Seshasayee Papers ltd

The Industry:

4 Categories of Paper :

- Newsprint

- Writing and print papers(32% market)

Poor growth can be expected in future with increase in digitalization and online activities - Paper boards for packing(55%)

Increase in growth can be expected in future - Tissue papers(8-10%) and other speciality papers(3%)

Present per capita consumption :

India = 13 kg (Expected to increase to 17kg by 2025)

World = 67 kg

The business:

Main Product in seshasayee : 100% revenue is from business of writing and printing paper

Units :

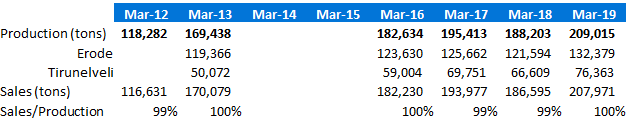

- Erode unit : (2018 data)

• Produced 121594 tonnes in 2018 as compared to 125662 tonnes in 2017

• Export = 11.88%

• Produced 23.9 Cr worth petroleum products

• Produced 510 tonnes notebooks

• Left over 16 tonnes - Tirunelveli unit :

• Produced 66609 tonnes in 2018 as compared to 69751 tonnes in 2017

• Export = 21.7%

• Zero stock left over

SUBSIDIARIES:

Esvi International Ltd :

• 100% holding

• Deals in properties

• Net profit in 2018 : 0.07 Cr

ASSOCIATES:

Ponni Sugars ltd :

• Invested 19.6 Cr

• Net profit in 2018 : 3.34 Cr

Equity shares:

Authorised shares = 4 Crores

Cumulative redeemable preference shares = 3 Crores

Issued shares = 12613628.There is high probability of issuing bonus shares.However,bonus shares have there own pros and cons.

Financial analysis

Sales:

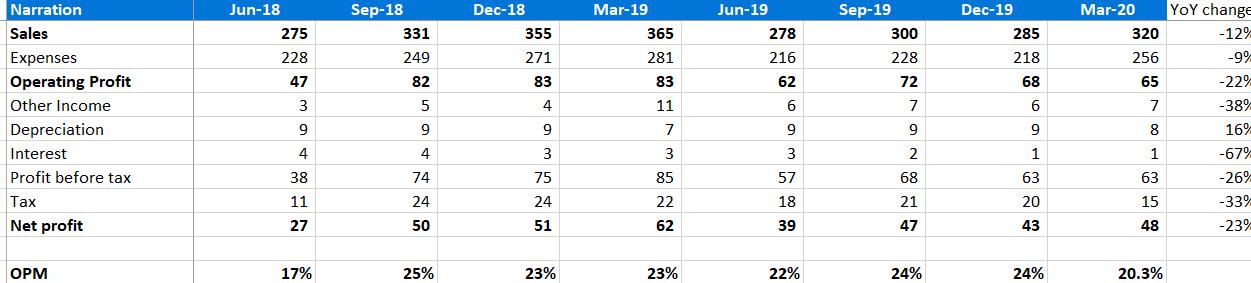

Sales is very irregular.increased from 437Cr(2008) to 1105Cr(2018).Since 3 yrs there is poor growth in sales(1%-8%-0%).

OPM:

Opm has been 19% and is improving.

Tax rate:

The tax rate at around the 28-30%.

Other income:

Company has about 7% of its revenue as other income.Its primarily from interest and dividends.

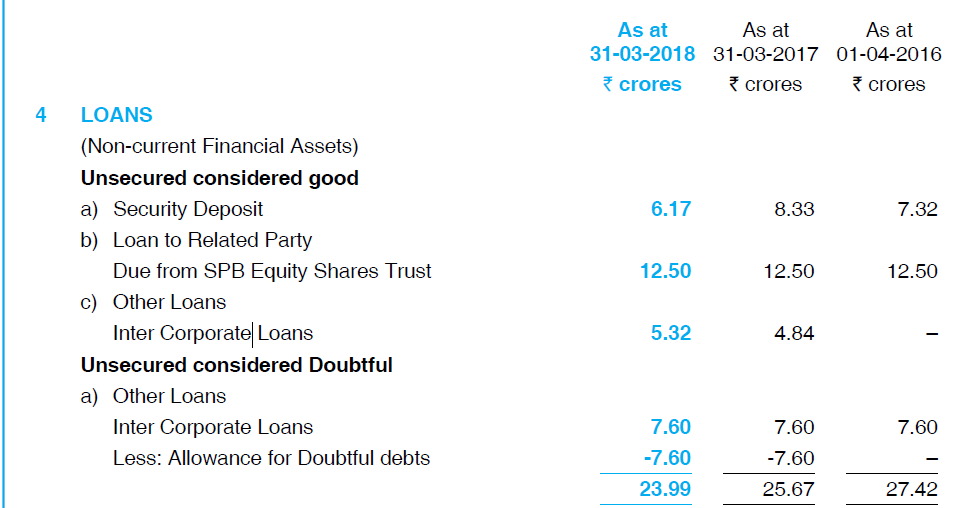

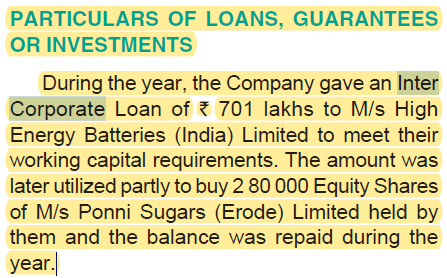

It has term deposit of 118.8 Cr.It has equity investment of108.37 Cr

Cash flow from operations:

CFO is 848 Cr.Capex is 984 Cr.Free cash flow is about -136 Cr.

Some ratio analysis

Asset turnover:

has decreased to 1.65,which means company is making poor use of its fixed assets.

Receivable days:

is around 35 recently,gradually reduced over years.

Inventory turnover ratio:

is 7.71(reduced).

ROE and ROCE:

is average around 19% and 16% respectively.It has reduced in 2018 to minor extent.

Cumulative Net profit/CFO:

= 473.93/847.91, which means company is able to nicely convert its profit into cash.

SSGR:

is 14% which says company can continue its operations without and external capital.

Networth:

Companies net worth has improved from 12.43 Cr to 725.47 Cr in 10 years.

Trade Receivables(106.86 Cr) is lesser than trade payables(236.46 Cr)

Cash :

24.63 Cr

Dividends :

15 Rs in 2018.Gradually increasing.

D/E : 0.2

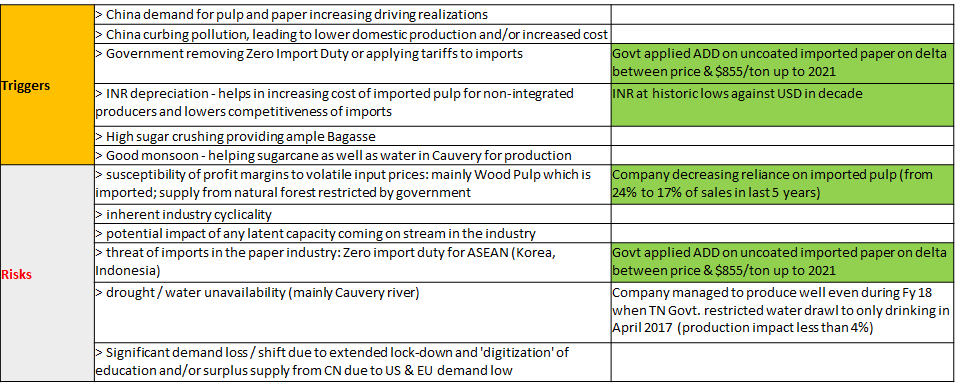

Risks :

• Change in RM prices(wood/coal/oil/chemicals)-They have tried pulp farming by providing seeds to farmers at subsidy.Thus,they can get wood pulp at efficient cost and manner.

• Monsoon-Water is required largely in paper industry.Rivers near units are usually dry in summer and off rain.

• Competition

• Capital intensive business

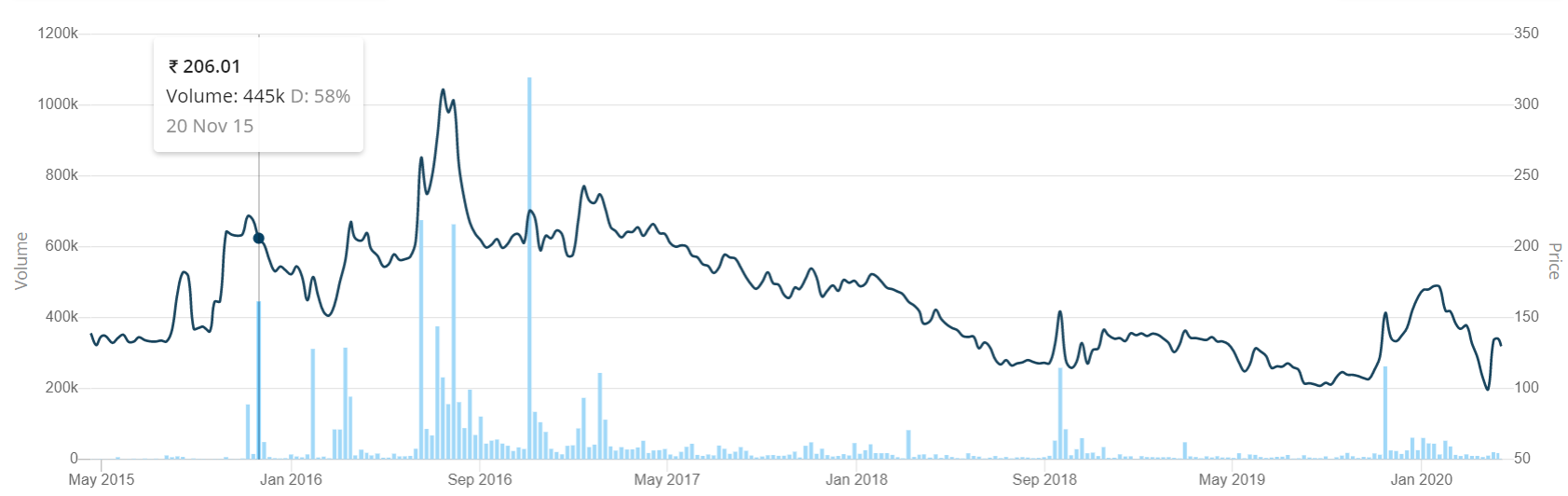

At current price of 900Rs per share,you get per share following -

• eps=100Rs

• Dividend=15Rs

• Equity inv=100Rs

• Term Deposit-100Rs

• Cash and equivalent=25Rs

Management analysis

Salary :

1% of net profit

Shareholders:

Couldn’t find any controversy and frauds.

Expansion plan :

2 projects :

- Mill development plan 2 @ Erode unit :

• Completed at 75Cr cost

• Produce pulp

• 1.45L tonne capacity

• 50Cr cost work is under progress - Mill development plan @ Tirunelveli unit :

• Completed @ 75 Cr cost

Conclusion:

Overall company is good till there is good rain,less and easily available RM.Since last year’s Q3 paper industry in India has got favourable environment and thus profits n growth can be seen ahead.Its 18q1 result is good and expected to see growth in further quarters.Big asset companies like LIC has invested in seshasayee papers.However,paper industry has lot of competition.

(Note:final conclusion of this being good or bad investment should be based on your own analysis.

Disclosure:8% of my PF)