Placeholder for some of the notes that I had put together while looking at different players…

Domestic Demand Drivers:

-

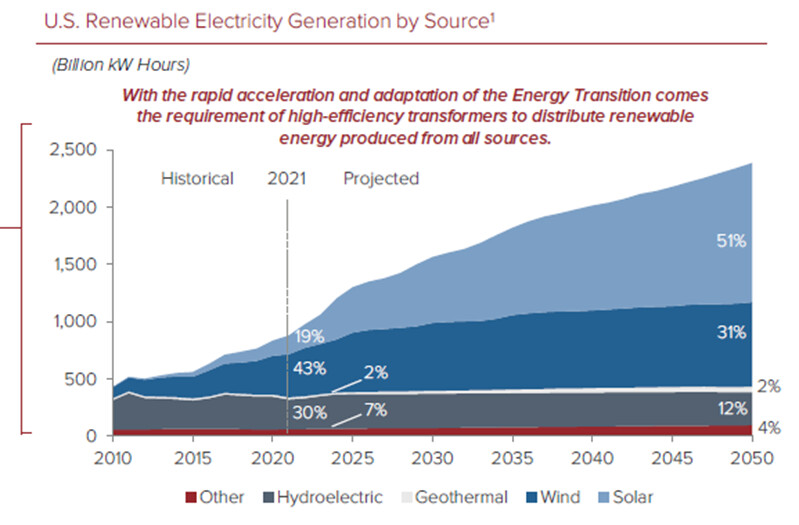

India’s power generation capacity is likely to be 623 GW in FY27 from 382GW end of FY22 (further to 865 GW in FY32). A significant increase is likely in renewable energy generation as the percentage of renewables in the generation capacity mix is expected to grow from 25% in FY22 to 57% in FY27 and 68% in FY32 while the overall pie itself is growing.

-

Policy support: Launch of $41bn power reforms funding in the budget should help kickstart power capex from FY23 after cleaning up discom balance sheets in FY22. The national infrastructure pipeline has outlay a capex of Rs 11,760 bn over FY20-25 towards the power sector.

Global Demand Drivers:

- Supply crunch in Key Markets. Wait times for some transformers have gone from weeks to over a year,1 and costs for finished transformers have soared in some cases by more than 400 percent since 2020. Predominantly due to CORG supply limitations.

- To combat the climate crisis and avoid the most severe impacts of climate change, the U.S. is committed to achieving a 50 to 52 percent reduction from 2005 levels in economy-wide net greenhouse gas pollution by 2030, creating a carbon pollution-free power sector by 2035, and achieving net zero emissions economy-wide by no later than 2050. Renewable energy is one of the focus areas.

Some Key Stats to understand the industry:

- Domestic market size in value terms: 13,000 Crs. (Power Transformer 6,500 Crs., Distribution Transformer ~6,800 Crs.)

- Dometic market size in value terms: 400,000 MVA

(based on a little dated report however not much capacity addition in the industry in last few years, rather capacity shrinkage due to implementation of stringent certification norms and few players going bust) - Realization: In the range of 7 Lac - 12 Lac/MVA depending on size, class and specs.

- Cost drivers:

- CRGO Lamination (H.S CODE:85049010, ) - ~23% of the cost; Price/MT – 3.50 lac/MT as on Q4’21;

- Copper - ~30% of cost

- Recent capex cost trend : Largely in the range of 70 lac- 1.25 Cr per 100 MVA for brownfield

Transformer and Rectifiers:

Manufacturing High Voltage Transformers viz. 220 kV - 1200 kV indigenously. Only Indian transformer company having NABL accredited lab for electricals steel testing. 80% Revenue from Power transformer

- Revenue by segment: Utilities - 51%, Industries - 43%, Export- 5%

- Capacity: 37,200 MVA

- Capex: As per Nov’23 concall, without any CAPEX, we can reach up to Rs.2,500 crores top line. Has planned Capex to the tune of 70 Cr. for enhancing the production capacity in the Changodar Plant in FY 2023-24

- Order Book: 2145 Crs (as on Sep’23), Book to bill - ~1.5x

- Revenue (FY23): 1360 Crs. (Growth 21%), Had seen significant 34% de-growth in H1FY24 (Y-o-Y). Still management has guided for full year similar revenue for FY’24 as it was last year.

- Margins: EBIDTA 9%, PAT 3%. Management guidance of EBIDTA moving to 15%+ here onwards.

- ROCE: 15%

- Working capital to sales: 51%,

- Cash conversion cycle: 143 Days,

- Equity dilution: QIP of 120 Crs in Oct’23.

In summary, working capital management had been one of the key challenges for the company. Debtor days has always been stretched (180 – 200 Days) due to customer profile (Utilities)/segment (power transformer). Situation was further aggravated due to wafer thin net margins of 1%- 3%. With the tailwind underway, TRIL may see meaningful swing in key ratios (ROE, ROCE) considering where they are today.

CG Power and Industrial Solutions:

6.4% market share in Power transformer and 5.4% market share in distribution transformer

- Capacity: Totally from 17,000 MVA now moving to 25,000 MVA. Operating at 100% CU

- Capex: Brownfield 11,000MVA capacity expansion plan at a capex of Rs1.26 bn. Incremental revenue potential of 850 Crs/year from capex. (nice 7x asset turn)

- Export 5% at enterprise level (Power segment is ~30% of FY’23 revenue)

- Order Book: 3363 Crs (as on Sep’23) specifically for Power segment, Book to bill – 1.66x

- Revenue (FY23) for power segment: 2023 Crs. (up 33%), H1FY24 revenue at 1131 crs. (19% Y-o-Y growth)

- Margin (FY23) for power segment: EBIDTA 12.9%, PBIT 11.2%. Significant margin improvement for H1FY24.

- ROCE (Power segment) – 61%

- Power segment EBIDTA is 13% now. ROCE 61%

- Debt Free, 662 Crs of cash+Equv.

- Working capital to sales: 23%,

- Cash conversion cycle: 13 Days

Text book example of what wonders good+capable management can do to a business and market position/valuations in turn. Murugappa group took over a 5% ROCE, ~1000 Crs LT debt business in late 2020. Turned it around into 45% RoCE, zero debt, 711 Crs cash, negative working capital, Dividend paying business – all in 3 years. Even, here onwards business direction and commentary looks strong (valuation stretched though).

Voltamp:

Voltamp operates in three different segments: power transformers (35% of sales), distribution transformers (45%) and dry transformers (13%). Oil-filled transformers constitute 81% of sales and dry transformers ~19%. Very wide end user industry sector thereby mitigating sectoral uncertainty. Max Sectoral exposure 16% is for steel/metal, no other

- Revenue by segment: 85% of revenue comes from private customers

- Client concentration: Top 10 customers 26% revenue

- Export: 2.36%

- Capacity: 14000 MVA, 84% Capacity Utilization

- Capex: Recently did capex to increase capacity by 1,000 MVA (de-bottlenecking). Management indication of further increase capacity by 2,000-2,500MVA depending on demand

- Order Book: ~1400 Crs orderbook as on Sep’23 (improved from 900 Crs as on March’23)

- Revenue (FY23): 1385 Crs. (growth 22%)

- Margins: EBIDTA 16.70%, PAT %14%

- ROCE: %19.60

- Debt Free balance sheet

- Working capital to sales: 23%,

- Cash conversion cycle: 142 Days

- Equity dilution: In Sep’23 promoters has sold 12% of holding (560 Crs.). Contrary to what rest players are doing (QIP/debt/preferential allotment) at this juncture of good times.

Positive CFO for past many years is remarkable. Significant improvement in realization from ~ 7lac/MVA as on Q1’22 to 12lac/MVA+. Very tight working capital management. Cash reserves of ~600 Crs helps to have creditor days in control thereby extracting better margins.

Just two data points should summarize the management philosophy and pedigree:

- No LT debt in last 10 years in such cyclical and working capital extensive industry.

- In last 10 years, creditor days has been below 3 days ALWAYS.

Bharat Bijlee:

Bharat Bijlee has a state-of-the-art plant with a production capacity of 15,000 MVA and a full-fledged testing laboratory which is NABL accredited. It offers up to 200MVA, 200kV, 3 phase transformers and caters to State Electricity Boards, Utilities, PSUs, Industries and overseas customers.

- Export: 1.70%

- Capacity: 15,000 MVA

- Capex: No info in public domain

- Order Book: 1076 Crs.

- Revenue (FY23): 646 Crs for transformer segment, growth 4% Y-o-Y, H1FY24 has significant 112% growth

- Margins: PAT 5.87%

- ROCE: 15%

- Debt/Equity - 0.5

- Cash + Equivalent – 324 Crs.

- Working capital to sales: 39%,

- Cash conversion cycle: 145 Days

- Investment of 860 Crs in equities as on March 31st 2023.

Meaningful land bank at current Aeroli plant. The company’s manufacturing facilities are located in Airoli, Navi Mumbai on a 193,000 square meters campus, with a working area of approximately 50,000 square meters. Possibility of monetization or brown field expansion.

Shilchar Tech:

Manufacture distribution transformers ranging from 5 KVA to 3,000 KVA and power transformers ranging from 3 MVA to 15 MVA. Domestically, Shilchar generates a major portion of its revenue by manufacturing transformers mainly for power and energy sector (with major portion from domestic renewable sector i.e. solar and wind forming around 50%-60% of net sales).

- Revenue by segment: Export 52%, domestic 48%

- Customer concentration: top five domestic customers forms ~54% of its domestic sales in FY23 [FY22: ~44%; FY21: ~72%].

- Export: 52% of revenue FY23, 25% of revenue in FY22. Exports grew from Rs.45.70 crore during FY22 to Rs.144.83 crore during FY23

- Capacity: 4000 MVA

- Capex: 1000 MVA (as per AGM comments, this may be phase 1 of capex and may look at increasing capacity further)

- Revenue (FY23): 280 Crs. (56% growth), H1FY24 revenue 173 Crs. (47% growth)

- Margins: EBIDTA 25%, PAT 15% | PAT improved significantly to 23% in H1FY24

- ROCE: 54%

- Debt Free, 28 Crs of cash

- Working capital to sales: 37%, Cash conversion cycle: 86 Days

Overall, Transformer industry had significant capex between 2007 - 2012 (2.5x capacity addition). However, went into an overcapacity and demand slump situation thereafter. Total manufacturing capacity has remained stagnant (rather has declined) for a decade.

This decade long demand slow down situation has resulted into under investment into manufacturing capacity. With multiple growth drivers ahead - both domestic and gloabal, industry is finding itself in a sweat spot.

Regards,

Tarun

Disclosure: Invested in Shilchar, transactions (average-up) in last 30 days