Hello fellow members and VP. I began my investment journey in 2016 when I took my first job and then by end of 2016, I started following valuePickr. Since then my view on equity has changed and improving day by day. Thanks for all your contributions, especially @hitesh2710 ji whom I used to follow for guidance.

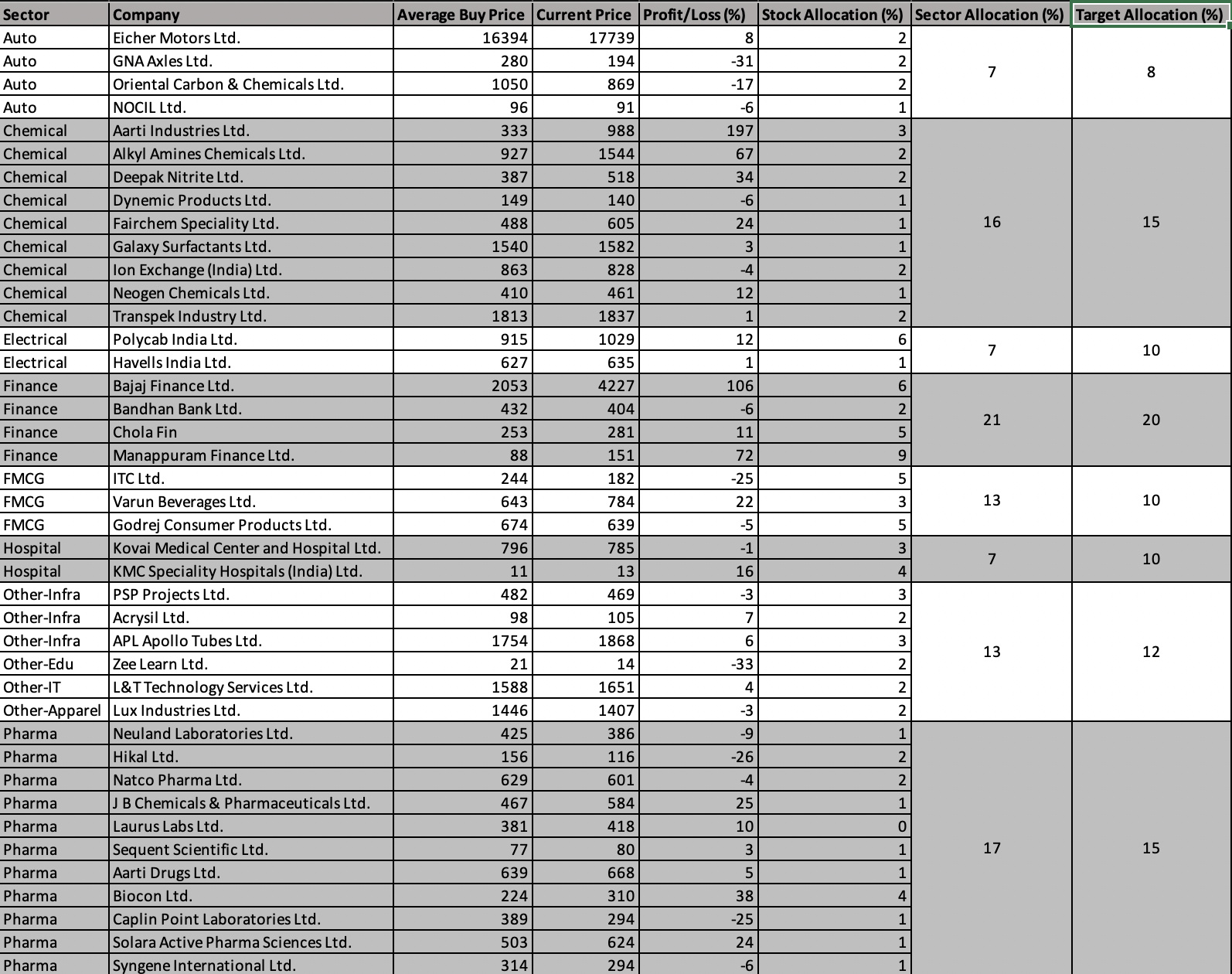

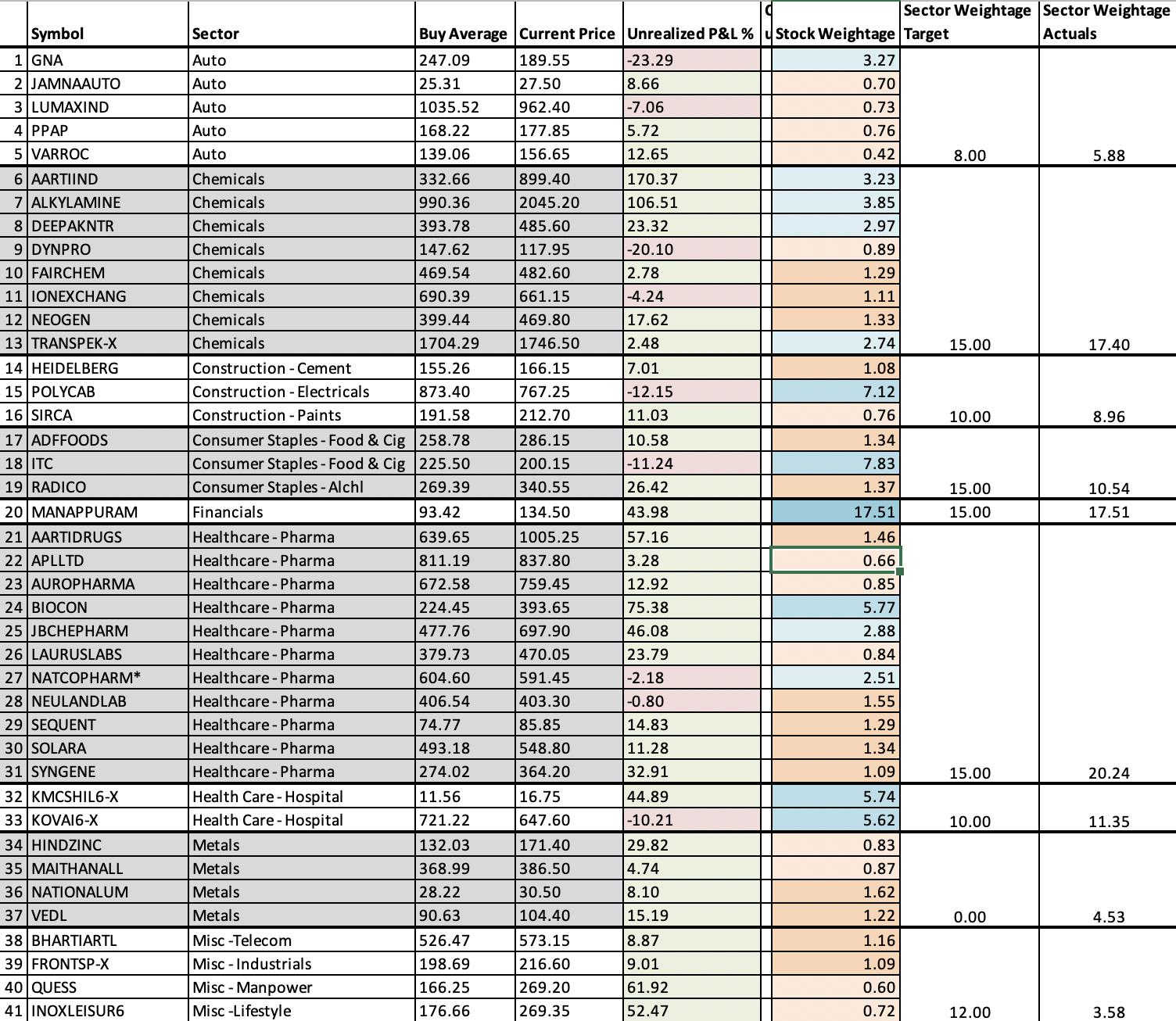

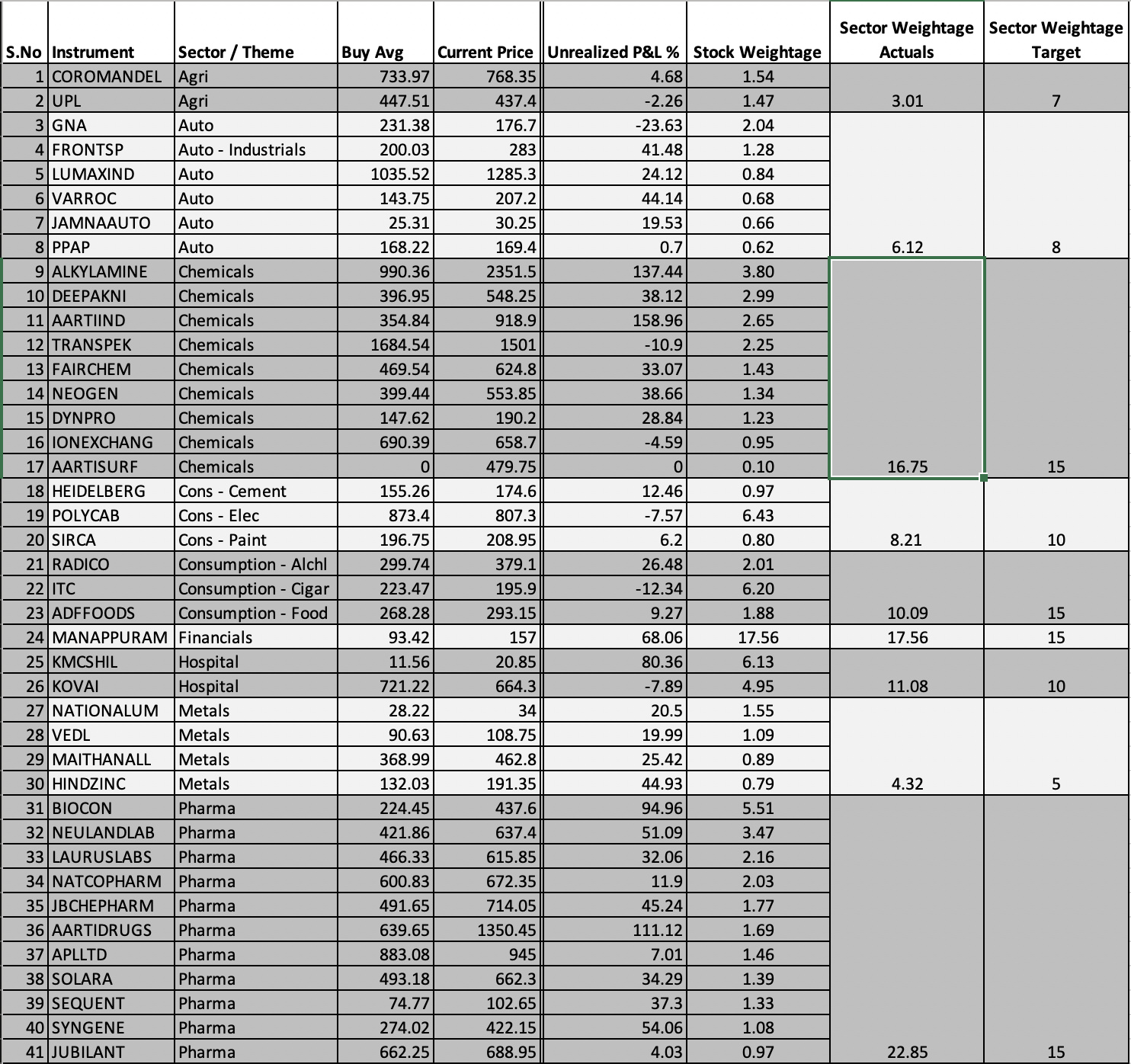

Below is the current state of the portfolio, please provide your valuable suggestions. This PF is recently revamped as the ongoing correction has burnt my fingers badly especially my holdings in CANFIN, DCM SHRIRAM and KTKBANK got impacted a lot so I booked losses and entered into Bajaj, Maruthi, and Eicher.

My holding in Manappuram is in red as well but I want to wait and watch since it is fundamentally strong and believe it should be able to bounce back but not sure whether there will be a meaningful reward for parking a huge % of PF here. Please advice.

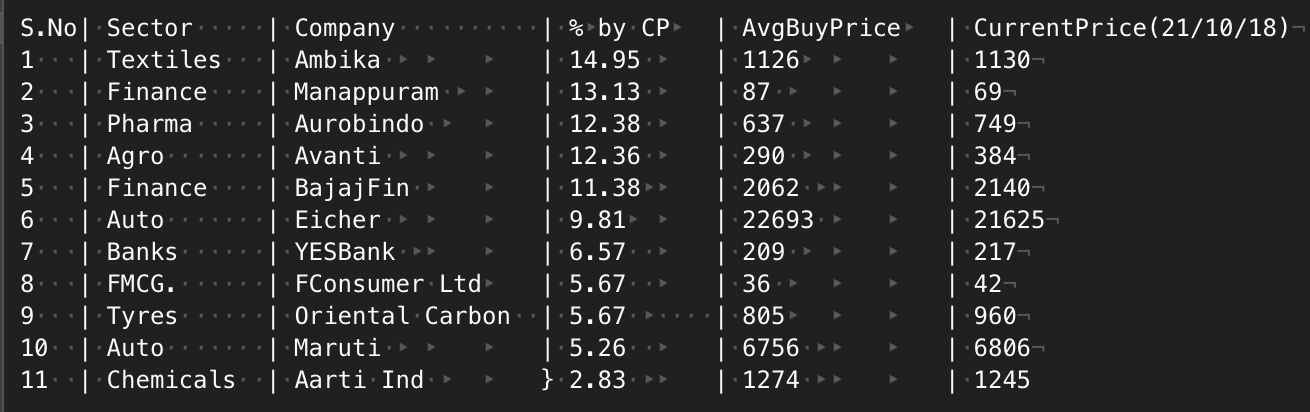

Ambika: This is for portfolio stability. I have been slowly accumulating this stock since the 600 levels. This is not a great company but definitely a good one with a credible management. Their ongoing expansion plans would produce a positive break out in the coming year

Manappuram: They have a strong network in South India. Hailing from Tamil Nadu, I could visibly see their presence and familiarity among the locals. I see this as a good business for at least the next 5 years as South Indians thirst for gold and land is continuing. The mortgaging land is tedious when the need is for short-term and small so people obviously going for gold loans. Recent corrections pulled my holdings to -ve territory.

Aurobindo: Managed by the founder. Unlike many other founders, he is willing to grow the company through both organic and inorganic way which shows his high aspirations. If things work out this could become a big story. Recovering pharma sector is another good news

Avanti Feeds: Another company that is being run by the founder with good leadership skills. People’s appetite for seafood is increasing so I believe the shrimp demand should pick up in domestic apart from the US. However carries a higher risk due to US regulations, Vietnam’s increasing competition, shrimp disease.

Bajaj Finance: Recently entered, I missed this stock 2 years back due to an early exit. Since then I have been watching it as I didn’t want to chase it due to higher PE. Used the recent correction to re-enter. Higher ROE and ROCE with a good management.

Eicher Motors: A past turnaround story under its new generation leadership. There is no doubt in the management’s execution skills and aspiration. The company is entering into its next phase, if the leadership’s plan to take it overseas and venturing into 600+ CC segment workout, another round of growth and compounding is possible. However, the current RE demand in India should provide the margin of safety for the next 3 years. So I initiated this position recently as there is a decent risk-reward. Based on the progress I will take a decision on this stock in the next 1 year

Yes Bank: Another watchlist for a long time. Recent slide game me an opportunity to enter. I feel Rana’s exit is overseen and the current valuation provides a decent risk-reward as the negatives are almost priced in.

Future Consumer: Backed by the strong network of the Future group which owns Big Bazar and Nilgris outlets. Bringing new items to the shelf is not a problem for this company. The FMCG war is heating up due to Amazon and Walmart’s interest over it as they see this as Retail 2.0 in India. Several acquisitions and merges are possible in the coming years and FConsumer has a great chance to get the strategic partnership to push growth.

Oriental Carbon & Chemicals Ltd: Dominant producer of insoluble sulfur which is used in tyres. The company has been expanding the production. Longtime holding in the portfolio.

Maruti Suzuki India Ltd: Recently entered after the meltdown. No need to explain the brand value in India. Its recent line up under NEXA is able to inspire a new set of consumers so the growth should continue

Aarti Industries Ltd: Recently started the tracking position to take advantage of China issues.