This seems to be an exciting news. Probably a product launch in Companion animal space.

-

Global animal health market size stood at US$33 billion in CY19 and is projected to grow at a CAGR of 4.9% to reach US$46.1 billion by 2026. The production animal segment accounts for a larger pie of 60% and the balance 40% is companion animals. Sequent, has strong capabilities to capitalize on these emerging opportunities.

-

Production animal health market size stood at US$20.5 billion in CY19 and is projected to grow at a CAGR of 8.2% between 2019 and 2025. Companion animal health market size stood at US$12.54 billion in CY19 and is projected to grow at a CAGR of 6.2% by 2024.

-

Sequent changing orbits in an efficient manner. The unseen capability of filings & CDMO will be seen over time. There is an increase in the sales of antibiotics for farmed animals in the US for the second consecutive year 6.1 million kg of antibiotics were sold to US animal producers in 2019 revenue from antibiotic therapy stands at 42% in FY20.

11 Likes

Detail Analysis of Sequent Scientific in simple and lucid language

22 Likes

Consolidation of Shareholding in Fendigo SA, Belgium to make Fendigo SA a Wholly Owned

Subsidiary of the Company

https://www.bseindia.com/xml-data/corpfiling/AttachLive/02066f42-5132-42a7-bc45-e25ad86defd0.pdf

1 Like

Sequent has launched a new pet care division

disc. Invested

10 Likes

@sahil_vi Curious to hear your opinion on current valuations.

This is now trading at TTM PE of ~69x and EV/Sales of 5.0x, which leaves very little room for upside IMO. FY23E consensus estimates of EPS are Rs.8.8. Considering Zoetis’ current TTM P/E of ~45x, I don’t see this trading higher than ~40x in the long run considering the much inferior margin profile. This would imply a share price of 352 in 2023.

4 Likes

Valuations depend on narratives. The current narrative is that of sequent being an FMCG. AS AN FMCG company this is fairly valued. Another thing is size. Zoetis is an innovator, however due to it being largest company it grows slowly. Sequent has a lot of growth triggers lined up. Entry into US. Entry into China. it is not even in top 10 global companies yet. Margins would also improve as they launch the companion animal therapies. As long as growth and Margin triggers are lined up, as long as sequent keeps growing valuations would be stretched. As long as indian equity is in a bull market valuations would remain stretched.

As an analyst we worry far too much about the valuations and far too less about the business. If we get the business direction right, there is some leeway in terms of valuations. Having said that there is imo no margin of safety in buying sequent at this juncture. A lot of growth triggers might be priced in partially (anyone’s guess to what extent they are priced in).

16 Likes

I agree that valuations depend on narratives, but I doubt this could be re-rated to a higher P/E than what it is currently trading at (only see a downward re-rating), especially considering that pharma/chemicals stocks are currently enjoying a great run. In this particular case, there is possibly some premium attached to PE ownership owing to their expertise in the field.

I totally agree that it is a great business with a very bright future. However, having entered the stock pretty late (at ~180), my margin of safety is not great and I have to be cognizant of the valuations. Ultimately, even though I like the business, I don’t think the risk/reward setup is great for me.

5 Likes

the rerating is always like a very sudden thing. If the business has momentum 3 years from now and the pe reduces to 30x that would be a buying opportunity. We have to let our long term investments compound. We cannot sell out for every 100% rise in valuations. Anyone’s guess whether it can go from 60 pe to 100pe or 30 pe. As the margins improve, the pe would reduce automatically making valuations better. If valuations still sustain this means market has visibility for more growth. This is why it’s important to track the concalls. If there are industry and company level tailwinds then valuations would sustain. We get soft signals of tailwinds Turning to headwinds in concalls and then it is up to us to act on those signals and sell out if business momentum is reducing or reversing.

9 Likes

My take on the valuation is, since SeQuent is now held by a PE now & most likely will be sold off to another promoter completely (like in Eggplant) or partially (like in SBI cards) in few years when they have made many more multiple times on their investments (currently they are at ~3X). If this gets sold to a MNC the high valuation will very likely sustain.

I doubt that we will able to see extreme downward re-rating anytime soon as they run a very tight ship (see SBI card’s last years’ performance even in face of COVID meltdown, Earnings have halved and GNPAs have doubled till last Qrtr, yet to see 500 Levels again) and any deep corrections in future would be happily bought into as fast, assuming the business keeps preforming as planned, enjoying the tailwind of the animal Pharma sector which could be a multi-year story in itself.

I am quite certain that it can stay over-valued for a long time or correct briefly to a fairer valuation in line with MNC FMCG/pharma valuation (read 40-50 PE band). From the current level where everthing already seems prices in, the growth in value would be in line with how fast the business keeps growing which could be decent given all the positive triggers they have.

I had held Sequent since 70 levels and cashed out 75% of my holdings around 240 levels due to the 3X run up in 10 months last FY and since then waiting for a deep correction. I do not have enough conviction to average up at 3X and I wait to be proved wronged in my above theory by the market so that I can again go back to a significant holding % of my PF in SeQuent.

12 Likes

It makes more sense to look at any future downward re-ratings as buying opportunities until the strong business momentum and industry tailwinds sustain. Thanks for the perspectives @sahil_vi @Rishu1202

3 Likes

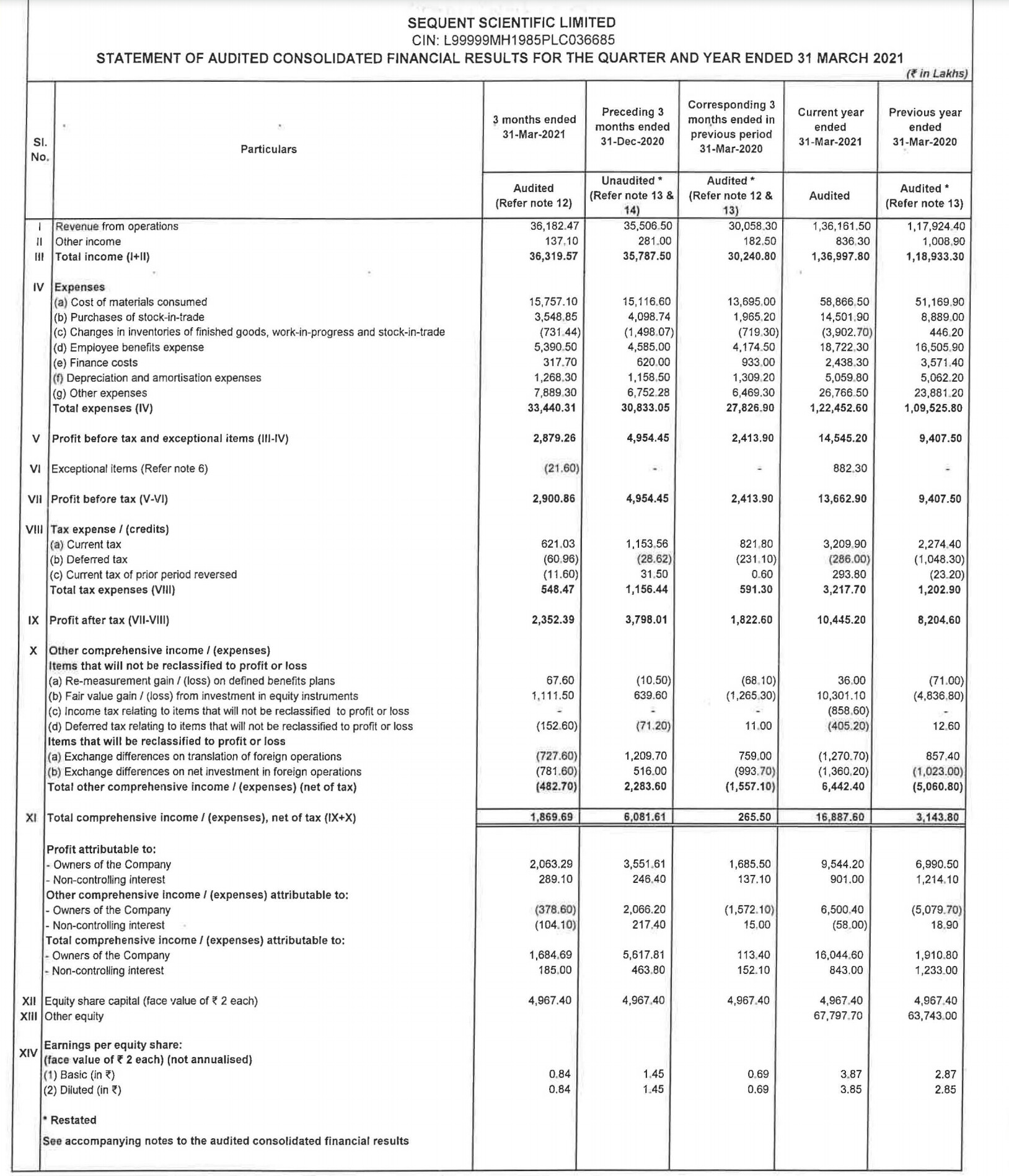

Results

https://www.bseindia.com/corporates/anndet_new.aspx?newsid=bd76c182-48e4-416a-89ad-ef6529a782c0

Q4FY21 concall notes

- Sequent 2.0: Stronger framework for growth

- Commercialized 3 APIs. Made 4 VMF filings in US.

- 1st formulation filing in Australia, US, Canada

- R&D team working on 35 molecules for formulations and 8 for API.

- Multi year multi product agreement with large global pharma player, marking beginning of CDMO journey. Innovator would do co-investment in Vizag. Would contribute to topline growth from FY23.

- Operationalized multi year contract with zoetis in India.

- Some mistaken Accelerated Revenue recognition was reversed. Small financial impact.

- We have an identified path to take for Sequent 2.0. Bolder steps to expand market presence in US, EU, injectables as core R&D. Into Pet market in India, Brazil, Turket. Complex generics. WIll scale up with 200cr investment in our global manufacturing facilities.

- Medium term mid-teen revenue growth. Investments for higher growth and governance taking place.

- Margin expectation for next 5 years is staying intact or maybe even expand. But in the next 2 years we will chase capability build up and not margins. Upskill and investment in management and employees.

- Pet business is a meaningful opportunity. Growth will be a combination of organic and inorganic.

- API growth was a bit low. What are our plans. Growth was ok in 1st 3 Q. Slowdown in Q4. Albentezole is a WHO procurement product. WHO is diverting their investment into other areas rightfully. Midteen API side of business.

- Among all one off costs: ESOP cost is going to be recurring.

- We have brought the concept of advisory board. Some of the costs will continue but wont be as lumpy as this year.

- Part of India biz performance is coming from Zoetis tie up some from organic business.

- Transforming from Branded generic to specialty branded generic player. We are now moving to a direction of creating demand, requires very different mindset.

- Steep devaluation of Lira in Turkey: We readjust price list every 2 months, so there is no sustainable impact of lira depreciation. Impacts smaller players and gives opportunity to larger players like US.

- Advisory board: Technical guidance about the future of this industry. Transitioning from branded genetic to specialty branded generic model. Same R&D team cant deliver the new vision. So need to upscale and upskill the employees for matching with the new vision.

- Pet biz was already existing in europe. Sequent’s big distinction is its position in India, Brazil, Turkey market which is why are targeting these. Will also target US markets but commercial plans are not firmed up yet.

- Innovator deal: 2 products on CDMO side and 6 on the commercial side. Will impact API topline materially.

- We are relying on carlyle network and expertise for entering china market. Looking for geopolitical situation to settle before firming up plans.

My thoughts: Sequent 2.0 strategy is to shift from branded generics to specialty branded generics with focus on injectables, focussing on newer markets, newer capabilities, guided by experienced market veterans in the new advisory board. All of this should lead to more sustainable and higher growth and eventually higher margins as well. For the next 2 years, margins would not expand. Co is planning to do 200cr capex in next 2 years, which is a 25% expansion on the gross block of 800cr odd they currently have. In the 5 year time horizon I think this strategy shift could lead to much higher value addition, higher margins (they talk about bridging the margin gap with innovators), as well as higher topline growth. Near sighted market participants are presenting good opportunity for longer time horizon investor which I am to increase allocation.

Disc: Invested, biased. Only describing my own thought process here. Do your own analysis/research or consult financial advisor before any buy or sell decisions.

42 Likes

Outcome of Board Meeting held on June 30, 2021 along with Audited Standalone & Consolidated

Financial Results and Press Release for the quarter and year ended March 31, 2021

The Board recommended a final dividend of Rs. 0.50 (25%) per equity share for the financial year

ended March 31, 2021.

2 Likes

Amazing summary Sahil and thanks for consolidating all the points so neatly.

Can you please let me know where I could find the concall? I could not find it anywhere.

Please delete the comment if it appears to be appropriate.

TIA…

A very strong and bold commentary, future looks bright IMHO

More focus on fine tuning the processes (opening comments is an evidence where they have formed an Audit committee to identify processes and transactions related to revenue recognition )

Animal pharma in itself is an high entry barrier and they are raising bar by entering into injectable (which in itself is very complex in nature )

Partners joining in the CDMO project is a good sign.

Experts in the animal pharma on the board, the movie is playing out nicely

6 Likes

I am following Sequent and I am invested in NGL finechem.

There is no doubt that Sequent has all elements that can set it up on a good path in coming years. However, my opinion is that the valuations are lofty. At a market cap of 7000cr, it generates 150cr cash flow. It trades at trailing 5.4 times sales, 70PE while RoE ROCE are in 15-20% range.

Personally, maybe I am making a mistake by judging a great company too early based on valuations. Would like to hear from investors here about the valuation matrix that you follow in such cases. I had a similar opinion of Syngene, which I bought in IPO and sold at lower level.

9 Likes

The valuations are certainly high but we cannot really judge valuations in isolation alone. I bought Sequent early on last year and my average entry price is below Rs 160. I haven’t added to the position since. Will I add to it today? No. Do I think the business is on right track? Yes.

Valuations seem high but may get even higher. Here is a personal example. I bought Happiest Minds when it IPO’d and my avg. was around 350. For months after IPO, insiders kept on selling and I ultimately sold my position in Happiest Mind to invest somewhere else. My reasoning was a) it was already trading at around 40 PE and b) insiders selling and employees booking profit surely must know better than me as investor. I thought the max Happiest Mind could go further was maybe a 30-50%. Today the stocks is past 100 PE and trades north of Rs 1200.

My learning has been to buy good businesses with margin of safety and let them sit and rest. Selling causes unnecessary churn in portfolio and we never can judge completely how high valuations can go for any company.

I haven’t touched my position in Sequent at all, nor I think I will. I do get tempted but resisting that temptation and mastering human emotions is the part of investing, I guess.

13 Likes

I have added my views earlier and you liked the post, thanks for that. To add to previous post: Sequent is going to the next orbit. Market pays up for the terminal value. NGL operates in unregulated markets where competition is much higher, compliance costs much lower. Is there any surprise that NGL margins are higher? As an example did you know that Sequent is the Only API or formulation manufacturer (i forgot which) to have a USFDA approved plant in all of India and China. Concentrated profit pools protected by durable competitive advantages result in high valuations. And the concentration is only getting larger here, they are going into the next orbit by getting into "specialty branded generics with a focus on injectables. Each bold word there is a source of durable competitive advantage. These are bound to reflect in valuations. Why does Divi’s trade at the valuation it does? Same reason.

Sequent ROCE will only improve from here. Would not be surprised if it is 30% 5 years from now. They have gone through the pain period that unregulated market players like NGL need to go through if they are to command similar valuations.

PS: I bought sequent at much lower valuations and so have a high margin of safety. This is not buy or sell reco. I am invested and biased.

10 Likes

Just to add Zaidus animal health sold for 6x of sales , bought by consortium of investors that has RJ as well

1 Like