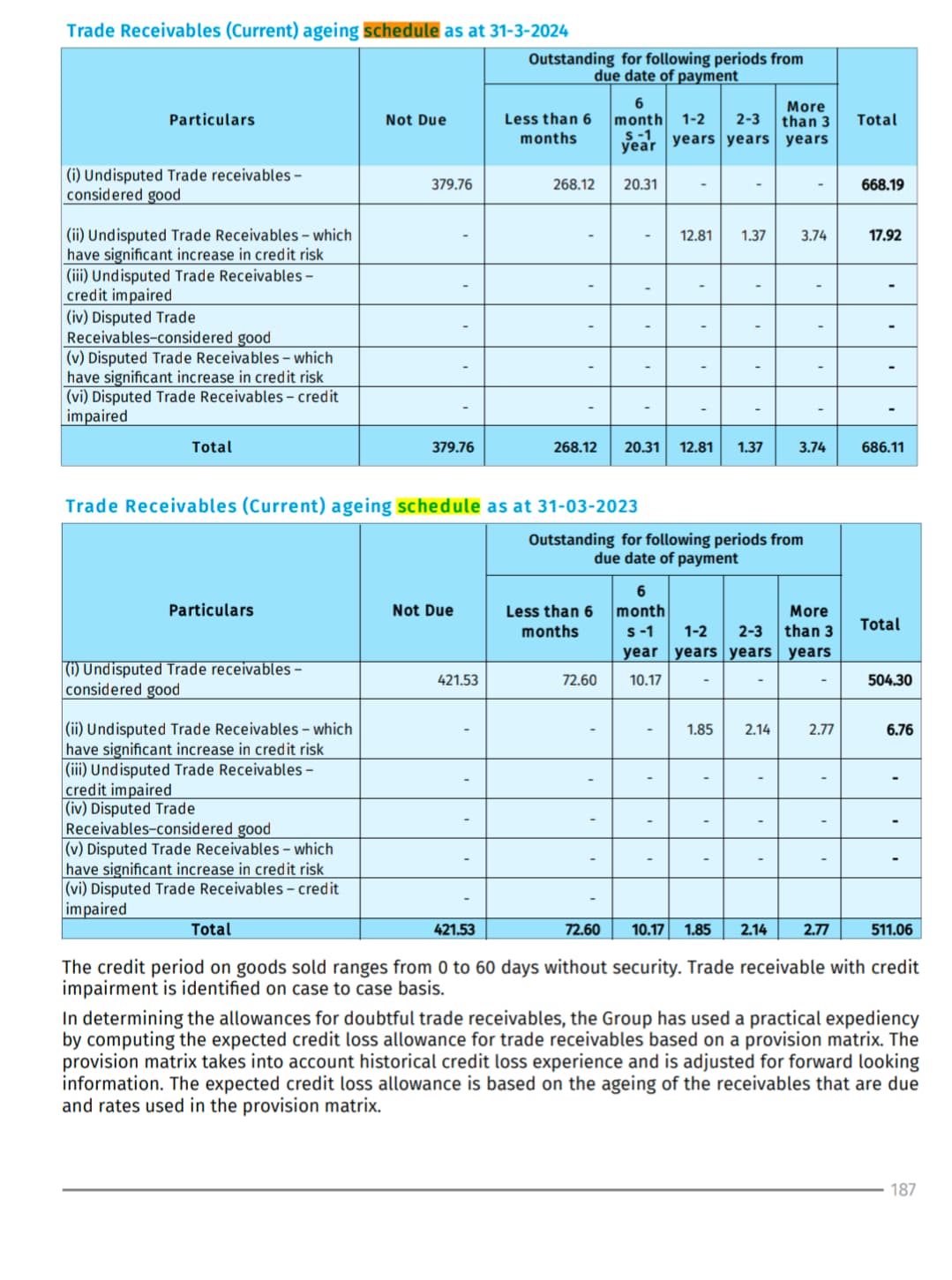

#Shankara Building Products.Annual Report for 2024 shows a significant increase in trade receivables outstanding for a period greater than one year, which has risen from Rs 6.76 crores to Rs 17.92 crores in FY 24.

1 Like

Even though trade receivables over 6 month is a key factor, but in this case the annual sale is 4800Cr. So compared to this, 18Cr is very small.

2 Likes

Last year profit was 81 crore. Trade receivables over 6 months is 38 crore and above 1 year is 18 crore. I would be concerned about my business model if I were the retailer selling on credit.

2 Likes

Anyone attended the conference call of 9 August? If yes, please upload the key points please.

1 Like

One thing i noticed there interest cost is increased this quarter

may be they have foreign debt,they are not declaring

1 Like

Management explained that the high interest payments are due to increased trade payables. They also mentioned that this situation will persist for another couple of quarters. Essentially, they lack pricing power, and as a low-margin trading business, they are being squeezed between their buyers and sellers.

Disclosure: Sold all my holdings today.

2 Likes

Ok,now their is no pricing power

Majority revenue still comes from steel trading and there is no pricing power there.

But my thesis for investment in Shankara has been -

(1) Growing Non Steel segment +

(2) Demerger value unlocking.

Both are still available. My concern is whether they can continue to grow non steel segment proftably and would their addl capacity at manufacturing can prove to be beneficial.

Let me know if anyone has any thoughts on this.

2 Likes

I agree, my thesis was also that (20% sales and 25-30% profit).

But with growth in receivables, high-interest and low-cash conversion, it would be difficult for them to scale without outside capital.

3 Likes

What is the time line for demerger? majority of revenue is still coming from steel business which is a comodity tradinf business. With steel price correcting their topline is bound to face headwind. But the non steel business is doing great. So demerger will be great thing.

Disclosure: not invested.

Yes that thesis only valuation was good enough but nothing worked

Just curious to know who will be the buyer of Shankara buildcon (existing entity) post demerger… this division will have low margin / low ROE business. Generally on demerger its assumed that existing company will trade at current valuation and resulting company will trade at higher valuation but in this case this does seems to work.

march 2025 may be tentative month

1 Like

In latest con call they mentioned the timeline till March 25 now it’s in NCLT after that I think 2 steps more

In Q1’25 results call, the mgmt said that they want to do 1000cr revenue in non-steel in 2-3 years. And that would be 25-30% of the total revenue. Since non steel revenue is part of only marketplace, and if I reverse calculate, then market place revenue comes to about 3300 to 4000 Cr…in 2 to 3 years. The marketplace revenue in FY24 was 3836 Cr.

Where did I go wrong? Or maybe the contribution range mentioned by mgmt is erroneous?

2 Likes

Time horizon: 3 Years

Current revenue: ~5000 cr

Expected growth of revenue: ~30%

Expected revenue after 3 years: ~11000 cr

Expected Quarterly revenue after 3 years: ~2800 cr

30% contribution from non steel: ~1000 cr

Rationale for math on the number

2 Likes

Marketplace do sell Steel as well. Steel is still the majority. They sell the manufactured steel plus trade others’.

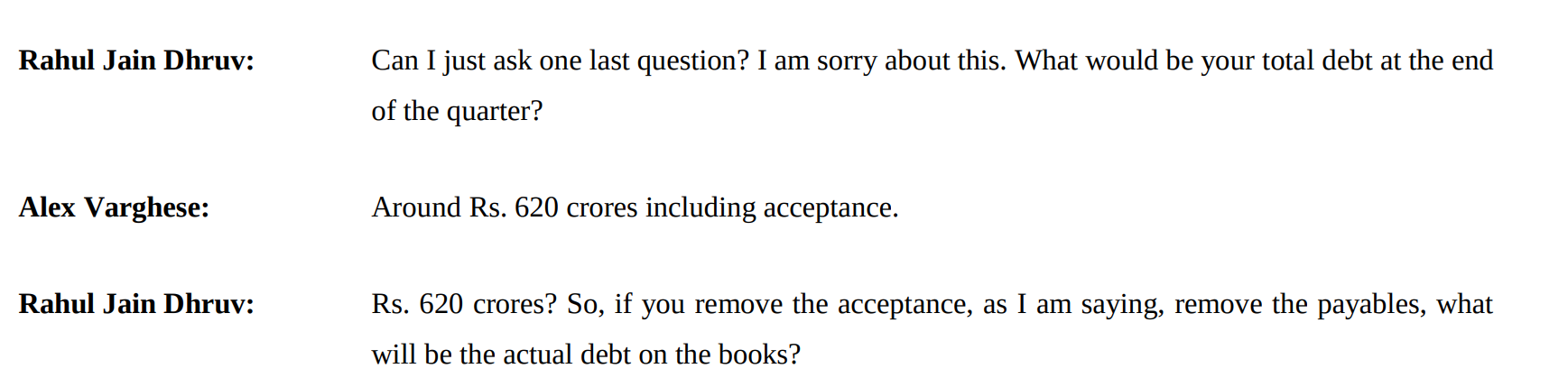

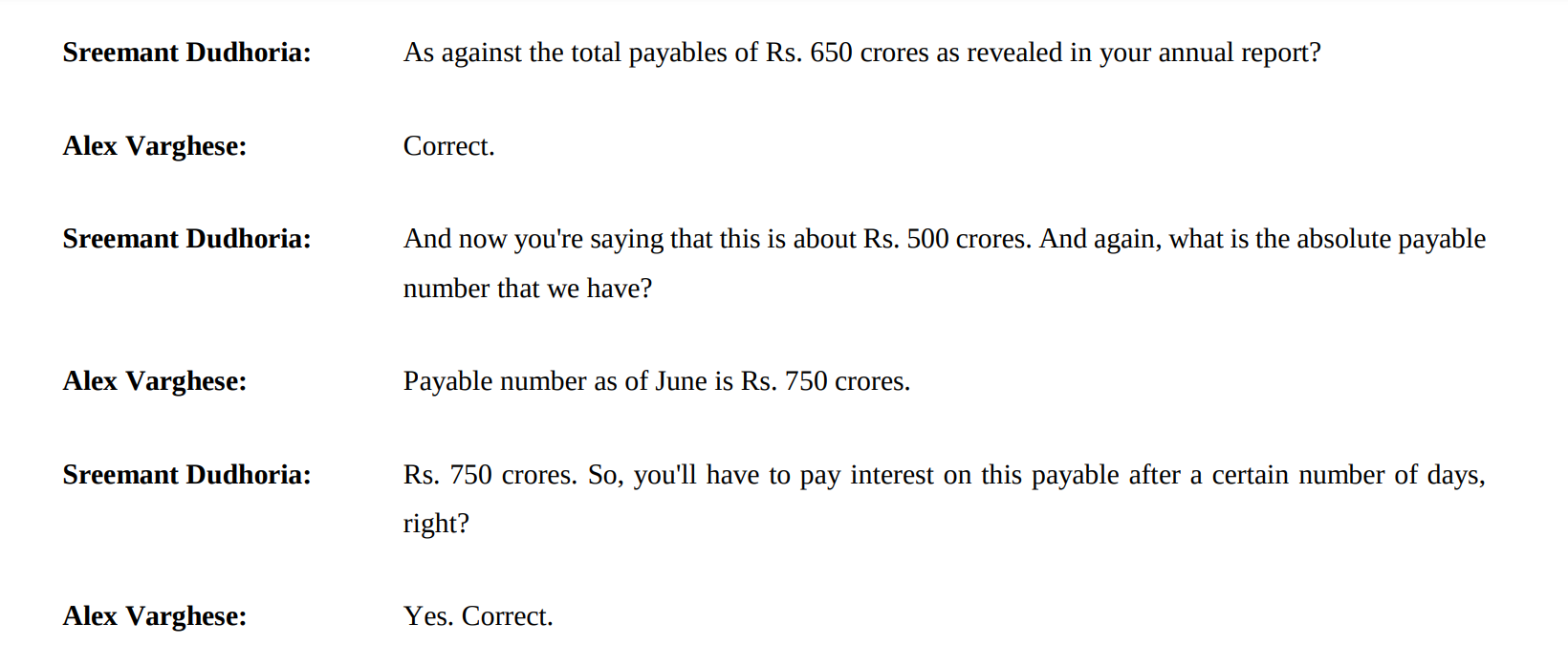

was going through the Concall transcript, they have off balance sheet (payable) debt which is 6x of the debt on book. Razor thin margins and most of it will spent in interest costs. Seems like a gruesome business.

Disc: Exited fully

9 Likes

If payables are high then so is receivables 686 Cr.

1 Like