At the heart of Shivalik Bimetals is the process of Electron beam welding (while they do follow other welding processes too, this is one of the important ones). Perhaps then it is useful to understand the process itself.

Here is a short video:

Another one:

A few key takeaways:

This is a fairly technical process. The chamber where welding occurs has to be emptied off air & water molecules (better the vaccum, better the outcome). This is needed because otherwise the electron beams collide with the air/water & lose their energy.

process uses kinetic energy of electron beam to produce heat energy (when electrons collide with metal atoms).

This process requires extreme skill. The direction & exact angle of electron beam is controlled by a human using a lens. One can now imagine why this is called “precision” welding. The skill with which the human operator has to gyrate & move the lens & thus the direction of electron beam is not any less than the sort of skill a surgeon requires to do surgery. The biggest entry barrier thus is the person doing the electron beam welding. This is a technical know-how moat. The experience they have received by welding many kilometers cannot be aquired with money alone (of course people’s allegiances can be bought or sold).

The cathode filament in the electron gun is heated to 2500C for continuous emission of electrons. For comparison, surface temperature of our host star (commonly known as Sun) is 5,505C (so the equipment operates at half the temperate of our host star surface. This shows us how dangerous this equipment is & how much are one must pay in operating it.

Electron beam welding is also used in nuclear, ship building, medical devices. Looks like there exist a lot of adjacencies whenever (X years down the line) they might want to expand their core competency (which is not shunts, it is welding of bimetals or trimetals).

Here are some “disadvantages” of electron beam welding:

Do those sound like disadvantages? Sound like entry barriers to me, each & every one of them.

This also answers one of most IMP questions to me personally. This business can run itself, promoter competence was needed to jump-start envision then early execution. Now that they have skilled people doing the actual welding (pretty sure Mr ghuman does not do welding on factory floor), this is the sort of business buffett would want to own (anyone can operate). Promoter competence would definitely still be needed in doing new R&D developing new core competencies (new materials to weld, new process, new applications). But the opportunity size is so huge even for existing products, one cannot go too wrong buying at 20 times earnings imho.

Link to see the shipments of Shivalik to US. Can think of Patterns by which i mean

the qty which Shivalik is giving to Vishay over time. Have been following this link for

a while and it clearly shows that Shivalik is the biggest supplier to Vishay for its shunt

resistors and the qty supplied to them has only gone up over time.

The only question is how much more can it supply if it is already the most dominant supplier,

no company would want to Procure all it’s material from one supplier considering the

current environment where supply stability is key.

It does not need to grab larger share of wallet of vishay because vishaya own resistor sales are growing. See the post i shared yesterday. Vishay sales are growing around 5% QoQ

Also, shivalik has already diversified it’s revenue stream away from vishay to a good extent i think. The actual numbers will come probably in AGM. Also, shivalik already has 3 scaled bms contracts, maybe more in pipeline.

My appreciation to sahil-vi for his commendable works on Shivalik. Kudos to you. Would like to mention here my apprehension for margin squeeze in Q1 & 2 due to unprecedented rise in raw materials price, which may not be 100% pass through. Also logistic and freight issues may have a bearing on its performance, as it is dependent both on imports(raw materials) and exports. Inspite of it, Dec21 result was good, which speaks well on its management. Matter will be cleared on concall after yearly result.

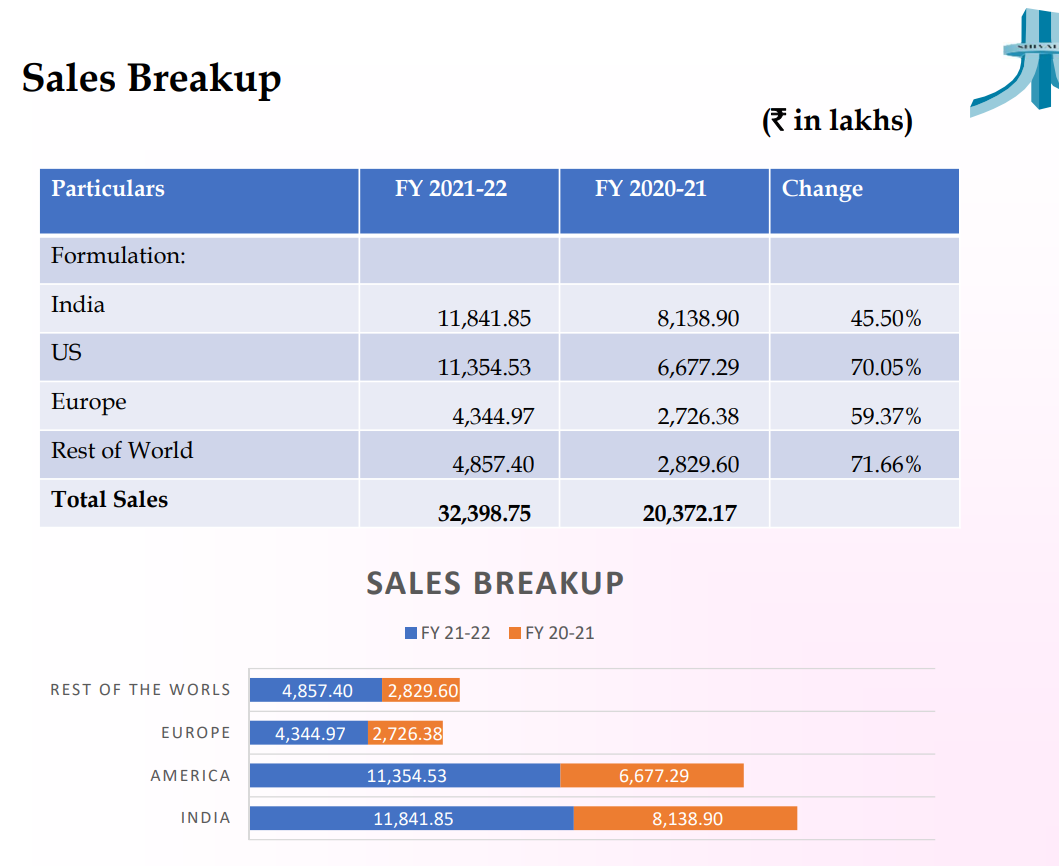

I dont think these numbers are matching.

In the co’s Presentation, they have given the breakup - Export sales have done equally well, actually better than the Indian business in terms of growth.

Did some research to understand the impact of Copper prices on gross margins.

(I am aware they import copper alloys and not copper, but I considered LME copper prices as good proxy)

Quarter

Revenue

COGS

Gross Profit

Changes in FP & WIP

Adj. COGS

Adj. margin

Avg. quarterly copper prices

Annual Revenue

Domestic Sales (%)

Exports (%)

Jun-19

51

26

24

3

30

41.3%

2.82

Sep-19

46

25

21

1

26

42.5%

2.68

Dec-19

44

23

21

1

24

44.9%

2.76

Mar-20

46

23

23

3

27

42.6%

2.50

187

40%

60%

Jun-20

29

16

13

-1

15

47.4%

2.58

9%

Sep-20

49

30

19

-5

25

49.0%

3.04

Dec-20

59

30

29

-1

29

50.8%

3.35

Mar-21

67

37

30

-5

32

52.0%

3.84

204

40%

60%

Jun-21

70

41

29

-6

35

50.5%

4.46

59%

Sep-21

76

41

35

-4

37

51.6%

4.27

Dec-21

88

44

44

0

45

49.1%

4.34

Mar-22

89

45

44

-1

45

50.1%

4.51

324

37%

63%

Negative correlation between copper prices and gross margins is weakening y-o-y, which is good for Shivalik.

It implies the company’s pricing power has improved along with strong topline.

In current scenario, company is recording ~25% (FY22) EBITDA margin, when copper prices are the highest.

In a situation where copper prices drop (due to clearing of supply chain problems and not due to weakening demand). The company might even record higher margins.

a 4000 crore tender for 5 million smart meters… in the Delhi region.

Smart meter is the need of this decade considering the weak financial positions of discoms. Discoms have been bailed out earlier too under PM ujwal yojana. It was in vain, still accumulated losses of 5.5 lac crores accumulated losses due to inefficiency in collection, due to non revision of tariffs.

Rajisthan, Tamil nadu, UP, MP account for major delays to the tune of 8-14 months. Rajisthan and UP have already started to put smart meters.

Very positive for SBCL if this theme accelerates. Cant bailout discoms again and again. It is throwing good money after bad

After reading the thread from starting I think that Shivalik falls in fast growers(overall) category , cyclical in terms of raw material, segment in which it operates . Shivalik has pricing power and operates in niche segment. Shunts form a critical application product in BMS as no one can’t get approval from OEM’s easily. As discussed company has a bright future prospects ahead at least for coming 4-5 years due to EV theme. Management seems to be good and have skin in game.

Disc: Trying to take small position and will increase stake to at least 4 %

Shunt resistors in general have thousands of players, but ultra low ohmic shunt resistors have very few, only 3/4- why so? In what ways is the chemistry/welding method for low/ultra low ohmic different from that used for high ohmic shunt resistors? And thus what prevents someone who is already doing high ohmic, to enter into low ohmic?

Look through the earlier posts in May by @sahil_vi on the welding process Shivalik uses. Electron Beam Welding which allows precision welding and is a high skill job is probably the barrier for many others to compete with Shivalik.

You can google about shunt resistors on sites which sell resistors and can see that many companies manufacture normal shunt resistors while there are very few companies which sell low ohmic shunt resistors as the precision required for manufacturing them is difficult to achieve. Furthermore, the price difference between low ohmic shunt resistors and normal shunt resistors is also significant. I think EBM technology which Shivalik uses is a differentiator. @rambaranwal is an expert in the industry and can give his views on the same.

There is so much varied information which is being attributed to Shivalik on this thread, but there is hardly any primary information from the horse’s mouth (promoter and management)

The company should make an effort giving more information through PPTs, press releases or interviews.

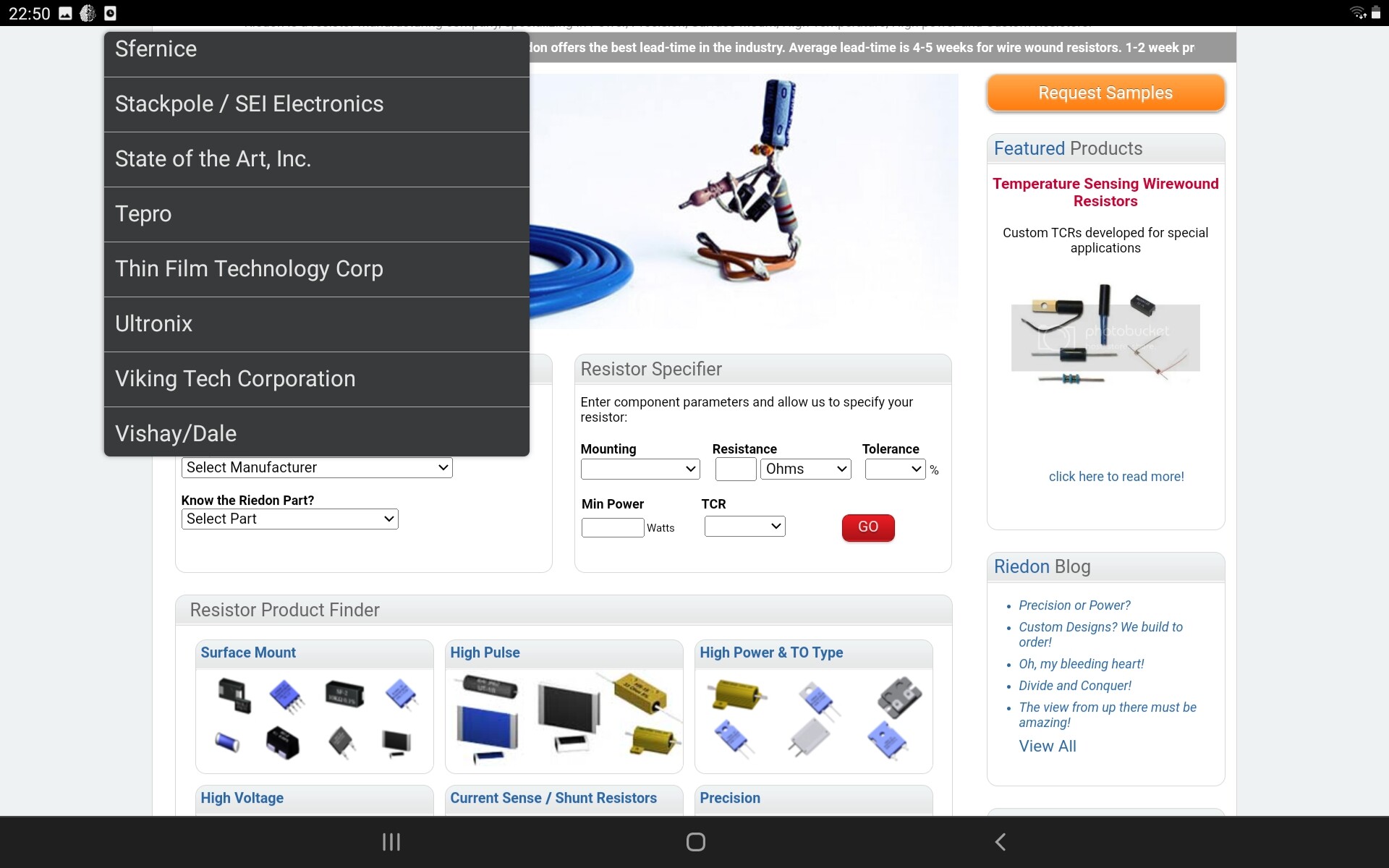

Interesting - Shivalik supplying to a competitor although the qty is very small.

Riedon is a global Player in resistors and is quite an old Player established in 1960 and they

have their own Plants in USA and Mexico.

Hope this is just the beginning because a Player with an experience like Riedon can

Provide significant volumes for Shivalik.

Rideon seems more of an aggregator( may have smal mfg footprint as well but with 130 employees one cant do much ), one can see many other players listed as well. Including ROHM, Isabellenhuette etc in drop down.

Even a direct supply to established player is useful scaling in a way, though suspect these suppies are on behalf of Vishay Dale as dont see Shivalik listed yet - one van see Vishay listed. As Vishay is a supplier to them, it would be a conflict for Shivalik to bypass its biggest client - and this will continue to be a problem for Shivalik in US region to scale shunt biz directly given likely non compete clauses per Contract with Vishay.

This is likely reason that we see Shivalik winning clients like ronertshaw and Airvent in direct supplies for bimetal, but none in shunts beside Vishay( or Vishay approved entities)

Even if Shivalik were to get direct Enquiries for shunt supplies in US - a lot will depend on Shivalik- Vishay contract as to how those will be supplied, most likely via Vishay. Hope Shivalik mgmt is at equal footing in such deals amd can negotiate with Vishay for better terms as biz scale grows.

This may be bit far fetched but there will come a time when Shivalik has to relook at entire Vishay relationship if they were to up the ante in US region and have aspirations to build direct biz relationships with enterprises in shunt and related solutions supplies. Till then Non US scaling is where Shivalik may be focusing more before they can reach a size and scale to have reduced Vishay dependency further lower.

Edit - Shivalik will continue to grow with Vishay, Keeping an eye on Vishay commentary for Q2 22- see no impact on demand due to inflation, inventories are lean ( high book to bill ratio and high backlogs) here is the commentary snapshot, bodes well for Shivalik

Those who want to understand Vishay better - here is a quick read - key take away is very few players in industry show non cyclical behaviors, Vishay is one of them. Again assuring from Shivalik demand visibility over long term.