I believe there is one off gain in the Results, they mentioned only 95% of their inventory is under Hedge. Furthermore due to recent tax change in the next two quarters, some inventory loss is possible.

345cd75d-ee54-46e7-a87a-460083362065.pdf (1.8 MB)

Hi,

I understand possible inventory loss due to change in import duty.

But Could you share why you felt there was one-off gain in results ?

As per my understanding from the investor presentation, 95% of the gold inventory was hedged. Due to the increase in gold prices, it was benefetted to the company as 5% of the gold was unhedged. This kind of benefit is one-off in this quater and may not be available in the coming quarters.

2 Likes

Senco Gold -

Q1 FY 25 concall and results highlights -

Current breakdown of number of showrooms -

Company operated - 97

Franchise showrooms - 68

Total - 165 ( spread across 109 towns and cities and 01 in Dubai )

Added a total of 06 new stores in Q1

Q1 financial outcomes -

Revenues - 1403 vs 1305 cr, 7.5 pc

EBITDA - 108 vs 67 cr, up 62 pc

PAT - 51 vs 27 cr, up 85 pc

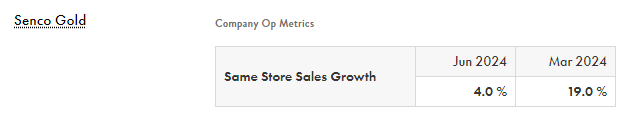

Same Store sales growth @ 4 pc

Avg Ticket value @ Rs 73.9k vs Rs 63.7k for FY 24

Q1 Stud ratio @ 9.9 pc vs 11 pc for FY 24

( diamond sales were down by 3-4 pc in Q1 - due rising gold prices )

**Sale of recycled gold stood at 35 pc of total sales ( ie customers exchanging old gold ornaments for new ones ) **

Have launched lab grown diamonds under the Sennes brand

Aim to add about 12-14 more stores in FY 25

Aim to add about 12-14 more stores in FY 25

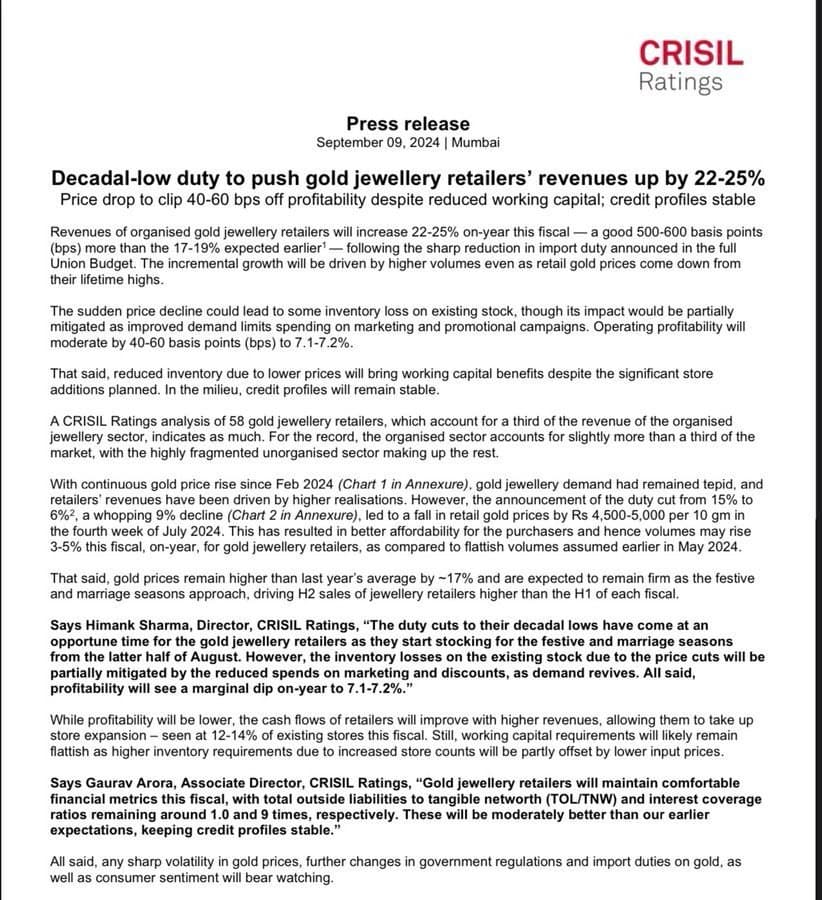

About 95 pc of company’s gold stocks are hedged. Due to the sharp duty cut on Gold imports announced by the GoI ( recently ), there will be an adverse financial impact of about 50 cr for the company for the remaining 9Ms this FY. However, the duty cuts have also stimulated the demand for gold and gold jewellery which should help the company offset this impact

Aim to grow topline by 18-20 pc for FY 25 vs FY 24

Depreciation charges in Q1 are 18 vs 12 cr ( up 50 pc YoY ) - mainly because of aggressive store opening in FY 24

Confident of touching a stud ratio of 12 pc for full FY 25

Growth in Q2 ( as on the date of Concall ) has been a whopping 25 pc ( triggered by duty cuts ). Hence the confidence to guide for a 18-20 pc topline growth for full FY ( with same store growth guidance @ 11-13 pc )

Also seeing healthy growth in Franchise stores in Tier -2,3 towns - probably an indication of improvement in rural economy and normal monsoons

Elevated levels of other expenses in Q1 are unlikely to continue wef Q2. The same were elevated as the company was spending a lot on brand promotion / marketing etc as the Mkt was showing weakness wef late May / Jun

Company is confident of making up for a large part ( if not for the full part ) of inventory losses of around 50 cr in the next 3 Qtrs - due increased sales, lesser discounting etc

To be on safer side, company is guiding for 15-18 pc bottomline growth for FY 25

Disc: holding, biased, not SEBI registered, not a buy sell/recommendation

14 Likes

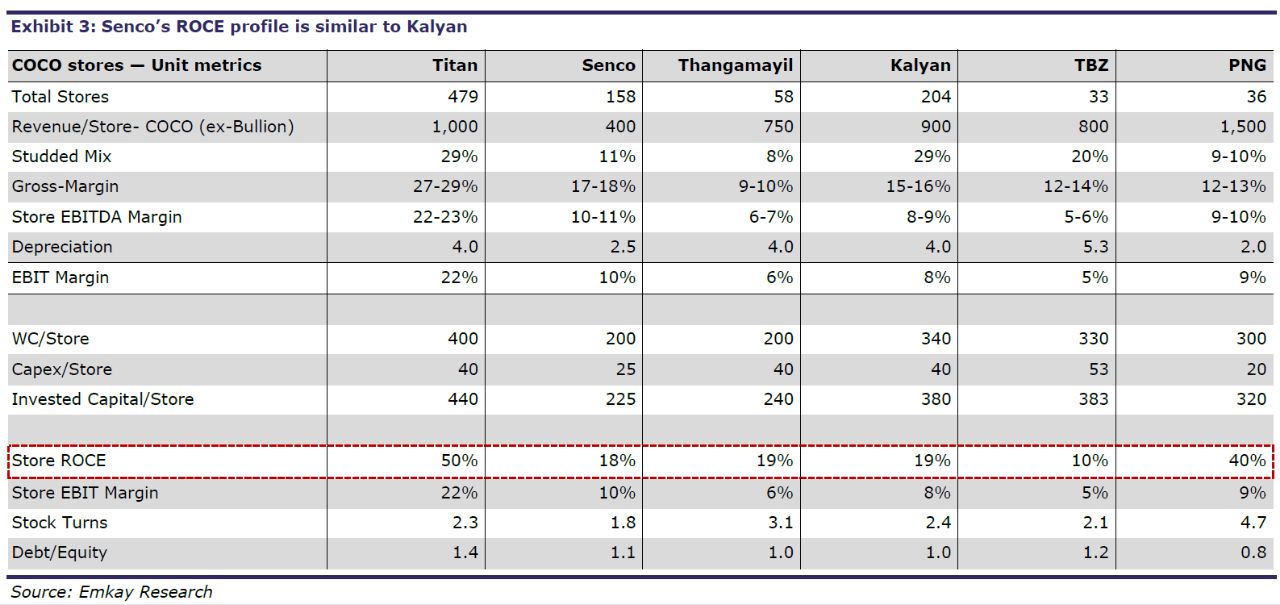

Hi guys, let me know your thoughts. Senco is a relatively small player trying to expand stores and there is also large shift taking place from unorganised to organized. Then why are they diversifiy into other business, what is the reason. If the margins are high in other business, the ticket size will be very small.

Why are they doing it. Isn’t it that they should establish themselves and then think of other stuff

4 Likes

3 Likes

Promoter Selling 16.09.2024

Market Sale of 750001 shares worth 96.32 Crs by one of the Promoters

This is 2.18% of this promoters holdings.

4 Likes

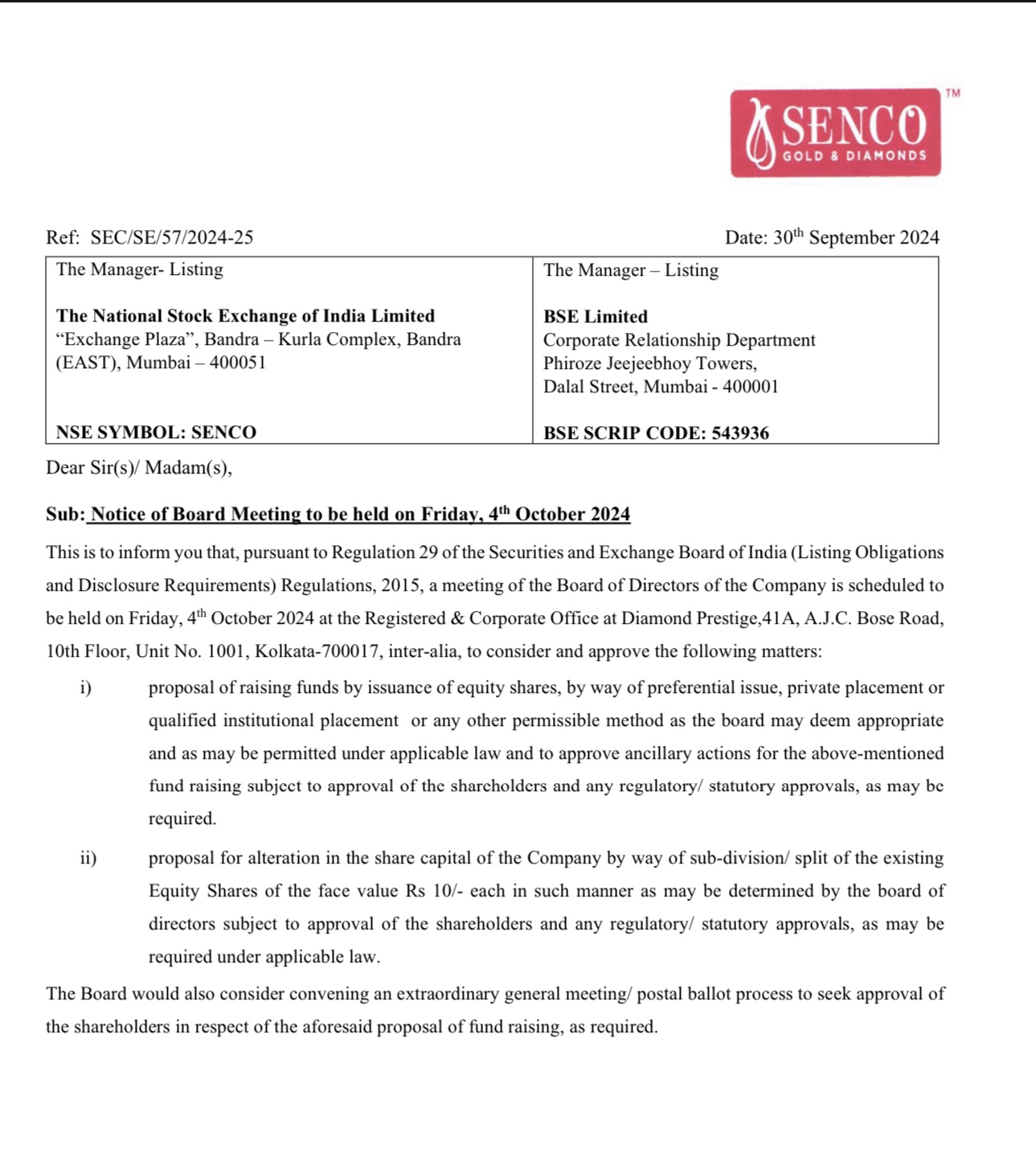

Fund raising plans through preferential issue, private placement or qualified institutional placement

Proposal for alteration in the share capital of the Company by way of sub-division/ split of the existing

Equity Shares

4 Likes

I guess I will be able to answer your question. Let’s say that gold prices have increased, now from a consumer perspective what options do they have if they wanted to purchase new jewelry? Either they can wait to have some correction in the gold prices or they can use their own old gold jewelry + some money from their pocket to buy new jewelry. This second option comes under GEP (Gold Exchange Program).

-

Now, how it predicts the shift from unorganized to organized market?

As, mentioned the old gold that company is receiving, out of that gold 65% is the gold that is crafted by other regional unorganized jewelers. Depicting a shift from unorganized to organized sector. -

Why that gold can’t be from other competitors like Titan or Kalyan?

Simple!!! because they have hallmark which is easily traceable.

I hope you would be able to understand.

5 Likes

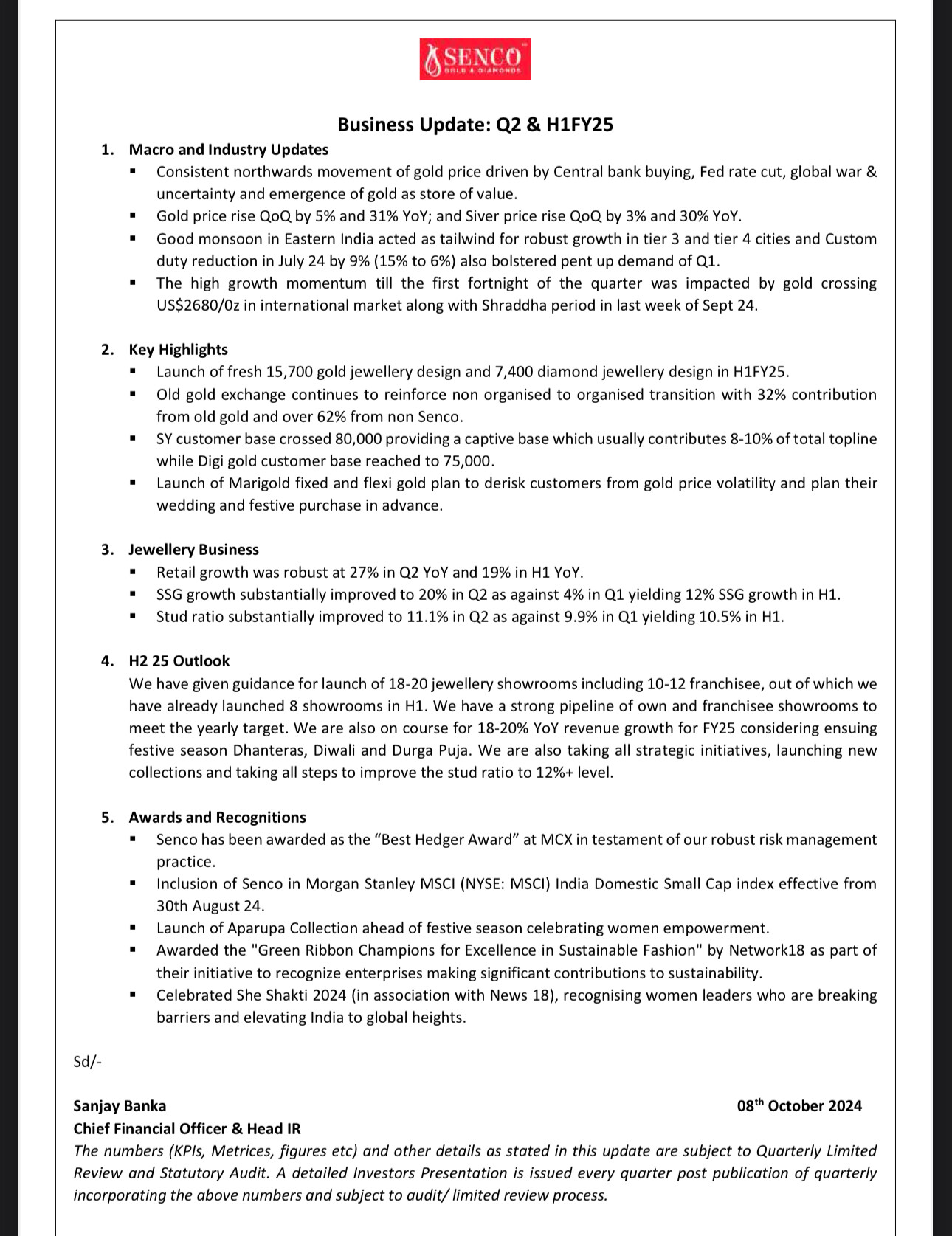

Business Update: Q2 & H1FY25

SSSG Growth 20 %

•H1 SSSG Growth 12 %

•Retail Growth 27 %

•H1 Growth 19 %

Studded ratio improved to 11.1 % against 99.9% in q1

On Track to achieve guidance

•18-20 Showrooms

•18-20 % REV growth

7 Likes

8 Likes

How do people see PE and growth of Senco against its peers?

PE has fallen from 54 to 45 as of 25th Oct and heavily impacted in recent fall than peers. Any view?

1 Like