What’s the point in scaling up the biz and then selling it out ? In my view he should take it to new heights.

Similar story in Strides people are hoping that Stelis would be listed

What’s the point in scaling up the biz and then selling it out ? In my view he should take it to new heights.

Similar story in Strides people are hoping that Stelis would be listed

As per Sequent 2.0 plan, they have bought out minority sharedsholder in their Brazil operations.

They paid 44.6 Cr INR to acquire the balance 30% stake in Evance, valuing the company at 148.6 Cr INR (1.2x FY21 sales).

Manish Gupta- company veteran - CEO has resigned

In a way it is not surprising as Carlyle would like to put their people in driving seat.

However Mr Gupta and other management team have been allocated ESOP at Rs 86- same price as Carlyle bought Sequent… Interesting time.

Quite a negative in my view. Given past MD ran the show for 5-6 years+. Handing out Esops shows that he was here to stay. What made him change his mind?

One has to be skeptical and not let 10-15% rise in stock price cloud the judgement. As the business is at a crucial juncture of filing ANDAs, acquisitions and operating leverage in Formulation business. Given Animal Healthcare is a relationship based industry, will take time to recover from this blow. It’s a negative in my view atleast. Seems to be Dravid has been bold on a lighter note

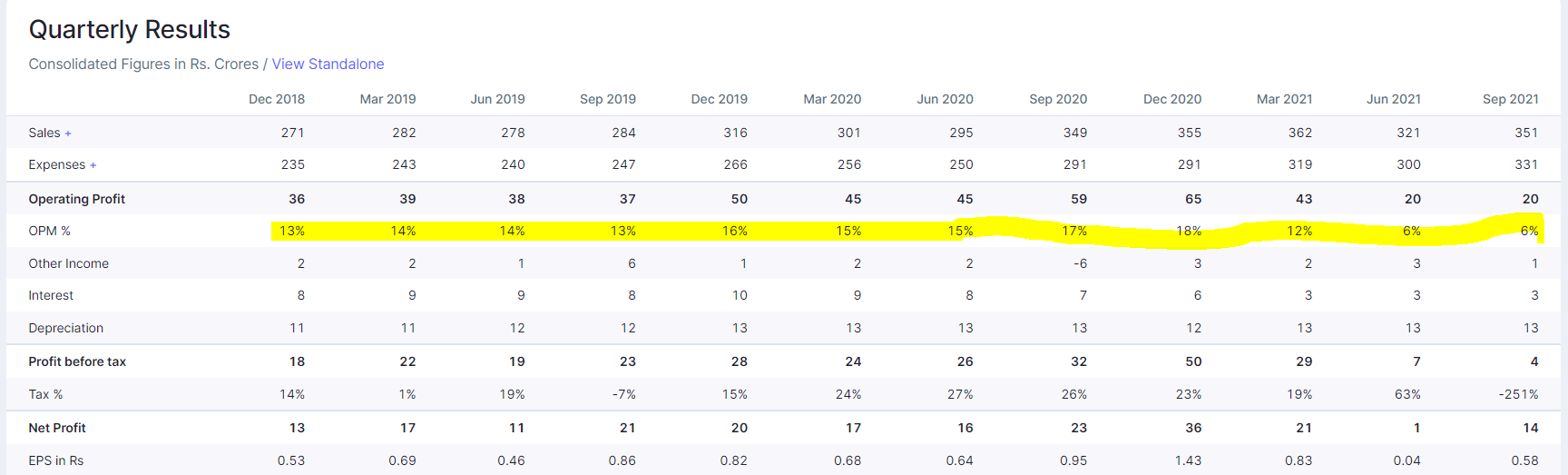

Just an additional Data Point and why it pays to track Quarterly results closely.

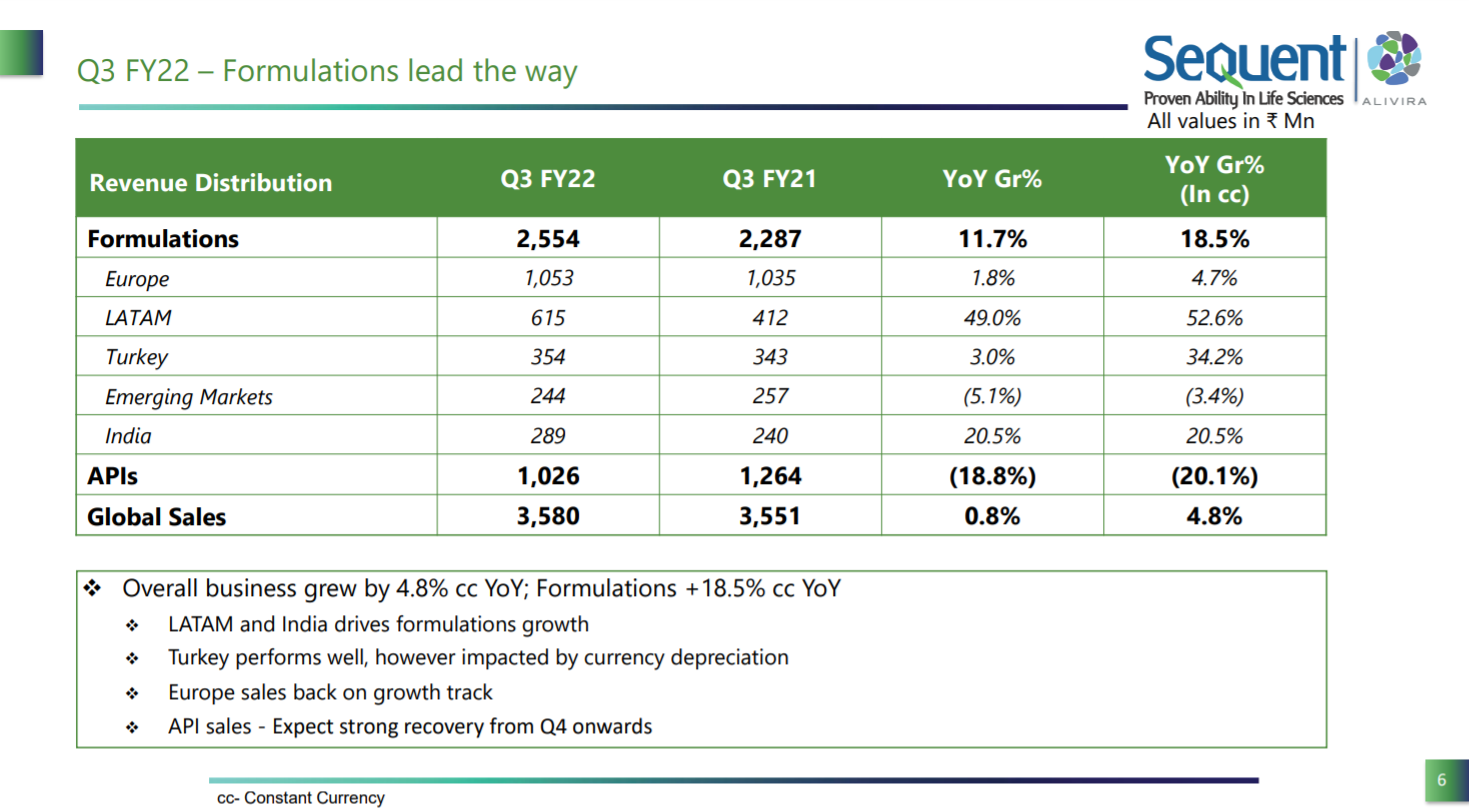

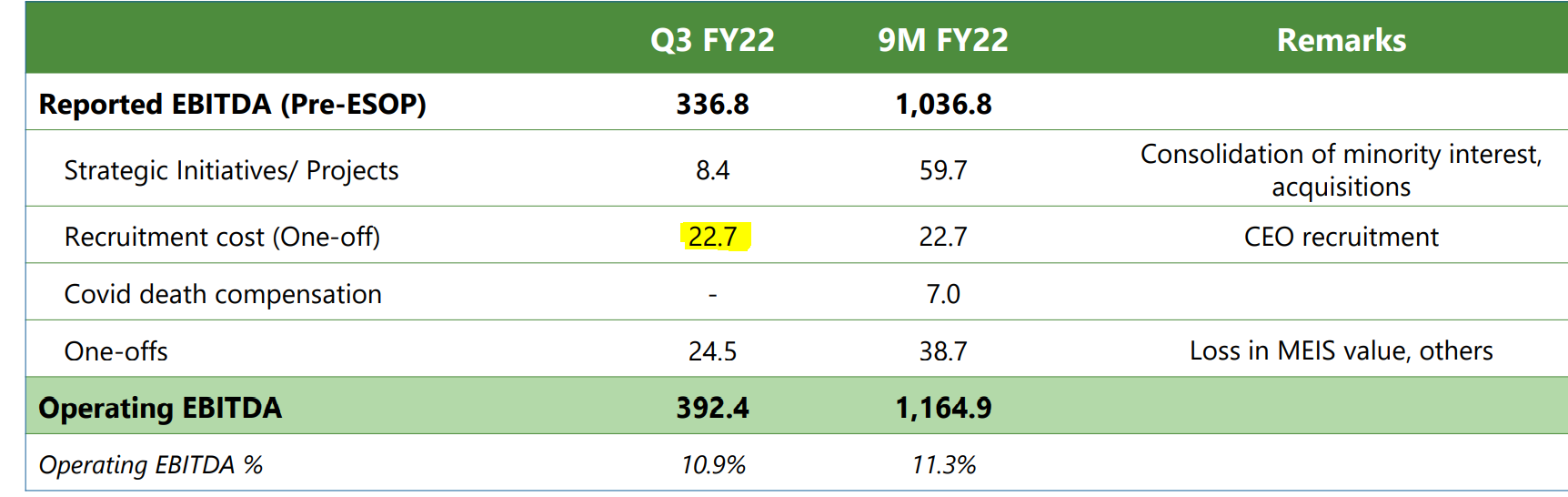

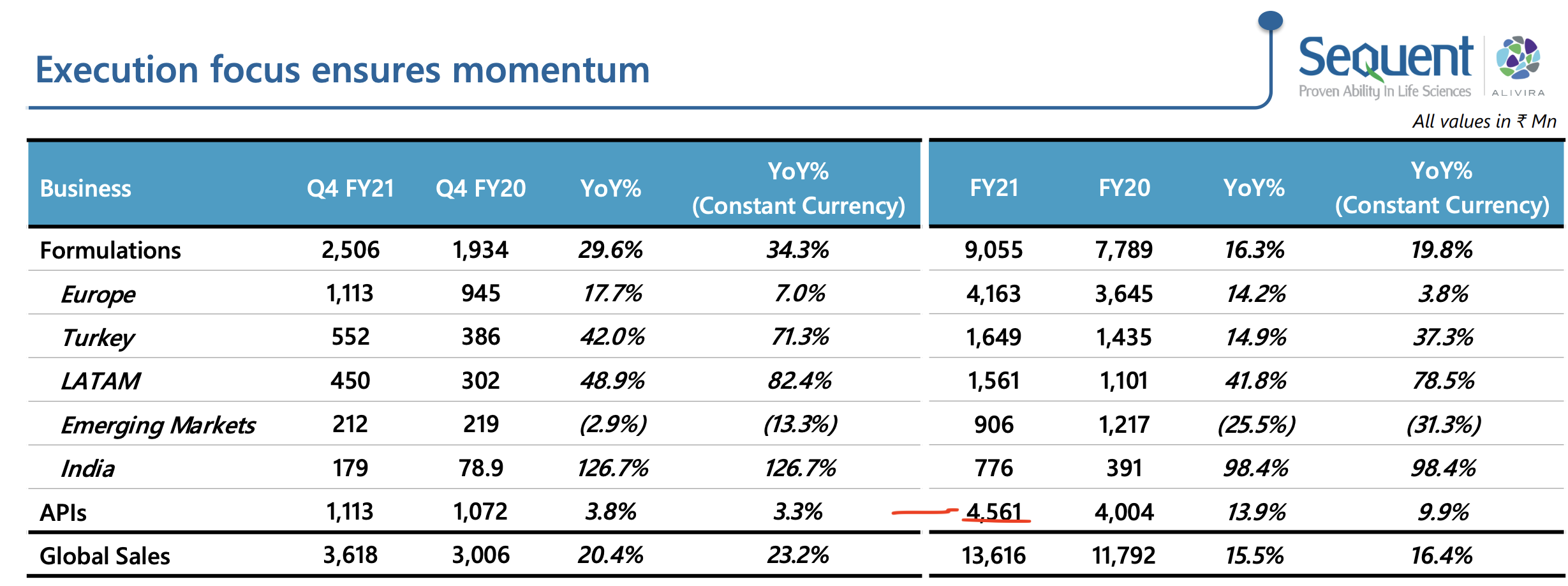

Just check the amount of degrowth in Api business and it’s eventual impact Pre-Esop Ebitda Margin. Small deleverage leading to massive degrowth in margins. What does it point to?

2 simple points come out of this for an observing investor:-

Api business is higher margin than Formulation.

Inverting the datapoint. Formulation business is barely doing 5-7% Ebitda margin and thus sitting on top of massive operating leverage.

Key data points to see in upcoming calls:-

When does the business revert back to mean (Api) which it will start from Q4. And when does the formulation business Operating leverage starts to play out.

Putting this out for investors to track and triangulate further from here ^

Too early to form an opinion in my view. While Mr. Gupta was a great asset for the company and replacing him would be a big task, the replacement looks pretty good as well.

One argument can be that Caryle management and Mr. Gupta were not on same page for Sequent 2.0, but it’s not a negative as it can happen in any organization going through change.

At the same time, we should expect a period of uncertainty (can be short or long depending on Mgmt capability). I would have been slightly worried had it been my biggest holding (or among top 5).

Currently, this event doesn’t alter my opinion about the Company. I will wait out and look for futher updates on this topic. Eagerly looking forward to Quarterly call for further clarification.

If we are co business owners and we know for a fact that

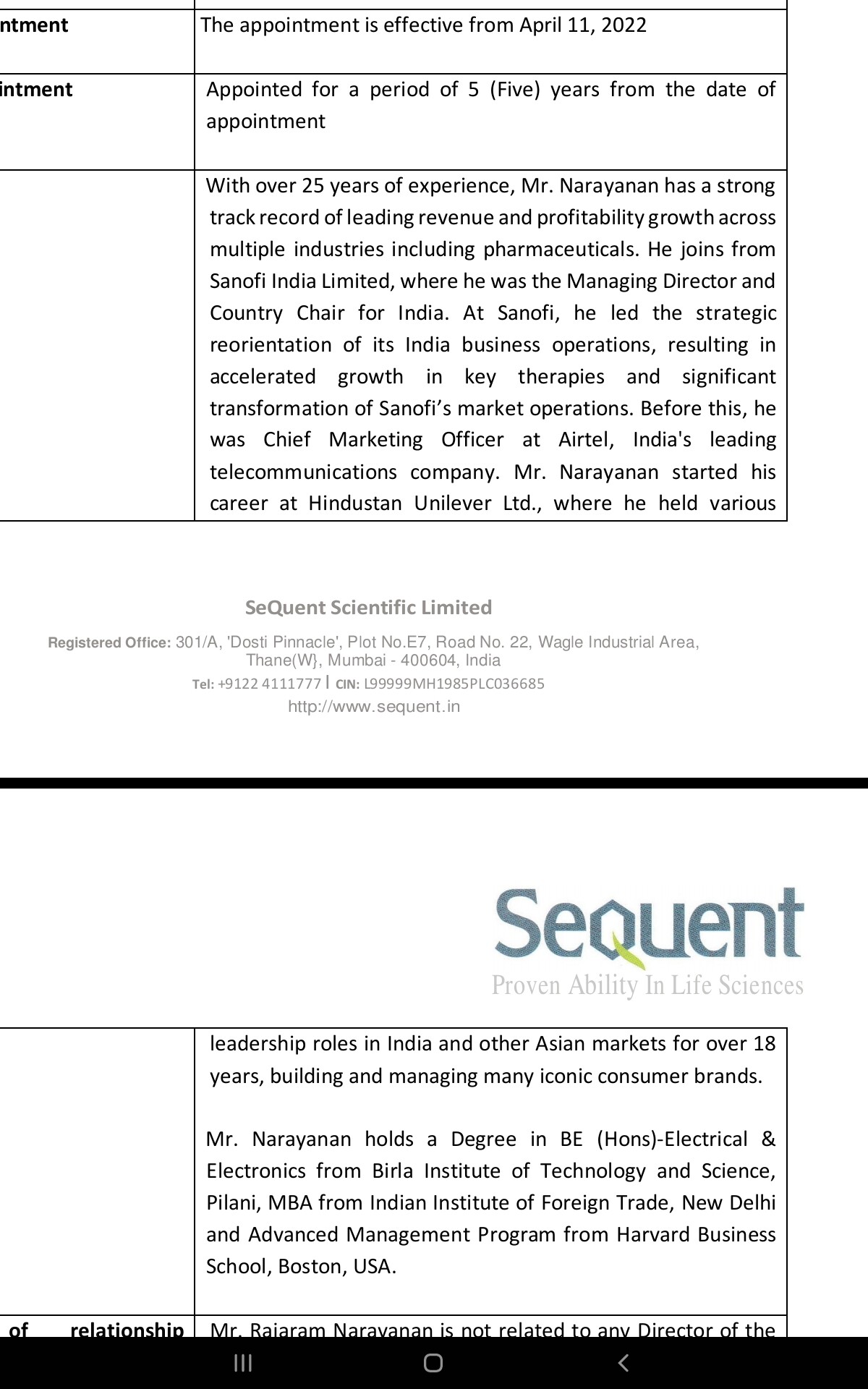

Having someone from Pharma Consumer, brand, FMCG background seem to be a positive for where Sequent is headed ( Alivira, Brand, Distribution, Formulations, Inorganic acquisition etc)

Here is profile of new CEO, seem a natural fit

Street has been bit underweight on script, given past few Qtrs performances, it is more important to have Carlyle aligned professional mgmt , one less variable to worry about, market needs performance and on face value new CEO seems a good fit ( equal if not better)

Reentered recently based on charts

Human formulations and human pharma is drastically different than Animal pharma in my view. Only distribution element remains the same. Will be a learning curve for any new CEO joining from a different non animal pharma co. Just my two cents.

Rest co should do well 2-3 years out from here.

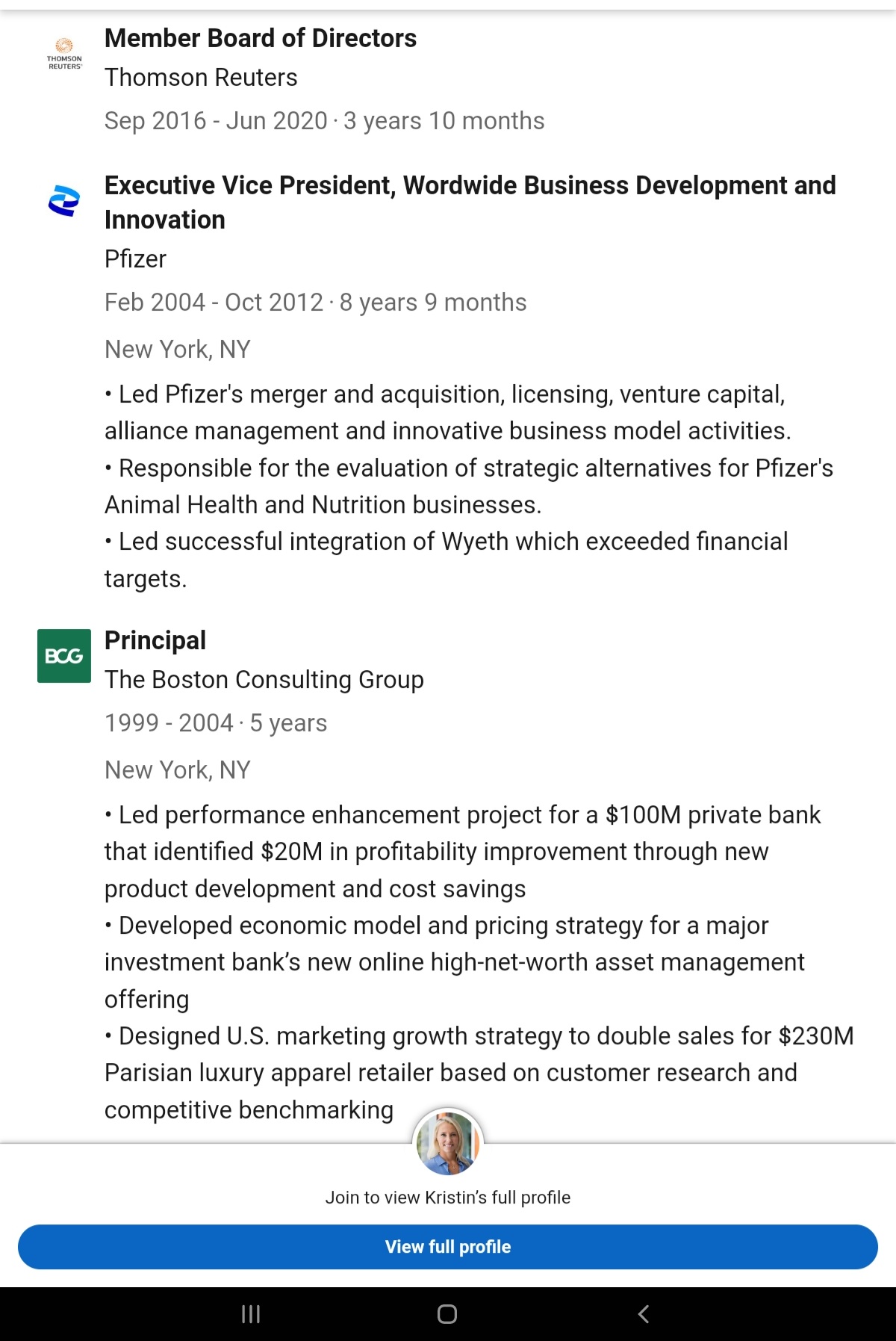

Zoetis CEO seem to be from interesting background as well (pharma consumer, consulting, marketing, investment banking) - Carlyle seem to be taking similar path…just a case in point

Zoetis used to be a part of Pfizer. Experience does talk about managing the animal health vertical in Pfizer ^

Can be interesting. Beyond a point, very difficult to know. Hope the co does well

Very Interesting development.

Just narrating one of my experience. May be relevant / may not be. But just sharing.

I have a friend in his 40s , who runs a auto-ancillary part manufacturing foundry. Few years back he received an order from an international company. Being very important order, he himself stood there and made sure all the components are up to the standard.

Well his that order was accepted but the company refused to place any further orders.

When my friend enquired he came to know from one of the company executives that the products were good quality but the owner was standing there during all the process. So the company didn’t want the person dependency but wanted some proper system / process in place.

So big corporates also try to have a proper process / system in place so as to avoid such person dependency. Deepak Parekh, Aditya Puri and N. Chandrasekharan are great CEOs but HDFC, HDFC Bank and Tata Sons must be giving more importance to the SYSTEM / PROCESS than one single person. And we retail investors must try to be partner with such businesses.

Just sharing

Regards,

Dr. Vikas

Interesting development. A snapshot from one of the old media release dated 2016, by Sanofi, detailing marketing and distribution agreement between Zoetis and Meril (subsidiary of Sanofi).

Very true but in my honest opinion, this is fanciful. The world bets on people.

The valuations of Tesla are a bet on Elon Musk. V Vaidyanathan of IDFC FB. Dr. Chava of Laurus. Venkat Jasti of Suven. People set culture and processes. Otherwise every process is malleable.

If someone has spent enough time in MNC culture, for him it would not be surprising to see organization change at regular intervals. Carlyle would have had there checks & balances (read multi level / multi country approvals process) before this change. Also these organizations have zero tolerances any compliance violations. From this episode, I read that Manish’s knowledge and experience was utilized in forming Sequent 2.0 now management is finding more comfort running the show with new jockey. Generally management changes at higher level takes 6 months for execution so there is high probability of this change getting initiated atleast 3 months prior to exchange notification.

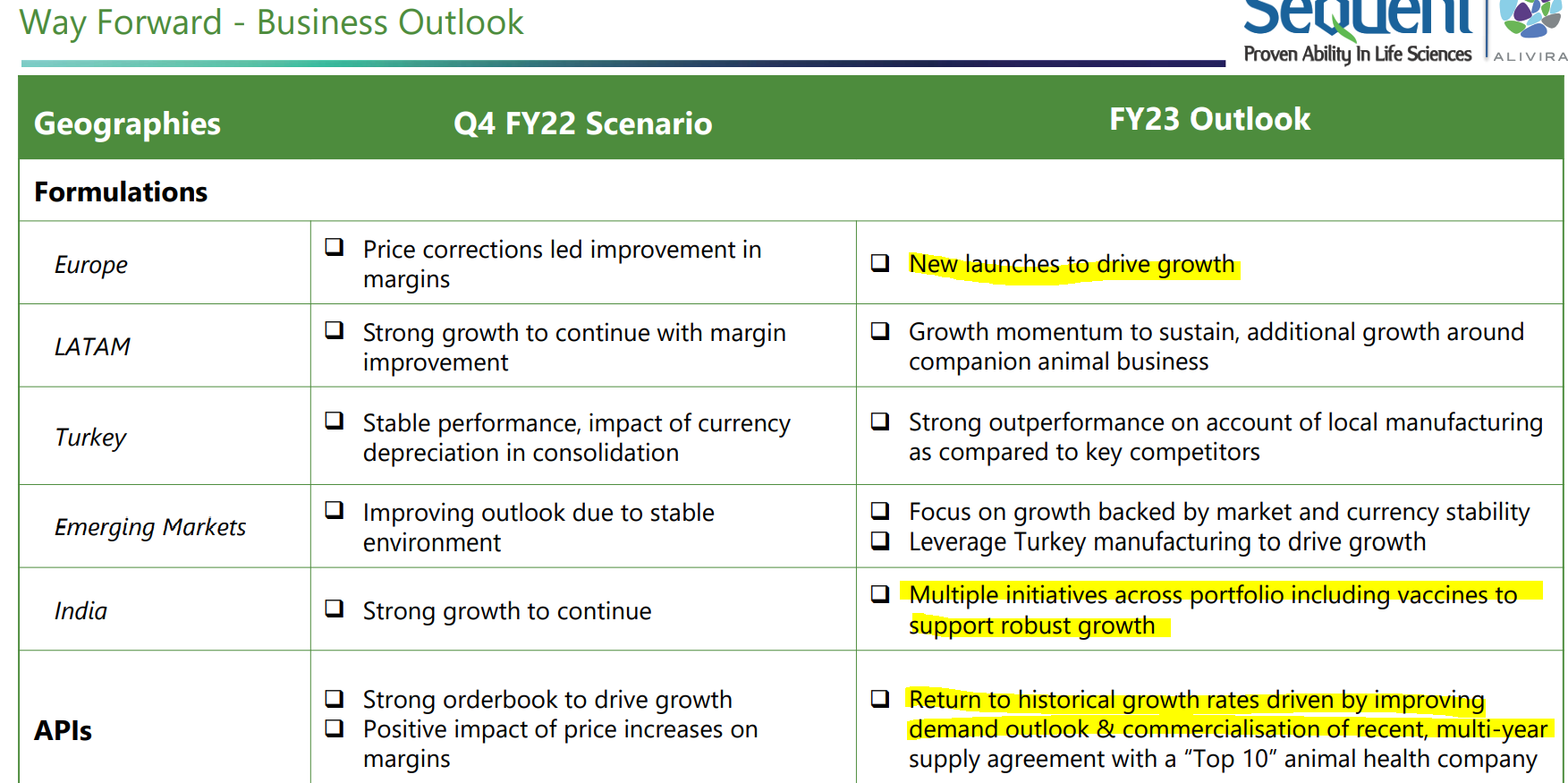

Any view analysis on recent Q3 FY23 results.

Poor streak continues

Gross margins have dropped again by 1% Q-o-Q, no growth in revenues Q-o-Q or Y-o-Y. Only reason EBITDA looks better than last quarter is due to reduction in employee cost (Related to reversal of ESOPs granted to erstwhile MD).

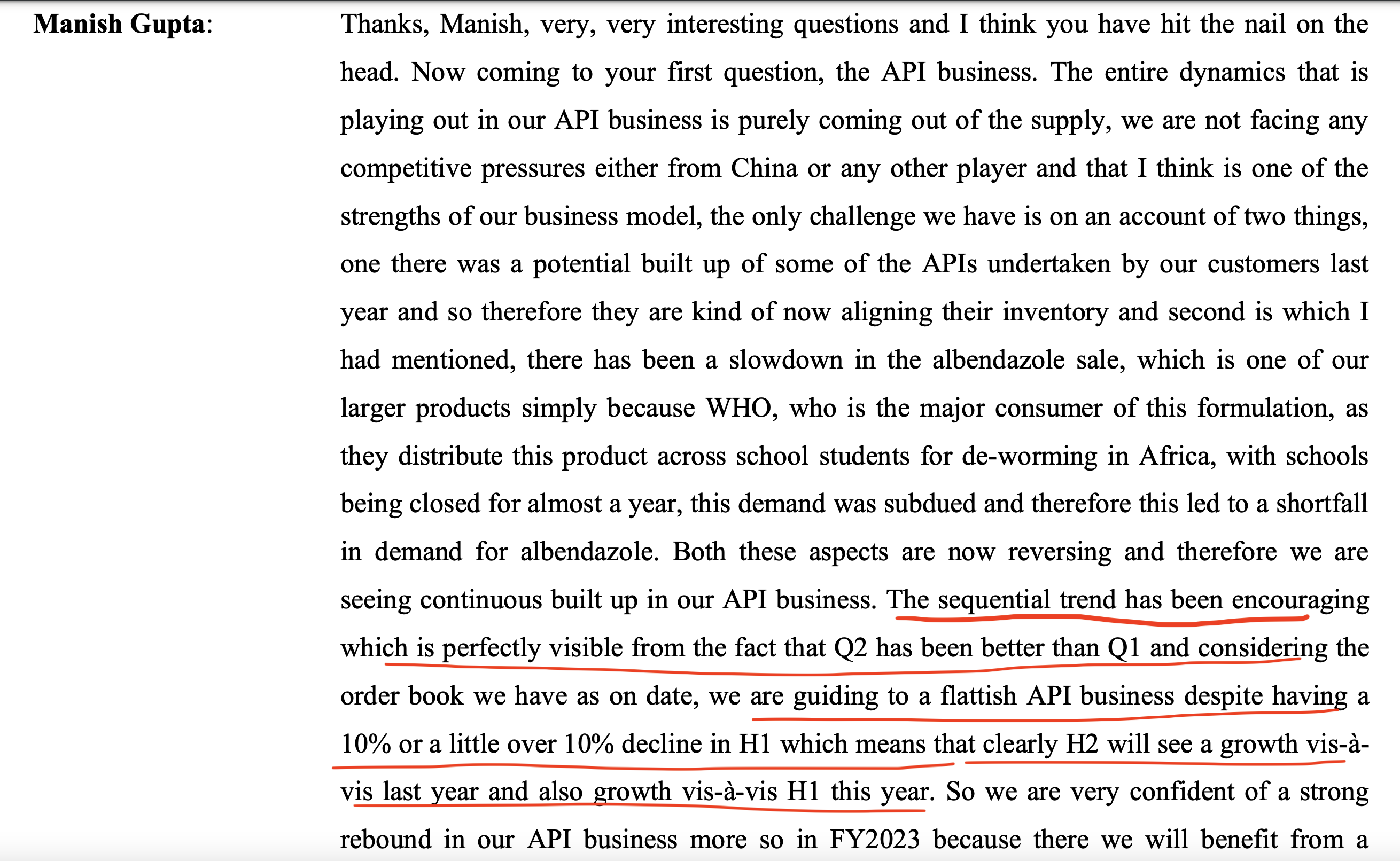

Poor performance in API segment continues. Q-o-Q de-growth in API revenues. Last quarter CEO had promised that H2 will see recovery in API revenues and they will end the year flat for APIs. That’s clearly not happening, will probably end with a 30% de-growth over last year. Albendazole sales haven’t picked up yet.

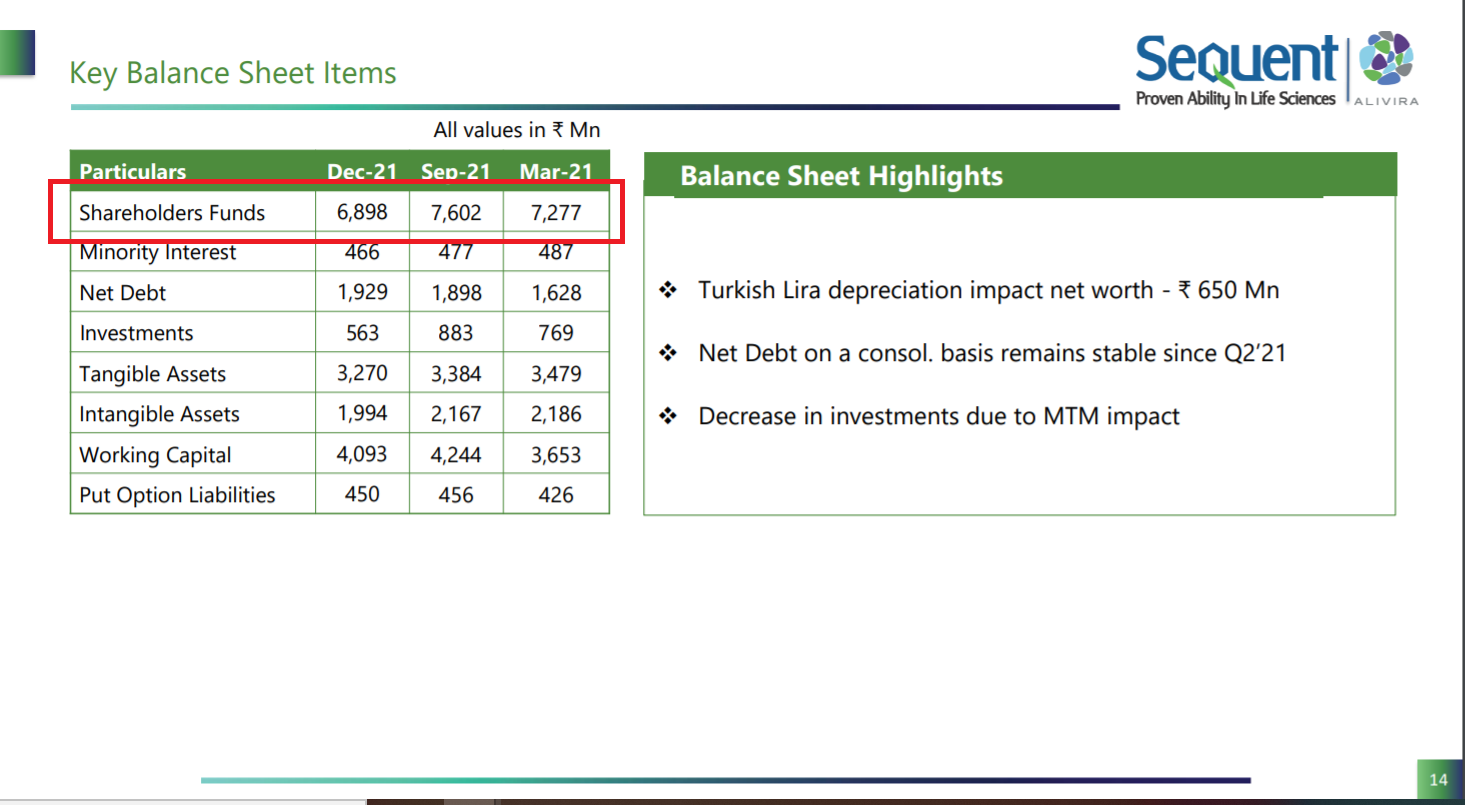

Turkey lira depreciation has caused erosion in Shareholder’s equity by 65 Crs Q-o-Q. I am trying to think how is this possible? Lira depreciation can cause revenue erosion, but how does it erode equity? Were they holding some investment assets in Turkey which have had to be marked down? If Turkey issues are going to cause equity erosion, that should be cause for concern for investors.

Concall scheduled for tomorrow (Saturday) 9:30 AM. Guess they are hoping nobody turns up.

There are some one off in the result- 2.5 cr for CEO recruitment.

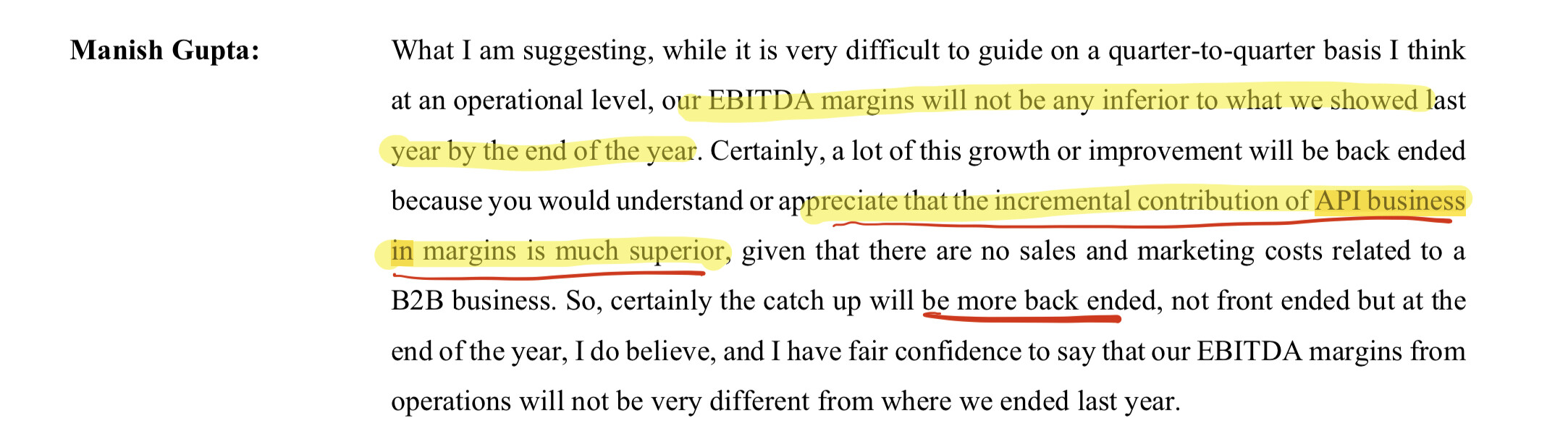

Hopefully Q4 onwards should be business as normal as ESOP cost will reduce and RM prices hike in place. Worst seems to be over.

Let me delve into just API number. In Q2 con call, they said YOY API growth will be flat.

In FY21, API sales were 456 cr.

So far TYD, sequent has done API sales of 304cr.

If we go by words of management, they need to do API sales of 150 cr in Q4, which is 50% of YTD (Q1+Q2+Q3) of API sales, with higher prices as management (price escalation happens at the start of new calendar year starting Jan).

…and API is a better margin business

So just based on API, additional 50 cr of sales (150 cr - 100 cr of Q3) shall result in decent PAT. I think they can report one of the best quarterly profit (keeping everything else same) in Q4, hence I said above that worst seems to be over.

Additionally, their OPM shall improve (regression to the mean) to mid teens (13%+). It may take few more quarters, but it is likely to be on upwards trajectory going forward.