Hi is there any update on the NCLT meeting scheduled on 26th May?

Any Particular reason why the stock is going UP ?

- demerger ?

- Discounting the future Cashflows?

- or anything else?

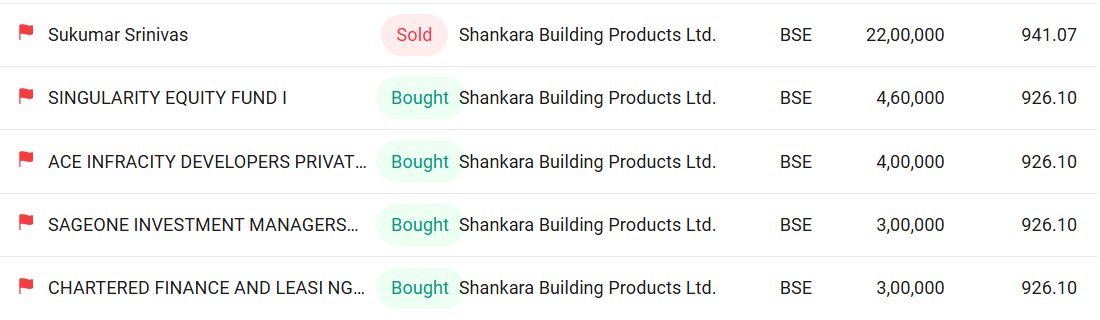

Any opinion on promotor sales and the funds that bought in !

1 Like

3 Likes

Does this help in anyway like knowing what big investors are buying

No., unless you’re a cloner like Mohnish Pabrai

1 Like

They finally received NCLT approval for demerger on 22nd Aug.

2 Likes

Hello,

Can anyone explain me the business model of the company in simple terms? I have the following doubts, while going through the investor presentation:-

- There are two businesses (which are going to be demerged). One is the manufacturing business and other is the market place business.

Now in the manufacturing business, the company manufactures steel tubes, strips, roofing sheets and steel pipes. Am i missing any other products here? While among the suppliers there is APL Apollo, JSW, Hitech, Jindle etc. What company buys from these suppliers when it is manufacturing the above products inhouse? - The market place business is both online and offline? I have searched their website (buildpro) and it offers products only in the tube category (round, square and rectangular in various thickness and sizes). Not a single product in sheets, tmt and structural steel. The online products are self manufactured or bought from suppliers mentioned above?

- The offline market place works through physical stores (92 operational store and 32 fulfillment centers as of Q4 25 IP) with steel and non steel products. What is the difference between operational and fulfillment center? Does both steel and non steel products sold from all these store and fulfillment centers? As per IP there are 18 hybrid stores and 13 dedicated non steel stores, so the rest are only steel stores? Is the online orders fulfilled through the physical stores and fulfillment stores or from warehouses?

- What is the retail and non retail selling business? I mean who are the customers in retail and who are the customers in non retail? Company sells products to these customers through online and physical stores and fulfillment centers or there is any other mode of selling the products?

- What is 5.1 lakh sq feet area in retail? The area of physical stores and fulfillment centers?

- What are the processing units as indicated in the IP? Are these in units work under the three subsidiaries of the manufacturing business? What these processing units does?

Forgive me for simple questions (if they sound stupid) .

Disc.: not invested and only studying.

3 Likes

What’s so wrong with the demerger sanctioning news of Shankara?? Why is it down 75% today?!

that means that valuation is going to the demerged entity Shankara Buildpro

So incase someone held shares of Shankara, they’d get the shares of the Demerged entity as well?

Yes, The date of listing the demerged entity is not et confirmed but will happen soon.

Hello, I have studied the business and here is my shot at valuing it.

-

SBPL: Shankara Building Products Limited is the demerged entity. It basically is in the field of manufacturing steel products like steel pipes, tubes, pipe fittings, color coding roofing products, cold rolled strips etc. It has 3 Manufacturing subsidiaries VPSPL, TVSPPL and CRIPL. VPSPL has tube and cold rolled strip manufacturing at Bengaluru. TVSPPL has steel pipes, tubrs and pipe fittings manufacturing facility at Hyderabad. CRIPL manufactures color coated roofing products at various facilities in multiple southern cities ( not sure if these are contracted or owned, as can’t find the info).

The current capacity utilization stands at 50% which management wants to increase in the near future and also will expand its direct sales (till now it sold/supplied its products to market place business).

Working capital (WC) is around 17 days.

Company has multiple warehouses which are spread across southern, central and western india. The warehouses were shared between SBPL and SBL (the resulting company- Shamkara Buildpro Limited). After demerger the warehouses will go to SBPL and can be rented by SBL on rent basis at arm’s length agreement.

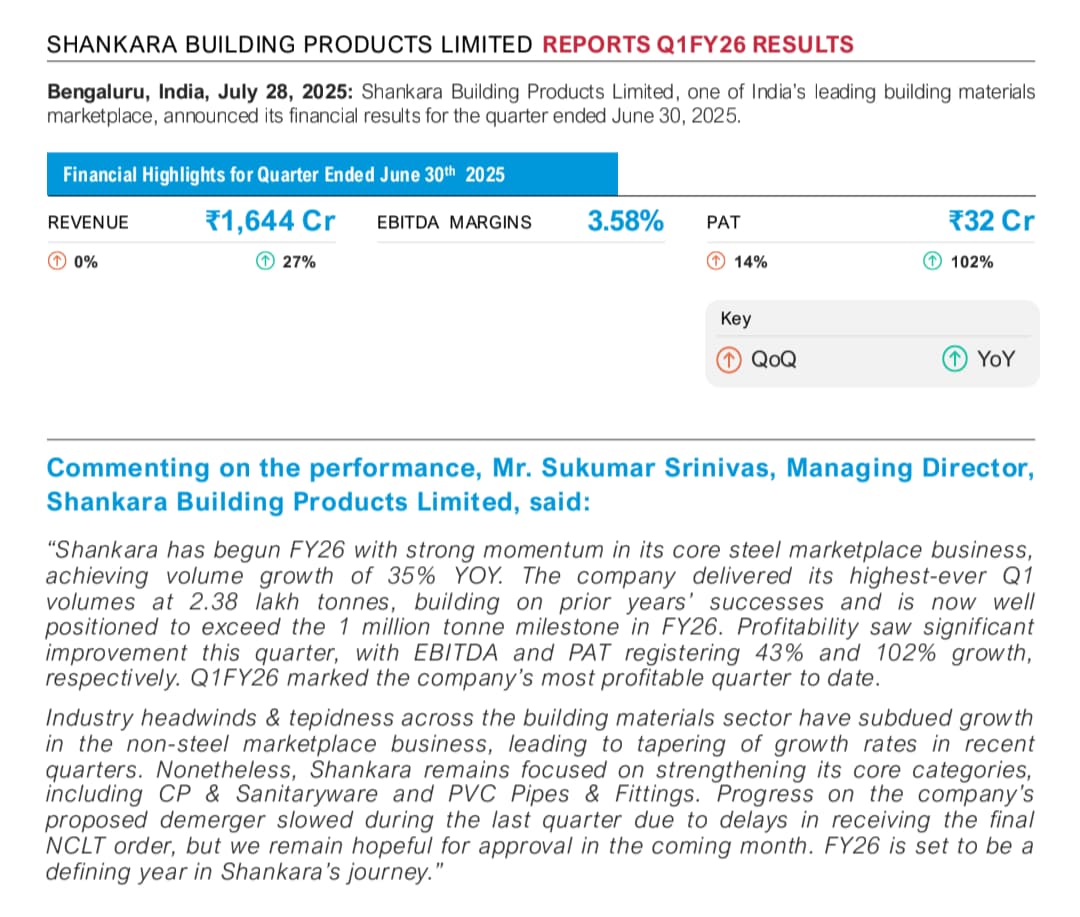

The management has guided 20-25% top line growth with EBIDTA margins of 2-2.5 %. The Q1 26 revenues were 323 cr. Taking annualized revenues at 1400 Cr considering improvements in capacity utilization and warehouse rental income.

EBITDA @ 2.2%= 30.8 Cr

Finance cost= 3 x 4= 12 Cr (Q1 26 Conference Call)

Depreciation= 2 x 4 = 8 Cr (Q1 26 Conference Call)

NPBT= 10.8

Considering 20% tax, NPAT = 8.1 Cr

Total equity= 2.42 Cr

EPS = 3.35

Price at 15 PE = Rs 50; Mcap= 121 Cr

Price at 20 PE = 67; Mcap= 162 Cr

Price at 25 PE = 84; Mcap= 202 Cr -

SBL- Shankara Buildpro Limited is the resulting entity. It is also called the market place business which is divided into retail (cash and carry business with small retail customers) (Retail contributes around 55% to the sales) and non retail ( Enterprise- large customers, contractors and OEMs; Channel - dealers and other retailers through branch network; which includes wholesale and project contractors which results in 30-40 debtor days stretching the WC (non retail contributes 45% to the sales) (depending upon customer type) and steel and non steel (depending upon material sold).

Currently (as per Q1 26 IP), there are 126 stores/centers from where the company sell it’s products which are further divided into 93 operational stores and 34 fulfillment centers which are there to fullfill the e commerce orders and along with warehouses also stores extra SKUs which cannot be fulfilled by operational stores (need to confirm this, have assumed this).

Added 2 fulfillment centers in Q1 26 and plan to add another 4 stores in Q2 26.

Currently major revenue comes from south india (company’s strong hold) but gradually company is expanding into west and central india and will expand in north and east india in future.

The steel products (2-2.5% EBITDA margins) sold include ERW pipes, HR/MS Tubes, Galvanized steel pipes, Hollow structural sections, mechanical tubing, long products including MS angle, sq rods, round rods, long S, MS channel, Beams, tubes, round rods, Flats include MS sheet, GC sheet, CR sheet, GP sheet, HRPO sheet, PPGI & PPGL sheet.

The non steel products (margin assertive- 6-6.5% EBITDA margin) include Chrome plated (CP) and Sanitaryware, tiles (Fotia- own brand but contract manufactured by third party), surfaces, PVC pipes & fittings, electrical & lightings, kitchen doors & hardware, plumbing and interior and exterior finishes, construction materials etc. The material is of different brands.

The company is transitioning existing steel stores to hybrid (steel plus non steel) and there are 18 hybrid stores as of now. (Q1 26).

Dedicated non steel stores are 13 so far (Q1 26).

The next leg of sales growth will come from growth of sales through existing stores (SSSG- same store sales growth) and newly added stores.

The stores and centers have 1 lac SKUs but stocking only 15-20k SKUs rest is fulfilled by warehouses/fulfillment centers. (Clarity regarding the exact role of fulfillment centers is needed).

The management has guided for 30-35% growth in market place business but i would take that with a pinch of salt as company already doing business of 5700cr (SBPL plus SBL in FY 25), doubling it will need more efforts and expansion compared to last few years.

Management has guided for 3.5-4 % EBIDTA margins (currently at 3.3 and will grow towards 4% with increasing contributions from non steel products and higher margin steel products like flats)

Following data is by Q1 data extrapolation.

Revenue: 1500 x 4 = 6000 Cr

EBITDA: 6000 x 0.035 = 210 Cr

Finance cost: 9 x 4 = 36 Cr (Q1 26 CC)

Depreciation: 2 x 4 = 8 Cr (Q1 26 CC)

NPBT: 166 Cr

NPAT: 166 x 0.75 = 124 Cr (assuming 25% tax)

EPS: 124/2.42= Rs 51

Price at 15 PE = Rs 765; Mcap= 1850 Cr

Price at 20 PE = Rs 1020; Mcap= 2470 Cr

Price at 25 PE = Rs 1275; Mcap= 3085 Cr

Price at 30 PE = Rs 1530; Mcap= 3700 Cr

Mcap before demerger is 2300 Cr at a price of Rs 950.

Therefore price after demerger should be SBPL at 15 PE and SBL at 20 PE (at max) = 121 + 2470 = 2600 Cr.

In my personal opinion the demerger doesn’t make much sense as the two subsidiaries complemented each other well and overall the individual subsidiaries were not big enough (so having managing issues) to warrant demerger.

Also the employee cost will increase as although MD will be common for the companies but other senior management will be additionally hired for one of the company.

This is my first detailed post on Valuepickr. Kindly forgive my mistakes and do provide feedback and comments.

12 Likes

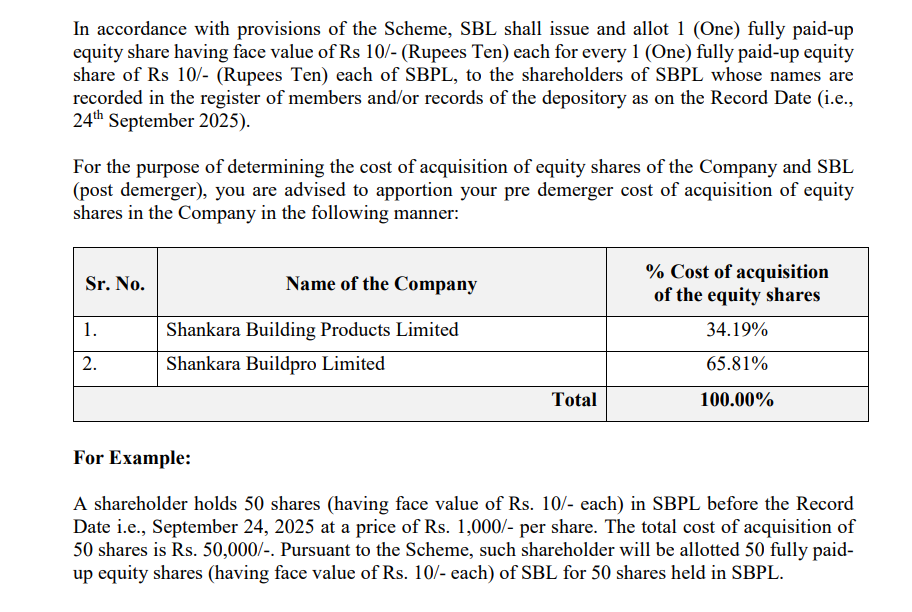

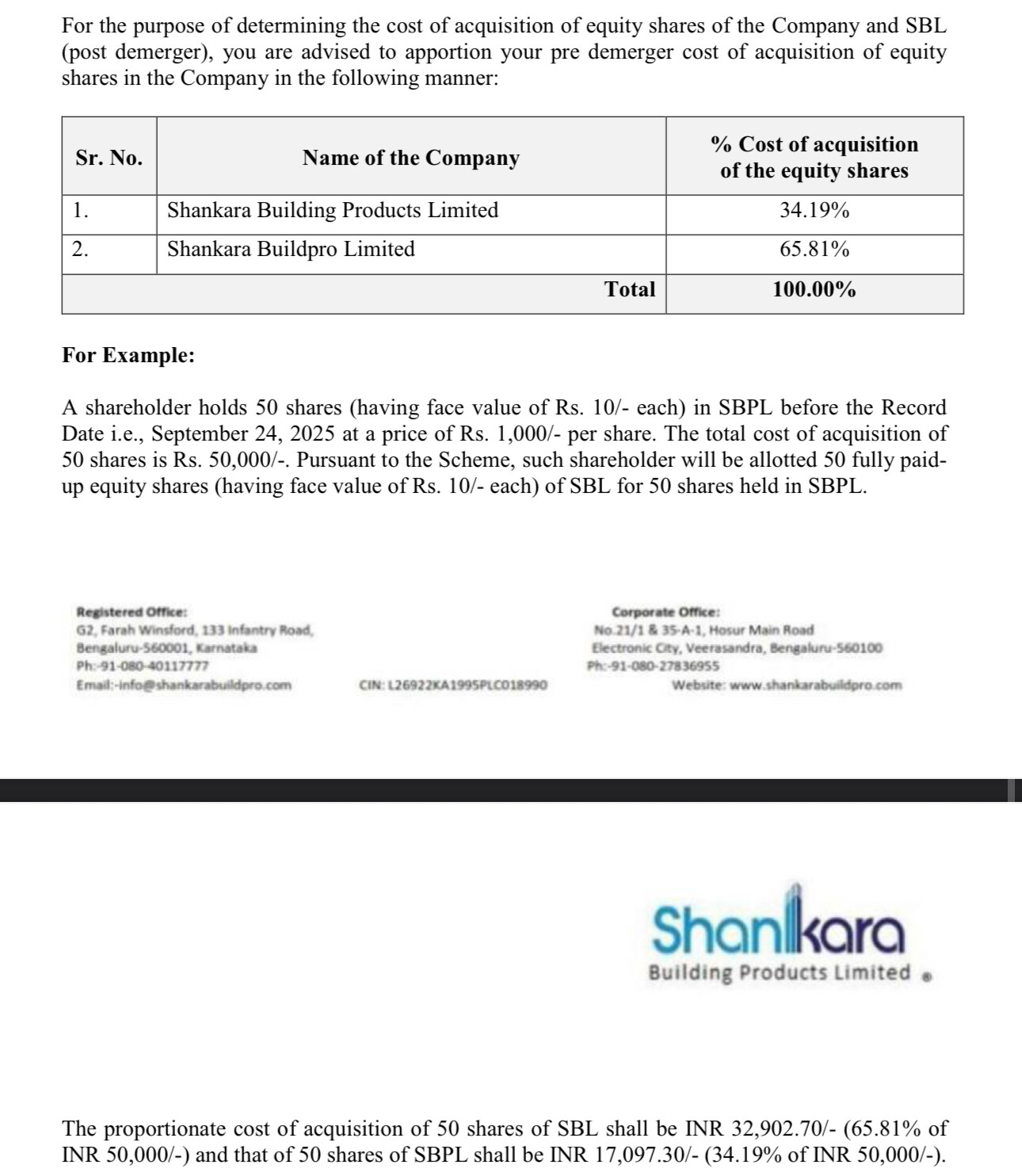

Hi thanks for the detailed explanation of the business model of both the entities. What I fail to understand is that if SBL was supposed to have 34.19% of the cost of acquisition, so from what I understand by this is if the LTP before the demerger was say 950 then 34%of 950 should be the price of the resulting entity SBL, which is ~325, then why has it fallen so hard and is still continuing to fall (below 180, as of today)?

Is the decision to demerge going to have such a bad impact on the value created by the companies, and hence their valuation? Or has there been a mistake in cost apportioned between the two companies and that SBL should have had a much lower share than the announced 34%?

1 Like

Market mostly is driven by earnings or anticipated earnings. If you calculate value of SBPL on the basis of NPAT, the lower circuit can be justified.

The cost of acquisition for both the companies may be based on capital employed. But the market is valuing those companies on the basis of returns that can be generated by that capital employed.

Also for the SBPL, management hasn’t elaborated any concrete plans for increasing utilization or business expansion, that may have spooked the investors.

Disc. : Not invested and only analysing as of now.

2 Likes