I have recently started reading up on this company. 2 QQ:

How are the promoters like? Do they have clean track record. Hardly any commentry on/from them.

What % of Shivalik’s revenue comes from Vishay? Is Vishay a mere aggregator or do they have the capability to backward integrate and make these resistors themselves?

Hi @ankitgupta & @Malhar_Manek, Technology at times is funny. You need one nitche to start and then build upon it. The risk of technology getting changed for some solution at times becomes moat for the company that builds & masters it first. Once you get a lead into certain domain and keep adding incremental value usually that tech survives quite good number of years. One example is CRT tube display. Its one of the most stupid solutions but once commercialized it remained into being for some time. It took good 3-4 decades to have LCDs then LEDS and what not. The threats we are looking for Shivalik is not only risk for Shivalik but also moat as new palyers would think multiple times before entering same domain. Shivalik has niche in manufacturing low ohmic shunts with superb temperature stability and great PPM, which only few in world could do. Developing that competence and making it commercially successful is time consuming and requires great degree of R&D. Once you are successful in building a product, selling it in volumes another challenge. I know more great product makers than good sellers being a R&D person, but at times generating volume sales and making the product commercially viable is challenging & good moat. It takes years of evaluation before volume sales start specially in automotive. Its combination of multiple items that gives advantage to Shivalik.

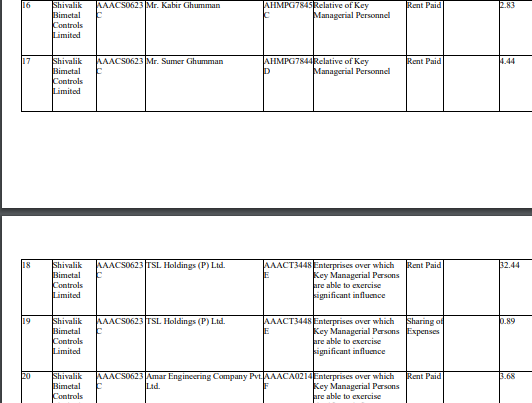

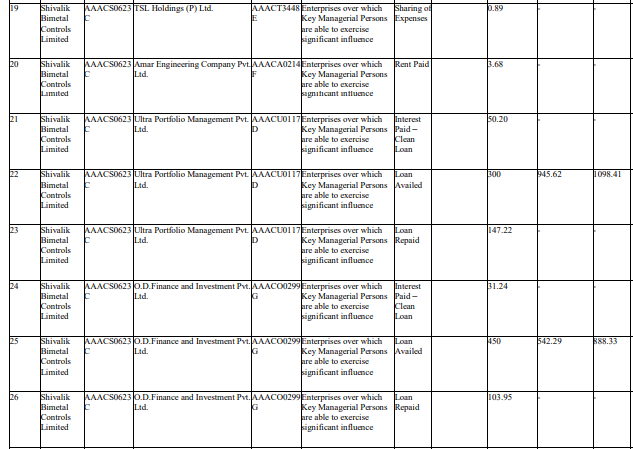

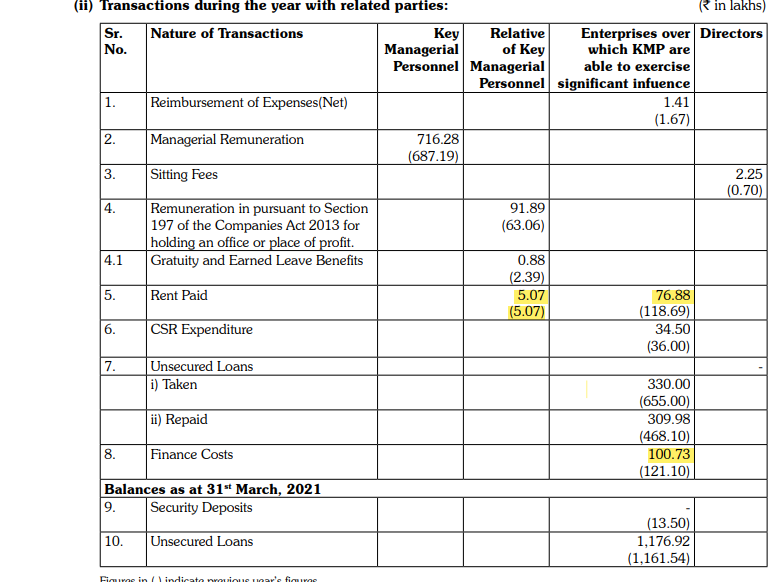

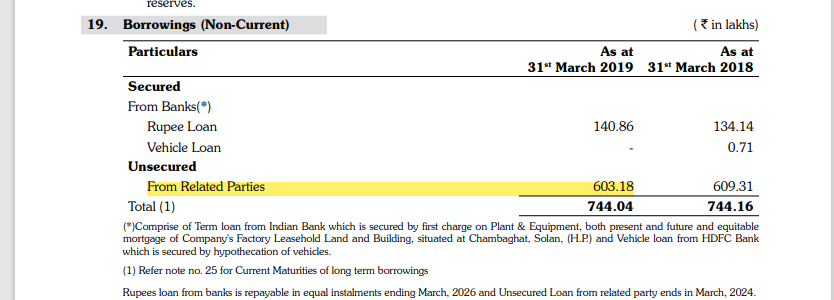

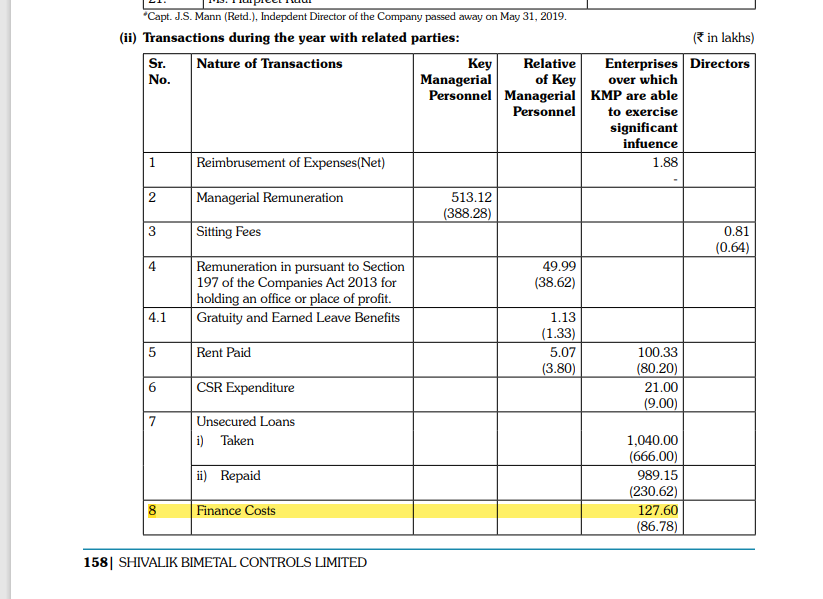

but in RPT submitted by the company I could find that rent is paid to KMP of the company and moreover loan is taken from a company where KMP are the directors

thought this was looking like a red flag

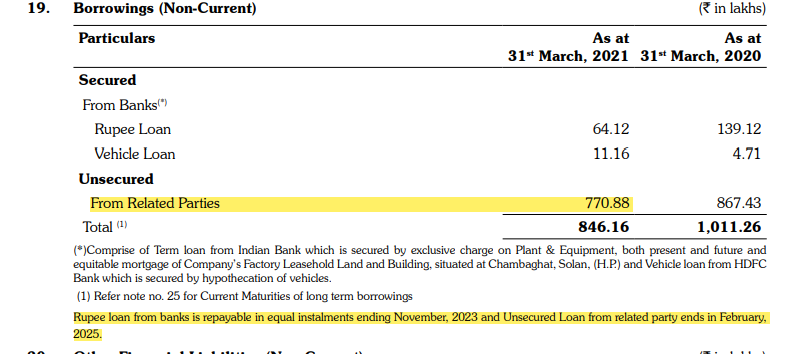

i checked the annual report which states that 1 cr paid on 7.7 cr unsecured loans from related party

which comes to 13.5%

the company has 15 cr in its current account as well as FD of 4cr

so cant justify why paying 13% interest on loan

now this is extracted from AR 19 which shows the interest rate on RPT loans to be 21%

still cant understand why co. took such high interest bearing loan from RP

You are assuming that loan shown in the balance sheet on 31st March was consistent through out the year. Balance sheet only shows you the data on a particular date(31st March).

I take your point. Unfortunately, I am not very good at detailed balance sheet analysis.

I have seen related party loans in micro/small caps a very common thing.

I generally ignore it if it is not large enough.

For example you can read NGL Fine Chem AR. There are quite a few RPTs. Still a great value creator the stock has been and I would rate management as A+.

Regards,

Raj

Disc: Invested. No trading in last one year.

My assumption is that since Indian Bank has first charge of almost every property of the company(present & future) as a security for the secured term loan, its not easy for a small company to get another secured loan on the same set of assets from another bank. Whether anybody else would be willing to lend the sum at lower interest rate is the question that needs to be answered before deciding that its a red flag. 3 years ago the yearly profit was 4 crores . I would say that for a company based in far flung Solan , it would not be very easy to get an unsecured 7 crores from anyone else .

Disc: Invested and I have no degree in finance or accounting.

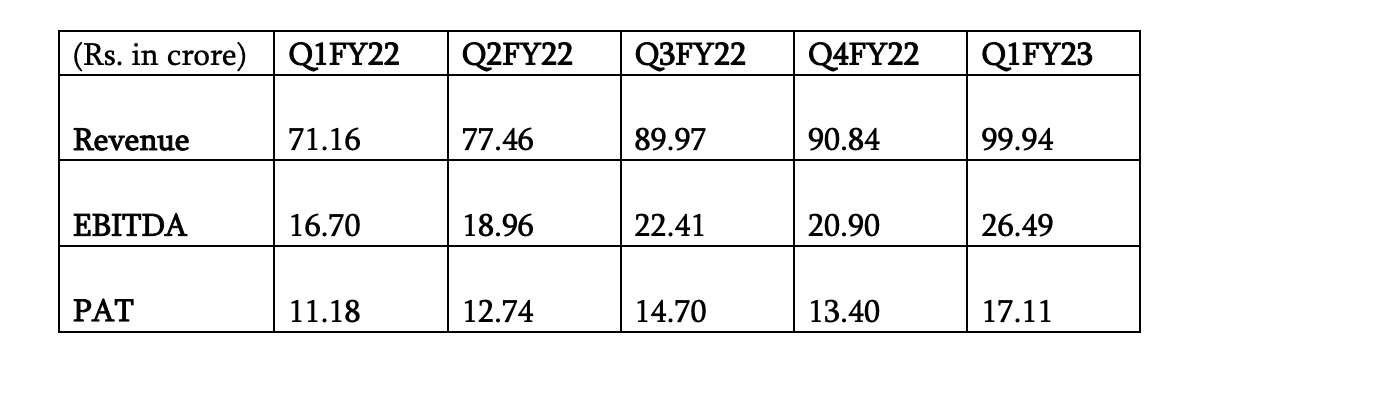

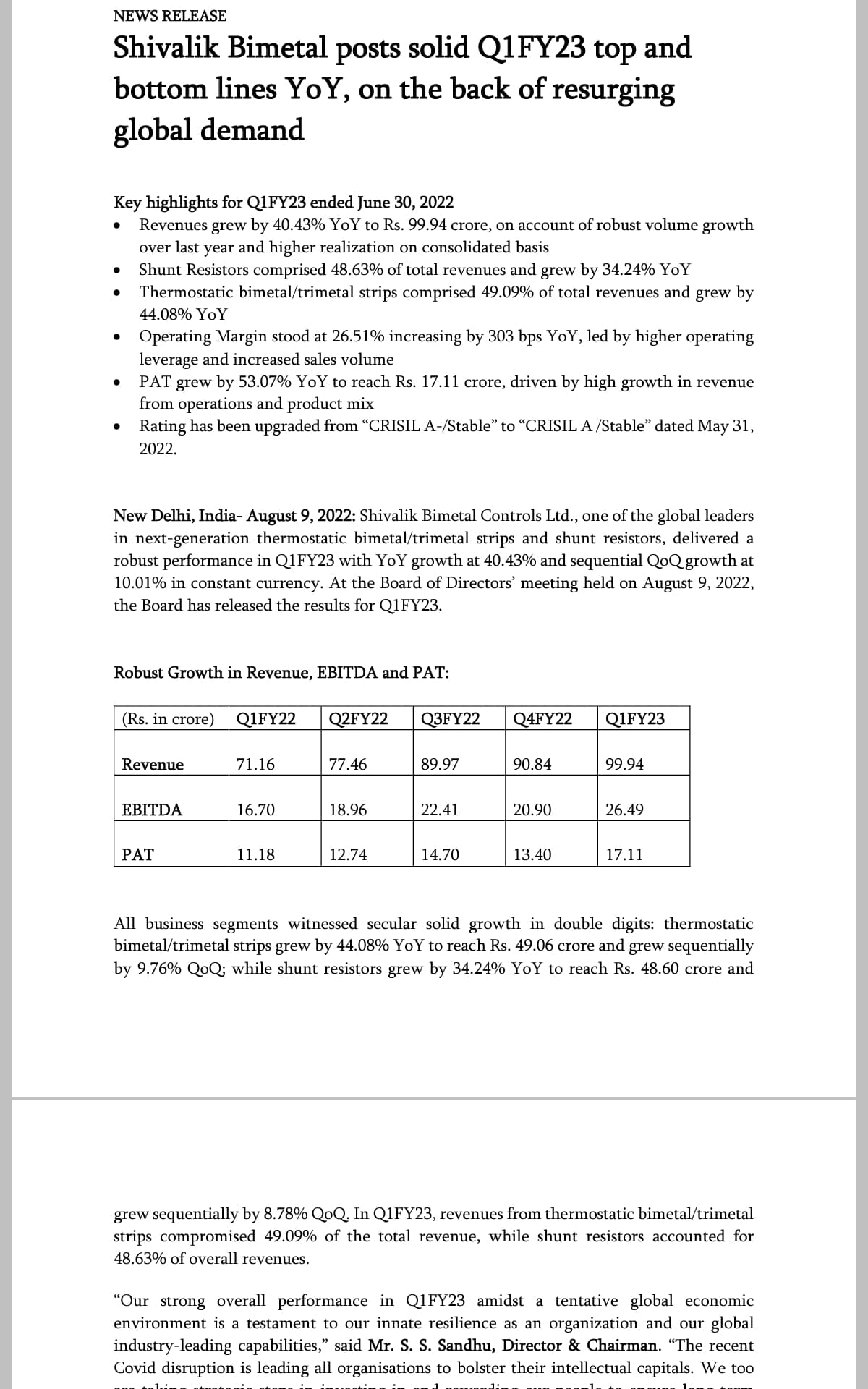

Growth is in line with scuttlebutt done by our smart VP folks…The stock will get rerated faster if company starts more interaction with investor community like regular concalls, investor presentations etc

There is a huge fair valuation gain sitting in other income. Margin needs to be seen removing this non operational profit. Pointed to me by another VP Friend.

Even if you remove the extraordinary gains, we still have significant jump in all parameters. Net profit would have been 17Cr+ on a consolidated basis which is 50% jump over Q1FY22 PAT.

The best thing is the result of capex is visible and top line growth is coming.

Regards,

Raj

Disc: Invested, no trading in last 1 year,