Share India Securities Ltd. (SISL) is currently engaged in the business of equity broking, investing and trading activities. Along with this the company is also providing the services as a Depository Participant, Research Analyst, Mutual Fund Advisor/Distributor and also an application has been filed with Securities and Exchange Board of India for the registration of Company as a Portfolio Manager. SISL got registered with SEBI as Stock Broker (Member of BSE) in the year 2000 and started the Stock Brokering operations. Later during the year 2007-08 it got registered as a trading and clearing member of Bombay Stock Exchange (BSE). Post the merger of the company it got registered with SEBI as Stock Broker, Trading and Clearing Member of National Stock Exchange of India (NSE) in the year 2012. With the introduction of the Future and option segment into the Indian capital market the company became Member under future & Option (F&O) Segment also. Currently, The Company is providing broking services in Equity, Currency derivative and Future & Options segment of National Stock Exchange of India Limited and BSE Limited

To part finance its working capital, sales and marketing plans, branch/distribution centre expansions and general corpus fund needs, SISL is coming out with a maiden IPO of 6432000 equity share of Rs. 10 each at a fixed price of Rs. 41 per share to mobilize Rs. 26.37 crore. Issue comprises fresh equity issue of 5932000 shares and offer for sale of 500000 shares. Issue opens for subscription on 21.09.17 and will close on 26.09.17. Minimum application is to be made for 3000 shares and in multiples thereon, thereafter. Post allotment, shares will be listed on BSE SME. Issue is solely lead managed by Hem Securities Ltd. and Bigshare Services Pvt. Ltd. is the registrar to the issue. Issue constitutes 26.33% of fully diluted post issue paid up equity capital of the company. From incorporation till June 2010 it issued equities at par. Thereafter, it raised further equity at a fixed price of Rs. 33 per share in January and September 2015. It has also issued bonus shares in the ratio of 3 for 1 in July 2017. Post issue its current paid up equity capital of Rs. 18.49 crore will stand enhanced to Rs. 24.42 crore.

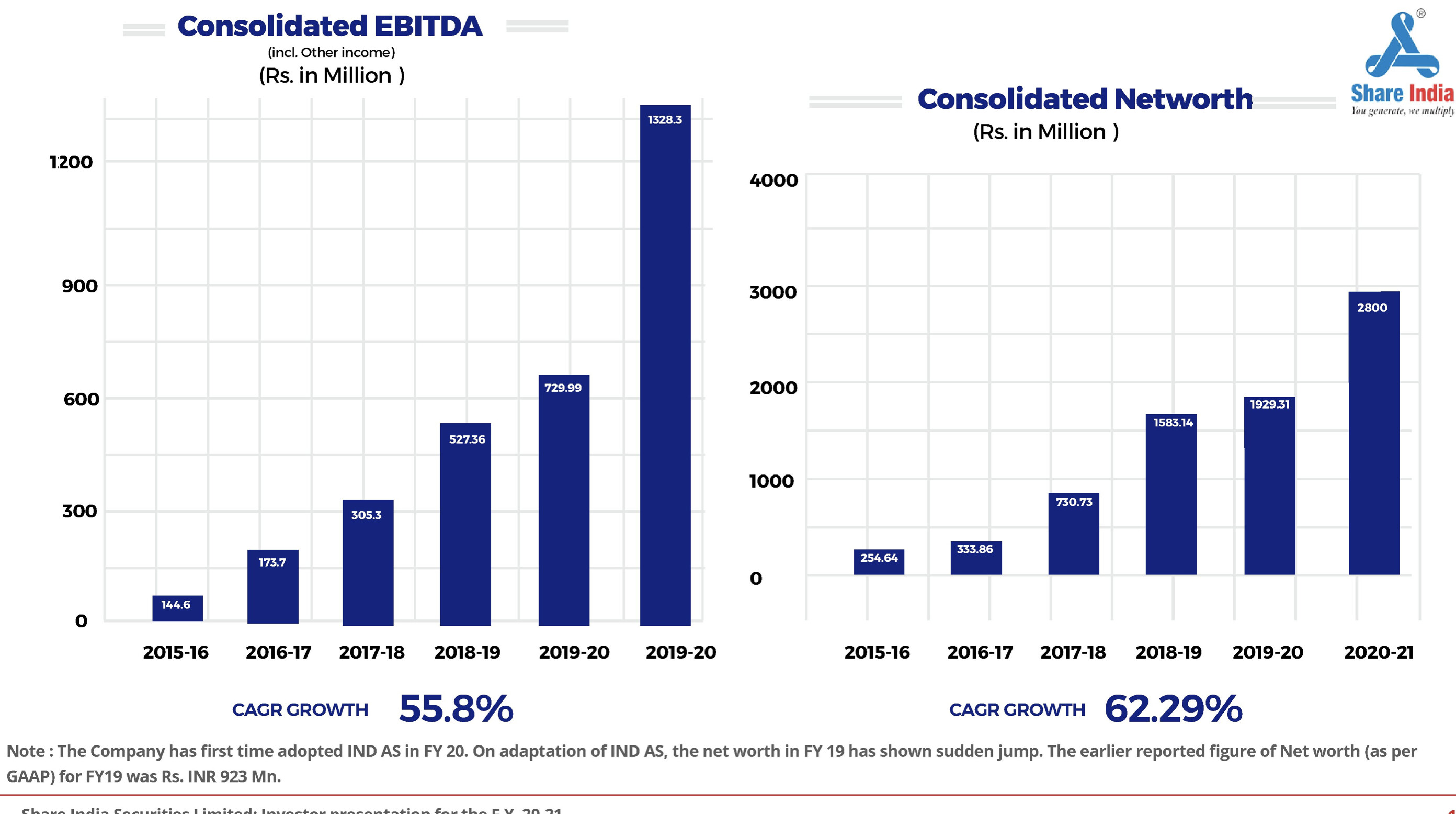

On performance front, SISL has (on a consolidated basis) posted total income/net profits of Rs. 73.99 cr. / Rs. 6.28 cr. (FY16) and Rs. 110.09 cr. / Rs. 8.03 cr. (FY17). Thus it has shown growth in top and bottom lines. For last two fiscals it has posted an average EPS of Rs. 4.04 on an equity base of Rs. 4.62 crore. It has reported average RoNW of 24.33% for past two years. Issue is priced at a P/BV of 2.27. If we attribute latest earnings on fully diluted equity post issue, then asking price is at a P/E of 12.

I went through the DHRP and had couple of observations on the company.

- Most of the income derived by company is fron trading of stocks. Last year it was around 98 Crores out of ~110 crores. Although they have not made any loss in trading in last five years but this looks to me a very high risk item.

Can somebody throw some light on trading activity of such companies.

- The salary income to promoters and their relatives suddenly increased to ~3.5 crores from ~20 Lakhs in financial year 2017.

3 Likes

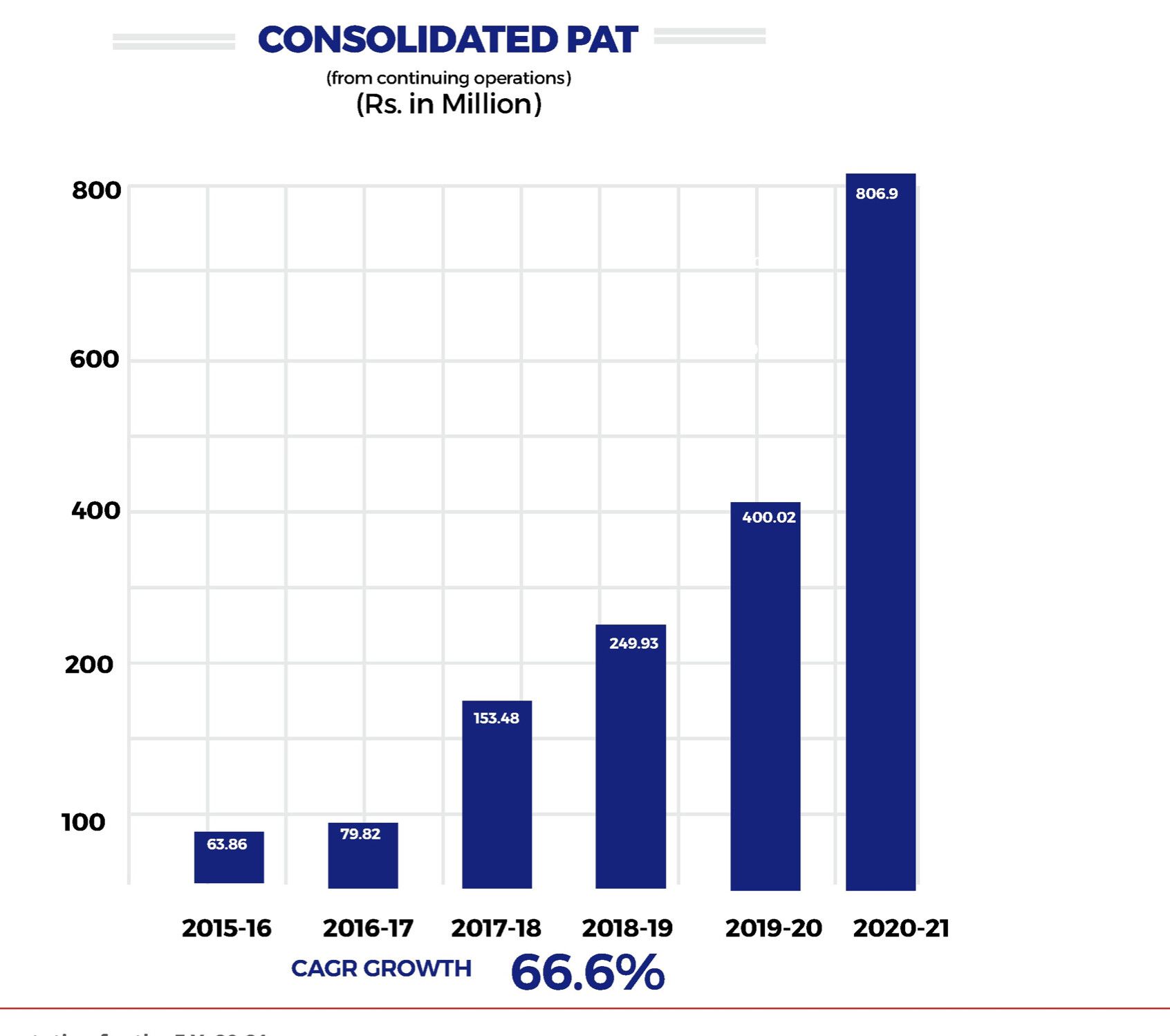

The annual results are showing consistent growth. They have added a subsidiary NBFC to the company and looks like they want to increase their product offering. One major risk is a major part of their revenue is from share trading activities which is high risk business. They have recently added a subsidiary called windpipe finvest ( having NBFC licensce ) so that should be interesting to see what they do with it.

another issues is they seem to be regularly buing shaes of another listed company Anisha Impex. Not sure what is the rationale.

Disc: Invested since 50 levels.

1 Like

This company deserves more attention than its getting:

I had bought this company around 50 and sold out in 2019 around with a modest profit. The reason of selling out was that I saw 90 % of their revenues are coming from stock trading activities and not from Fintech activities ( broking / mutual funds etc ) which they are claiming to be. If one looks into 2020 annual report the situation remains the same. 90% of their revenues comes from stock trading activity. So if someone is buying this company basically you are betting on their stock trading skills more than anything else. Stock has gone up 10 times in last one year and now people in social media and other places are showing this as the next big thing. I would be extremely careful about buying at these prices

1 Like

They are into algo trading a lot, beside this says hedged positions , need to go thru concalls to clarify this point. Good point indeed.

Last concall was in 2018 which i attended. Dont think they did con-calls after that. Even the investor presentation they gave out did not report this or give the breakdown of their revenues. I am presuming they are using the profits of trading activities to acquire other small finance/broking companies. Well known TV anchors / social media handles have started talking about this company after 10x increase in prices.

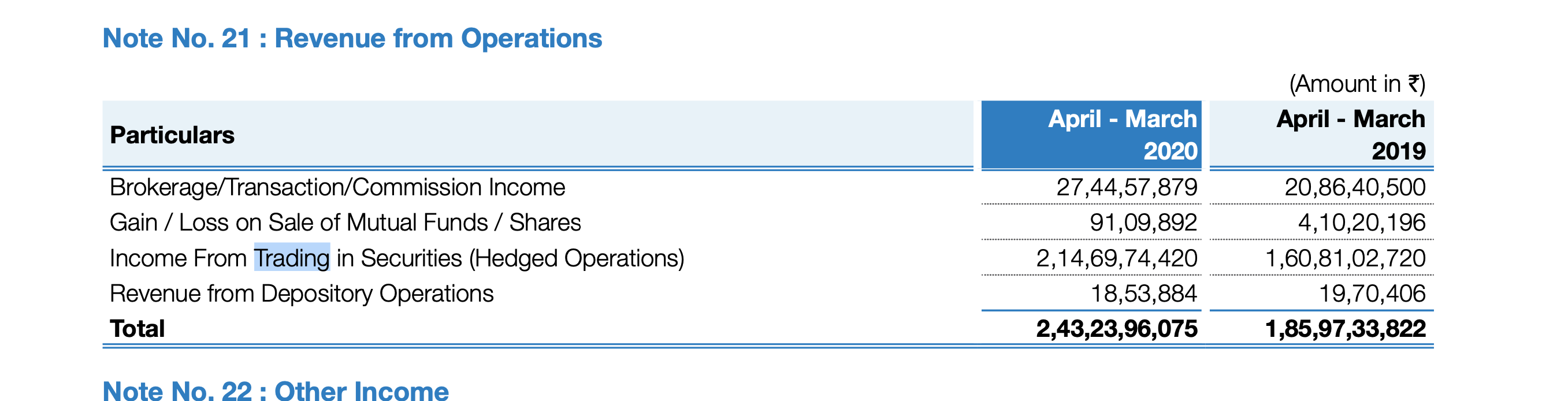

Can you share the source of above screenshot ? I could not find breakdown.

see page no 92 of 2020 annual report.

I may be mistaken here but it seem like its about trade activities for client , which is part of core business, if it was really something worrisome should have been asked in their concall on June 1:

Not meaning to counter here but a bit curious as even I am a bit in doubt after your statement

Counter arguments are always welcome in any discussion. Basically what i understood from the concall is that they are claiming to have some sort of algo trading platform/software which is helping their clients to make a lot of money and hence this is where they claim they are different from other brokers. Now personally I also do algo trading in big volumes on intraday basis using platform like tradetron connected with Zerodha - which to be honest is giving me decent returns. Brokerage remains the same with zerodha and some other expenses I have with tradetron platform. However I am not sure what kind of revenue model they have with their HNI clients( could be profit sharing basis which is generating this huge income ) . But even if we accept they have some sort of path breaking software/technology it is very clear this part of their business accounts for 90% of their revenues. Now all im saying is if someone is investing in this company then one should understand that this is their core business that is generating their revenues as of now and future of the company will depend upon the success of this part of their business.

Yeah, I agree with your points, so far management has been able to walk the talk and flagged the red pointers too where they needed to flagged, quite transparent so far what I have understood, one good point is they are diversifying already and doing go progress on those fronts too.

That’s such a good observation and even I had the same exact question!

And I found valuepickr through this, so thank you.

It was so surprising to find that most of their revenue comes from proprietary trading.

Even the brokerages, received from traders using their platform only constitutes a smaller share of the revenue.

I think all these efforts to move into Insurance broking, NBFCs, merchant Banking etc, are to diversify and reduce exposure to their trading based revenue.

I included their other income - interest income and income from dividends which were recently reclassified in the March-21 results, into their main operating revenues because these were from NBFCs and their investing activities etc, so it seemed sustainable.

Despite including the other income, the trading activity still consumes the lion’s share of the revenue, and that’s definitely a questionable red flag in the future prospects of the company.

Here’s a chart I made using Financials from Annual Report FY-20.

1 Like

If prop trading is such a large part of the pie, should we be cautious about recurring revenues? How is management able to guide such high revenues and profitability in that case?

As I also do fair amount of algo trading , I reached out to them on their website contact nos and emails asking for details and showing interest in opening an account. No one reached back to me from their end. If they have some good trading skills which is helping their clients make so much of money I would want to be part it. Maybe other forum members can reach out and see if they have a viable trading product.

2 Likes

I am shareholder and reached out few weeks back, no-one reached out to me too.

1 Like