Why do you think it is expensive?

As mentioned by Arka,

- Management said net profit in FY26 are expected to reach ₹300 crore.

That translates to EPS of ~18 with exit PE of 25, it comes around Rs:460.

Why do you think it is expensive?

As mentioned by Arka,

That translates to EPS of ~18 with exit PE of 25, it comes around Rs:460.

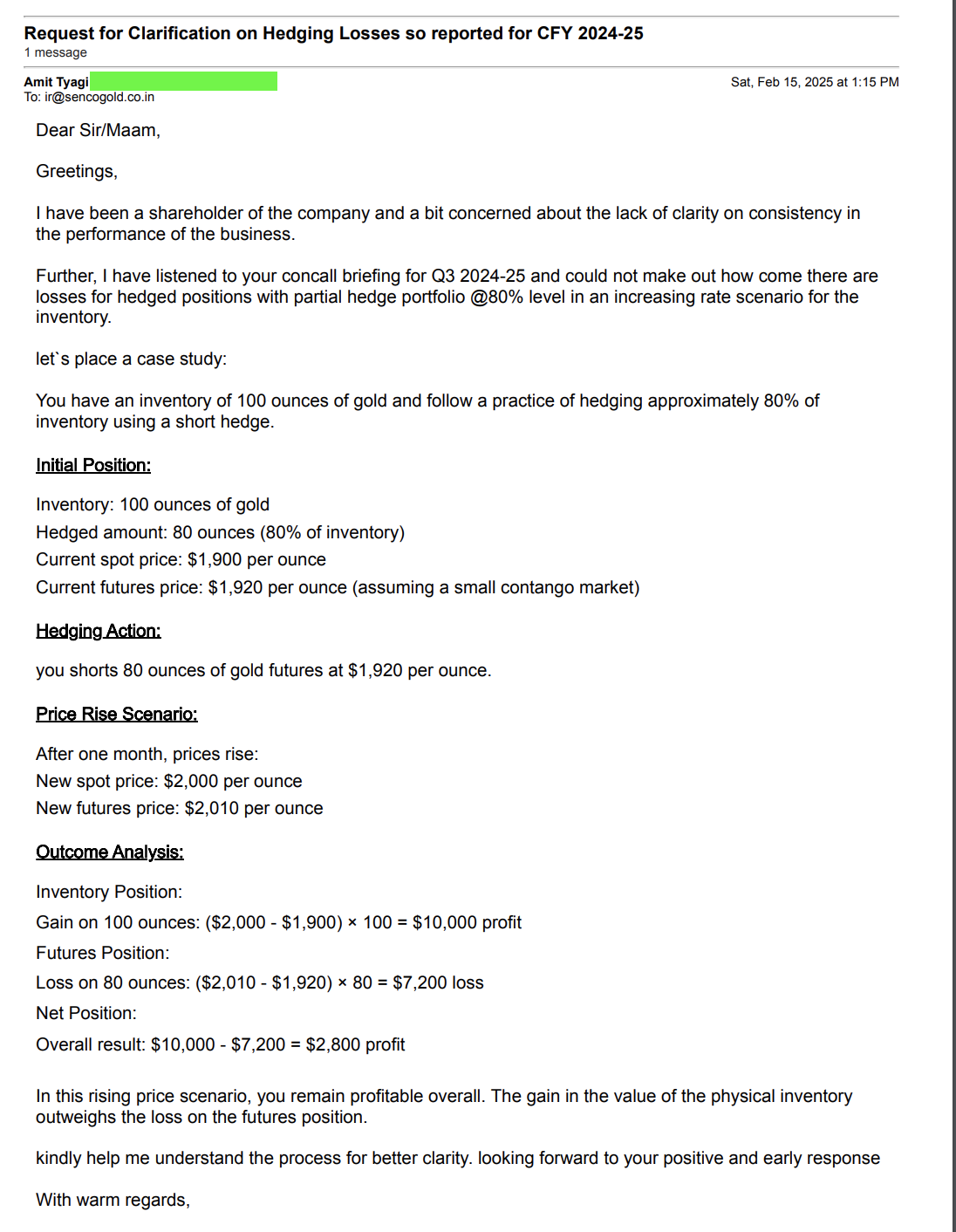

Yes, thank you. I went through it. I don’t see any problem holding Senco, remove hedging, inventory and custom duties. I don’t see any problem when it comes to consumer facing business, or any business economics. Suggest something if I didn’t over see anything?

Just checking if anybody here had a chance to hear Senco Gold call or analyze its results.

I could not understand the management explanation that hedging led to lower margins.

My understanding is that gold price increase would lead to expansion of margins on inventory which would be offset by losses on the hedge. This should lead to gross margins staying in a narrower range (like it happens for Gravita).

Could not understand as to how Q3 margins were so bad when most of the hedging loss happened in Q1. In Q3 the only one off is 27 cr of loss due to custom duty. On a 2000 cr topline that is an impact of 1.35% on gross margins

Another reason given was lower studded mix. Studded mix has gone down from 11% to 10.5%. Gross margin this quarter is lower by ~3% from normal gross margins. 1.35% from customs duty. So balance 1.65% gross margin. How can a 0.5% change in product mix impact gross margins by 1.65%. The math just doesn’t work out.

Please if someone can help me understand this

Exactly the same thing I have pointed out to the management investor relation desk…lets see what clarification they have to offer

Please do post here if you hear back from them.

In the concall they had also mentioned that they will update presentation on exchange website with a new slide (slide number 45A) to explain these losses better. But seems they haven’t done that yet

Sure, I will update if anything received from the company end… but It is not convincing to have hedging as a reason for losses if they hedge 80% of inventory in case of increasing price scenario

236f9408-0151-4560-9b3b-84574e68aab3.pdf (328.6 KB)

Clarification by Senco Gold on the queries on Hedging. Please share your thoughts.

Thanks @moons. This is helpful

Just wanted to understand Line 2.41 a little better and in conjunction with lines 2.42 and 2.43. If they had a hedging loss on their GML (2.43) and on the MCX positions (2.42), there should have been a corresponding gain in their sales realization (2.41).

This gain in line 2.41 was there in Q1FY25 but somehow not there in Q2 and Q3 of FY25. Is it due to some timing difference or due to the way it is booked in accounts, I am not able to comprehend.

If you look at FY 24-Q1 & Q2 there is losses in all the heads… Difficult to understand why losses in all the place despite of hedging…May be a timing difference of accounting, if any… if someone can clarify in a better way

https://www.bseindia.com/xml-data/corpfiling/AttachLive/faf984d6-273e-4ed6-b8a0-2cd3bfea2423.pdf

Senco Gold FAQ on Hedging

Why is the stock falling so much?

If we compare peer to peer, Senco is the worse hit in Jewellery sector. The stock was a high flying one few months back. Why it is underperforming compared to peers. PNGadgil , Thangamayil etc have all delivered good numbers. Why Senco is worse hit? Profitability has taken a big knock. It is worse hit in inventory loss. Why not others. Khemka participated in QIP. Adjusting for split, it is down more than 60% from QIP price. How these big investors gone so wrong?

It happens sometimes,one needs to remember story would not change in 1 quarter let that sink in it is a decadal theme where whole sector is going from unorganised to organised.

Suvankar Sen, MD of Senco Gold & Diamonds, said the increase in gold leasing rates was a cause for concern for firms quoted in the report

Senco Gold Mgt Clarifications through Concall and Investor presentations

Senco Gold Mgt clarification can been seen with two angles but reason for continuous explanation is they are worried about crashing stock price which should not be the focus of any business but still**

Either, they are giving too much explanation to justify themselves as clean management and hiding something in accounting or word game

Or

They are facing first hand market experience how market can punish if they don’t execute well and giving detailed explanation in writing to bring transparency in their accounting.

Core point layman can understand by their explanation

Whatever has happened and what ever explanation company gives, In Q3 they mis-managed hedging position and sudden gold price rise resulted into Rs.46 Cr hit to PAT. It could be considered as one off due to such swing in gold price is rare case but shown inherent risk in this business if gold price fluctuates or mainly shoot upward which company continuously denied in past that they don’t get affected much due to their hedging position, company will take a hit on profitability.

Another way to look at it is as per mgt clarification, mgt has shown in addendum is that if one look at last three quarter all together then effect is nullified by realization gain and hedging losses. Also in past concalls mgt has boasted that custom duty impact of Rs.60 Cr will largely be covered due to rise in demand but they failed.

Another Key headwinds for industry is due to Trump Tariffs, Gold Metal Loan interest rate may double from currently 3.1% to 6% which put pressure on margins on all industry players who are hedging through GML. Senco source almost 47% of its gold through GML and its 64% of total borrowing on Senco books. As per Mgt this will have impact Q4 profits by Rs.7 Cr to Rs.8 Cr.

As we are not into Jewellery business but have only option is to trust management as a minority shareholder. Their explanations create two camps those who believe them and those who doubts on number as said in the beginning of these notes.

Key Fact to Watch – Mgt has guided for Expected Revenue from Q4 is Rs.1400 Cr (24% up YoY) (As they said by the date of concall they have achieved Rs.5700 Cr YTD sales and expected to close the FY at around Rs.6400Cr to 6500 Cr) so expected conservative PAT should be above Rs.50 Cr (above 30% YoY)

For FY26 Company is guiding for Rs.7500 Cr Revenue Margins of 7% to 8% and Profit of Rs.300 Cr

Above guidance may be in hurry due to investors jittery reaction to stock price

Disclaimer: I am not a SEBI Registered RA or RIA. Having financial interest in this company. Dont consider it as an buy sell recommendation. Invested and cautious positive going forward.

You get validation on underline VALUE and PROSPECT to buy and keep it. If you are just looking at price you get exposed to fluctuations.

In short, answer why you bought the share. If don’t know, then sell…

Summary:

I booked my loss today that was -52% and shifted to some other stock. I think high gold prices and increase interest on gold loan for jewelers look negative for the whole sector and this stock is not stopping its fall, i wish it find a strong support at 250. If you want to be in jewelry stock then you can also look pngjl, titan, goldiam etc.