Another decent quarter. Recently, company has received the balance payment towards warrant conversion by APL Apollo, further strengthening the partnership for future growth. This equity infusion will be allocated towards debt reduction and operational requirements, bolstering the company’s financial stability

3 Likes

Q2 FY 24 Short Notes:

Sales Growth and Potential:

Revenues have grown at 31% for the first half of the year.

Retail Sales grew 27% y-o-y with Same store sales growth of 23% (13% increase in number of transactions and 12% increase in average Ticket size per Transaction).

Channel and Enterprises segment has grown at 36% y-o-y with Real estate and infrastructure upcycle. Company believes this segment to grow in coming quarters and years.

Non steel Business grown by 30% y-o-y. Non steel building Materials industry is concentrated towards second half of the year. So, company expects good growth in this segment in the second half of the year.

Private Label Tiles Brand Fotia Ceramica introduced by the company.

Non steel revenue to be 25% from the current 10% in 4-5 years. Dedicated Team set up for achieving targets in the non-steel segment.

Q2 seasonally weak Quarter due to Monsoons and Floods in some areas.

Online currently does not contribute to the revenue and it is used as discovery Platform.

Concept of Store-in- Store started with Nippon Paints and may expand to other segments in future. Nippon Paints helps in Sales and marketing side.

Revenue contribution from APL Apollo products is 35-40% and volume contribution is around 40-45%. APL Apollo relatives has recently started SG Mart in the similar space but company does not feel it as competitor and APL Apollo is strategic partner for the company and that is the reason they have subscribed to the warrants.

Revenue Guidance of 25-30% for the entire year.

Company believes with the existing infrastructure they can double their turnover in next 4-5 years.

Margin Growth and Potential:

EBITDA Margins improved sequentially from Q1 by 13bps to 3.2% due to improvement in product mix within the steel category (Flat Steel and TMT grown by 60-70% while steel roofing grown by 35-40 %) and operating efficiencies.

Gross margins on Non steel Business is 10-12% and since this is the beginning expenses are high and EBITDA margin is 5-5.5%.

Company expects margins to improve with more contribution from Non steel products.

Working Capital Cycle maintained at 30 days in first half of the year.

Geography they operate and future plans:

Company is in the process of opening two new fulfilment centers, one in Maharashtra and the other one in Madhya Pradesh in the coming months. Given our established presence in the South our endeavor is to continue our cluster-based growth approach and strengthen our penetration in the Southern region by gradually expanding to other regions.

Key Monitorable to Track:

Non steel product composition in overall Sales as this is necessary for margin improvement.

Margin Improvement to check whether company is delivering on the promises.

Relationship with APL Apollo as majority of the revenues comes from selling their products.

Same Store Sales growth Rate as Retail has more margin than Channel and Enterprise Segment.

Disclosure: Invested and Biased.

3 Likes

I’ve looked at the whole thread on the company posted here. Would like to summarize here for anyone taking a fresh look

2017-2018 Phase

- Co growing well in terms of growth and margins

- Co planned to add 15 stores evey year (existing 90-100 stores)

- Being compared to D mart in India and Home depot in USA

- The story was around growing demand for building product in India

- Institutainal interest was seen and research reports were released

- stock was trading at >50x PE and people projecting growth of 30%

All these things happened when the co. has very poor cash on the balance sheet. The IPO was made to give exit to PE investors but not enough capital raised for expansion. The ROEs were less than < 15% and so the co. was not able to fund it’s growth. planned to raise 300cr via QIP and it never happened

2018-2019/20:

- Management wanted to increase sales by offering at lower prices. Margins reduced from 7% to 3%

- Tried to hive of some steel processing business

Street didn’t like the reduction in margins. Stock took a beating

2020-Current:

- Management optimized Working capital cycle

- reduced unviable stores. Current store count same as 2017

- Much better balance sheet

My thesis:

- Sales growing at >20% for coming 4-5 years. Management guiding to double sales in 4-5 years

- Net debt free baance sheet (already happened in H1 FY24)

- Improving sales mix of non steel business from ~10% to 25% by FY28. This has margin of ~9% against 3.5-4% for steel business

- Above point will lead to expansion in EBIDTA margins

- This combined with higher SSSG will improve the EBIDTA margins further

- Depreciation to stay at same level as no aggressive store expansio going on

All this would lead to a business growing at ~20% with >20% ROCE with net debt free balance sheet and opearting leverage would continue to play out. This would make for a very good investment thesis

Anti thesis:

- Slow down in building material industry growth for any reason

- Limitation to grow Same store sales beyond some value

- Concentration in South India

- Opening stores in new regions may lead to poorer return ratios (poor IRR)

- Pressure or margins

- Competition grabbing market share (Grasim has entered into B2B building material business and plans to invest 2000 cr in next 2 years, launched in Aug 2023)

Disc: Tracking but no investment at the moment. There may be inaccuries in the data/story presented here

Thanks

Praveen

19 Likes

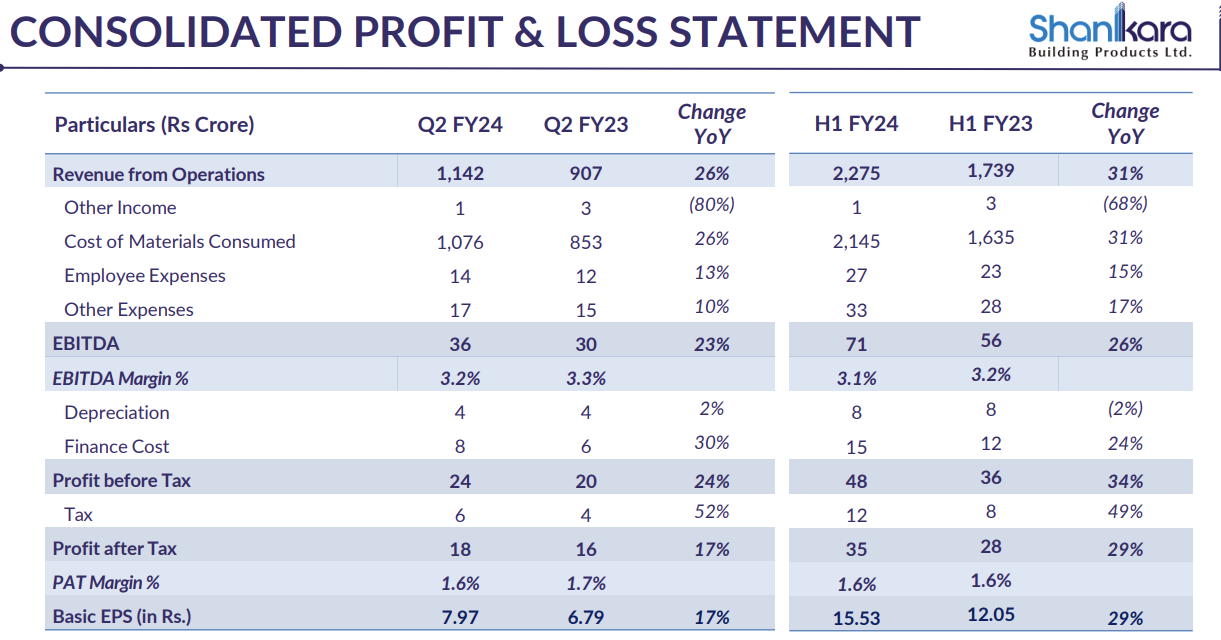

Shankara Building products Q2 highlights -

Sales - 1142 vs 907 cr, up 26 pc

EBITDA - 36 vs 30 cr, up 23 pc ( margins @ 3.2 vs 3.3 pc )

PAT - 18 vs 16 cr, up 15 pc

Revenue break up -

Retail - 54 pc

Institutional - 46 pc

Same store growth at 23 pc

Introduced their own private label - Fotia Ceramica in Q2 - should help in margin expansion. Will be procuring tiles from Morbi

Received balance payment ( Rs 78 cr ) towards warrants conversion by APL Apollo - strengthening their balance sheet and will aid in debt reduction

Total retail stores - 90, spread across AP, MP, Maharashtra, Gujarat, Karnataka, Kerala, Orrisa, Goa

Growth in rental costs @ 4 pc YoY vs 26 pc growth in revenues

In process of opening two more experience centers in Maharashtra, MP

Both Steel based products and Non Steel products grew 30 pc YoY

H2 is always better vs H1 for the company as the construction activity picks up in the second half post the monsoons

Have set up a number of Stores in Stores in collaboration with Nippon paints

Intend to increase the contribution from Non-Steel business to 25 pc in next 4 yrs ( currently at 10 pc of the total business ). This should help improve their blended profit margins. Aim to reach 5 pc EBITDA margins in 4 yrs

Deterioration in cash flows should reverse in H2

APL Apollo’s shareholding ( post warrant conversion ) in the company stands at 5 pc

Company guiding for 25-30 CAGR growth for next 2-3 yrs. Well on track to achieve it in this FY

Company has closed a few unprofitable stores in the recent past. Did not mention the number of store closures

Won’t be growing the number of new stores in an aggressive manner ( likely to open 2-3 stores/yr ) as the company feels that same store growth can be buoyant for the foreseeable future. Company can double its sales within the existing infrastructure

Revenue contribution from APL Apollo products in Q2 @ 38 pc. Company shares a very cordial relationship with APL Apollo. Company has helped them a lot in expansing in South India. Don’t see them squeezing company’s margins

EBITDA margins at present for non steel business @ 5-5.5 pc. Should improve as the volumes improve

Disc: a recent buy, invested, biased, not SEBI registered

7 Likes

I am trying to understand how margins were 6-7% in 2017-18 when they were on expansion spree and lot of new stores were not breaking even? If i see current results, i think all stores are profitable and commodity prices also cooled off but still margins are around 3% as compared to 6-7% in 2017-18. Even retail contribution has increased, now around 55% as compared to less than 50% back then. I have gone through concals and AR but couldn’t figure out why. Could be something straightforward which i am missing, please let me know.

Thanks.

if you go through the investor presentation 90% of revenue is from steel business. As per Crisil Rating August 01,

Exposure to fluctuations in input prices:

As with any retail business, operating margin remains modest. The operating profitability has been volatile in the range of 2.9 to 3.6 percent over the last five fiscals ended fiscal 2023, mainly on account of fluctuation in steel prices. The operating margins for fiscal 2024 is expected to be sustained at around 3%. Improved contribution from the non-steel segment is expected to support the margins, going forward.

If you see the concall summary posted by @ranvir

2 Likes

Yes, i am aware of the fact that 90% business is steel related. I tried to find this ratio for 2017-18 period but couldn’t find it anywhere. My guess is it will be in similar range or maybe lower than the current. I made a mistake in checking steel price, instead of that I checked steel and metal index which was lower than the current the levels. Looks like steel prices are still higher by 35-40% from the levels of 2018.

I found the beta version of Grasim’s building material website, they have already partnered with most of the companies which Shankara has and they are offering some 20% discount. It will be interesting to see how it plays out.

www.BirlaPivot.com

3 Likes

Most of the retailers do give a discount of 20-30% on MRP. How are they going to grab the market?

Your question is answered here. Hope this helps

3 Likes

Demerger Notification.

4 Likes

Dalmia group has launched Hippo stores which are also one stop shop for all building materials. In addition to the website they have pretty massive offline stores as well – I’ve been to one.

5 Likes

But these are only there in north india whereas Shankara building is throughout south and central India.

3 Likes

There will be value unlocking due to demerger. And company is trading at somewhat a discount to the 52w high so potential to consider for new positions. Key is whether real estate sector/ Housing is truly growing as indicated by increasing housing loans. Has anyone

(1) validated Housing Growth… where are we now and what is expected in the next few years.

(2) Visited any of Shankara sales centers in Bangalore or other places? I am not sure whether they have any notable differences.

thanks for your inputs.

1 Like

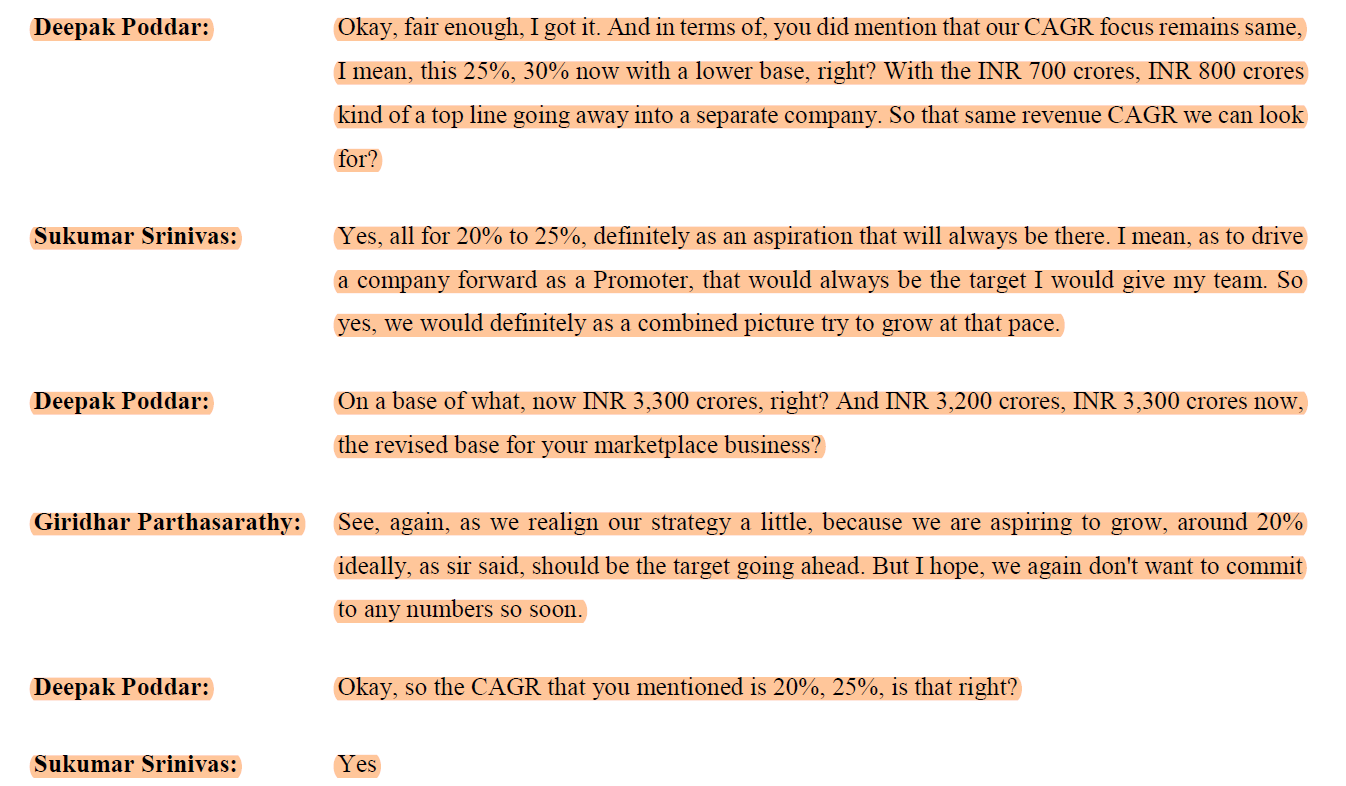

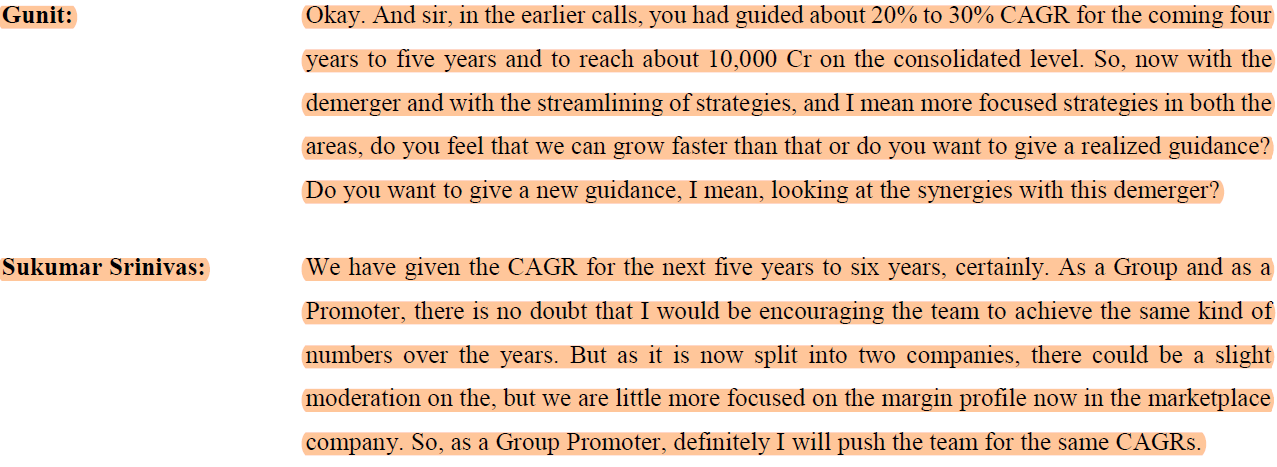

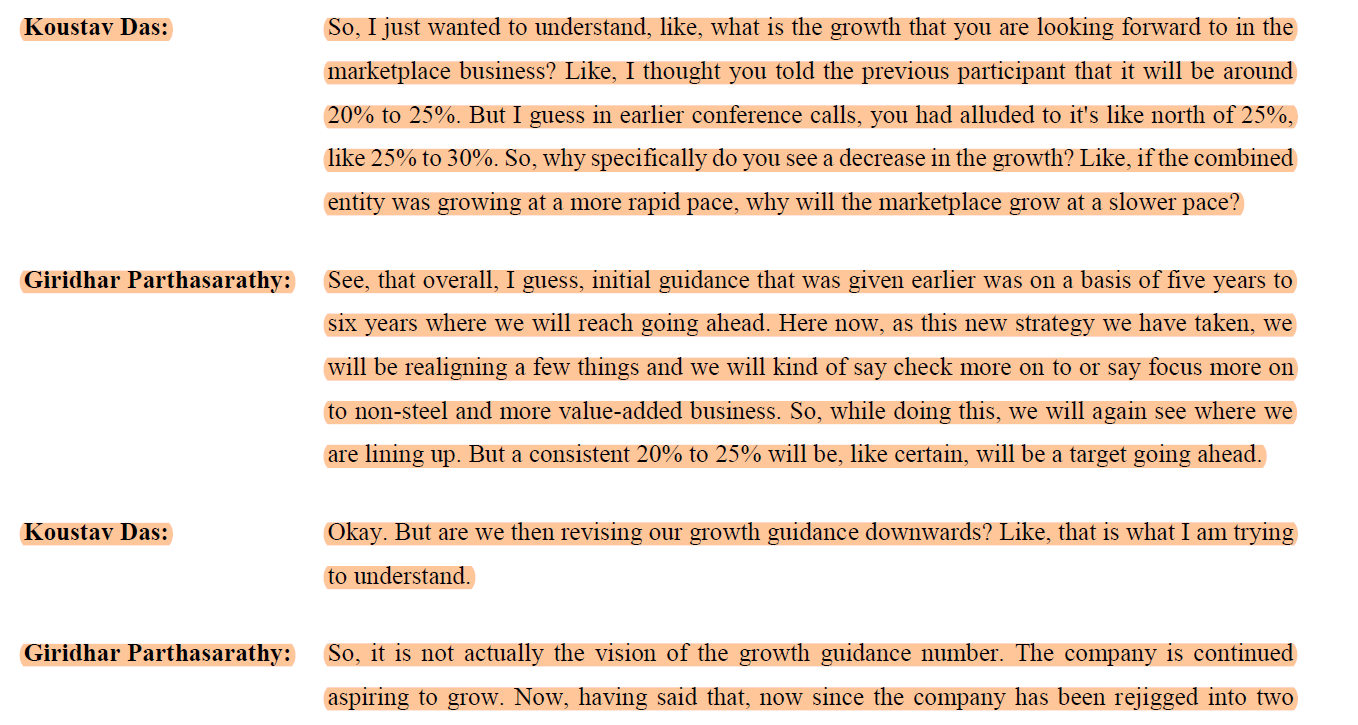

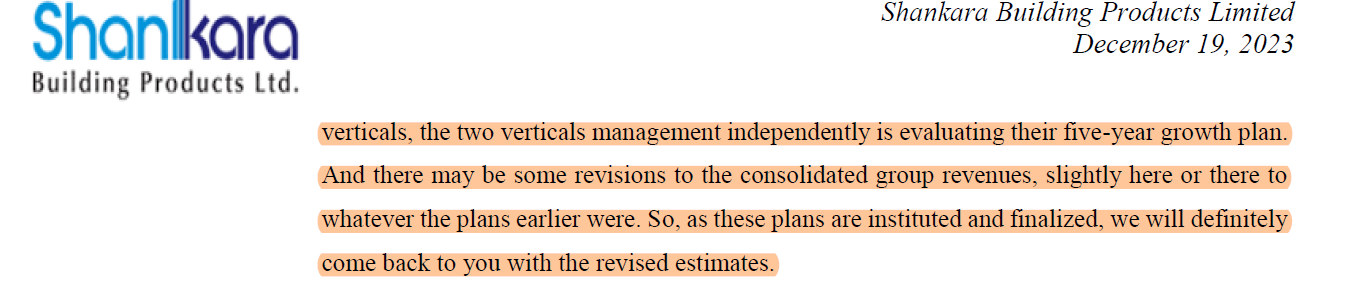

As per my readings of latest concall, the earler growth guidance of 25-30% has been down graded in the name of demearger uncertainity…

disc: No holdings… reading recently.

Can you please share snapshot of that

Interesting developments happening here

Non-steel products sales will help in transitioning Shankara from steel distributor to “Home Improvement” player

Higher EBITDA margins of roughly 4-5% in the medium term and PAT of around 2.5% will yield around 28% ROC

Manufacturing operations will be separated( sub 10% margins and ROC), which will boost Shankara Buildpro valuation

Manufacturing operations post spin off might surprise with average return metrics thus unlocking some value there as well

Growth guidance has been revised downwards by 5%, but if they can consistently grow in the range of 20-25%, Shankara might create decent value going forward

3 Likes

Do anyone have idea how they are going to grow marketplace business with 20-25% CAGR, without any significant number of new stores

(Checked few concalls but haven’t found any concrete trigger)

One more thing, company is focusing more on non steel products but as per my experience these kind of retail stores are too much crowded with products, so are they going to reduce steel products in their stores which would lead to decreased steel products sale, eventually overall revenue growth would be much lesser, or the case is something different, do they already have enough space in their stores to increase non steel products?

1 Like

According to Mgmt, they think there is a lot of pote tial left to increase same store sales for Non steel products. I assume physical space is avaialable in this scenario.

Whether they can hit the growth rate or not, for one thing, will depend on whether real estate market does well. Indications are that it is doing well and may further grow when Interest rates cut. Other than this, I am not sure whether company has specific strategy for growth. Ofcourse, they talk about eCom, adding more suppliers, etc but those are pretty common.

Any other thoughts on why they can or can not grow?