Senco gold is largest organized retail jewellery player in the country with a market presence in more than 13 states. They have company owned company operated (coco) stores as well as franchise store model.

The company has a dominance in the eastern part of India with a volume growth rate of 32% in h1fy24 YoY.

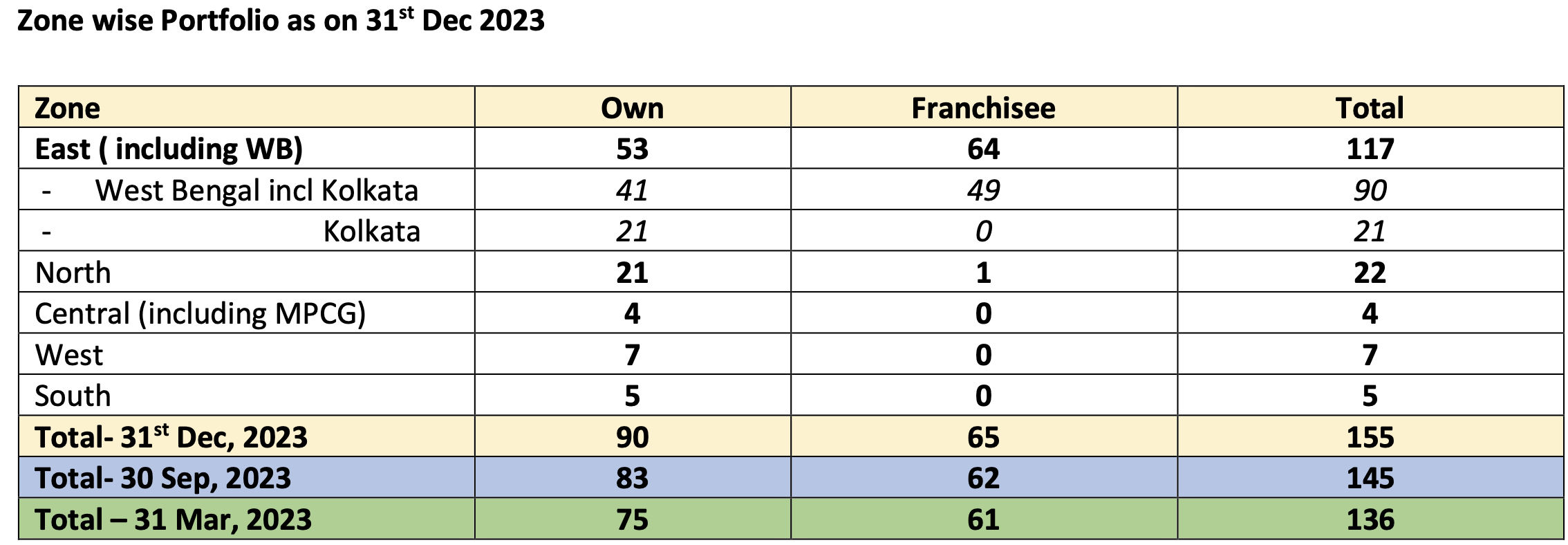

Senco has 145 stores which includes 83 coco stores and 62 franchise stores. 57%-43%) .90% of the showrooms are leased.

The number grew from 136 stores in fy23. so, a 6.6% growth in 2 quarters as far as store opening is concerned.

Out of the 62 franchise stores 49 showrooms are in tier 2 cities.

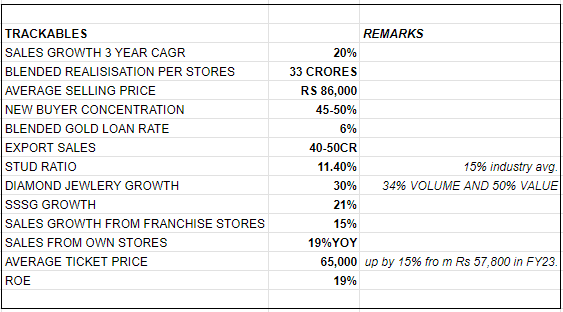

The company has allocated different showrooms for different audience.D’signia being the most premium with an average ticket price of Rs**.76,900** and house of Senco and Everlite being the most economical @ Rs. 37,000.

WORKING CAPITAL REQUIREMENTS FOR A STORE:

A store spends on two things while opening a store:

Inventory : Inventory requires approximately 10-12 cr. capex requires 1-2cr.

Capex: The company does no capex for any franchises. the franchises themselves have to pay for their inventory and their capex.

STORE’S ECONOMICS

The current stores are open in 55:45 ratio between coco and franchise stores. Franchise growth rate is 15% and the contribution stands at 35%.

The inventory turnover for a franchise store from 1st year is 2 and reaches 3 by the third year. blended franchise turnover is 2.

The company owned stores have a gross margin profile of 18% and in case of franchise stores, the gross margins are anywhere between 10-12%.

Senco keeps 6-7% of the margins with them while leaving 11-12% for the franchise stores.

that implies = 2*10cr of inventory = 20crs worth of inventory in a year with 12% gm = 2.4crs approximately, when accounting for inventory. the store pays and get the inventory. the company doesn’t show these inventory levels in their books

HEDGING:

• The company is 80% hedged and have hedged it using two instruments:

1.) Gold metal loan: accounts for 50-55% of their hedging positions:

gold metal loans are taken from the bank for their requirement of gold for their inventory. They take an unfixed loan where gold prices are directly related to the amount they pay to the bank.

•Positions on mcx: They hedge the rest of the positions with futures and options. this is a common practice in the industry.

• the crux is that they have no effect scenario as far as price escalation or de escalation is concerned.

SWOTANALYSIS

I have done a swot analysis keeping in account the various strengths, weaknesses, opportunities and threats I find in the company. This analysis covers most of the aspects of the space that the company is right now in and might be in the coming future.

STRENGTHS:

Their reputation, industry expertise and knowledge:second largest retail jeweler in the country, presence in more than 13 states. have company owned stores as well as franchise stores.

Dominance in the eastern region: *East has 110 stores, approximately 76% of total stores. with 49 own stores and 61 franchise stores.

gold price escalation and de-escalation does not have any effects: because of proper hedging mechanisms in place.

Inventory stock turnover: Churning of stock where required gives them an edge in stock turnover ratio : **higher stock turnover gives them better roe

Tech savvy: launched a metaverse which allows customers to view and try on all the designs virtually. giving them a sense of the design and look. have a website names ever lite, targeting gen z by offering modern diamond designs.**

WEAKNESSES

too much dependence on just gold. 90% of the sales are in gold products.*

stud ratio lower than of industry average. 11.8%vs 15%.*

slight seasonality in sales. h1 is lighter in sales as compared to h2*. The margins also get affected due to this.

Sectors like exports have negligible margins for them. But with decent growth potential.*

OPPORTUNITIES

Male jewelry growing at a 15% rate (gold chains and rings)

Replacement market growing because of government policies eg. HUID code : purchase from old jewelry increased to 24% of sales from 19%

Sectoral shift from unorganized sector to organized sector: currently stands at 33-38% for organized and 62%-67% for unorganized. expected to reach 42%-47% for organized and 53-58% unorganized by fy26.

their average ticket price is rs.65,000, with a revenue of 4,000 cr. number of transactions has been around 5l, this suggests: the light stud jewellery which is sold on their online portals and stores increases the diamond sales. as they grow more in this segment. margins are bound to get better.

daily wear jewellery trend. 35-40% people are buying jewellery for them for daily wear purposes.

as their share in diamond jewellery increases which is very insignificant right now profitability increases on an ebitda level and looking at their target audience, their market share is expected to go up. As far as diamond sales are concerned they have doubled their sales in diamond in the last 4 years.*

THREATS

Heists: Two stores in the same region were looted, insured but insure repayment takes time.

Regulatory developments: Any potential regulatory developments can hinder with the short term , medium term growth eg, Deomotization.

Lab made jewelry: has a major effect on diamonds, especially the large studded ones. effect has not yet been seen on the smaller sizes yet.

Potential strikes from karigars: Company is heavily dependent on karigars from east.

GUIDANCE AND OBJECTIVES:

Better reach in north. to improve on stud ratio: some stores in the north particularly delhi ncr has a stud ratio of 20%*

Guidance is to add 20-25 stores every year till FY26: blended realization per store is around 33crs.

open coco stores in metro cities for higher diamond sales and better realization.

plan of action is to use hub and spoke model and penetrated deeper into tier 2 and tier 3 cities.*Targeting north and east as primarily.

maximise inventory turns because better inventory turns, higher roe’s.

for fy24 the guidance for the topline growth is at 20%.

Some of the trackables which are important for the industry are as follows:

*This is not a buy or a sell recommendation!

I have created this thread on Senco gold to have better understanding of the company through the wise inventors and learners we have on this forum. Its imperative to keep having discussions on this company through this thread to have a better understanding of how the company performs.

So what happens is that while setting up a store whether its company owned or a franchise store. The store requires a minimum inventory as jewellery for them to offer to the customers and all the inventory is sourced from Senco. Inventory turn is basically the churn the stores do with the inventory towards the customers. The iventory turn for the first year for a franchise store on an average is 2.

That means they are able to turn the 10-12 crore inventory which they brought from senco twice. That implies that total sales from a franchise store if their inventory turn is 2 could be around 20-24 cr with 11-12% gross margins in hand. So Higher the inventory turn >> Higher sales >> More profits on the same fixed assets >> better roe.

Senco Gold is in an expansion phase and valuation very comfortable, still trading at a discount at 28 PE FY24E in comparison to Kalyan (60PE FY24E) and Titan (85PE FY24E).

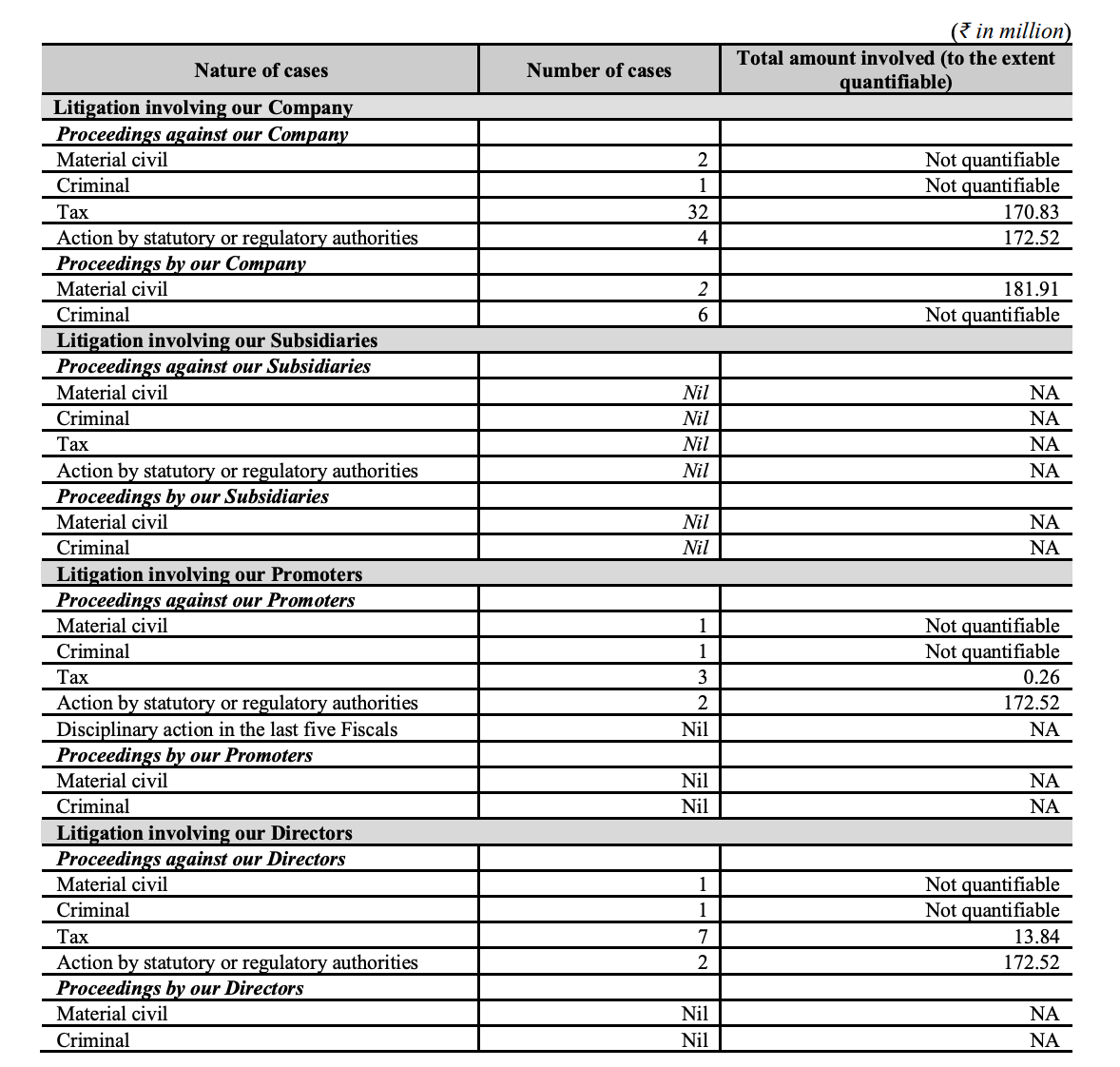

However, can someone throw some light on the pending cases against the company, as mentioned by a boarder here:

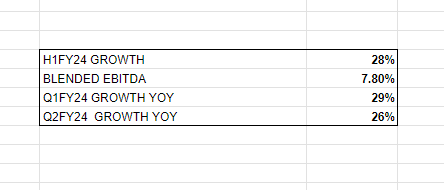

• Q3 first half has seen good growth; Dec onwards demand tapered due to higher gold prices

• 20-25% growth seen in Q3FY24

• Increase in Gold Prices is keeping the demand in check but consumers are happy to see the value of existing jewellery going up

• Growth in Diamond Jewellery – 14C, 18C products is showing good demand

• Profits improving due to premiumization

• 18-20% growth guidance held for the year; Q4 may not be as good due to seasonality

• Diamond share is at 12% of the whole revenues – targeting 15%+ in coming years

• H1 – 33% Diamond, 11.4% Gold

• 80% of the inventory remains hedged (making charges is where they earn their margins)

• Trying to balance b/w growth and margins via diamond growth and discounts / offers

• Stores: 153 stores (4-5 stores in Q3FY24 and 3 stores to be opened in Q4FY24; 18-20 stores opened in FY24) – 60-70% Company-owned, Rest is franchise owned

• SSSG at 19%

• 1-1.5% market share at a national level; much better at a regional level

• Online: Lighter jewellery doing well as customers are getting comfortable; Heavier jewellery remains more retail stores based

• Lead generation and digital led retail sales is what one needs to look at

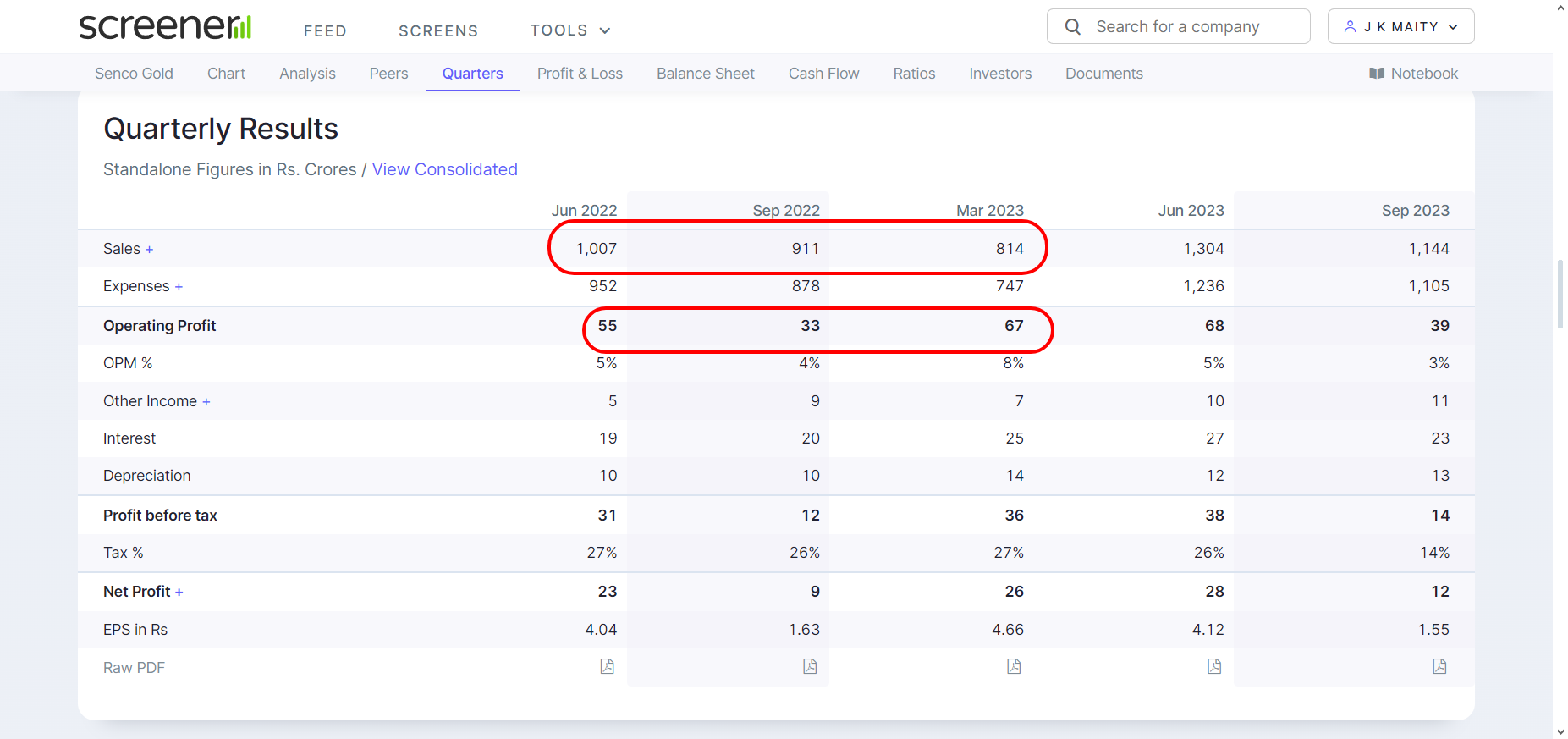

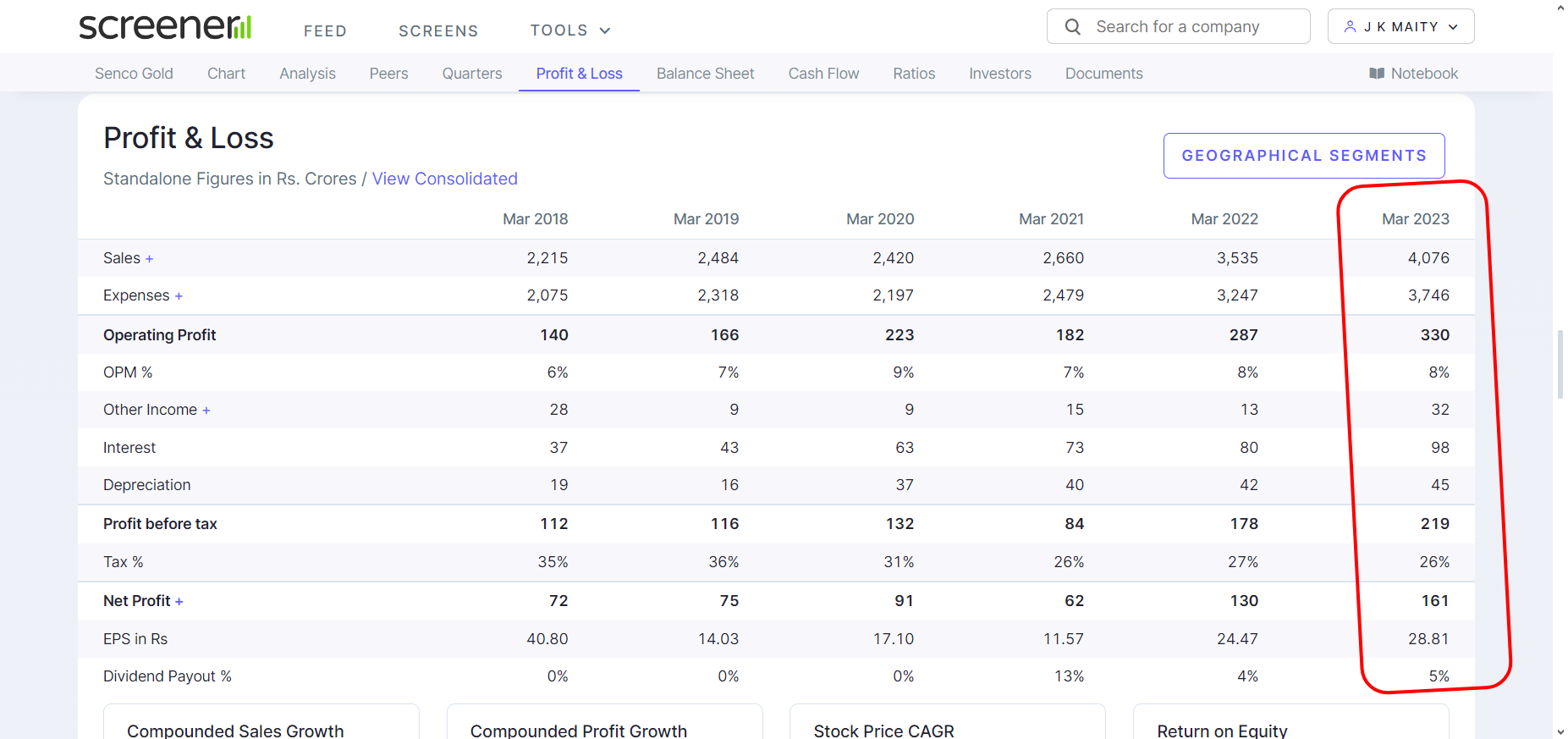

Though the company has not given Q3FY23 result, it is understood from the already available data.

Sales for Q3FY23 should be 4076 - (1007+911+814) = 1344 Cr

Operating profit should be 330 - (55+33+67) = 175 Cr

Now what I cannot understand is how they got to 13% operating margin that quarter. Though there is operating leverage, do you think it normal for the margin to reach 13% from a meagre 4 - 5% previous quarters? Or am I missing something?

When compared with Kalyan, looks like jewellers biz have legal proceedings against them. Senco’s amount seems to be comparatively less, to it’s revenue/PAT.

9% volume growth in Gold and ~ 27% volume growth in Diamond jewellery

The 9 months SSSG was 19%

Stud Ratio: We have achieved consistent improvement in stud ratio (Diamond Jewellery as percentage of total turnover) . Our own showrooms achieved stud ratio performance of 13.2% (achieving 190 basis points growth over 11.2% of last year 9m) , while the blended ( own showroom and franchisee room) stud ratio was 11.0% (as against 9.7% for 9 months last year). The stud ratio was highest in North at 17.8% .

Shift from unorganised to organised sector playing really well. Decent SSSG and improvement in stud ratio.

>>Why is the studded mix relatively low for the company (vs peers) despite a higher preference for studded jewelry in North and East and the presence of dedicated stores like Everlite that specialize in diamond and lightweight sales?

Stud ratio in east is among the least (11.8%) where they operate maximum number of stores(117) and in North, stud ratio is 19% where they operate 22 stores as per the latest update. Management guiding for reaching to 15% in next few years and in last couple of quarters they are on track.

>>And also most of the Gold investment schemes offer some discounts to customers for their monthly installments, and management mentioned they dont offer any discounts and they have completely mitigated the price risk? so whats the incentive for the customer to lets say enroll in their Swarna yojana scheme??

Not sure where you got this but a look at their website does say that they pass on the benefit.

Is it a good time to enter right now ? I am a local from Kolkata and have visited the 8000sq ft store and it is phenomenal. However, the “Karigars” are mostly from Bengal region and the type of work Senco manufactures orients around a typical bengali jewellery design. Whilst such a design is relevant for Eastern India, don’t you think there might be an inherent taste clash when expanding their market share from 1% nationwide ? Or is it a relatively fixable problem ?

Disc: Not invested, but looking to enter

I have recently visited their flagship store in Kolkata Baguati, I went there to check the customer experience and dig some --( on ground ) info from the store. Few things that I found out are listed below. I have not validated these with any sources, so these information are completely based on what i experienced and heard in that store. (So don’t invest in Senco based on only these pointers, do your own research before you invest.)

CX is very decent, at par with almost any leading Jewelry store across the country. I have visited other stores like Zaveri, Tanishq, Kalyan, in cities like Bangalore and Ahmedabad.

The team working in Senco’s flagship store, seems very happy with the work culture and sounds very motivated.

Senco is entering into Luxury accessories segments like Bags, wallets, belts, Laptop bags. These are very premium, in a range 15000 INR and above.

Also heard they have aggressive plans to enter into perfume segments as well, again luxury and premium segment only.

Very good collection in the artificial jewelry segment, they have almost a dedicated floor on the same. The ranges starts from 1000 to 15K

I have not invested in this but tracking this closely. Any further guidance or intel specific to Senco as an opportunity will be helpful.