Have tried to delve into some of the pointers/questions which got discussed multiple times on this thread.

1. What is the actual business construct under PM Kusum scheme? Is it B2G or B2G2C

On the surface, PM Kusum Project may appear to be a B2G (business to Government) play. However, particularly for this scheme, the business nature is slightly nuanced (and maybe, has not been explored well). In a typical B2G, end-user dont have much say/choice on the brand, configuration and prices of end-product. However, in case of solar pumps under PM Kusum scheme, farmer is indeed deciding on the brand and specification that he want to install, right at the stage of application:

How do we know? Here is the policy roll out document from HREDA portal:

Same is validated by the process flow outlined by Tata Pumps:

So, in a situation where rest being equal (price, technical specification etc.) factors like long standing history, brand trust, after-service reliability, grass root level presence/engagement etc. will be key deciding factor for a farmer to make a purchase decision. Thinking with this context, established players (the likes of Shakti Pump, CRI, Roto Pump etc.) with market standing for few decades are serious contender in the decision-making process for farmers.

On the other hand, in general, many of the state level empanelled vendors appears to be one who are comparatively new entrant in the domain and may be piggybacking on the capabilities that they have got on solar modules side while procuring pumps from white label manufacturers. For context Oswal Pumps is the major supplier for Tata Pumps and claims to have supplied ~44% of the total installed pumps under Kusum scheme thus far. If the numbers are to be believed, it clearly establishes the lack of competency for the assembly /fabrication type of vendors.

Take a look at the recent approved vendor list, many of them has no noteworthy history as Pump Manufacturer:

Maharashtra:

Empanneled Vendors Maharastra.pdf (565.2 KB)

Haryana:

information brochure_2024-25.pdf (537.8 KB)

2. Contrasting performance amongst states:

IMHO, in context of PM Kusum scheme, second important nuance worth noticeable is the performance contrast between the top 3/5 states vs. rest.

There lies an underlying common theme with states which has reported highest installation of solar Pumps under Kusum scheme (i.e. Maharashtra, Haryana, Punjab etc.). Some of top states has embraced the scheme well and have made enabling policy and administrative measures.

In the initial draft MNRE had envisioned 40% cost share by farmer and rest 60% split between state exchequer and MNRE (central nodal agency). These top performing stats have reduced the farmer share of installation cost substantially by providing additional subsidies from state side. Farmer has to pay only 10% of total cost in Maharashtra, 20% in Punjab & HP, 25% in Haryana.

And all these enabling efforts are reflected very well in the leap and bound growth shown by states who have embraced the policy and have created an enabling mechanism. Please pay attention to the kind of growth that Maharastra and Haryana had in last 6 months.

Whole point being, centre may have grand plans however conducive policies and alignment by respective states is the driving force and may continue to be so.

3. Must be elongated working capital cycle being B2G:

Further, there are some concerns related to working capital heavy operation effect considering the B2G contracts. I think we ought to understand the end-to-end administrative mechanism and event workflow.

In nutshell, MNRE who works as a central government nominated monitoring agency has created a portal/digital platform for centralized monitoring which in turn takes feed from state portal/databases. Each of the vendor has to update the work status report on the portal. State level allocation, inspection, approval, payment and rest of the workflow steps goes through this portal. Ultimately, MNRE completes the central government part of funding to states based on closure of state level tasks. Each of the steps has well defined timelines and remedial actions.

[perhaps that’s the reason that MNRE is able to report the performance updates on an almost real-time basis on the portal ]

Theoretically, vendors are getting paid 90% of the billed value for the month and rest 10% after a waiting period of 30 days.

4. Growth Run-way:

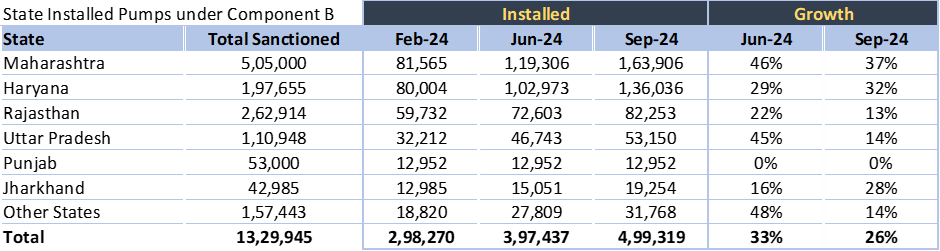

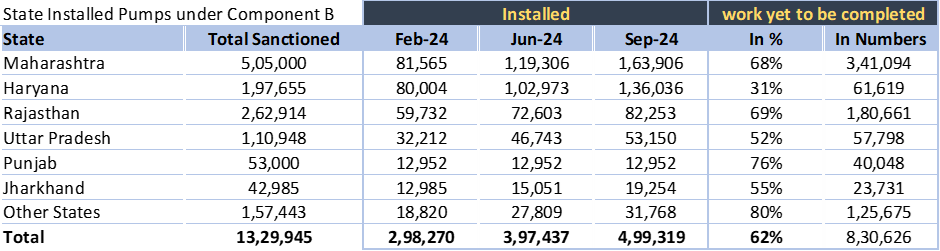

Final part, Government has set a target of ~14 lac pumps under component B of PM Kusum scheme part 3. Below is the breakdown of sanctioned vs installed numbers to get a view of pending scope of work. At an aggregate level, ~62% work is still pending (translating to ~8 Lac Pumps). Shakti’s strong hold states like Maharashtra and Haryana (20% market share) and Rajasthan (37% market share) alone has close to 6 Lac pumps deployment work pending. As evident from the below table, the way execution pace has picked up in top states (Maharashtra, Haryana and Rajasthan) in last 6 months is good indication of things to unfold in next 1- 2 years.

On the negative side, have learned few things which are slight negative at the overall PM Kusum scheme – at least from farmers POV.

- For the farmer, Solar Pump costs 15% to 20% more under PM Kusum scheme since Kusum has DCR (domestic content requirement) provisions -which may not be there on marketplace purchase or other similar government schemes (I think Mukhyamantri Saur Krushi Pump Yojana, Maharsastra did not had DCR) . Also, there is additional 10% cost difference under Kusum scheme due to requirement of 360 degree dual axis rotation structure requirement. However, on big picture view, the 60% subsidy by centre and state government will by far outweigh the cost difference due to DCR and dual axis cost inflation.

- Finally, in some states the subsidy on electricity for agriculture uses is far higher than the 60% subsidy offered under PM Kusum scheme. This becomes more relevant since the Kusum solar Pump installation cost of 2 – 4 lacs is upfront investment for farmer. Hence, in those specific cases, less lucrative for the farmer to opt for Kusum scheme.

Thanks,

Tarun

Disc: Invested, transactions in last 60 days