with a positive move from auto in their schedule agreements and they readjusted. So the week-by-week demand pulls that are forecasted would show a positive Q3 over Q2 for auto. But at this point, we’ve decided to guide it flat, fewer workdays in Q3 seasonal holidays in Europe, seeing automotive car count declining a bit. We decided to go flat even though the signals from the auto customers are a bit up.”

[Q] What is our guidance for the shunt business segment in the near to mid term? Are we seeing an increase in orders? Or the continued softness sideways market for another quarter or two longer? Getting a sense of the Orderbook to Bill improving/declining trends would be great. Vishay’s Book-to-Bill trend for Resistors segment has been 1.05 (2Q 2022) → 1.08 → 0.85 → 0.88 → 0.74 → 0.65 → 0.82 → 0.79 → 0.87 (2Q 2024). -

“Automotive revenue declined 6.7% QoQ in Q2 2024 and 13.6% YoY as Tier 1 automotive customers pulled below their schedule agreement plans primarily in Europe. OEMs in North America and Europe pulled back on EV production and postponed some of their new EV platforms.”

[Q] We believe that the postponement of EV platforms will likely affect us as well. Are these reductions in EV production being driven by the rise in Chinese EV launches? Are we largely reliant on non-Chinese EVs, or do we also hold a substantial share in the Chinese EV market? -

We understand that our Electrical Contacts segment is currently operating at around 90% capacity, and with the move to the new plant, capacity will increase threefold, bringing utilisation down to about 30%. According to the Shivalik Q2 FY25 concall, the new plant is expected to be operational by Jan 2025. Are we still on track for this timeline?

- Also, is the Metalor JV on schedule for a Jan 2025 launch? This would enable us to utilise the extra capacity at the new Electrical Contacts plant, greatly reducing the lead time for setting up additional facilities.

19 Likes

Thank you @Donald da for the writeup. This summarizes the major questions. The queries that I have are follows

- We know that by 26-27 onwards California, EU , UK are pushing NEVs ( BEV and PHEVs) by various regulatory push. As far as I understand that there are no changes in those. Will we start to see higher capacity utilizations due to that as we approach CY 26-27.

- Second concern is that OEMs as a means to diversify their supply chain have started approving Tier 2-3 suppliers outside of China. Are we a second source / third source supplier for the Tier 1s. If yes what are the ways that we can become 1st source.

- Has there been any interest for shunts from BMS manufacturers dealing with utility level battery storage ( also called BESS )

- How does the IP work in the shunt space? e.g. If an OEM approves some shunt designed which you have manufactured and optimized, do you also protect the manufacturing process via patents ?

I will update more questions as they come to my mind

13 Likes