I am still unable to find out why they have not expanded their product category till now and why should we believe management that they will be successful in expanding their product category to more non-steel products without a significant increase in working capital.

2 Likes

Yes,you have a point for building material company to grow company should have significant increase in working capital

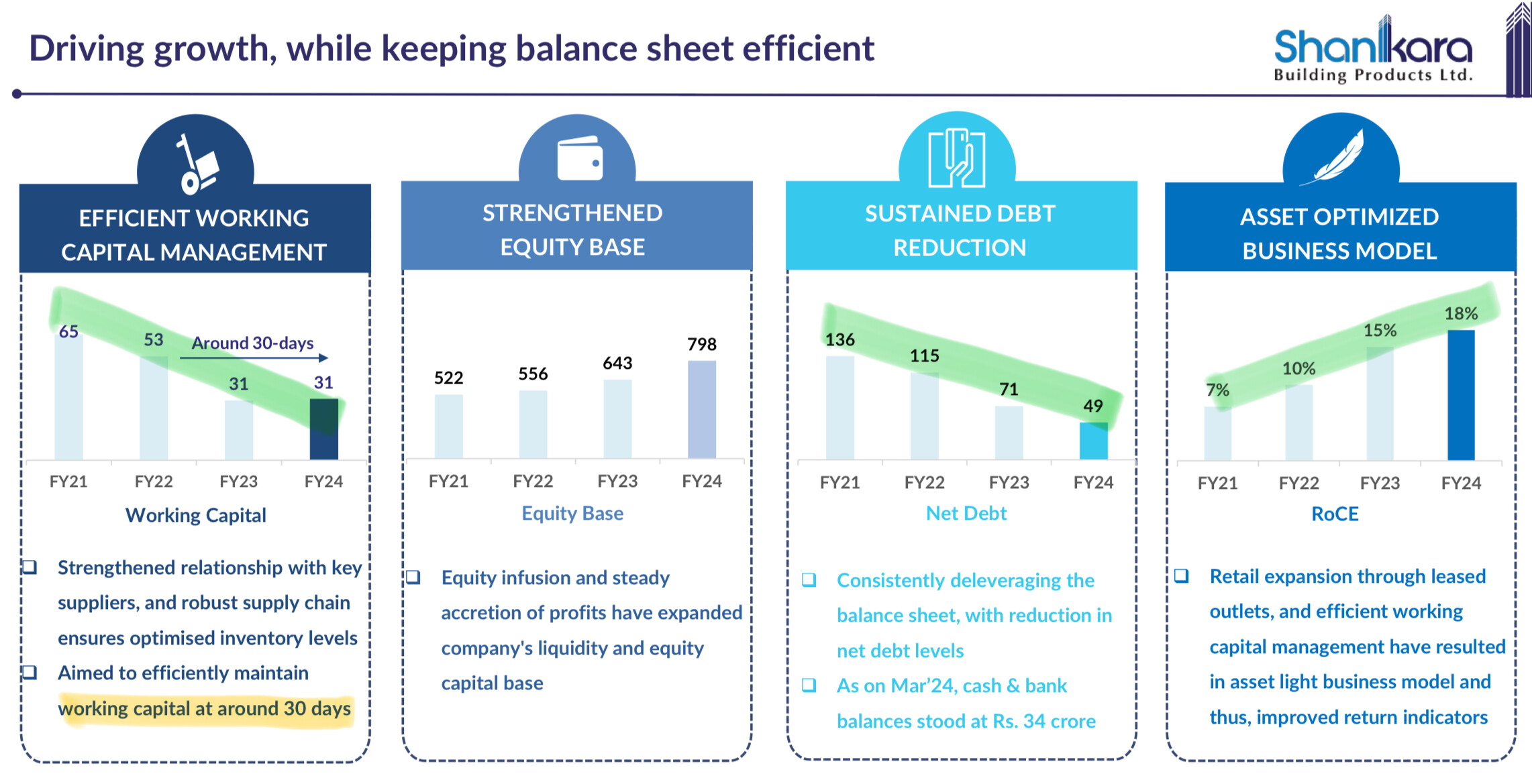

Same store sales growth has been 15% during 9MFY24.Company is focusing on VAP and non steel products.Furthermore,Non steel share improved to 11% in Q3 from 9% in Q2.Operating margin is at its lowest 3%.Company is consistently adding premium brands.Sanitary revenues and tiles revenues were up by 40% in 9MFY24.Fotia ceramica did well in kerala and is being expanded in karnataka,maharashtra and tamilnadu.states.Company has given 20%-25% sales growth guidance for next 5-6 years.It is obivious that company will have good OPM if it improves its non steel products share.However,how swiftly company does that will be key growth driver here.Company has not provided any targets for the share of non steel segment.Steel segment has EBITDA OF 3-3.5% whereas non steel segment has 5-5.5%.Company is targeting 3.5-4% EBITDA in near term.Capacity utilisation(Manufacturing vertical with low ROCE) was around 40% due to less focus on manufacturing but after demerger they will improve capacity utilisation and returns.Management is trying to squeeze highest returns from same store as much as it can then strategically adding new stores.Company has 4% to 5% private label share which they will increase in future.The key metrics to track here are same store sales growth,non steel share,margin expansion,inclusion of premium products,ROCE of manufacturing vertical and fotia’s perfomance in other states

Disc:Not invested still tracking

4 Likes

Good update. Mgmt has been looking into working capital and getting into a proper agreement with suppliers to balance trade receivable/ payable.

Does anyone know whether they own thier retail stores or all leased?

As per this data,stores are on rent and leases.i think this is due to pursuance of asset light model

3 Likes

They already have enough working capital. They don’t use it as fund based working capital, which is why you see low working capital in their balance sheet

2 Likes

Ok,thanks for clarification

New stores opened in kartnataka and mahrastra while few closed in kerala.

Net stores count increased to 92 overall.

3 Likes

Q4FY24: Good Results

Improvement in average ticket size and contribution from west

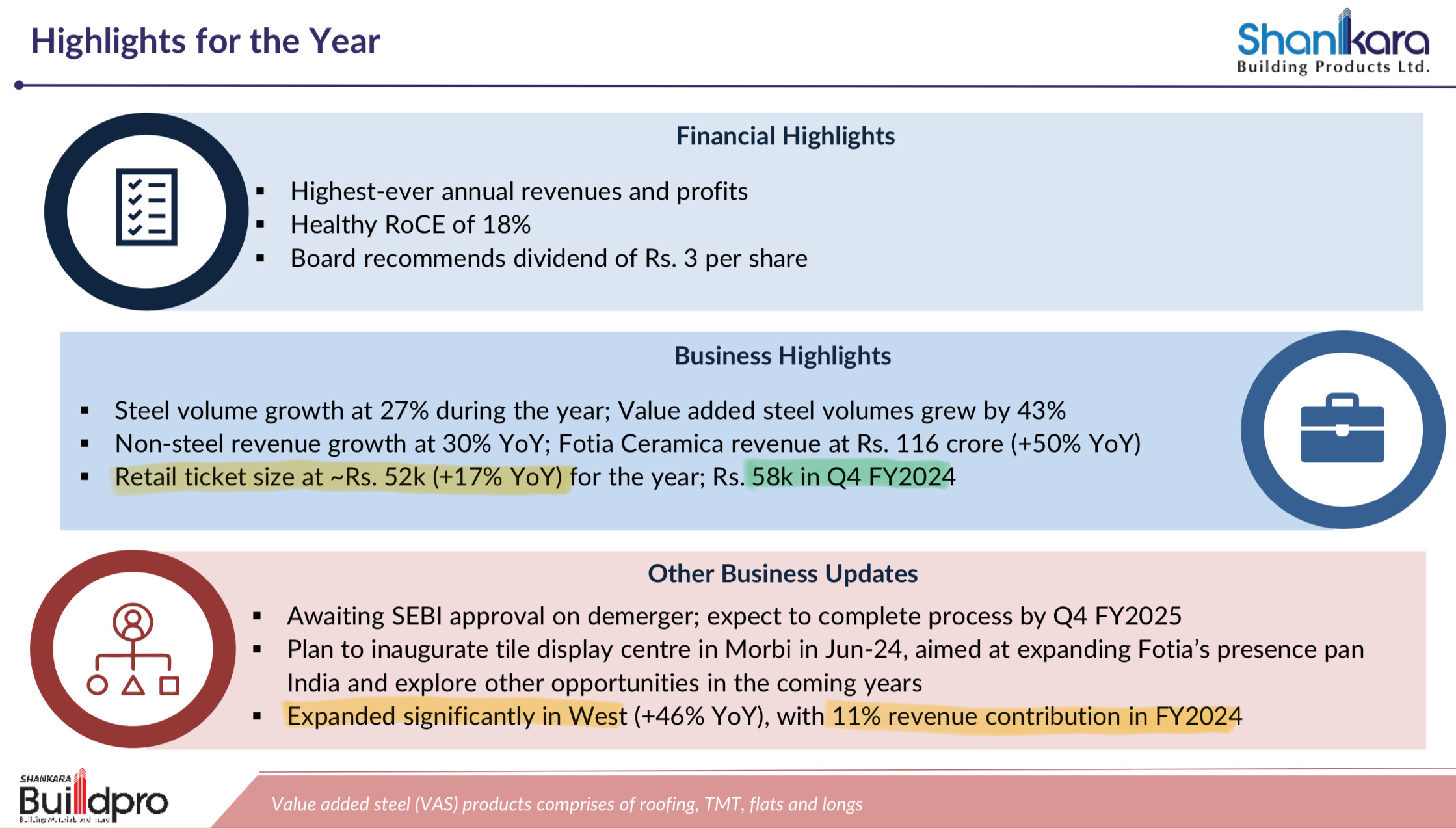

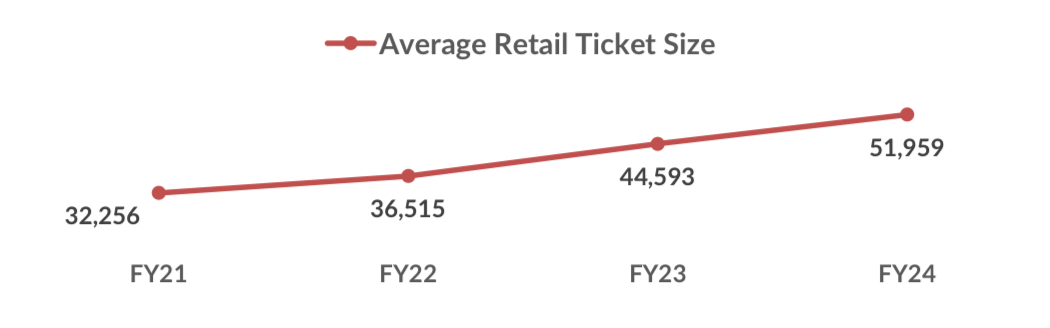

For reference average ticket size of Retail in Q4 was ₹58,000

Improved ROCE, Reduced Debt, Healthy working capital days on sustainable basis and reasonable valuation w.r.t. peers can trigger its re-rating

5 Likes

Marval Capital Ltd. , which is Ben Watsa’s India investment fund has increased stakes in SHANKARA and now owns 350k shares (1.44% of the company). Note: Ben Watsa is the son of Prem Watsa - the Canadian-Indian billionaire investor and founder of Fairfax Financial.

The company looks interesting at these price levels: if it executes similiar to management guidance and successfully de-merges the Retail part of the business, it seems like a decent amount of upside. If they manage to scale across the country, revenues could easily grow 2~3x in the next few years. Margins should also improve with scale, as many expenses (like HQ expenses, Tech systems and eCom website) do not increase with more stores.

However, there are a few risks to monitor:

- Increasing competition from chains like Ikea , “@home by Nilkamal”

- More shift to online purchases , where Shankara doesn’t have significant market share compared to IndiaMART and others

- More direct purchases from building product OEMs (e.g. Kohler sells in BuildPro stores , but also has their own website : https://shopkohler.in/)

- The management is still guiding toward opening stores across the country , but not sure whether they would be equally successful in places like Mumbai where there are many entrenched players. Even if they are able to enter these cities, the ROCE might not meet management’s mark of 20%+

After going through this whole thread and their regulatory filings, I’m still not clear who are Shankara’s “core” customer group. Have they mentioned anytime in the past, how much of their sales go to different customer segments like individual homeowners, building contractors, sub-distributors, property developers etc.?

Disc: have just started a small tracking position and will monitor the next few quarters to decide on further investments

Thanks,

Sharad

OpenSourceInvestor @ Substack

4 Likes

Hi,

Has anybody compared Shankara with SG Mart? Valuation wise SG Mart seems expensive currently, but given that SG Mart just started operations this year, they would grow faster than Shankara I believe. Shankara on the other hand has gained experience and has some track record while none exists for SG Mart.

Further, can there be any rerating/value unlocking in Shankara due to the demerger?

The tech based platform for building materials seems to be gaining steam. Grasim’s Birla Pivot, SG Mart, Shankara, Infra.Market are the names that come to my mind, any one I missed?

Disc: no investments, studying.

5 Likes

Would anyone know why Ashish Kacholia and Mukul Agarwal reduced their holding in the company?

@ranvir any idea?

Disc: have a small position

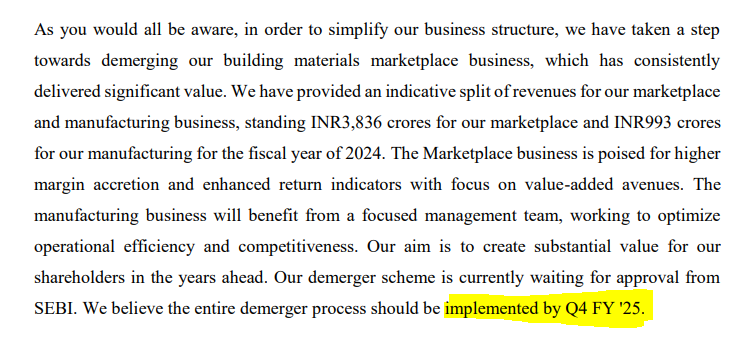

Can someone comment what is current status of demerger and approx timeline for completion (as it was announced in dec23) , also record date for eligibility of shareholding for demerger is yet to be announced right ?

During the May 2024 concall , the management team mentioned that demerger is awaiting SEBI approval and expected to be implemented by Q4 FY '25

Link - https://stockdiscovery.s3.amazonaws.com/insight/india/4933/Conference%20Call/CC-Mar24.pdf

Thanks,

Sharad

OpenSourceInvestor @ Substack

2 Likes

Operating cashflows has not been good which is stopping the growth of the company

Yeah, I noticed that…and didnt like it. CFO just 10Cr.

But the revenues, operating and net profits have grown. Their working capital days also decent now. RoCE improved, so how do you say cashflow is hampering growth.

Check the operating cashflow of last 10 years vs last 3 years

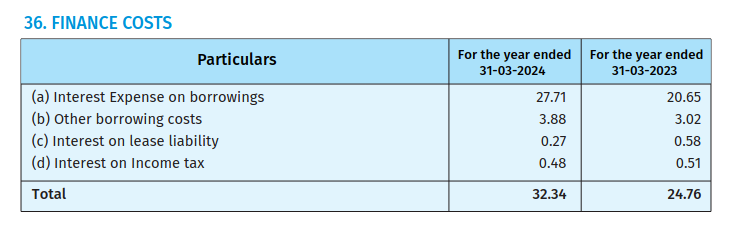

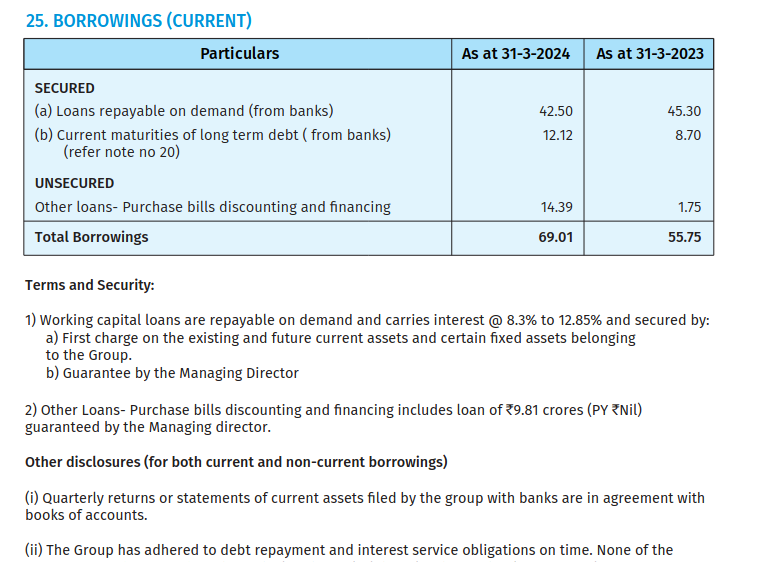

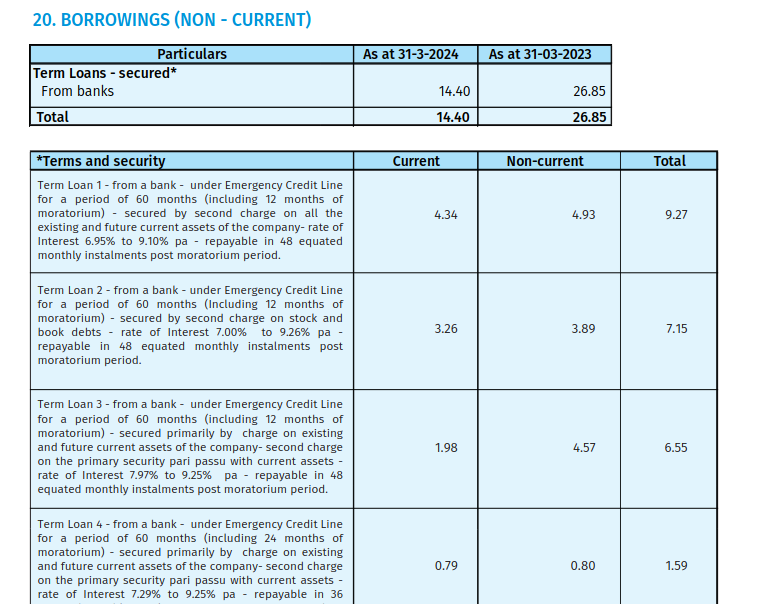

I was going through the Annual Report 23-24 consolidated P/L statement and found that there is an interest expense of 27Cr. while total borrowing of the company is only 83Cr. as per consolidated Balance Sheet. This amounts to around 32% cost of borrowings annually, similar to credit cards! I could not find any explanation regarding high interest expense by going through the notes. Is this really correct or am I missing something?

3 Likes

Balance sheet is prepared for point in time. P&L is prepared for the given time duration.

It is quite possible they took loan during the year and repaid it in same year. e.g. working capital loan. So, the loan is not outstanding on 31st March. But interest is charged for the period loan is availed.

2 Likes