Dear All,

They are selling as they are exiting prompters. They have sold large chunk of their stake at Rs.86 per share to Carlyne and now they are selling rest of their holding. so no worries.

holding

thank you.

Dear All,

They are selling as they are exiting prompters. They have sold large chunk of their stake at Rs.86 per share to Carlyne and now they are selling rest of their holding. so no worries.

holding

thank you.

Turkey has been added to the FATF grey list. This may result in weakening of the Turkish Lira and potential impact on trade, at least in the short term. Rating agencies could downgrade the country. I’m not entirely sure of the consequences this may have on Sequent, but it is bound to make institutions uncomfortable. Could be one of the reasons for the price action. Request anyone with more information to please share.

Pardon my ignorance, I didnt quite get the connection between Sequent & Turkey.

@sougataG Turkey makes for about 20% of Sequent’s business and is among the highest margin contributors with large share of injectibles

The article says that the FII exodus from Turkey has been on since an year or so…it would accelerate. What is new as on today as per the article?

Also, FII investment is one thing and doing business can be another. Will exodus of FII reduce turnover & profits for Sequent in Turkey? If yes, how?

@Investor_No_1 As I said in the post, I am not entirely sure of the consequences that Turkey getting added to FATF will have on Sequent. The article simply talks about the anecdotal impact that getting added to FATF typically has on a country’s investment climate and currency.

We know Turkey has been added to FATF and we know that Sequent has a reasonable exposure to Turkey. Whether or not this will materially impact Sequent’s business, or us it just short term noise, is for us to figure out. I am not sure, and am hoping that someone with a better understandings of the issue can throw some light.

if we have gone through previous concalls , we can fairly say that Turkey is always a unstable business for Sequent. That is the reason they are making lot of efforts to move the business to regulated markets (USA & Europe). Please don’t forget that they recently started CDMO business and I believe zoetis is their biggest client. I personally feel, these few coming months are excellent opportunities to accumulate this one of the kind business

https://www.bseindia.com/corporates/anndet_new.aspx?newsid=87b396e6-7464-44dd-be77-9a64c269db5c

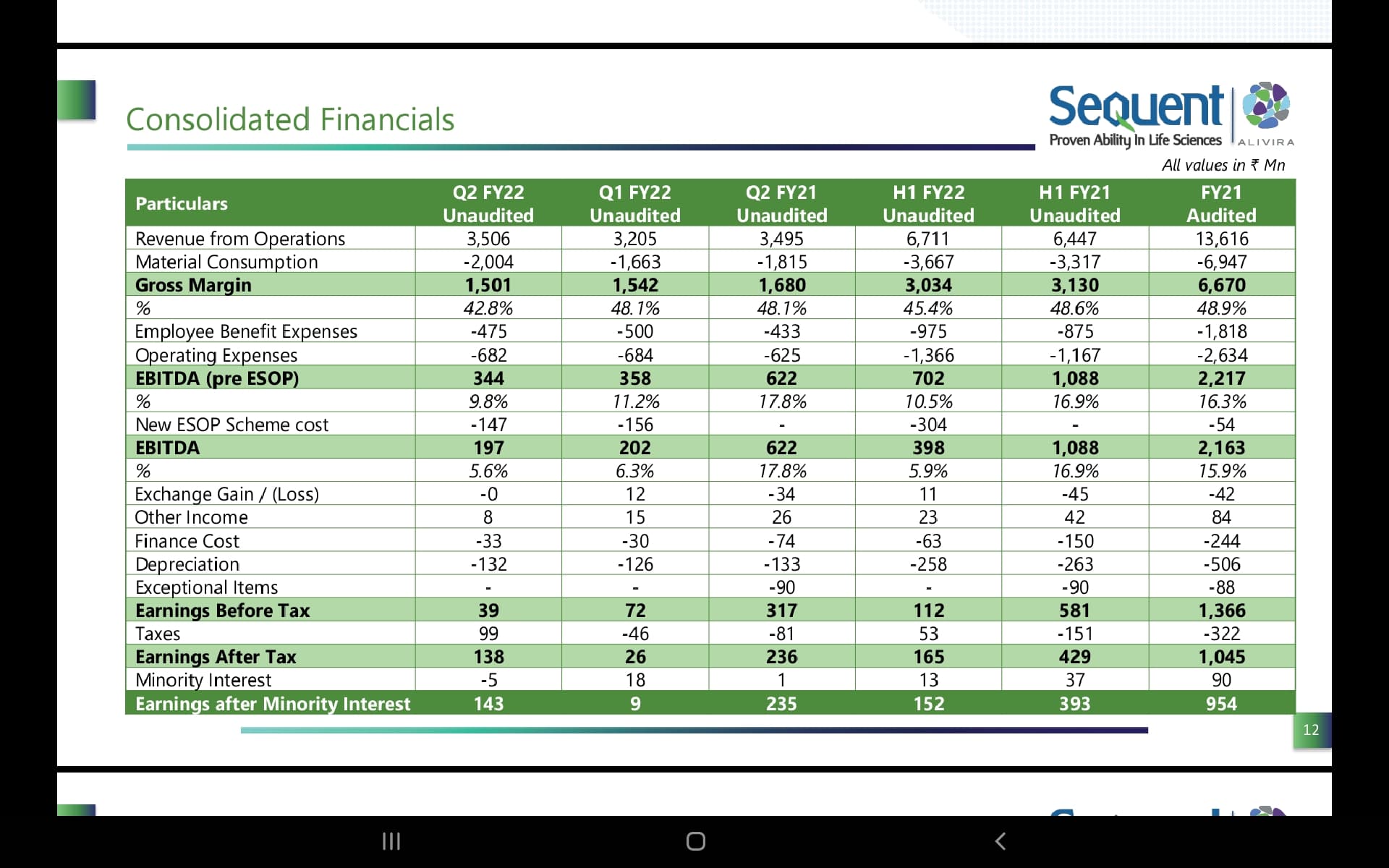

Results are out

Sequent has been a good learning experience on expectations build up vs reality mismatch as well as risks that investors tend to ignore during momentum.

It’s clear from results that things when slide, seldom turn around in short time, also given if a sector falls out of flavor takes time to come back in vogue- as is the case of Pharma set.

Tracking position - intend to add slowly

Looking beyond the reported numbers and at the commentary. Seems entire industry has been suffering from destocking and RM issues (temporary or structural, one has to form their own views). Ex of Albendazole (they Debottlenecked at Mahad in FY21), Api portfolio grew by 25%+ due to due to lower offtake as WHO demand lagging (reason given: Closure of schools and no deworming programme). Topline recovery is good, gross margins contracting could be a one time issue due to RM hit that the entire industry has gone through.

Where do we go from here?

Likely data points will be to get the view on the margins to come back to normal in H2 of this year+ Management has indicated in the past call that growth will comeback from FY23 onwards. They will be growing on FY21 base and not FY22 base

A good case study in market psychology:- initial euphoria driven by Carlyle purchase has settled down. Now the business has to perform in next 2-3 years. Another positive sign was the long term contract with a global api company. If these issues are transient (Rm hit& destocking) or not. One has to take an individual call.

Disclosure:- invested since last November. Saw the entire human psychology and business narrative bit playing out as a live case study for me to learn.

Not sebi registered. Not a buy/sell

Turkey’s business saw good growth but the country macro also compounded the headwinds. They are trying to build an export business from there I would like to see how that plays out

Disclosure:- Invested

I wonder if it is actually an industry-wide issue. Both Elanco and Zoetis reported good numbers last quarter (in fact, both raised their guidance), while Sequent struggled.

It’s an input cost pricing issue. The companies you’re mentioning are more into companion animals and do gross margins above 60%.

That being said:- Two key data points I was looking for, Margin recivery in H2 and FY23 subsequent growth. Concall was satisfactory and got the answers.

They will be initiating cost hikes from Q3 as they enter into fixed contracts with the innovators for the APIs towards the end of financial year (Financial year followed by innovators).

They have signed a new long term Api supply deal to a US top 10 Animal Api company, where there is only 1-2 other European suppliers.

Api business guidance to be flat this year, given it degrew in H1 by 10%, H2 likely to see strong growth compared to first half of the year.

Albendazole was impacted due to closure of schools in Africa.

Where do we go from here? Part 2

-Intitial euphoria has died down which is good in a way.

-If the business starts delivering again (all indications it will). They will easily do Ebitda of 250-270 crores in FY23 and grow much faster in FY23&FY24 on a subdued base.

-Long term guidance remains the same.

Key learnings personally, as always there’s much to learn from @hitesh2710 sir, that profit booking done at peak narrative and numbers lagging is not a bad strategy. Learning from a trading/momentum mindset can actually help investors in the journey of a stock.

Disc: invested. Renforces the view, that why being humble is important in markets

Few points in addition to @Worldlywiseinvestors Post

One aspect that is probably being underlooked currently in all stock price movement mayhem is Role of Carlyle in driving growth

Market enthusiasm and narrative is well placed if spread out on longer duration with reasonable returns expectations, unfortunately that’s not how market participant and psychology works. Also believe when a sector is out of favor it takes time to come back, FOMO and average down is real issue for retail in such counters.

Tracking position

What is RM here? I am new to investing and do not know a lot of financial terminologies.

Thanks in Advance!

Rm indicates raw material  sequent uses Api from China and Ksm+intermediates as raw material

sequent uses Api from China and Ksm+intermediates as raw material

Thanks Ishmit. I share the same enthusiasm for the business. My key investment thesis is:

Risks

Also, I think that most people missed that the business was over-earning in FY21 because of COVID. Its a sales and marketing heavy business - sales team needs to travel to generate demand and because of COVID it could not travel and that was the entire saving flowing to EBITDA. I estimate that such savings were as high as 200bps and therefore true EBITDA margins in FY21 would have been 13-14% instead of 16% what we saw.

In light of all the above, cost inflation, and slowed demand has eroded ~4% of EBITDA margins (16% reported in FY21 minus 2% over earning due to sales and marketing savings - 10% reported post ESOP adjustment).

Where do we go from here

Questions still unanswered:

Disclosure - not invested, but tracking and doing more work!

Apologies for some more notes on this. Did a bit more reading and I stand correct that Both Elanco and Zoetis have also reported significant pressure in the supply chain in Q2CY including inflation in employees cost, logistics cost, and manufacturing cost. Due to the nature of its business in favor of companion animals, they could take some price hikes (~2%) but did not fully pass on the inflationary cost. @Worldlywiseinvestors had already mentioned this in his post. Both Elanco and Zoetis will report Q3CY results today/tomorrow which should give us more sense of the supply chain pressures.

Also, some notes from Animal Health Conference attended by someone in my connection

its due to the reason called our by management that they can negotiate prices of API only once a year , so seller’s disadvantage is buyers advantage hence Zoetis hasnt faced the issue ( my guess )

COVID time was an exceptional year for the customers - both in animal and human health. Considering these are very efficient customers who would want an assured supply chain - would there be potential that the big customers increased inventory levels and kept them high during this period - to ensure that they could always keep producing despite an uncertain external environment? This could have then led to elevated demand levels in the previous year for APIs (not only Sequent, but others like Laurus as well, I am not tracking numbers for NGL).

In that case, this would potentially not be a temporary destocking phenomenon but probably some destocking + mainly due to demand normalisation? And would 2019 sales be a reasonable sales base for the future as well, versus the higher levels in 20-21?

I do not track Sequent in depth, but this is my thought on the situation in the API industry so might be flawed by how generic it is.

Discl : Not invested