Sequents management is guiding to grow from FY21 base and not just FY22 , FY22 will likely be a flat year for the Api business, which implies strong H2. Reading between the lines as H1 business degrew by 10%

12 Likes

Sequent Scientific Con Call Notes Q2FY22

Business:

· Revenues increased by 1.9%: Rs.350 crores in Q2FY22 vs Rs.349 crores in Q2FY21

→ Formulations:

· Revenues from Formulations Business increased by 6.1%: Rs.240 crores in Q2FY22 vs Rs.226 crores in Q2FY21.

· Our businesses in Brazil & Spain which have a greater dependence on anti-biotic APIs from China faced significant margin pressure due to a sharp increase in the input cost.

· Turkey business has been an outperforming business and continues to benefit from our close to a leadership position in the local market and we are very confident of maintaining more than double-digit growth in the local market.

→ API:

· Revenues from API business declined by 10.1%: Rs.1,104 crores in Q2FY22 vs Rs.1,232 crores in Q2FY21.

· There was some decline in API margins as well partly on account of cost increases and balance on account of product mix.

· Expect the growth to accelerate in the coming quarters.

· Seeing muted sales for Albendazole for the last couple of quarters which is largely due to slower offtake from WHO which is a major consumer of this drug for deworming amongst school children in Africa. With schools now re-opening, the WHO demand is slowly coming back.

· A strong rebound from FY23 onwards. The new multi-year contract that we signed with another Top 10 animal company should come in very quickly and FY23 should see a significant spike from this contract.

· Impact of gross margins has to do with the pressures on margins in Spain & Brazil which is coming from API cost increases because most of these APIs that are consumed in these markets come from China given that these are oral anti-biotics markets.

· The share of API business in the overall business mix is down. And within APIs also the product mix has dropped.

· One of the newer products in our portfolio has been validated and commercialized a year or two back. This demand is largely for the US market and in the 2nd year of commercialization, it should contribute over $10 million of revenues for us. We are very well placed for this molecule. There are only two more competitors present for this molecule from Europe. Significantly backwards integrated into this molecule.

· The reason we always talk with confidence about our API business is not that we are taking a competitive position and taking away the market share of others, we are actually working with the so-called innovators and gaining their wallet share. Our business model should not be seen in line with other API companies.

Management:

· MD: Manish Gupta, CFO: Tushar Mistry, Joint MD: Sharat Narasapur.

· The industry is facing challenges due to rising inputs and logistics costs. We have undertaken several steps across the business to mitigate the impact and we expect these to start reflecting in our margins in the coming quarters with the full benefit from Q4 onwards.

· Taken steps to pass on the incremental cost and expect sequential improvement in margins and expect to achieve normalcy from Q4 onwards.

· Strategically we are getting new growth engines with several new initiatives to expand our offerings to include vaccines in India and Turkey. Recently concluded a long-term agreement with a top 10 animal health company. All of this will start contributing from FY23 onwards.

· Continue to make progress in the inorganic initiatives and expect some new growth engines to be added in the second half of the year.

· Qualitatively there is no deterioration in the business. We continue to be uniquely positioned in all the markets where we are, especially in our API business.

· From Q4 onwards we will be back on our growth track as far as margins are concerned.

· 3 years out, the India API ecosystem will not be that reliant on China directly/indirectly.

· We are also in discussions with an innovator

· The vaccine business for Turkey will commercialize in FY23 as the companies which we are dealing with are already registered both as products and plants in Turkey. The India business will commercialize in FY24 as the company that we are dealing with is yet to be registered and therefore that will take 18 months for registration and commercialization.

· We had launched Alivira Italy 2 years back and we have now gained traction there and hit the EBITDA break-even level. In the next 6-9 months we shall be launching Alivira Germany & Alivira UK which will be additional growth engines.

· Fairly confident of maintaining a mid to high teens growth going forward.

· The focus area for Pet animal business is India, Brazil & Turkey.

Risks:

· The industry is facing challenges due to rising inputs and logistic costs.

· We face multiple challenges on the business front due to cost pressure and the recent energy crisis in China.

23 Likes

I was not aware that Sequent’s API is also used in “humans”. I was under the impression that its a pure play animal API business. Looks like it is not

5 Likes

Views change with time and timing is important in this type of stock with cyclical earnings. Sajal even partially sold sequent below 50 rs. He is not a buyer at high levels

3 Likes

I guess we are reading it wrong. Those are not views but facts about the business model. Let us look at those facts-

- 425 K USD application fee per product

- Market size for 90% products is less than 10-20 million USD

- There is no India/China based low cost animal generics player with B2C model

- 80% of FDA approved animal drugs have no generic alternative

- 25%+ EBITDA

None of these points are Sajal sir’s views, they are facts based on Con calls with management and can be easily verified.

17 Likes

As per the annual report, Sequent spends on R&D using its subsidiary SeQuent Research Limited. Anyone aware of the R&D spends?

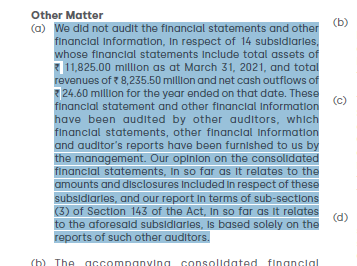

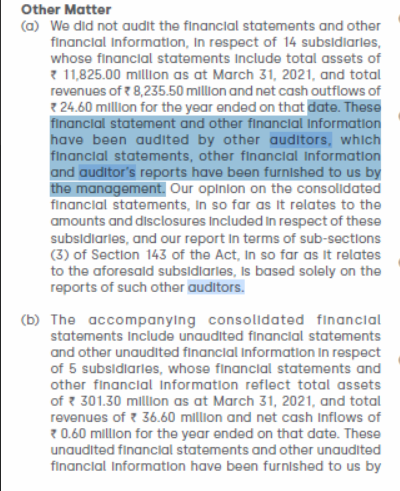

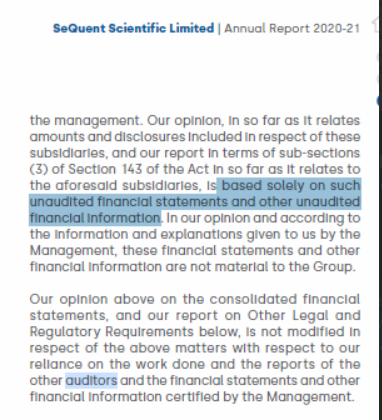

And in Independent Auditors Report, it kind of mentioned they have done financial audit of the subsidiaries

1 Like

Look for the auditor basically saying “I haven’t done the work here, somebody else has given me the numbers & I basically signed off”.

2 Likes

This is pretty standard in all audits where subsidiaries are involved. Saying that as a big4 guy.

5 Likes

3 Likes

Sequent Sci. Acquisition.pdf (2.0 MB)

1 Like

USA m&a may follow soon, what they r doing is setting the S&D network before going for mass scale production & filling , in VET market setting up S&D is a concern, CDMO with USFDA+ API+ volume+ Branded Generic+ S&D+ Huge Network + entry in pet segment = Blast

5 Likes

How does the lira turmoil and Turkey inflation affect Sequent since it is a major revenue and manufacturing source? Today Turkey has hiked the minimum wage by 50% due to growing inflation and lira tumbling

1 Like

it’s only 11% contributor, it generates volume, it also hurts others players as well, it’s a base for meat eating countries non regulated market

4 Likes

Specific to Turkey, Sequent does both manufacturing and selling in the same country, and to that extent the impact will be mitigated but with a lag effect (as price increase of output may lag the cost increase of inputs)… Also, overall exposure to Turkey is only 10-11% of revenue… In my opinion, the weightage to Turkey may fall as % of overall pie even further, due to its organic growth elsewhere and also inorganic acquisitions…Short term margin impact will be there, but medium term it will stabilize

4 Likes

4 Likes

Hi Ishmohit,

I recently noticed that you have exited Sequent in your portfolio. Could you elaborate the reason for doing so, when as late as Nov 3rd you seemed to think that the last 2 quarters were only a blip and the medium-long term story was still intact? Is it because of opportunity cost or you spotted something that could lead to the thesis breaking down?

Asking only for learning purposes and to test my thesis for investing in Sequent (I have a small position, looking to increase). Thanks in advance.

19 Likes

They have ventured in new business in Brazil Sequent Scientific forays into pet segment in Brazil | Business Standard News

4 Likes