Below is from the investor presentation:

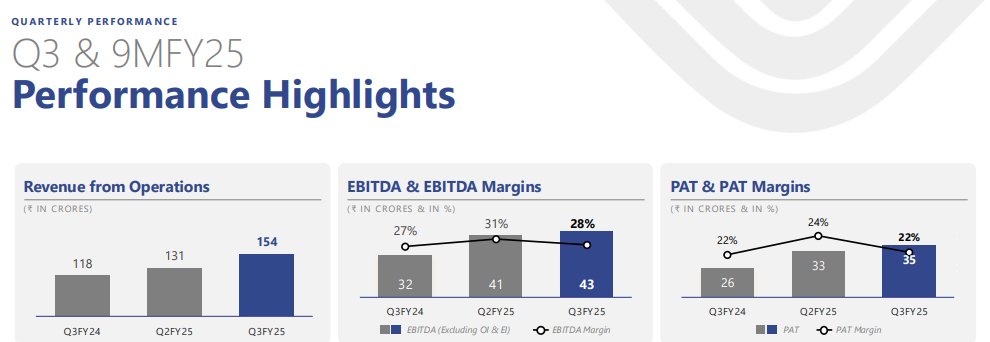

As per the same, the new capacity is fully utilised in Q3 which gives revenue of ~155CR with PAT margin of 22%.

If we extrapolate it to full year, it would be ~620CR (which management guides to 750-800 and i assume they would be right but it cannot be more than this) and considering 800Cr rev, the PAT to be ~180Cr.

With this, the stock runs at the 25-30 forward PE, which is quite expensive given no further growth visibility, until management announces further expansion plan.

Disc: Not invested but got interested in overall sector story and recent corrections in all these stocks. Tracking others too, but still feel these like SHilchar, Indo Tech, Danish are quite expensive at these levels.