Seya Industries Limited was incorporated on October 11, 1990 as Sriman Organic Chemical Industries Private Limited. On April 20, 1992 it was converted to public limited company. Promoted by Mr. Ashok G. Rajani, Seya Industries Ltd (SIL) is engaged in manufacturing of organic chemicals, viz., mono chloro benzene (MCB), para nitro chloro benzene (PNCB), Ortho Nitro Chloro benzene (ONCB) and by-products sulphuric and hydrochloric acid. As per the Care Rating report company has capacity to produce 18,000 MT of MCB, 5,000 MT of ONCB, 10,000 MT of PNCB, 6,000 MT of DNCB, 7,600 MT of DNCB and 4,000 MT of PNA as on March 31st, 2015.

Company started it’s expansion plan from 2010, Company has already initiated work for its upcoming projects integral to it’s existing business operations by embarking on a backward & forward integration project and capacity expansion of captive products. Company has a clear focus to manufacture specialty chemicals which is evident from the following segment wise revenue breakup.

SEGMENT 2011 2012 2013 2014 2015 2016

INORGANIC 0.53 0.43 0.27 0.45 0.34 0.08

ORGANIC 7.02 13.94 23.02 26.32 14.99 9.18

FINE & SPECIALITY 11.34 11.73 11.27 93.94 225.59 261.77

PHARMACEUTICALS 0.74 2.0 6.8 7.44 6.58 3.62

AGROCHEMICALS 0.93 0.22 10.92 2.67 0.88 0.6

OTHERS 0.09 0.01 1.91 0.45 - -

TOTAL 20.68 28.39 54.21 130.84 247.61 275.25

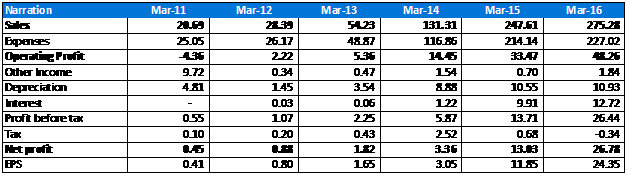

Financials: On the back of massive capex, company’s sale has grown from from 130.84 cr in 2014 to 275.25 cr in 3 years. Co.’s profit has increased from Rs. 3.36 cr to 26.78 cr in the same period.

Negatives

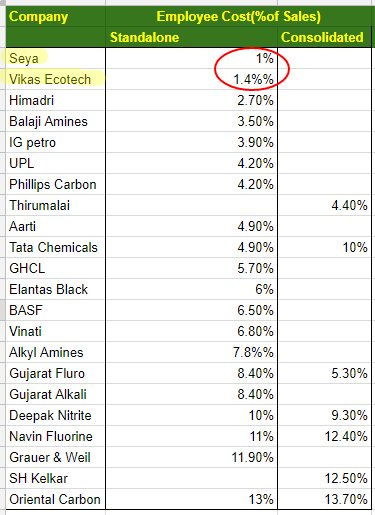

Employee cost is Rs. 2.14 cr in F.Y. 2016 i.e 0.77%, I have never seen employee cost so low in any chemical company. IN the AR2016 company talks about plant automation which has made it to emerge as one of the highest quality and lowest cost producers of benzene derivatives in the world.

Debt Equity Ratio is 2.93 times as on 31.03.2016. (Total Debt = 261 cr and shareholders fund is 89cr.).

Other long term liabilities – payable for purchase of fixed assets – rs. 185.40 cr.

Seya has witnessed 870% growth in last 5 years with sales crossing USD 45 million and has already embarked on its journey of forward and backward Integration to achieve target sales of USD 150 million by 2020

We are delighted to share yet another crowning achievement that your Company share price in BSE recorded more than centurion growth on reinstatement of trading during 2015-16, complementing our Silver Jubilee celebrations.

Your company continues to focus on consistent, competitive, profitable and responsible growth with its forward integration products in the Fine and Speciality Chemicals segment which witnessed Revenue from the segment contributing to almost 95% of the total revenue and those from the new products comprising 86% of Net Sales.

in FY 2015-16 Revenue from Operation grew by almost 11% to 27,528 Lakhs while EBIDTA margin was 18.20% (5,009 Lakhs) underscoring an extra-ordinary growth of 47% (PY `3,417 Lakhs) even amidst extremely challenging backdrop of sharp decline in the global crude oil prices considerably reducing realisations.

The world’s epicenter has shifted to Indian manufacturers to fill the void created by the deficit in supply owing to shutdown of Leading companies in China due to environmental concerns crafting highly lucrative opportunity for SEYA, which is well known as one of the lowest cost producers in its class of products globally, owing to the level of integration in our manufacturing processes and wide international market presence through merchant exports.

Our Company has an advantage that its Businesses have good potential to grow (as the industries they serve are growing) and its manufacturing blueprint is reasonably complex (not complicated) and integrated, therefore not easily replicable.

Overall volume growth stood healthy at 15% driven by balanced growth of almost 5% from the Speciality Chemicals contributing 95% of Revenue, followed by 3.43% in Organic Chemical Intermediates, Pharmaceuticals and Agrochemicals/Inorganic Chemicals inishing the top-line at 1.32% & 0.25% respectively due to the new products launched continued to deliver double digit growth to sharp decline in International Crude Oil prices resulting in disruption of volume off-take by some customers, however the same was set-off as Global prices of crude oil stabilised at albeit lower levels.

This growth has come about despite significant increase in Interest and Depreciation cost on account of full commissioning of the forward integrated new products.

Finance cost was higher at `1,272 Lakhs due to post commissioning interest cost against Long Term Loan and Short Term Working Capital Loan availed from Banks & Institutions for Upgradation, modernisation and added capacity of Nitro Chlorobenzene Plants which were commissioned during the year under review.

Seya’s sustained focus on process development, plant automation and high quality benchmarks has made it possible to emerge as one of the highest quality at lowest cost producers of benzene derivatives in the world.

Your Company has the largest installed capacities for its premium high valve and high margin products.

Seya has been REACH-compliant and emphasizes on Reduce-Reuse-Recover principles across its manufacturing site following the highest SHE (Safety, Health & Environment) standards. Your Company is looked upon as a benchmark and standard of Quality. Your company has revolutionized Quality of all the Products it manufactures to standard which can be matched by none and commands premium pricing for all its products.

To meet the increasing demand last year your Company had announced setting-up of a Greenield project to be self-reliant for most of its Raw materials, Reduce Cost of Energy, Diversify into Specialised High Value & High Margin products, Value addition to By-Products by reusing the same for manufacturing of high margin products and expansion in capacity of its captive use products.

With a Capital Outlay of 73,458 Lakhs and having so far incurred31,533 Lakhs, this phase of expansion shall phoenix up the Bottom and Topline of the Company and shall make it achieve leading and dominant position in Specialty Chemicals globally for all its products. The Project entails:

a) Expansion of Intermediate Product for downstream consumption

b) Backward Integration into manufacture of Bulk Raw Material so as to reduce Raw material & Logistics Cost and Environmental Hazard

c) Recovery of Waste Heat and Recycle/Reuse of By-products so as to reduce Cost of: Materials, Energy and Efluent treatment

d) Forward Integration & Diversiication into high value & high margin Speciality Chemicals based on existing product mix which are having high demand and growth potential considering their application in end-user industries to achieve better integration in the existing value chain through established market network and customer base

e) Captive consumption of 50% of products proposed to be manufactured

f) Setting-up of Captive & Cogen Power plants based on Waste Heat Recovery Systems.

The recently introduced forward integrated products in the Fine and Speciality chemicals are expected to report good volumes. Increasing utilisation of these newly launched products will further propel volume growth and proitability.

Considering the overwhelming response of your company’s participation in Chemspec Europe 2016, your company has strategized to set up of Sales ofice in Europe and North America to further propel its momentous growth by i) broadening its market reach in new geographies, ii) increasing its manufacturing and working capital eficiencies and iii) introducing new products.

During the year in retrospect your company has undertaken modernisation and upgradation Project of its Nitro Chlorobenzene manufacturing plant at a Capital outlay of `6,552 Lakhs which has resulted in Increase in Raw material eficiency, Improvement product quality, Reduction in Utilities consumption, Increase in ease of operation and moreover increase in Capacity of Nitro Chlorobenzenes from 15000 TPA to 33000 TPA. This expansion will further enhance the proitability by contributing to the Top & Bottom line.

With Respect to comment on CFO, your Directors would like to place on record that the Board had appointed one candidate as CFO, however, before company could assess his skills and knowledge, he left the organisation due to some personal reasons. This is crucial position which requires proper due diligence before appointing anyone on this position, there has been a delay in appointing CFO. Interviews are in process and the Company shall appoint CFO very soon. At present, responsibility of CFO is carried out by the Managing Director of the Company.

Your Company is signatory to the ‘Responsible Care’ initiatives and Responsible care logo holding organization.

Expenditure incurred on Research and Development: Particulars 2015-16 2014-15 -Capital Expenditure 4.50 (620.71) -Revenue Expenditure 787.92 - -Total R&D Expenditure (% of Net Sales) 2.88% (2.51%)

I had also come across this company sometime back as it was posting fantastic numbers and valuations looked attractive and I also have a tracking position. Some points which seem really concerning to me are:

Their annual reports seem to have too much of marketing jargon. Its really tough to understand what exactly the company is doing.

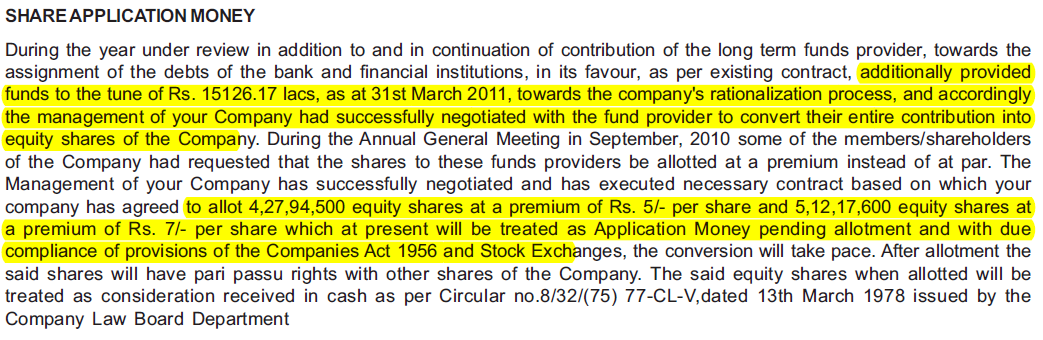

If one goes back into the history, the company had a troubled past and was in financial mess. Around 2011 the company came out of the problems with a big fund infusion of 150 Cr. If one goes into detail, the company had allotted equity shares at just Rs 15 and 17.

and then for next 4 years, this amount is shown as share application money pending allotment. In 2016, this gets changed to Non-convertible Pref Shares.

So who lent such a huge money with no returns?

Its also strange to see that 50% of the gross block of the company is into leasehold land.

3 . The business seems highly capital intensive. Asset turns are low and it seems the company has additional capex plans of 500 Cr in coming years.

Overall, given the aggressive nature of things and fast pace of developments, there may be more things and reasons behind the above but it would be important to understand and have clarity.

I have got the list of preference shareholders from the MCA website, attaching it below. Promoters have lent money in the form of preference shares, but i am not able to figure out who are the other parties. Preference shares have been issued at 1% dividend which is almost zero return.

Asset turnover is low also because of huge amount of land in fixed assets. The additional capes won’t involve land, so the asset turnover will be higher than current. Asset Turnover is currently 2 times if we exclude the land value.

In the big dilution which is coming up, Reliance Nippon Life Assets have subscribed to 20 lac shares. Is it a good thing for such a small company to have a backing of a fund like Reliance Nippon?

Ashok Rajani - 102.6 lac shares

Shalani Rajani - 93 lac shares

Whiz Eneterprises - 424.80 lac shares

(Rajani Group Company)

So total 620.40 lac shares issued to promoters which is approx 41% of total 1512.61 lac shares issued.

All other private companies have two directors - Ashwin Gajanan Pandya and Narendra Gajanan Pandya. And also all these private companies are registered on the same address.

Kalpana Tirpude has also been allotted 48.80 lac shares. Kalpana Tirpude is serving as Independent Director on the board of company since 23-04-2015. Address of Kalpana Tirpude is same as that of other private companies of Pandya Group.

It looks that promoters have invested their own money in the company.

Pretty strange but interesting transaction. Can we try digging more about the promoters, how are they do cash rich? What are the other businesses they might own?

After long time I had time to check up on the company. Some notes: From Screener

Debt /equity ratio : 2.93

Interest coverage ration : 3.95

From Moneycontrol

Return on capital employed(%): 4.08

But if you view the Return on equity, its 30.06.

So this is a debt fueled vehicle it seems. With the inventory turnover of 9.68 there wouldn’t be much requirement of debt (at least not for working capital), it seems that the promoters are more into Real Estate rather than in speciality chemicals. Quite a gamble I’d say.

The stock was also covered in ET today, it seems the company is undergoing both backward and forward integration and is looking to treble sales by 2020. It’s trading volume is too thin which is a little discomforting.

It is important to look at the competitors in this space. Among the listed entities, Aarti industries is the largest player in the benzene derivatives space with it’s corresponding product capacities being 5 - 10 times that of Seya. There is also Kutch Chemicals (Panoli) and Hemani Industries which manufacture similar products at capacities that are higher than Seya.

I highly doubt that Seya can be a cost competitive producer and there seems to be something amiss in their reported numbers as highlighted by others already - the low employee costs, questionable treatment of capital etc.)

On the other hand, if Reliance MF has started accumulating this stock then there is a need for some on ground research before fresh comments can be made.

I guess the reason for raising money though preference shares was that their D/E ratio was going out of limits. The share price being just 80-85 during that time , the promoters did not want to raise money through common equity and dilute their stake greatly.

I am not sure what is going on here. What is aiding such abnormal industry beating margins, such low employee costs, almost negligible manufacturing costs, gross block containing leasehold land, high inventory turns meaning highly efficient or discount model. They are paying negligible taxes.

There are 132 employees as of March 2017, total remuneration is under 2.5 cr. 3 KMPs are taking 33 lac as salary in total, so just do the math for salaries of the remaining 129. Around 1.7 lac. Odd?

There annual reports are like marketing presentations. If you look at mgmt discussion and analysis, full of extreme marketing jargon, self praises, SWOT analyses, and things like that.

When 99.34% revenue is from one division (specialty chem), why does the company go on explaining 4 other division under revenue head. Why not just put “others”.