While revenues and margins were down sequentially,one should probably look at yearly comparisons.The AGM was also held yesterday,some KTAs:

→ Order book of 130 cr.,45 cr is exports

→ Seeing no slowdown in enquiries and pipeline continues to be strong

→ 55-60% business comes from renewable sector,30% exports and rest is coal,steel,sugar,etc. Company has been able to make inroads in the capex heavy segments and has gotten fairly large orders(not quantified) in India,expect this to be one driver of growth.

→ RM prices are down while realizations are strong given good exports.Company expects 16-17% EBTIDA margins for fy23.

→ Work only with private players and will continue to.

→ Expect to do 225-50 cr revenues in FY23.Can do 350 cr at peak.Brownfield capex will take 18-24 months,have huge surplus land available for doing so.

→ WC is well under control,no cash flow issues.Looking at monetizing old plant(amount not disclosed)

Overall,management seemed bulllish on growth for 1-2 years atleast.Given Q1 nos. achieving 16-17% margins for full year might be tough but let’s see what they end up with.

Capex - We did last capex in FY19 to increase capacity from 1000 MVA to 4000 MVA, that is enough for growth in near term, no new capex needed for now.

Capacity at Gavasad - 4000 MVA. If capacity is used to produce 100% renewable transformers, it would be 5000 MVA. If capacity is used to produce 100% oil & gas transformers, it would be 3000 MVA.

Order Book - present order book is more than 130cr (exports - 45cr, domestic - 85cr). Majority of domestic order book is from wind & solar segment. 15-20cr order from sugar/steel/cement segments. It is taking 14-16 weeks to deliver an order

Export is better margin business

capacity utilisation was 60% in FY22, it is projected to be 80% in FY23

Customers - Adani/Tata Power/Sterling & Wilson/L&T/Mahindra/Torrent Power. Not doing much business with state electricity boards (SEBs) due to large receivable days.

Current land have space to increase capacity by 2-3x. 10cr capex needed to double capacity. Time taken from start of capex to commercialisation is 18-24 months.

oil & gas transformers have better margins than renewable transformers.

The company is not present in 220 kVA step up transformers

Disclosure - Invested from much lower levels, sell transactions in last 30 days, still a decent part of portfolio, not a buy/sell reco, not a SEBI registered analyst, please do your own due diligence

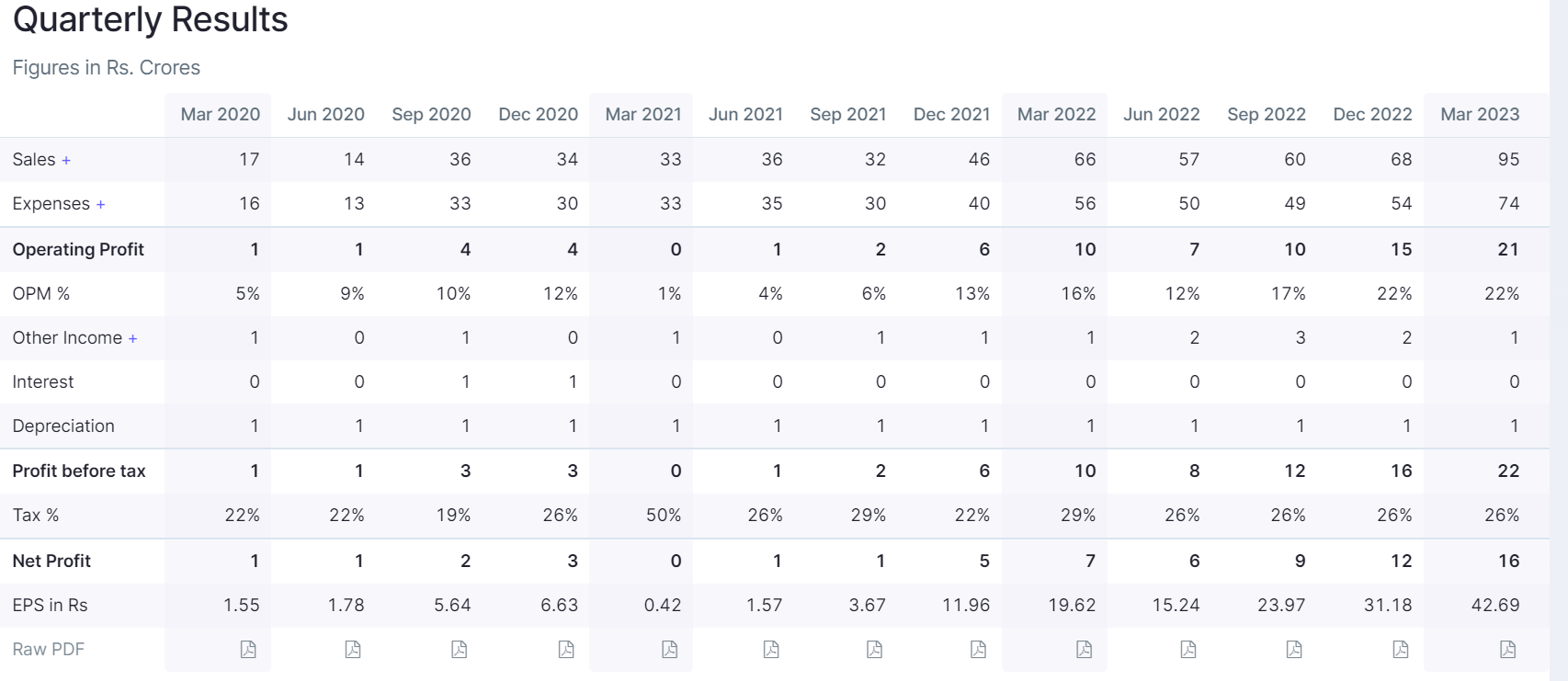

Shilchar reported another excellent set of earnings yesterday:

Revenues up 44% yoy

EBITDA up 110% yoy

PAT up 128% yoy

For the full FY company has ended with 280 cr revenues & an EBITDA of 53 cr,which translates to full year margins of 19%.Thus,revenues & margins are both well above the management guidance.Cash flow is also fantastic with ocf at 39 cr.It is also noteworthy that the sharp rise in EBITDA margins from Q2 to Q3 has sustained in Q4 as well.Operating leverage alone can’t lead to such a jump.So,it stands to reason that better export share too would be contributing.Key point to understand would be if there is a change in the sales/delivery model of the company.

Going by the Q4 runrate,company should be very close to 80% capacity utilization.As such I would expect a capex announcement some time in Fy24 if demand momentum sustains.There is a small rise(3 cr) in PP&E for FY23.

Overall,inspite of the sharp rise in price over the last 12-18 months,stock trades at pretty reasonable valuations of 17x TTM.If the company can sustain earnings at close to Q4 runrate then further re-rating awaits.Return ratios are now north of 40%,though this maybe nearing a peak.Looking forward to the AR & then the AGM for some hints at capex & demand scenario.

Here is a quick peak in possible drivers behind this performance and more importantly how long can this demand tailwind last going ahead

Transformer Demand-supply scenario in US indicates supply shortages, structural pattern given a new transformer plant takes 1.5 to 2 yrs to commission - interview of largest transformer maker in USA

US power infra needs massive upgrade (partly being 35-40 yrs old and beyond age limit) - per Utilities companies Transformers are critical to make it happen and are in shortages

Transformer shortages are causing delays in home deliveries

Above are not comprehensive but just to get a feel of factors affecting demand - supply

In general Transformer players are upbeat, more so those in exports of electrical infra(shilchar doesn’t do concall but one can get good idea from concall of Apar industries, CG power etc on global electrical infra scenario), as captured in thread @rupeshtatiya notes + exports tracking - Shilchar is lot export focused and this reflects in performance (including cashflows), one can also see export trends of transformers from india

To watch for/better understand in next AGM

India positioning in global transformer supply chain (China is biggest supplier globally but may not be into customization etc and high on labor costs, as well as in general China+1 theme playing out as described in Virginia transformer mgmt interview above)

Shilchar technology differentiations and demand visibility

Capex plan given demand visibility is indeed long term, minor uptick in FA per this qtr bal sheet visible as well of near 4 cr - quantum unclear

High time required to commission a new plant - 1.5 to 2 yrs

and a 5.5 cr. entry in cash flow stmt. gives hope that mgmt. is working towards it. Given that they needed just 10 cr. for a 2x capex, this is significant.

I have been trying to understand the company profile but unfortunately could not find few points. Would appreciate if knowledgeable members following this company can provide their inputs…

Are any capex projects going on now or to be taken up in future? If yes then what is the timeline for completion?

Is capex cycle completed recently?

What’s the current capacity utilization?

Company is facing big competitors (BHEL, ABB, Siemens, etc.) who have better financial and technological strengths. How is it going to compete them?

What I am trying to understand is whether this performance has peaked or there is still some steam left?

If you read the thread in detail, most of your questions would be answered. They haven’t announced capex yet. Takes around 7-8 months for completion, as per management.

I think the kind of transformers required are more of the heavy duty type which a company like transformers and rectifiers/ voltamp would be making. I didn’t get that feeling looking at the product profile on their website . I might be wrong,not an industry expert.

CRGO steel constitutes approximately ~30% of the raw material cost of transformer. Thyssenkrupp has set up a plant in Nashik for 50K tonnes per year. But, India’s consumption of CRGO steel is around 300K tonnes per year. So mostly it is imported, not many companies in the world can produce this high grade steel.

More info here in this interview → CRGO steel is critical to India’s de-carbonization goals: Thyssenkrupp Electrical Steel -

Given demand and growth rates achieved last year this seems to be good timing. Cash flow & liquidity was never an issue for the co. TRIL in it’s call talked about very strong domestic market demand. Always heartening to see a smallcap company that is fiscally prudent but doesn’t miss out on growth opportunities. Looking forward to the AGM next week.

From AR : Domestic and Export demand continues to be very strong

A number of government initiatives to upgrade the current grids along with the installation of cutting-edge technology will fuel the expansion of the power transformer industry. Global demand is anticipated to be driven by an increase in the use of 100 MVA to 500 MVA products in transmission networks. The government has also announced large target for installation of renewable energy capacity. This is generating high requirement of transformers for solar & wind applications. Various governments in Middle East & Africa are also taking initiatives in renewable energy production which is driving high demand for transformers.

Some quick notes that I was able to scribble during AGM:

Capex:

Increasing capacity by 1000 MVA (25% increase from current 4000 MVA). Outlay of ~10 Crs and facility will come online by March’24. With incremental capacity, max revenue potential of ~500 Crs.

Also, market studies are going on for further bigger capex. Will be possibly initiated after current capex of 25%.

Projection for FY’24 and beyond:

Guidance for FY’24 is ~350 Crs. Current Order book of 300 Crs. and further RFPs in pipeline. Expected to be equally split between export and domestic. Aspiration to reach a top-line of 800 Crs. – 1000 Crs in next 5 – 8 Years.

Strong demand scenario both domestic and international markets.

In export markets, farsightedness of obtaining certain approvals is yielding result now for certain sectors. Export shortage cannot be easily fulfilled due to approval requirement.

Domestic: Equally strong demand. Massive reforms underway in power sector. Shift towards renewable is driving the demand. Massive infrastructre has been added and will continue the move for next 5 years. Also, cyclical capex in other sectors like Cement/Steel is driving demand. JSW buying strongly.

Q1’24 and Full Year 2023 specific snippets:

Q1 demand was soft. Even historically Q1 has been lowest and Q4 being highest. 60% - 70% demand was for export that’s why higher margin.

Misc:

All across demand by participants for better/frequent info dissemination by way of concall, investor presentation and business updates. Management acknowledges the need and commits for concalls post every result going forward.

Someone asked 3 year outlook so management stated they aspire to reach 800-1000 cr revs in 3 years. The period of 5-8 years was never mentioned.Even for renewable led demand they said 5 years.Other attendees can confirm.

They gave a generic statement saying “we will maintain margins”. But they categorically said Q1 margins were too high owing to large export skew. Prior to that,company maintained 22% EBITDA & with capacity nearing 100% util I would assume atleast 22% should be sustainable margins for Fy24.

At the AGM,the management had guided for 360 cr revenues in Fy24 & had clearly said that they don’t have capacity to generate more than 400 cr annual revenue(500 cr post expansion) Interestingly,in Q2 itself they are at ~425 cr annual run rate. Moreover,they had said that Q1 margins were one-off & won’t sustain since export share was too high. Yet they have done 28% EBITDA in Q2.

If people scroll up they will see that even for FY23 the management had guided for 16-17% margins & 225-50 cr kind of topline. So it seems clear to me that the promoter group likes to underpromise. It could also be that since the company has never made such margins they are being cautious in guiding the investor community since the improvement in EBITDA & GMs has been stratospheric in recent years. Company’s GMs have expanded all the way from 22-23% to ~40% in FY24. I had asked the management about this at the AGM however this question went unanswered. In any case,the execution of this company stands out vs peers. They are able to deliver high revenue growth alongwith strong profitability quarter after quarter. Stock has done very well but multiples have again fallen to 23x ttm or 17x(Q2 annualized) On the macro front things continue to align both domestically & internationally as @Dev_S has shared in some articles earlier.

Only issue with the company is that they aren’t willing to talk to investors outside the AGM which delays price discovery. No interviews to blogs or biz channels either. At the AGM we were assured of a concall soon. Hoping that now with marketcap at 1600 cr company can open up to the community.

Promoter sold 70,000 shares worth 20 crores on 30.10.2023 and 31.10.2023.

What is interesting is even though the promoters sold almost one percent of the equity through open market sale, there was no downside due to selling. Looks like some big investor/investors have entered around@2800 through block deals. Will be interesting to see in next shareholding pattern that who has entered.