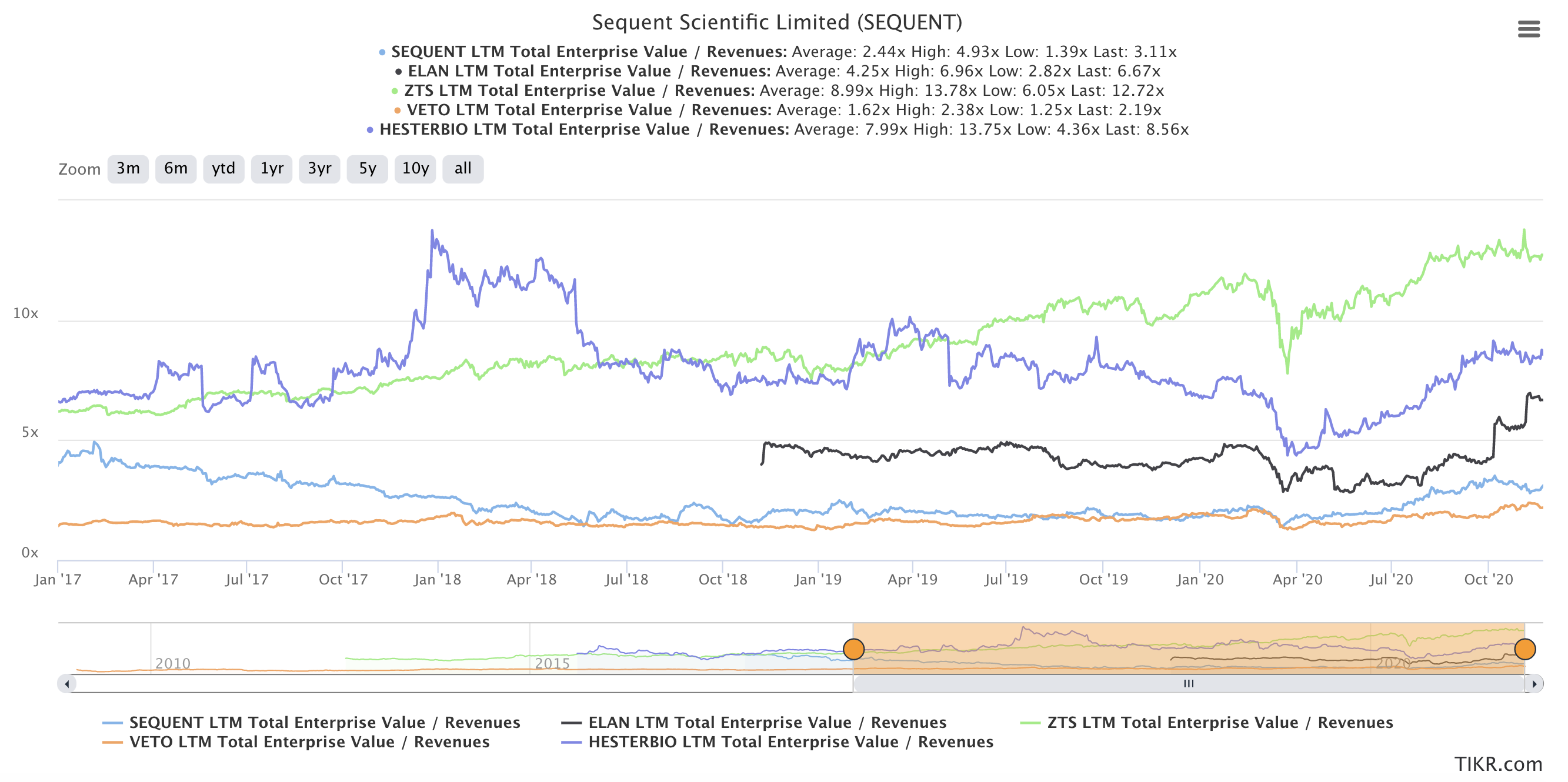

At an optical level, one might think that Sequent’s valuations are high. It is available at 42 times TTM earnings, with very few one offs. It is also the largest listed animal health company in India. Hence, I compare it to 4 other animal health companies on various metrics:

Zoetis and Elanco , top 2 animal health companies.

Hester Biosciences, very small listed indian Animal health (vaccine) company.

Vetoquinol, a top 10 animal pharma company from France.

Here are the valuations (EV/Sales) over the last 3 years or so (since 2017). I use EV/Sales because earnings can have multiple moving parts like one-offs, tax related matters as well as moving margins.

Valuations for such companies are typically driven by growth & profitability, among other factors (such as market narratives). Here is the fundamentals + Valuations data for all the companies:

Attribute/Company

Hester Biosciences

SeQuent

Elanco

Zoetis

Vetoquinol SA

Revenue (M $)

FY20

25

156

3071

6260

396

FY17

19

105

2889

5307

352

Revenue CAGR (%)

CAGR (%)

9.57

14.1

2.05

5.65

4

R&D Spends in FY20

Absolute (M $)

0.32

0

280

462

30

% of Sales

0.01

0

0.091

0.073

0.075

Gross Margin (%)

FY20

90

47

52

70

52

FY17

75

46

50

67

53

Net Margin (%)

FY20

15

6

2

24

7

FY17

19

-2

-11

16

10

Valuation (EV/Sales)

Avg b/w 2017 & now

7.99

2.44

4.25

8.99

1.62

Now

8.56

3.11

6.67

12.72

2.19

A few observations and notes:

I have used R&D spends as % of sales as a proxy of the innovative nature of the company.

Zoetis is an innovator company & has extremely high and improving margins. Hence, even with medium growth (this is bound to happen given that it is industry leader), it has extremely high valuations, both historically and right now.

Net Margins have actually shrunk for a few cos and they have suffered for it, valuations wise. Example here is Vetoquinol.

Hester being extremely small size (compared to opportunity size), having extremely high gross margins is also valued quite highly. It’s net profit margins are falling though. it remains to be seen whether it can maintain these high valuations with falling net profit margins. The scalability of the business is key monitorable for any investors here.

Coming to the main observation: Sequent. Sequent has been improving Net profit margins consistently for last many years (including a Net profit margin of 7.2% Ex one-offs in Q2-FY21). It has also maintained a healthy growth rate for revenues. Since Sequent is not an innovator company, it cannot expect to be priced similar to Zoetis. However, as per management guidance in last many concalls and also AR, the EBITDA margins should improve due to increased scale of operations (For API) and also due to improving quality of business (including new launches in US, Turkey and EU, higher sales realizations per sales person). If the management can execute on the 1.5%-2% margin improvement for next few years, then the Net Profit margin would go up even more due to the retiring of debt. IMO Sequent is fairly valued to slightly under-valued and could be re-rated if management can deliver on future margin improvements + growth as guided.

Key Risks/monitorables:

Management has guided for improving quality of business. This should ideally lead to improving gross margins. This has to be monitored and possible lack of improvement has to be understood.

Sequent now has Carlyle as promoters. PE firms typically want to own a business for 3-5 years and then exit. For a longer investment horizon, incoming promoter quality and priorities would remain a key monitorable.

Management is considering multiple new optionalities such as: Companion animal health, China entry, Acquisitions, US entry (this will happen for sure). Peanut-buttering can lead to lack of desired outcomes due to splitting of management focus. One has to monitor whether management is able to focus and prioritize among various optionalities.

In the past, appreciation of Indian currency has led to lower growth and profitability vis-a-vis constant currency basis comparisons. This remains a key risk/monitorable for a globally diverse revenue stream.

Note: Source for all the data: tikr.

Disc: Invested and might increase position in weeks to come.

Each and every company above is unique. Industry comparisons are only for getting a range of valuations. All such comparisons are apples to oranges.

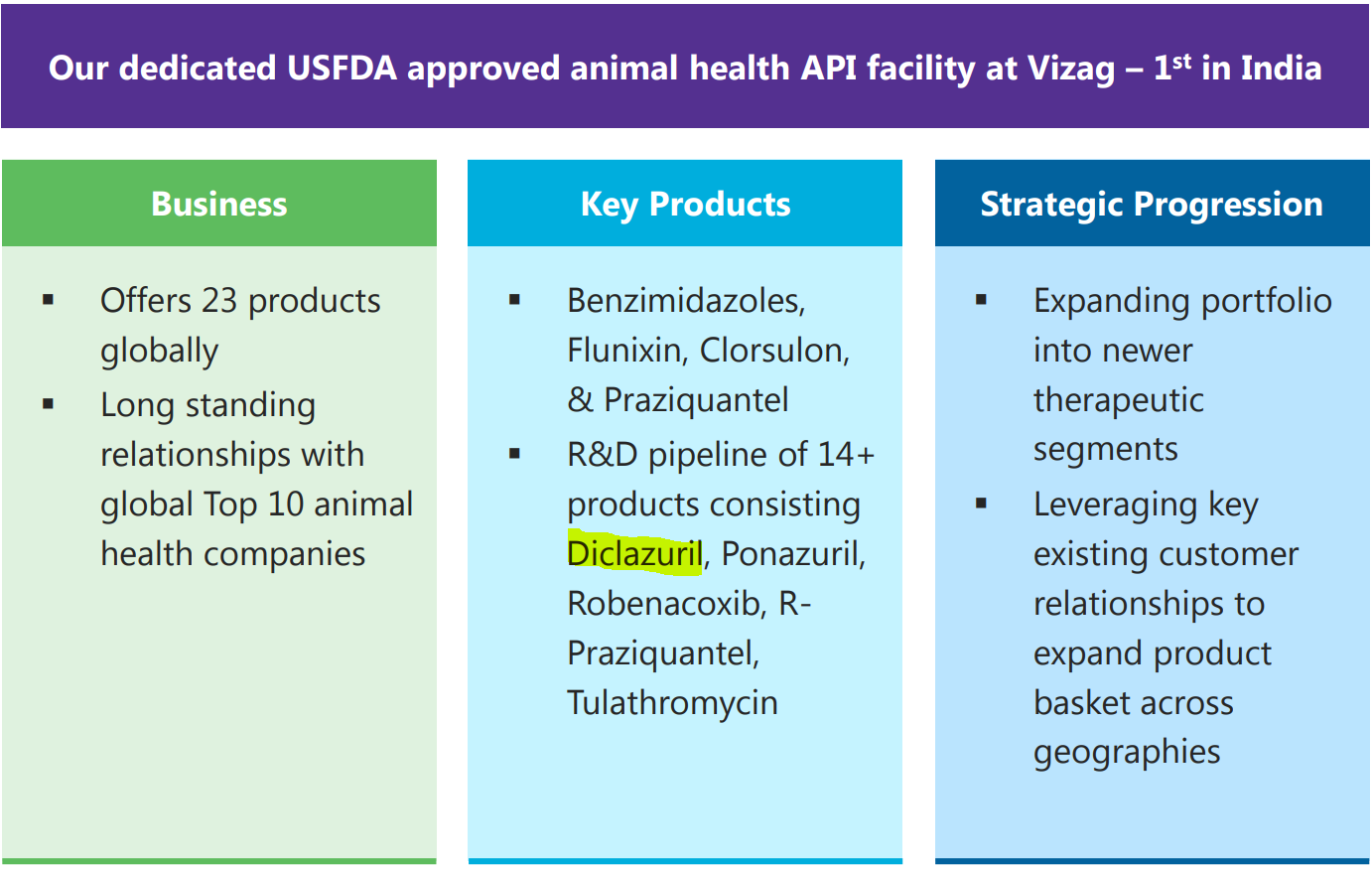

Although sequent is not into vaccines yet, this is something they are actively considering getting into. This is part of their sequent 2.0 planning wherein they are reimagining what sequent can look like 5 years down the line.

SeQuent announced launch of inhouse developed Halofusol® in EU

SeQuent Scientific Limited (SeQuent), announced launch of Halofusol ® 0.5 mg/ml Oral Solution for Calves in 19 European countries. The product had

recently received approval from the European Medicines Agency (EMA) through its Spanish subsidiary Laboratorios Karizoo, S.A.

The product was developed at SeQuent’s R&D centre at Barcelona, Spain & will be manufactured in Spain. The approval follows the recent approval of

Tulathromycin, both of which were approved within 12 months of filing, reflecting of SeQuent’s growing strength in product development for the

regulated markets.

Halofusol® offers superior value for farmers with user-friendly and cost-effective drug delivery system.

Halofusol is an oral antiprotozoal solution for the prevention and reduction of diarrhoea in new-born calves, diagnosed with Cryptosporidium parvum

and is a generic version of Halocur (Innovator: Merck Animal Health) with market size of ~€10Mn in EU. SeQuent is also planning to extend the launch to

other geographies.

SeQuent Scientific Limited (SeQuent), announced launch of Citramox® LA 150 mg/ml Suspension Injection for Cattle and Pigs in 10 European countries, including the key markets of Western Europe. The product has recently received approval through its Spanish subsidiary Laboratorios Karizoo, S.A., and will be the first Long-Acting injectable to be offered by SeQuent in Europe.

This new approval for SeQuent builds on the recent approvals of Tulazzin® (Tulathromycin) and Halofusol® (Halofuginone) in Europe. All these approvals have been received within 12 months of filing, which reflects on SeQuent’s growing strengths in introducing new products for the regulated markets.

Citramox® is the first generic version of Vetrimoxin LA (Innovator: Ceva Animal Health Inc) to be approved and launched in Europe, which is an effective antibiotic indicated for the treatment of respiratory infections caused by Mannheimia haemolytica and Pasteurella multocida susceptible to amoxicillin in cattle and pigs.

Citramox® formulation has good homogeneity and high fluidity profile, which along with its user-friendly plastic vial packaging and withdrawal times offers superior value to farmers.

The market size in Europe for Amoxicillin Long-Acting products is estimated to be ~€ 20 Million.

Technocrat appointment Good move by promoter Carlyle

Dr. Kausche returned to Europe and took part in a research

program that led him to receiving the German PhD

(Dr.med.vet.) in a combination program between the

Hannover Medical and Veterinary Schools. Having completed

the Advanced Management Program in 2005, he is also an

alumnus of Harvard Business School

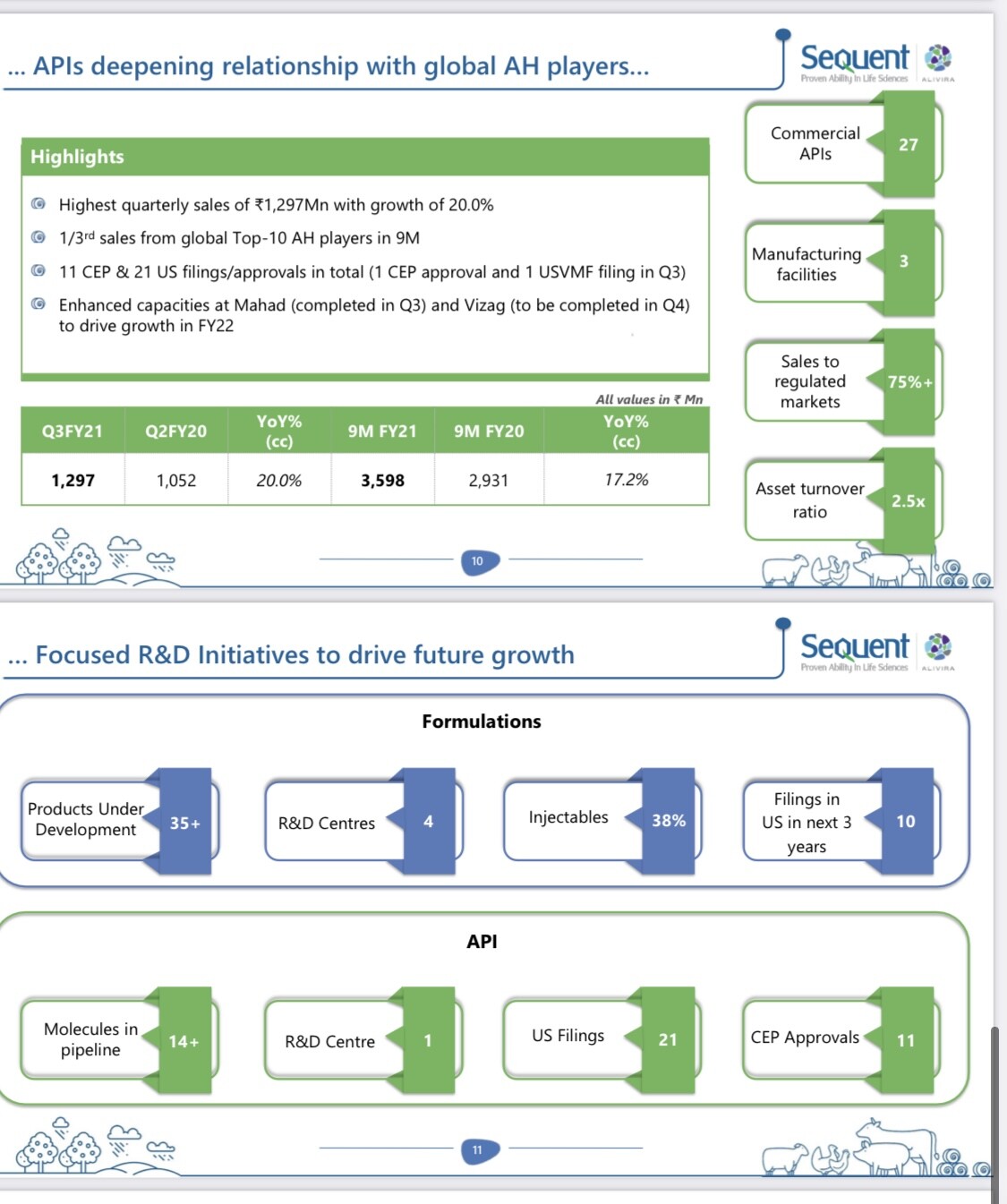

Sequent now among Top-20 players across the globe.

Prepayment of all INR denominated term loans along with integration of Zoetis protfolio in product offering now completed.

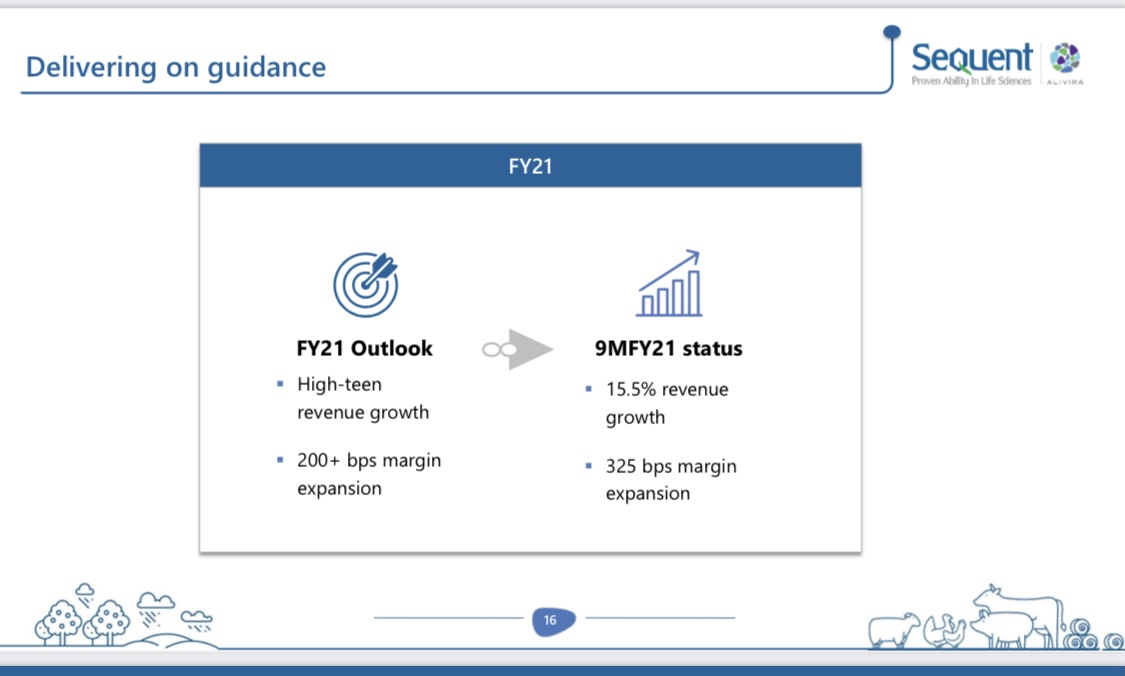

FY 21 outlook guidance of High teen growth with 14+ API molecules in pipelines and 35+ products under development. 21 US filings and 11 CEP approvals, So much to look forward to.

• Overall, revenue growth driven by API & formulations business

• India business has doubled in last 9 months

• Cash flow generation of ₹1.5Bn+ from operations drives

net debt reduction of ₹975Mn in 9M

• Debottlenecking in Mahad plant completed; Vizag plant – by Q4

• API

o will continue to grow at 20% - faster than formulations

o No big products in animal health unlike human pharma. Multiple small products – which is the company’s forte

o US commercialization 15 months away (no inspections happening currently)

• India Business

o On 9M basis, business has almost doubled yoy

o Partly the growth is driven by Zoetis portfolio and partly by market picking up. Zoetis tie up is only in India

• LATAM business

o Has picked up in current year - partly due to licence they bought (Anything in brazil takes 5 years to register) - but have adopted strategy of buying licences to reduce time for commercialization) + partly due to market also picking up

• Europe – one of the most competitive regions. Some impact due to Covid 2nd wave. Should return to 6-7% growth in coming quarters.

• Emerging market business

o Worst is behind us. Hopeful of picking up .

o Strategy: Operating on Secured payment business. Not undertaking business with open credit.

• Turkey business

o A difficult market where we have done well.

o Turkish currency has stabilized and strengthening against dollar. Shouldn’t see any impact of currency depreciation going forward.

• Margin improvement

o API , Turkey & Brazil – 3 businesses which contributed to margin improvement.

o With integration of Zoetis portfolio, there is enough headroom for further expansion

o 150 to 200 bps improvement guidance. Will moderate a little starting from FY 22 onwards maybe.

o Targeting early 20s margin range in near to medium term .

• Bird flu impact - Business model - not singularly dependent on any particular animal or particular market. Won’t make any significant impact

Takeouts : A mgmt which knows the dynamics of each market very well. Using Carlyle group expertise in difficult mkts like Europe, China and Zoetis arrangement (in India) should drive the next leg of growth.