Peter Lynch has a pretty interesting insight on insider selling/buying in his book.

He mentions that Insider Buying is usually an excellent sign, and a good indicator of the company prospects and bullishness of the management on their business. There is no other reason for insider buying other than positivity on the business.

In Insider selling though, his take is different. He says that he learnt to start to ignore insider selling in his companies of interest. Usually the reasons for Insider selling could be manifold, from fund requirements to diversification to even buying a house.

Though insider selling could be a reasonable indicator, it’s efficacy versus insider buying as an indicator was usually much more limited in his experience.

I used to focus a lot on insider selling as well, but just found this facet an interesting read into things.

Discl : Not invested in Sequent as current valuations seem high, interested in the story but missed out on the initial boat.

Couple of incorrect data points being shared here.

Cadila sold their animal healthcare division at 2’921 cr. which translates into P/sales ~ 4.84x, PE ~ 21.1x (FY21 sales: 603 cr., PAT: 138.4 cr., EBITDA margin: 25.6%).

Competitive advantage is always shown in return on capital over a longer time period and returns on incremental capital. NGL has 25%+ ROCEs over the last 10 years and this is being maintained incrementally. Sequent’s ROCE has been all over the place, this is also because of the restructuring of the human API division but simply calling Sequent a moated business because they sell in US is incorrect interpretation. A business’s value is the amount of cash they generate, not where they sell their products.

Almost every large Indian human pharma company have tried their hands on specialty branded generics in US and failed (maybe except a Sun Pharma). That might or might not play out with animal pharma, do we have previous examples of how easy it has been to build on branded generic business in regulated markets?

I saw a bit later that there was some discussion above on this so let me elaborate a bit more on what I am after, and thats not how the price can move. Like @Tar mentioned, we need to see if the business is on track…to support these valuations

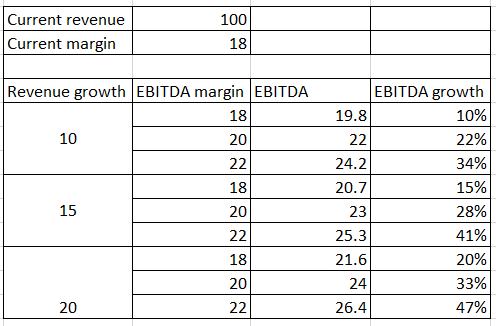

Syngene trades at a PE of around 60x. However, it operates at EBITDA margin of 30-35%. Sequent is operating around 17-18% margins. Clearly any improvement on margins along with a 10-15% revenue growth can make EBITDA grow at faster rates. Just simple calculations below. As a base case I will assume 15% revenue growth and somewhere between 18-20% margins. Then there is a possibility to grow profits by 25% odd.

The question is what margins can this business make? I think the sector is growing at ~12-15%.

If investing was all about looking into the past, sure. But fortunately it is more about predicting the future cashflows and unit economics, not looking into the past. Please read about sequent to understand why the ROCE was all over the place. That is the pain period i was talking about. USFDA approved facilities is the competitive advantage.

As far as my understanding goes, both markets are vastly different. It wont go that way. Besides, Sequent is already into specialty generics, they are simply doubling down here.

As far as I know, no.

Would request you to please study the animal pharma industry. Please do not assume that conclusions about human pharma apply to animal pharma industry as well. A company with stellar USFDA compliance has a compliance moat imo. Agree to disagree if you think otherwise.

2 points there:

This isnt about where one sells products but rather the predictability of cash flows which is higher for markets with larger barriers to entry. India and such like markets have almost no barriers to entry.

Not every market participant subscribes to the DCF viewpoint. You might, others do not. Which is why market price can choose to reflect a reality different than what the DCF model might tell you.

This doesn’t make much sense IMO. The E part already captures the margins. Claiming a co with higher margins should trade for a higher P/E is a fallacy IMO. What controls valuations are narratives around:

Unit economics and where it is headed

Topline Growth

Strength of durable competitive advantages resulting in stability of cashflow generation.

In any case these valuation discussions are unending and non tractable, so no point indulging in them any more than necessary. (last message from me on this topic).

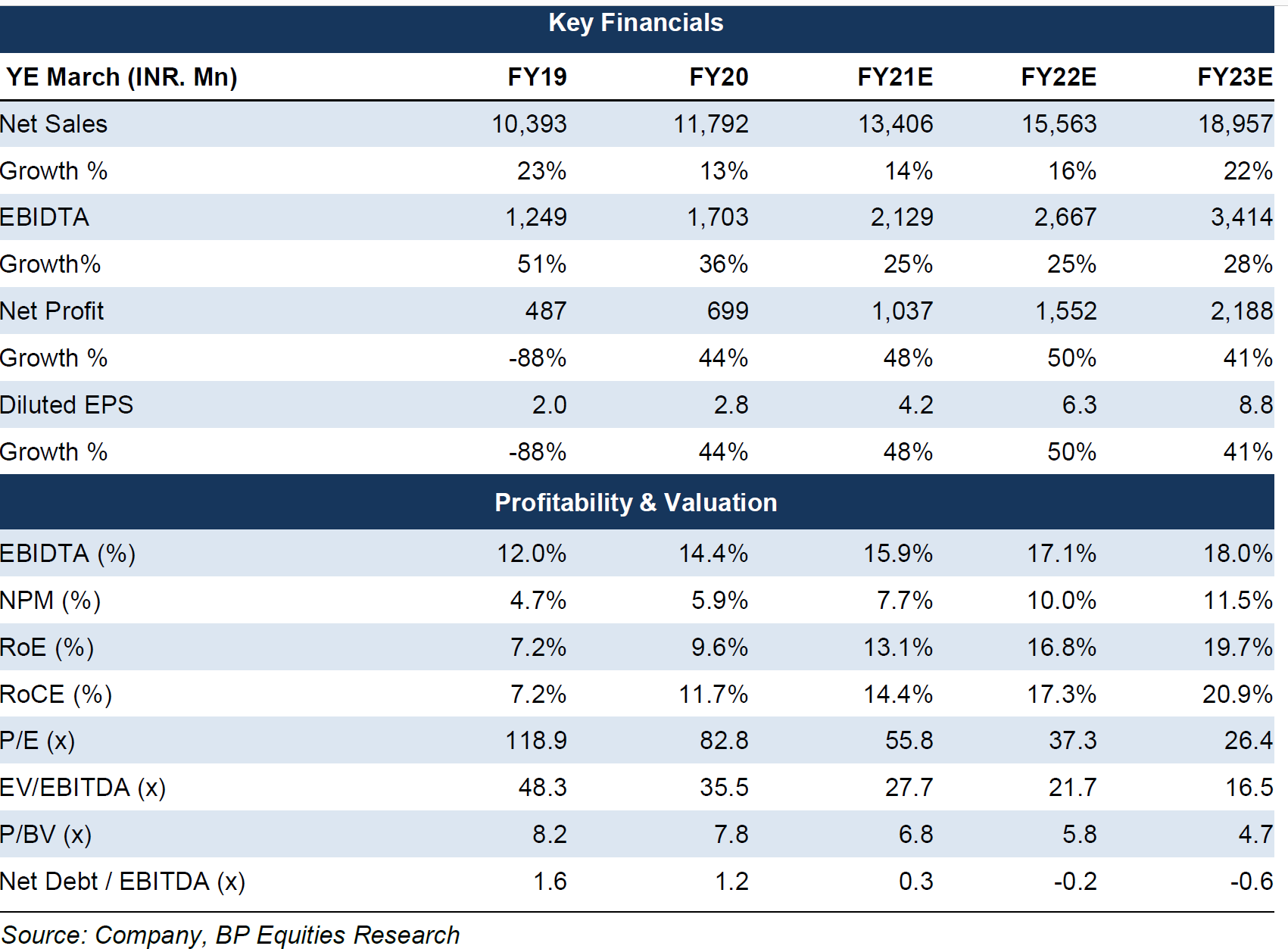

Below is a snapshot from BP Wealth report in Feb. Not taking it as written in stone but some broad level estimates

“We foresee 17.1% revenue CAGR, 356bps margin expansion, and 46.3% growth in earnings over FY20-23E. The balance of portfolio among high value/ low volume products with operating leverage kicking in to help it clock a faster growth in earnings.

At the CMP (INR 233), the stock trades at 26.4x FY23e EPS and 16.5x EV/EBITDA.

We downgrade our rating to Hold (from Buy earlier) with an upward revised target price of INR 264 per share (earlier INR 224), valuing the company at 30x of its FY23e earnings.”

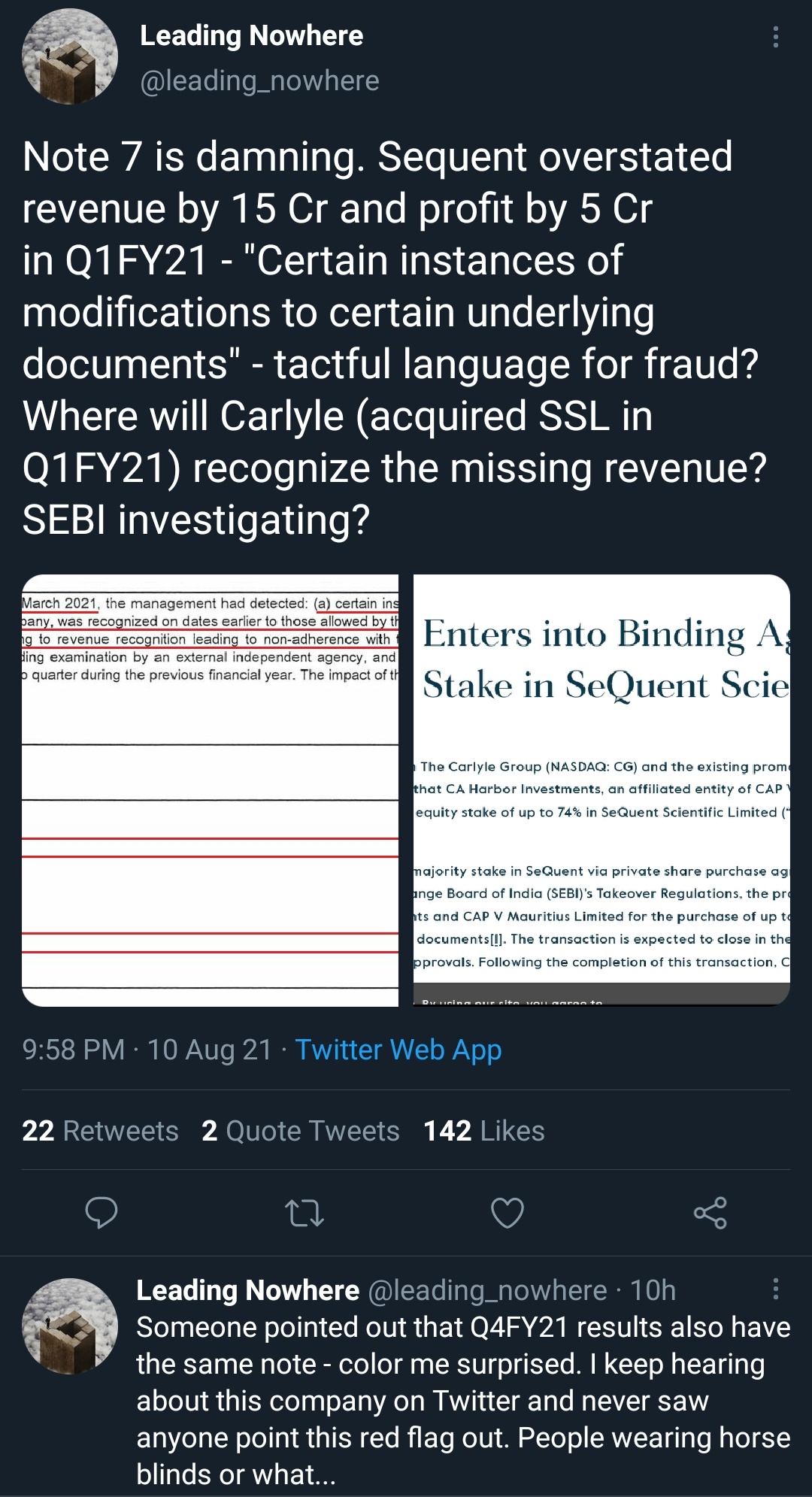

Irrespective of the mis statement pertaining to last year, there is a lurking fear in the market that there may be more cockroaches when one is detected… Sentiment has taken a hit.

Disc: Invested and no transactions for the past 30 days.

Management hasnt changed much since carlye got onboard. Manish gupta is still incharge. Yes, There have been some additions to the board.

I have always liked this management and have no reason to think they are dishonest. Cant say that about Carlyle group with the same level of confidence. They have been linked to cases of financial engineering in the past(George Bush Fiasco, Hertz IPO etc).

For now i ll give them the benefit of doubt but i try not to catch a falling knife. Lost way too much in the past this way. Its best to let things cool down in such cases.

I was reading some news on this Q result and management has mentioned these irregularities, its impact last year and also corrections done etc. along with this Q results…therefore this topic maybe coming into forefront now…

It’s a non material issue. On the other hand there was also upfront disclosure related to auditor observations in the annual report which the management very proactively clarified in the concall. Quarterly volatility has led to such price action, former is not a material issue in my view.

Disclosure: invested, transactions in last 30 days. Not Sebi registered

Before coming to financial performance, I wanted to bring to your attention that during the financial closing for the year ended March 31, 2021, the management detected certain instances where revenue in respect of certain sales transactions were recognized on dates earlier to those allowed by the group’s revenue recognition policy as well as certain modifications of underlying documents relating to revenue recognition. The management brought this to the attention of the auditors and the Audit Committee. And under Audit Committee supervision, a detailed review was undertaken, and all cases of such nonadherence where revenue recognition was accelerated were identified. The Board has taken the findings on record. The financial implications, though not material, are comprehensively detailed in the note to the results. We have corrected the processed leading to such nonadherence, and we’ll continue to strengthen them further. And there is no continuing impact.

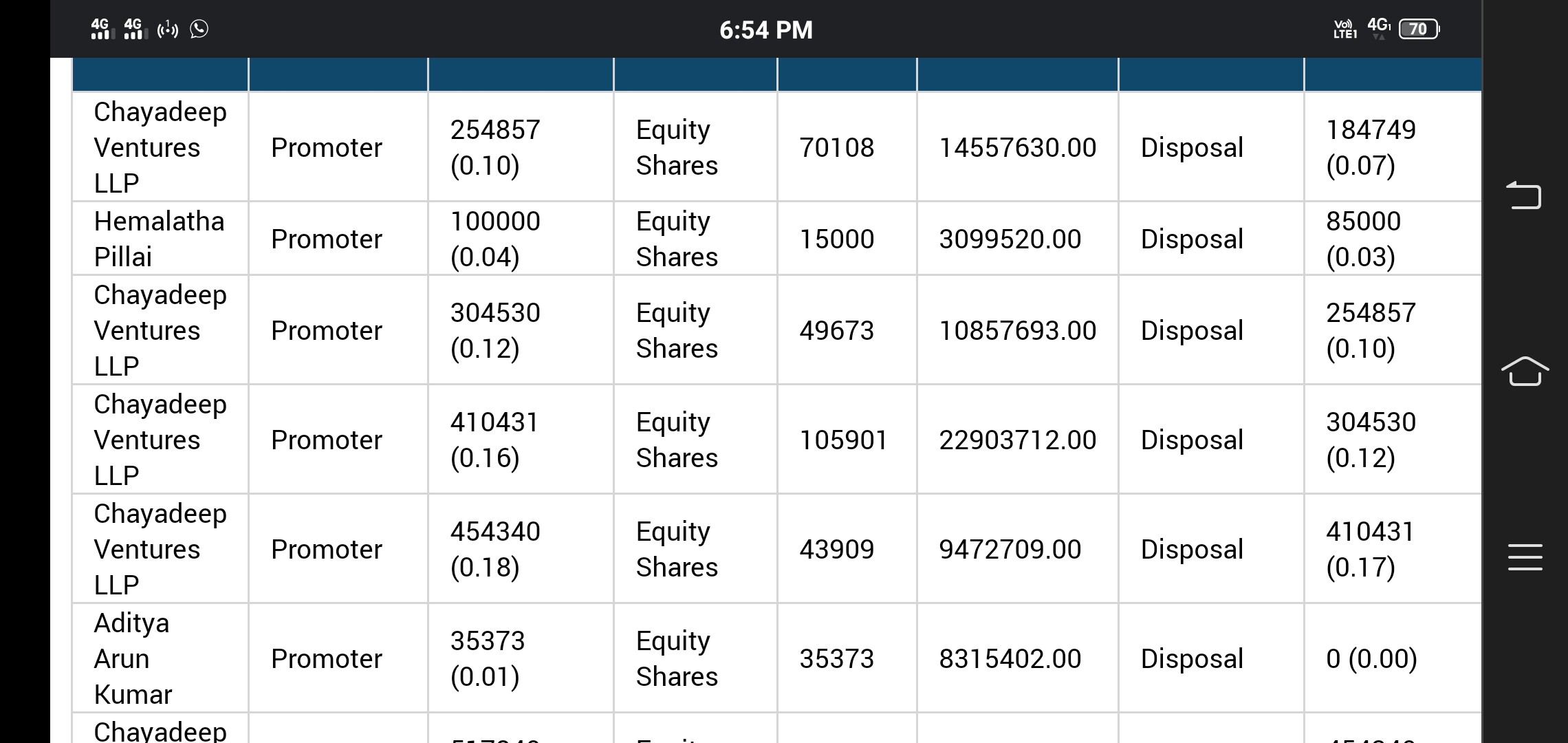

Promoters are selling their stakes in open market. Aditya Arun Kumar has sold his complete stake in the company and Chayadeep Ventures also selling the stake in open market. Is there anything that insiders knows and retailer doesn’t.

I think they are previous promoters yet to be corrected, now Carlyle group are the sole promoters, these people are promoters of solara which also they are trying to sell , it is their usual activities since stride days