Reading the thread, I think, the company which should have deserved a multiple of typical steel pipe supplier (could be 10-12) was carried to great heights during the frenzy (partly due to DMart’s listing when most other junk retail companies also got re-rated).

Another fundamental question that I have is that in future most of the construction would be in high-rise or apartments. Would any builder/person in charge visit a retailer like Shankara or directly get deals from companies?

As acknowledged in the AR, the business seems fragile with multiple risks.

From the AR

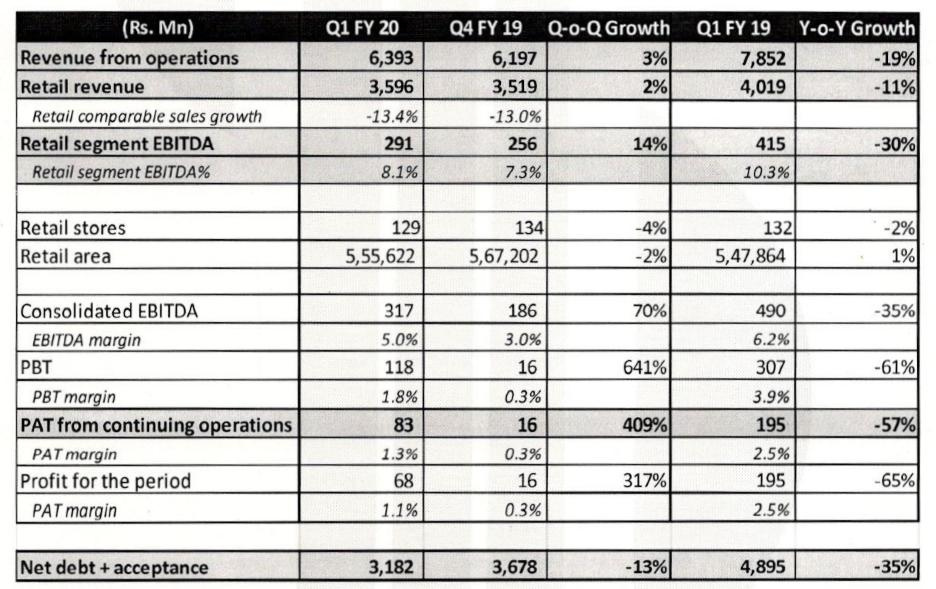

"The year started off on a positive note. The first half of FY 2018-19 was in fact good. There was a revenue growth of 23% which is commendable. However, there were sudden and strong headwinds in the second half.The sharp increases in raw material prices, especially steel coupled with an inability to increase end user prices was a double whammy. This had impact on margins as well as inventory.

Overall, we delivered a revenue growth of 4%. We recorded EBITDA margin of 4.7% (vs 6.9% last fiscal) and PAT margin of 1.2%.

While the company is increasing its focus on diversifying into building products, there is still a large dependence on steel which hit us last fiscal.Further, our business has legacy elements which impact us in our journey to be a retail building products chain. That resulted in a y-o-y fall of 11.6% in sales vs last year in the second half of the year."

No, I have not done that deep analysis but the whole IPO process needs to be critically analysed by the regulator. Why did they bring a company in the primary market if the core biz itself was unsustainable. Within a year they want to transition to retail segment. How could wholesale margin evaporate so quickly or there was no margin at all? So many unanswered questions on the business side here and I would not spend time on accounts just yet.

To be fair to the management, they came with an ipo price of Rs460 and the current price is reasonable on the basis of fall witnessed in all smallcaps. If we bid up the price in exuberance and buy at such high levels, we cannot totally blame this on the management.

The management is making right moves to pivot towards retail footprint away from wide commodity swings. They already pay a high price for steel oversupply. Focus is more on providing a physical and online presence to buy building material products. This is unique concept in India and such moves have been successful in developed economies. They need to slowly make a pan India presence and away from concentrated presence in South India. They could start from Online presence in N India, and other states.

Key watch for me is leaders in Building materials, uptick in real estate.

It is now at good valuations but you can play a waiting game if you are unsure on the business model. My bet is on business model. But then I know competitive dynamic can make high cash burnout rate and retail margins are also crucial here if they can improve it.

I think it would be premature to assume that ongoing de-rating is over. Sales are falling and one has to assign 3% EBITDA margin to project PAT for FY20 and apply PE at the time IPO to arrive at the minimum target in this bear market. We should evaluate wealth destruction at that point of time.

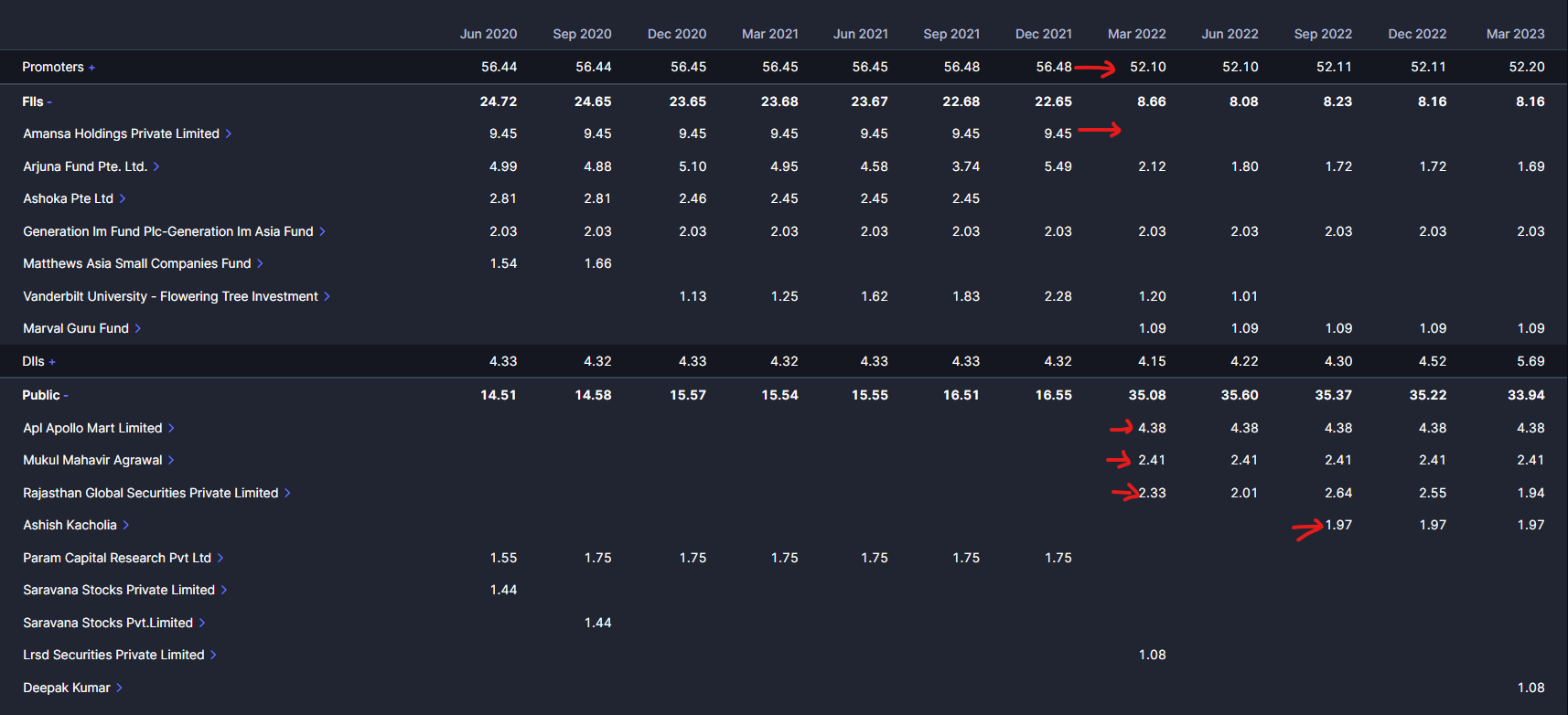

In March 2022 APL Apollo bought 4.38% stake or 1 mn shares at Rs755. Company also took 1.4 mn warrants at Rs750 or 105 crs. Out of this 30% has come in and balance 70% or 73.5crs will come this year. When this comes all debt will get repaid and interest cost can potentially go to zero which is another 27 crs boost to FY24 profits of Rs101crs.See the link here

The stock at Rs700 is below that price. At Rs101 crs profits stock trades at 16x P/E with improving RoCE

Tracking the company for last few quarters

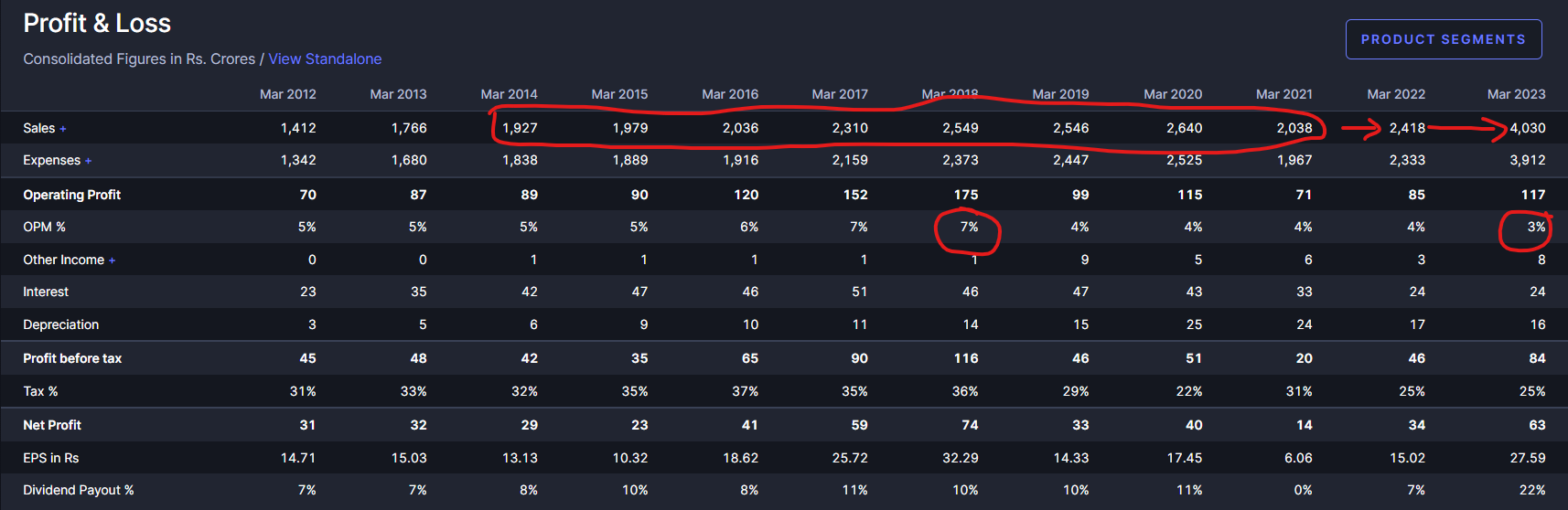

The company changed its business strategy to deliver topline growth in fy19 at the cost of margin which slaughtered the stock because margins took dip along with earnings. But now the margins are stable and topline bottomline all are growing very fast. So what the mgmt did in FY19 now we are seeing the results.

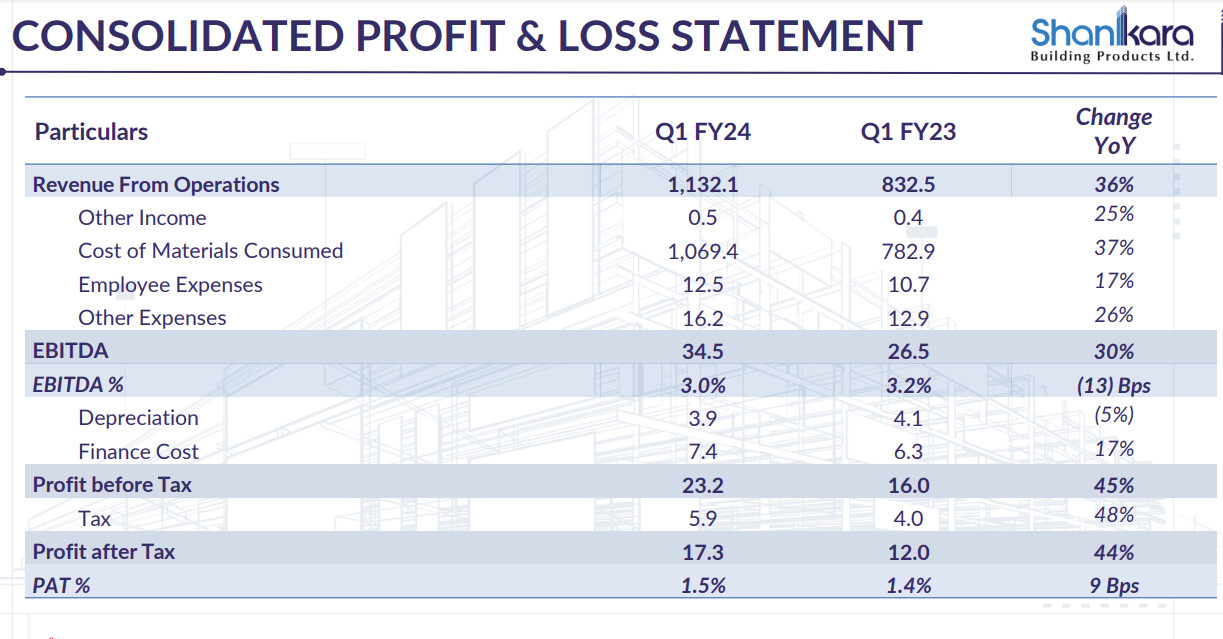

Sharing concall notes for the Q4FY23

Q4FY23

Let me straightaway get into the industry dynamics and business scenario in the Q4 of the financial year ending FY '23. In FY 2023, building materials sector has experienced a consistent growth and business expansion. The thrust in infrastructure development, coupled with the uptake in real estate demand helped the industry to bounce back strongly to the pre-COVID levels. Demand for new building and redevelopment projects have risen in both the residential and the commercial sectors. People’s preferences have shifted in the last 2 years towards larger homes and changes in architecture and interior design.

The building material industry is predicted to be strong in FY '24 due to all these factors and the government’s sustained focus on expanding infrastructure, low-cost housing and rural housing

On the back of a recovery in the entire home improvement industry our top line increased by 67% in FY '23. Consistent efforts have been taken over the last few years to strengthen our balance sheet, and that has also yielded good results. We have received tremendous response from the market and customers, clearly indicating that customers are looking for a one-stop solution for all building materials. We aim to make home building easier for our customers

SSSG at Q4 end is 53%. As stated, we have achieved a strong SSSG for the quarter and for the year

Our working capital cycle for Q4 came below 1 month and the net operating cash flow for the year was at INR92 crores.

Future guidance: We continue to aspire to grow our top line by 25% to 30% in FY '24. We are also working hard to improve our profitability. will try to improve ebitda margin by 50 to 100 bps.

Revenue segments and their margins: In FY '23, we did a total turnover of INR361 crores of our nonsteel products, as compared to INR200 crores in FY '22, registering a growth of around 80%. We are working towards achieving 20% to 25% of our total volumes in this vertical in the next 4 to 5 years.

So the steel products will be the gross margin of around 3.5% to 4%, wherein non-steel, it will be around 10% on average

ROCE: In FY '23, our return ratios improved. For FY '23, ROCE stood at 15.03%, a substantial improvement over the 10.4% achievement in the previous year. We are confident of improving our return ratio in the coming year.

Our current ROCE is around 15% and our working capital is already reduced to, let’s say, 30 days, 31 days. So what other measures you would require for us so far the ROCE to move to let’s say, 30% or so? : Better margin. So we are focusing on better margin this financial year. And within the same number of days of working capital, really it will help us to improve our ROCE.

Yes. We are certainly looking at the margin expansion. As my colleague here said, I think the way to improve the ROCE now currently, I mean, we have at least in mind, the target figure of 20%. We have moved from 10% to 15%. So we have a target figure of 20 this year. And we believe that the – on the back of an expansion of margin is where the ROCE should start improving.

On the ROCE, you’re guiding for about 25%, 30% odd growth in your top line and about 1%, 1.5% improvement in your margins. And given where your working capital is right now, and I assume it’s going to be the same for the next year. So don’t we see, sir, your number should be significantly better than 20% in terms of ROCE? No, I think we will still be cautious in the guidance.

Hopeful of keeping wc days to 30.

New Stores: We believe that we can definitely add even in the current year, I’m talking about FY '24. So I think we can manage with our existing square footage probably with a marginal increase, we are planning about 2 to 3 stores addition in this coming year. So with the margin increase, we can manage with the same square footage that we have

Finance cost to remain around similar levels of 24-30 cr for this year.

Right now, the focus is very much South India. We also believe, as I’ve mentioned earlier, that we do have scope to further expand in South India. So as of now, for the next couple of years, we are not really looking at moving beyond our – let’s say, comfort zone

Retail vs non retail: We are currently at around – when we look at the breakup of our retail and non-retail. I think in the last year, we were at broadly around 50-50 broadly, between a retail and the non-retail part. So I think, we will probably grow another 4% to 5%. So the retail this year should be targeted close to around 55% of our sales

70% volume growth in FY23.

To receive 70 cr in November from warrents issued. With that company will become net debt free.

And last question, in terms of your free cash flow, right? So what do you intend – can we maintain the similar kind of cash flows for the next year? Or how are you thinking about it? Sukumar Srinivas: Yes, we can deal with in the improvement in the cash flow. We are expecting better net cash from the operating activities

On competition: And on the online business, how do you see the competition playing out, right now? Because what I understand is it may not be directly competing, but there are established players like off business, which is there, for example, Grasim is also planning to kind of go aggressive on an online platform. The details are not yet out, but they have a similar B2B online platform. How do you see the competition in the entire online space? Sukumar Srinivas: I think most of the players there are many, many, and many have come in. I mean many startups have come in, many – of course, some of the established players, like you mentioned, are either partly there coming in. But what I find significant traction has not really happened. And if one would just sort of broadly compare some of the existing e-commerce sites in building materials to us, I can easily say that probably in the variety and the range of products, we may be amongst the best. And what we generally find as of now is the online is still look more like a catalogue reference. People do a lot of reference on the online and then come offline to the stores. So most of these people are also talking of what can they do on the offline space. So I think, ultimately, in the building materials space, an online plus an off-line, what we call as an omnichannel is what is really probably at this stage, looking like a win-win combo. So because even if you look at the international markets and even the Western countries, where – there has not been significant growth in the building materials sector linked with the online platforms. So I think it will take a little time. So right now, I mean, it’s too early days to comment on the competition.

Some antithesis:

From q3fy23 concall effect of steel price: Yes. Steel, there has been a bit of an issue in this current year because we saw much of the first nine months where the prices are generally going down. So that means we do take some hits in our inventory when the prices keep going down. So that is one part which has been factored in our current EBITDA

The stock made a top in 2022 when steel price made a top. However inspite of steel price correction in 2022 there was not much impact on ebitda level. Margins were intact at around 3%. As non steel products will grow this impact will be offset as they have higher margin.

Margin trajectory in FY23

Conclusion: The company has shown massive earnings growth in last few quarters however the stock price went nowhere. In the upcoming Quarters also the earnings growth will be huge. In Q2FY23 concall notes the mgmt told of 25-30% growth and delivered massive 67% growth so mgmt is like under promise and over deliver type. This is a candidate for sureshot upmove. Won’t talk much about valuation a pe ratio of 26 with earnings growth twice that of PE stock will always look cheap. But the main things is growth in earnings is what will drive the share price. There are many such examples (adf foods, repro, ugro capital, idfc first bank, mas finance) where stock price goes nowhere for few quarters whereas earnings kept on continue to explode and then suddenly the stock gives 50-60% move in few weeks. Hoping for the same here.This is my thesis.

Disclosure: Invested.

@Anirban_Manna Unless the link shows previews, please don’t just post external links for conference call highlights or similar things. Official links from company or BSE/NSE websites are allowed though…

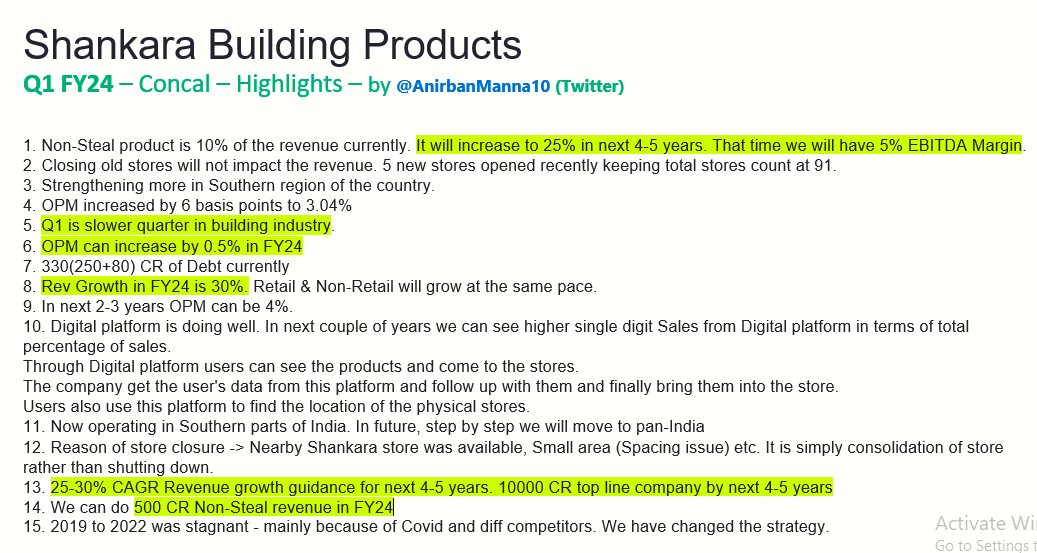

I am attaching the image for everyone’s convenience.

I dont get that , where will the addiitional growth that they are guiding(25-30%) come from as they arent planning to increase retail stores in near futures would it from channel and enterprise along with increasing the average ticket size on the retail front?