Thanks for your views. Appreciate it.

Any feedback on their product proforlio and break up & product diversication plans.

Many thanks.

Thanks for your views. Appreciate it.

Any feedback on their product proforlio and break up & product diversication plans.

Many thanks.

Currently dont have. Will revert later.

I would say that if H1 ebitda implies 10% of gross block in such difficult period, i think safe to assume 13%, though my base case would be 15% of 1200crs now and 1500crs would be gross block in fy23.

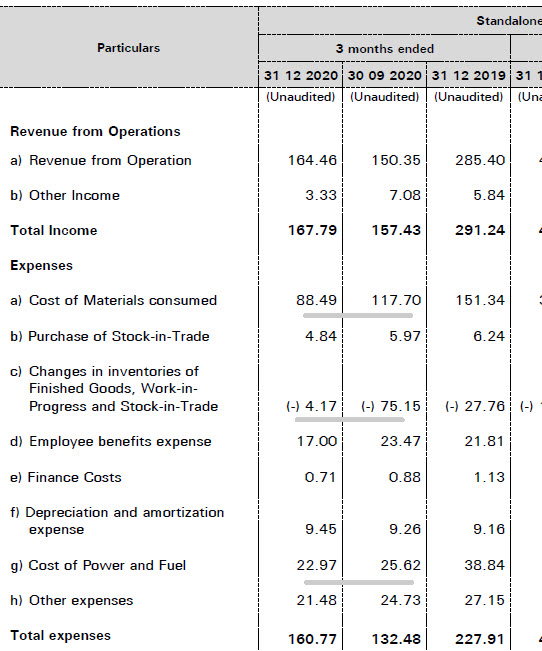

SSPB 2020-21 Q3 results came - Sales 164.52 vs prev Q3 285.46 and Profit 4.65 vs prev Q3 45.82

From company’s notes:

“The lockdown imposed in multiple phases by Central / State Governments in India, to contain the spread of COVID-19 pandemic, had resulted in closure of commercial establishments, schools,

colleges and educational institutions. Consequent slowdown in the Indian economy, coupled with poor offtake in export markets resulted in significant reduction in demand for Printing and

Writing Paper, key segment in which the Company operates. Due to these factors, Company witnessed significant drop in Revenue and profits, during the quarter / nine months ended

December 31, 2020.”

Something that caught my attention is that ‘Changes in inventories of FG, WIP and SIT’ for Q3’21 is back to historic levels of (-)3-4% of revenue from operations. This figure had surged to (-)50% for Q2 and Q1 and hence reduced the expenses and increased reported profits. Also looking at Cost of material consumed as % of revenue - this figure for Q3’21 is around 50% which has been the norm in previous years. But Q1 and Q2’21 was exceptionally high at around 80%. At the same time labor and power expenses have more or less remained flat in absolute terms.

Can someone who understands accounting well help explain what implications can one draw from this?

They have built up huge inventory. 2 reasons i think. Will take care of shutdowns for plant upgradation. They might have thought that lean RM cost could be used for some inventory buildup. Else this co carries zero inventory in March end or low inventory in general. So maybe 1 or 2 qtrs later we will again see drop in inventory and surge in cash, part of which will be used in capex.

True sales.no is weak. More so after seeing jk paper

Interesting insights on Paper industry with comparison between companies :

Also, the article also mention about the impact of New Education Policy on paper stock, though its vague & very brief.

Disc : Invested in my Core Portfolio for more than 2 yrs now !

company has 500CR cash and trading at 4 times cash

ROE 20% + no debt

only concern is growth…for long period

Why all the paper stock give 52 week high break out including seshasayee , west coast , Andhra paper , what is the main reason or its just for bull market run up

its giving proper valuation…because its not cyclical business