This is a somewhat abstract topic - difficult to get to grips with. I have been struggling to come to terms with this from mid 2015 or so. My thinking is still work-in-progress, but as usual I am excited enough to make bold to take this discussion forward at VP. The attempt is to evolve a framework based thinking on separating Skill from Luck - getting better at investing decision-making - with copious help from all the bright minds at VP. Inviting fresh views from folks interested.

A. Luck and Skill Continuum

This has been sort of an eternal question for me - ever since I understood (somewhere around late 2013) that we at VP had been extremely lucky. Extremely lucky to start in 2009 with typical beginners luck of a bear market. Extremely lucky to have attracted very talented hardworking folks like Ayush Mittal, Hitesh Patel, Abhishek Basumallick (and many more) to closely work with. Even more luckier that we attracted Mentors like Mr D and Mr M (anyone who has followed our Capital Allocation thread should be aware of them) to guide and prod us in our journey/learning curve.

Meanwhile most of our businesses we picked (VP Public portfolio) continued to perform exceptionally well, and Mr Market continued to reward. I started wondering about luck and skill in our choices, but couldn’t make much headway. The purists anyway attribute most outcomes to randomness (one outcome happening out of a range of possible outcomes) – an unsatisfactory response for an individual on a quest for a Luck vs Skill Framework. Quizzing my friends & seniors then, did not yield much either.

However by early 2015, I did run into the Success Equation by Michael Mauboussin – which finally provided something tangible for me to start grappling with.

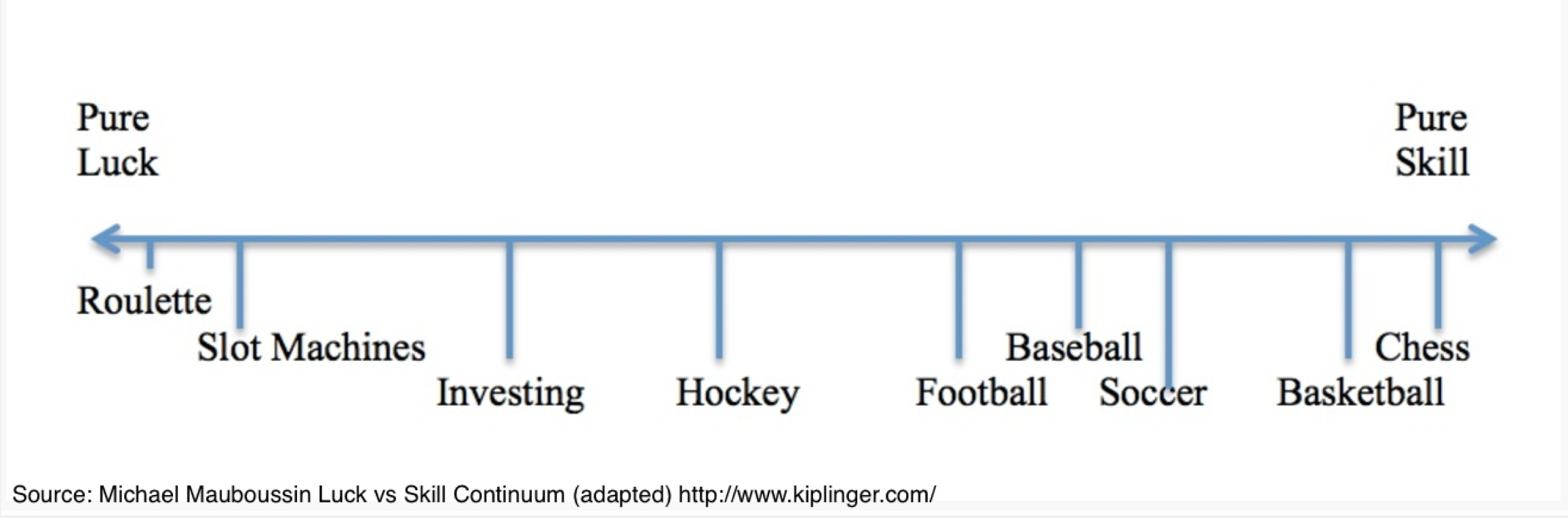

Mauboussin says “Some activities allow little luck, such as running races and playing the violin or chess. In these cases, you acquire skill through deliberate practice of physical or cognitive tasks. Other activities incorporate a large dose of luck. Examples include poker and investing. In these cases Skill is best defined as a process of making decisions.”

Re: Process

One could reckon that how much luck is involved determines the range of outcomes - where little luck is involved, a good process will almost always lead to a good outcome. Where a measure of luck is involved (like in Investing), a good process will usually have a good outcome, but (perhaps consistently) only over longer periods of time.

At the heart of making this distinction lies the issue of feedback. On the skill side, feedback is clear and accurate, because there is a close relationship between cause and effect. The fastest swimmer will almost always win the race. The outcome is determined by skill, with luck playing only a vanishingly small role. Feedback on the luck side is often misleading because cause and effect are poorly correlated in the short run.

The luck/skill continuum in investing is almost entirely a function of sample size/time. Over shorter periods, our results are highly contingent on luck and chance. We might see a bad process provide excellent results due entirely to chance and a good process provide poor results for the same reason. Sustained performance over the longer term - i.e. repeatability of successes - however, may provide clues to a good process/better skill.

Mauboussin also says "As we move from right to left on the continuum, luck exerts a larger influence. It doesn’t mean that skill doesn’t exist in those activities. It does. It only means that we need a larger number of observations to make sure that skill can overcome the influence of luck.

While the sample size of our decision-making process is undoubtedly small (over 2010-2017 and will grow over time), I still want to go ahead at this stage of our investing journey and explore a case for Expertise/Skill as distinguished from Experience.