Seya’s latest investor presentation

Disclosure: Holding.

Seya’s latest investor presentation

Disclosure: Holding.

Here is a management meet report from ICICI Sec. They haven’t put any target price for the scrip.

the allotment of preference shares to the tune of 42.5 lacs at 180 per share is only 72 cr, they could have easily raised this amount from the market, however they prefer not to buy shares from the market. with current prevailing price of 400 rs per share, the promoters already have a gain of 2.25 times without doing nothing. also this seems to have been done at an opportune time as the co. is expanding so share price should increase in expectation. management quality is a big concern for this stock.

Seya has released it’s Investor Communication which includes status of it’s expansion. Stock has gained significantly after this communication.SeyaQ1FYUpdate.pdf (517.6 KB)

Expansion plans and net profit growth all looks very rosy until one looks at the ROE and EPS growth. Net profit trebled in the last 3 years while the EPS has stayed stagnant at Rs20 odd.although the company is growing, nothing is flowing to the minority shareholder. The reason seems to be heavy equity dilution at Rs180 not only to promoters but also to RNAM. How did they arrive at that figure? Looks like a big negative in my mind. Probably this should trade at Rs180.

The company in the latest investor presentation showing 84% rise in employee cost compared to last year

Company in right industry. Growth is visible. But lot of issues related to management.

Continuous equity dilution. They convert their unsecured loan to equity at 180 and 523.

Current EBITDA per tonne of Rs.75K is unsustainable. It should crawl back to 33-35K.

There has been constant delay in execution of Phase II plant and that’s why dilution and issuance of NCD’s. This will take almost 9 months more than their initially guided date.

Disc - Invested

Rating downgraded to default -D as company not able to make the repayment on timely basis

http://www.careratings.com/upload/CompanyFiles/PR/Seya%20Industries%20Limited-10-15-2019.pdf

Company has no single year with positive fcf.

Free cash flow is negative since 2011.

Disc…not invested

Can anyone here summarise all that went wrong with this stock?

Why is this stock at 0.1 Price to Book?

Pragnesh a post above yours has summarised it very succinctly

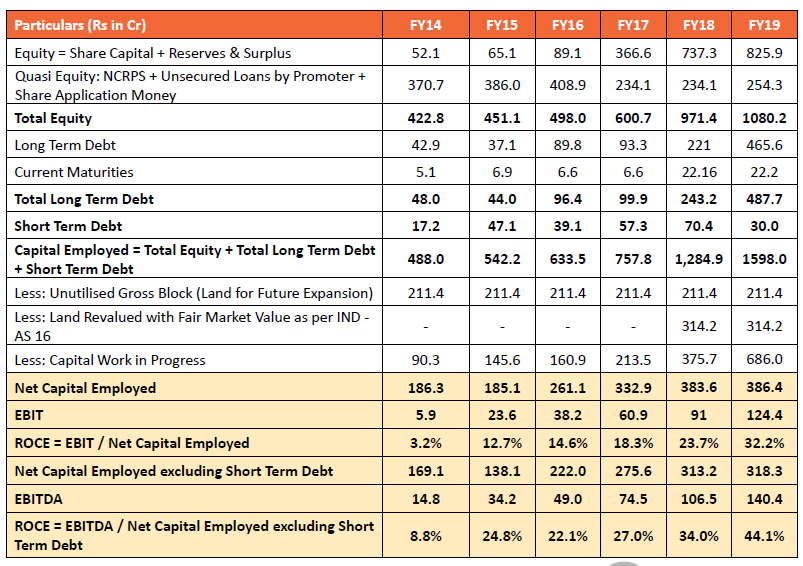

Just got curious to know about company as rememberd they objected to Credit down grade by credit rating agency. While going through past submission to BSE, came across presentation by management in August 2019. What I like is way they calculated ROCE during FY19 at 44%. While nothing wrong in approach of calculation of ROCE (that is excluding Capital WIP and Unutilised land), but the point is In Rs 1600 Cr Capital employed nearly 1200 Cr is non productive assets. Just wondering why chemcial company with this size shall carry Rs 211 Cr of untilised land (again base of upward valuation of 300 cr due to revaluation)?

Interesting learning for me.

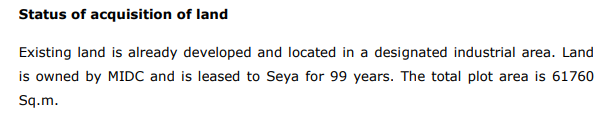

When I further explore about Land details, I got interesting development. As per FY19 AR (Page 24 &25).

I refer to Project report submitted with EIA (not sure whether same being for Phase I or II).

On Page 23 of August 2019, We find nearly 196,000 sq mt land being un-tilised land. (It may be important to note that on same slide there is private placement of equity with Reliance Nippon and Zillow Real Estate Rs 41.4 Crore at Rs 180 per share).

While I do not have understanding about various project and that may be limitation to my wokring, I found interesting how can we have around Rs 300 Cr being added to Land value which is leasehold as given in Annual report. Further, when Project report (Environment impact study) provide for area of 61,000 sq mts (again leasehold from MIDC), there is no details of 196,000 sq mt as provided in presentation. Even annual report details of Gross block only provide for Leasehold land. So investor shall explore further details about commercial viablity of real estate deal by the company.

Lastly, depsite being Rs 300 Cr+ being added to Capital work in progress during Fy19, the company did not provide for any details about items which made up capital work in progress. Further, total debt being Rs 400 +30 Cr workng capital, say Rs 430 Cr, being subject to interest in MCLR to 260 bps, assuming cost of around 10% would result in Rs 43 cr while company has shown in ino material ncrease in interest charge in P&L and also not mentioned anything about capitalised interest in Annual report of FY19.

I would suggest investors to get more details about above mentioned issues.

Discl: No investment in the company