“Certain disclosure obligations for the acquirers/ promoters, etc, pertaining to acquisition or disposal of shares aggregating to 5 per cent and any change of 2 per cent thereafter, annual shareholding disclosures and creation/ invocation/ release of encumbrance registered in depository systems under takeover regulations” would be done away with from April 1, 2022.

In a release issued after the board meeting, Sebi said the relaxations would be done due to implementation of SDD.Under SDD, relevant disclosures are disseminated by the stock exchanges based on aggregation of data from the depositories without human intervention.

Revenue growth has slowed down. It could be a one off weakness. Company is hosting a conference call. Will know what happened in the same.

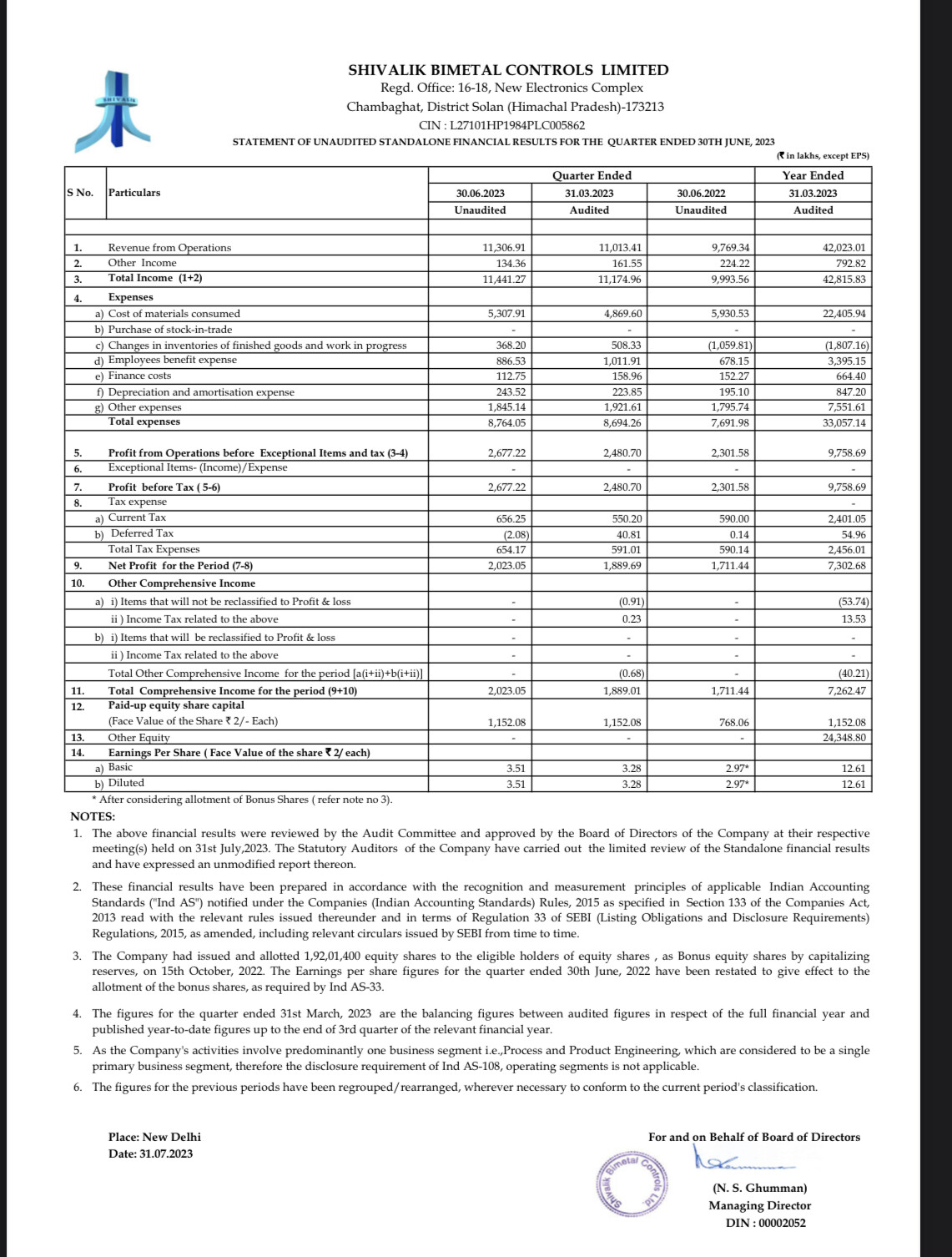

The company had exceptional items in first quarter which boosted consolidated PAT. If you remove that from the base of last year’s numbers then growth is much better, which perhaps is the right way to look at it. See the notes to accounts below, "The Net Profit for the quarter ended June 2022 and year ended March 2023 includes aggregate amount of Rs 512.44 lakhs comprised of Rs 329.16lakhs as valuation gains on acquiring stake in SEPPL & SBEPL included under the head “Other Income” and Rs. 183.28 Lakhs on account of creation of deferred tax liability in accordance with "Ind AS 103-Business Combination”.

Shut Resistor Automobile: Demand from Export was relatively weaker during Q1FY24 due to normalisation of investory levels. While company has added many new cusomters in last 3-4 years, the scaling up with new customer would take time. Anticipate demand to recover in Seond half of FY24

Shunt Resistor Meters: In single phase meter, Shivalik has around 65-70% of market share for Shunts. With new GOI policy about implementation of Smart Meter (around 250 mn), demand for shunts is likely to increase. Shivalik already have capacity now at place. However, implementation speed as suggested in GOI appears very agressive if one compare same with past experience. Only 2 mn smart meter (as against plan of 250 mn) are currently installed. Further, Smart meter use Relay as input, which was imported in past. Now many German/Indian and Chinese reputed players have installed relay capacity. That would drive demand for Shivalik Shunt as well as Shivalik Silver Connect.

Shivalik potential market in Smart meter is from 45-50 (in case only shunt is used) to Rs 150 (in case all products of Shivalik are used). The demand growth form Shivalik would be mainly determined by scaling up of Relay Capacities, for which Shivalik is optimistic. Hence, during FY24 and FY25 Shivalik see Smart meter demand from India being a main growth driver for revenue.

Birmetal: Demand for Bimetal has improved mainly from Indian market. Export market reported lower growth than Indian market.

Capacity expansion and Capex: The company has already spent 80% of Capex for Bimetal/Shuts. Post completion of capex, the company could achieve Rs 1500-1600 Cr sales. The company expect same would be achived over period of 6-7 years. First three years, Smart meter would lead demand for new production and subsequently it expect Automobile sector to be growth driver. Operating leverage from new capex could result in 2-3% improvement EBITDA margin from current level of 25% to 28%.

Silver Connect: The company in process to triple its capacity over next 24-28 months. Next 12-14 months, phase I would be complete and capacity would be doubled and further 12-14 months, Phase II would be complete with total installed capacity being 3X of current capacity. Increase Relay production in India for Smart meters would be main demand driver for Silver Connect. Previously, Silver connect business was in JV but now it is part of Shivalik Group.Hence, they are looking at getting synergies from existing Shivalik skills set and client network.

Other information:

In exports of Bimetal,nearly 100% of of customer are Tier I supplier to Automobile companies, while in Shunt nearlt 30-35% customers are Tier I supplier and Balance 60-65% are Tier II Supplier

FY24 Outlook: Anticipate 15-20% Growth over FY23 revenue. Since the capacity are now operational and Domestic enviroment is good, do expect Indian market to drive growth in FY24 and may be FY25. While the company expect export market to peak up from H2FY24, still expect growth rate to be lower than Indian market in short to medium term (say upto FY25).

Disclosure: Shivalik Bimetal is my largest holding and hence my view may biased. There is scope for communication error at my side. I am not SEBi registered advisor. I am not recommemding any investment action in Shivalik. I may exit fully from my investment without informing forum.

It was good to see @ayushmit and @sahil_vi getting opportunity to participate in the concall.

Unfortunately the time was short and I ended up waiting in line.

I have some queries if someone in touch with management or answer it here.

Queries-

Hydrogen fuel cells for cars are being developed. So how many shunts will each fuel cell utilise and are we in talks with any of the company for capitalising on this opportunity? (Google Bard gives an interesting answer to that in terms of quantity but someone advised not to trust that. So…)

How is Shivalik Bimetal benefiting from the Electronics manufacturing ecosystem thats developing in India and for exports market?

EBW is also utilised in semiconductor mfg.

Does our company have plans to tie up with some Big names?

Tesla is coming to India (most probably), will our company be benefitting from the existing arrangements that we have, as Tesla has big plans for exports from India.

The contract manufacturing of ACs and implementation of ACs in trucks being mandatory also presents an opportunity wherein we are already supplying to some existing players. The temperatures around the world going up and rising middle class in India also hint at fast paced adoption of ACs. Any colour on the opportunity size in this segment? What is the revenue per AC as well as other household appliances that use Bimetal strips and shunts that can be realised.

Is the company planning to develop any new complementary products in near future?

What is the opportunity size for our company in battery storage as PLI schemes have been announced?

Lithium mining story in India will result in a massive opportunity for battery production in India and EV adoption. Does the 1600 Cr revenue forecast take into account this development or we will be able to achieve this in earlier timeframe, provided the mining process and refining issues are sorted well in time.

As of now the company is only in B2B segment, any plans in near foreseeable future for product development and going B2C or contract manufacturing by taking on some contract manufacturing from some reputed brands.

Semi conductor Manufacturing is evolving landscape in India,Its Multi stage process and Complex ,But going through it briefly I found Metallization as process may require products that Shivalik makes or kind of have speciality in their manufacturing.

Metallization:Metal contacts are formed on the wafer’s surface to enable electrical connections between different components of the integrated circuit.

The choice of metal contacts depends on factors such as the semiconductor process technology, the specific semiconductor material being used, the desired electrical and thermal properties, and the intended application of the semiconductor device. Different combinations of metal contacts are used in the multi-layered structures that form the integrated circuits and other semiconductor devices. Each metal contact material is carefully selected to ensure optimal device performance and reliability.

Entering after re-rating of P/E and at the time when everyone has too much optimism…connecting each and every big story in news with the company’s capability…are sometimes the prefect recipe of FOMO and loosing money!

If big semiconductor company coming to India …they are coming with all advanced technology know-how and with mass production capability…it might not benefiting to small company like SBCL…

Sorry, I do not agree. Shivalik has already proved its mantle. It has attained its reputation by delivering through last several qtrs. Advent of global semiconductor companies will be greatly benefitial to it. Big companies will depend upon value chain and assured and quality suppliers. Shivalik with its reputation as a time tested supplier to MNC is bound to benefit. Timely capacity expansion is another big positive.

Share price movement is unpredictable and it is individual’s conviction as to buying range. But recent dip in the share price in a bullish market gives an opportunity.

NB- Have bought small quantity in recent dip, so my view may be taken as biased.

Like exercising options.

So, the individual/firm took delivery here.

Why does this impact the valuation, cause its only solidifies company’s value.

We all would like to have more of something (at a lower value) when we have seen it increase in value.

This is a positive for all the valuation estimates we all have. Performance has been compelling enough for someone to exercise such an option.

Let me know if anyone thinks I am wrong in my understanding.

Disc. Invested.

Shivalik Bimetal: The shares of the company settled over seven percent lower on Monday, ending in the red for third session in a row. The stock remained under pressure post large block. Dealers suggest that promoter entity is the likely seller and a leading domestic AIF is the likely buyer along with few hedge funds.

Extract from CNBC.

Although this is a negative for the stock, it would be interesting to know the identity of the Alternative Investment Fund.