Results are out:

Decent set of #'s

Hi Sir,

I think there is some problem with calculation. If I am checking Australian revenue per employee it is 0.34 crore or 34 Lakh per employee which will convert to 45000 Australian dollar per year.

Now we can check with anybody from Australia that it is possible or not! If anybody having any idea about wages in Australia please write your comment.

Thanks!

SIS Ltd Q4 FY21 Earnings Call notes

Our focus predominantly will continue to remain on organic development . As we scale over the next 4 years, and we’ve modeled this out, so we’ve modeled it out by SBU by month for the next 48 months. This modeling exercise was already taking between December and mid-February with all SBU heads and forms the baseline for the vision 2025 document and the ESOP, which is now rolling out to more than 700 key managers.

So if I give you specific numbers, less than 15% of our next 4 years revenue development is being planned for M&A. 85% or predominantly is organic development .

M&A is only strategic for – either for market share and geography or to enter a customer segment or to add a service portfolio gap. The real growth has to be organic.

we see facility management to probably be the biggest gainer in our entire portfolio because facility management pre-corona used to be a cleaning and hygiene issue. It was an outsourcing and efficiency issue. Today, it – facility management has transformed into a health and safety. It’s about having a safe workplace for employees or a safe place for your customers to visit.

So I see the per square foot expenditure on FM services going up because it’s become a business continuity imperative. That’s the way I see it playing up.

Henderson put option adjustment

So when you make a purchase of the 60%, obviously, some element has gone to goodwill and other intangibles. But this entire 40% has also gone to the goodwill line. Now of course, the founder has chosen for his own reasons, reasons best known to him, to exercise the option in 2020. Obviously, there’s not enough time between then, 2019 and 2020, to execute all the plans which the business had planned to achieve over the next 3 or 4 years

So what we did was because this entire consideration was – future consideration was sitting in goodwill, and that was also a very large number, and so a significant write-down of the liability. So conservatively, we had a discussion and consulted with the auditors as to how we should treat this entire event. So they also suggested that because this was there – right now, it is largely towards there, you’re going to write down the liability. It is a significant amount. So our recommendation is also you adjust the goodwill to that extent.

Rituraj Sinha - All our acquisitions are 2-stage, 3-stage acquisitions, where we acquire majority and then we acquire over time linked to performance of the business, right? So what we basically do in very simplistic terms is to try and assume how much we’ll have to pay 2 years down the line or 3 years down the line, depending on how the business performs. We had obviously made a similar calculation for Henderson. And because the promoter is going out 3 years earlier, our payout is significantly lower. So our future liability to this deal is significantly lower than it would have been in 2023 when the business would be significantly larger. So therefore, we are adjusting down .

The true value of the business remains as is. In my head, this is just simply a reassessment of what was payable for the remainder 40% if it was done in '23 versus it being done now.

Why not pay down debt with cash on hand?

yes, we could use the cash on hand to actually repay debt. But you have to understand that we are a business which is doing roughly INR 820 crores monthly revenues. And out of this – nature of business is such that almost 85% is statutory payments and wage payments every month. So the cash that is sitting on my books may look large. And the question is natural that why is it not used to repay outstanding debt, et cetera. But the point is that the cash is only equal to 5 weeks of working capital for SIS, maybe 6.

So I don’t think that we have so much extra cash just as yet . And I’m sure at some point in time, if we do have that, just like we are meeting SXP payment through internal accruals, we will look to take up more and more repayment and buyback and outstanding shares purchased through accruals and not debt.

But as of right now, you must understand that the cash might look large to you. But in my head, it’s only 5, 6 weeks worth of working capital. And given the current environment, I think it’s better to sit on cash.

SIS continues to pursue 20% year-on-year growth, 20% return [indiscernible] and greater than 50% OCF to EBITDA. These are the 3 metrics I’ve spoken about at several occasions in the past, and these are the 3 metrics that you should use in your model. Please understand that the vision 2025 is an internal commentary. It is designed to show people the opportunities that lies ahead.

Lower margins in Indian Security and Facility Management in Q4FY21.

I think let me say that the important thing for us is to look at the gross margin line. If you look at the India security business gross margin line, that remains intact. There’s no change on the gross margin side. The change in EBITDA is because of gratuity accounting catch-up that has happened in Q4 and some SG&A movement. Otherwise, the India security business is pretty much reporting similar margin profile as it did in Q3. The FM margin is compressed because of the negative operating leverage. The business scale actually – monthly revenue scale has come down. So it’s looking lower right now. But if you normalize it, gratuity, if you normalize it for SG&A, that will still show up at close to 4%. And when the business scales back to INR 120 crore plus revenue, I’m hopeful that it will come back to the 6-odd-percent range. So a very high-level comment there is SIS margin profile continues around 6% ballpark when you normalize it. It’s at par with what it was Q4 of last year.

on the SG&A, I think all businesses – around about mid-December, we took stop to say that India is going to go back to normal, everything is going to go back to normal. We started pushing up some SG&A expenses in Q4 in anticipation of a big jump start of the economy.

Obviously, like most, we also did not see the second wave. And that’s why you have a surge in the SG&A cost between Jan to March. I don’t see that to be a permanent phenomena entirely. And I think it will level out. But Abhijit, again, my advice to everybody is do not get super excited with an outlandish 7.5% EBITDA performance of SIS International in one quarter because that’s not the steady-state number of EBITDA margin for international business, more than 7%. Similarly, the steady-state margin performance for our FM business is not 1.9%. These are just quarter-to-quarter aberrations that are happening in a crisis here. The important thing is to look at the gross margin profile. And that remains stable, which basically means that this will – given a few quarters of wobbly behavior would settle down around the 6% ballpark range as it was pre-COVID .

transitioning the business from a services to Solutions business. I just wanted to understand that a little bit better given the fact that you are looking at sort of a 20% transition or 20% contribution there.

They are more like more than 2 lakh ATMs in the country and more than a lakh, lakh and a half or off-site ATMs so the banks actually were using 5 lakh-plus guards to be sitting outside bank ATMS. Now they want to reduce all of that, cut all that cost. What they are doing is alarm monitoring and response. They want to put in alarms instead of guards. They want to monitor these alarms remotely, and they want to have emergency response or beat patrol, somebody to go and check at certain frequency, et cetera, rather than having a full-time guard.

In the last quarter itself, in the last 3 months, we’ve picked up 13,000 such ATM locations in the last 3 months, which adds up to maybe 10% of all ATMs in the country which are off-site. So I think this is a customer-led change from a manpower headcount-type solution to a – service to a solution where they are asking us to provide alarms on an OpEx model. We own the alarms, we leave it to them. It’s a 4-year, in some instances, 5-year contract, and we are doing all the technology-based monitoring remotely out of good now. And we are using the IOPS technology platform to use our area offices, spread across 600 districts to give them Google coordinates to go and check these sites, fill up a form on their mobile app and upload the status of this ATM check once or twice every day. So that’s a classic example of moving from a service to a solution.

So what’s happening with the COVID is another trend that we have seen that clients want a single solution provider. They don’t want to deal with multiple vendors, both from a safety point as well as the coordinating point. And we are getting more and more contracts on a one is a year basis. That includes not just our usual housekeeping, mechanized housekeeping, security, or even the tax equity, but other value-added services from horticulture to linen handling to even providing qualified staff for the health care sector.

We just took up a large hospital in Mumbai, where we are providing patient care attendance and qualified nurses, too.

So it is that entire outsourcing of all noncore activities that are coming under the One SIS. And they are usually on an output base, not a cost-plus model, which allows us to earn a higher margin . And at the same time, often save costs for the client side also. So this is a model that we also want to adopt and promote more in the future. And I think this will be a trend that many of the clients do.

Solution means that there are lesser competitors who can tackle that level of technology. Solutions also means that you have longer duration contracts. Solution also means that your pricing is outcome-linked, not input-linked. Overall, Solutions business means that you operated a higher gross margin line by almost 5% compared to a standard service .

How confident are we in terms of sustaining 6% rather than actually thinking on the upside?

SIS operates 306 branches across the country. In larger cities like Bangalore, Bombay, Delhi, we have like 20 branches in one single 50-kilometer radius. So we are not suddenly going to add another 300 branches to achieve our doubling market share objective. Absolutely not. The branch growth is going to be negligible because I think the time to really leverage our pan-India presence has come .

The second thing is, are we looking to increase market share by pricing ourselves low, the answer is absolutely no. We do not want to become the cheapest and the largest security company in the country. That’s not our objective. I’d rather be not so large, but hold my premium pricing.

So you must understand that this market share growth is not going to come at the cost of gross margin compromise. That’s not how we’re looking at it. This market share growth is going to come from the 5 factors I called out . You have to understand, Alok, that labor reforms means that my addressable market is going to go up significantly. When the government spends INR 5 lakh crore on infrastructure over the next 4 years, the locations where they need FM services is going to go up or security services or CCTV cameras is going to go up. So the trends I called out is for that reason. I see the market expand and then I see also our market share expanding within that. So the opportunity is very clear. And I think we are in pole position because of our #1 spot that we are occupying, our pan-India presence. And most of all, the showing of SIS is during the crisis year.

SIS security numbers or even overall 7% year-on-year revenue growth in FY '21 is without price change. It is purely volume-oriented. This is the first year in many, many years, at least in my '19 years where we haven’t had rate revisions. Government of India has not hiked minimum wages this year. States haven’t hiked minimum wages this year. There were some parts and pieces in international markets. But by and large, in India, there is no price escalation. It’s all volume growth that has helped these numbers come through

Management view

RITURAJ K SINHA – MD, SIS India on overview of FY21 & signs of recovery

“The India security business saw a 102% jump in March 2021 as compared to March 2020; while facility mgmt. continues to be down at 12% on a fullyearbasis. There have been pockets of increased demand like hospitals, ecommerce and manufacturing.

There has been a rise in demand for security services and facility management from hospitals, nursing homes, warehouses and mfg facilities. On the other hand, a slow rebound is happening in segms such as hotels, malls, offices, railways & airports – which remained closed for large parts of FY21.

However, our international business of security services has been the outlier with over 22% YoY growth in revenue. The steep growth here is on the back of adhoc Covid contracts with the govt in Australia & New Zealand along with rebound in the aviation and special events business.”

Hi Friends

PFA some notes we collated on SIS

#About

SIS is a USD 1.2 Bn Indian multinational and market leader in Security, Facility management & Cash Logistics solutions with operations across India, Australia, Singapore and New Zealand. SIS is the largest Security Solutions company in India. It is also the 2nd largest Facility Management company and the 2nd largest Cash Logistics provider in India. With 230,000 frontline essential services workforce, we are among the top 5 private sector employers in the country. SIS services over 9000 clients at 23000+ sites spread across 630 districts in India.

#Thesis

During its detailed analyst meet, SIS outlined its Vision 2025, whereby the company plans to aggressively capitalise on its market leadership in almost all of its businesses and hence double the market share by 2025. Importantly, SIS plans to achieve 85–90% of these growth objectives organically. Impending labour reforms too should assist the company consolidate market share.

Valuations

-Key Issues

In the book Consolidators - one chapter devoted to the company. Some very useful insights on the journey of the company and the management & owner Rituraj Sinha https://www.amazon.in/dp/0143429302/ref=cm_sw_r_wa_apa_glt_fabc_2QDWQDSZJ3J5RV7Z6V4B

Some excerpts from the book

Reason for Rituraj coming back

Legacy

A journey of Ambition and gumption

Diversification

Capital Structure

Training

The system has helped Rituraj focus on three important requirements—hunting for the best talent, identifying new businesses and new partners, and fund raising. To help him in these three areas, Rituraj is aided by teams.

Values espoused by Rituraj - Culture

Disclaimer

CEO says Q1 21-22 revenue and profit will at least be equal to Q4 20-21. April and June in Q1 were good and May was weak, he said. Let us see the actual Q1 result when it comes

My notes from the AGM:

The format was closer to a family living room conversation rather than a formal company presentation. After a mundane speech from Mr. Kishore Sinha that felt like your grandfather reading an email out loud, Mr. Rituraj took over.

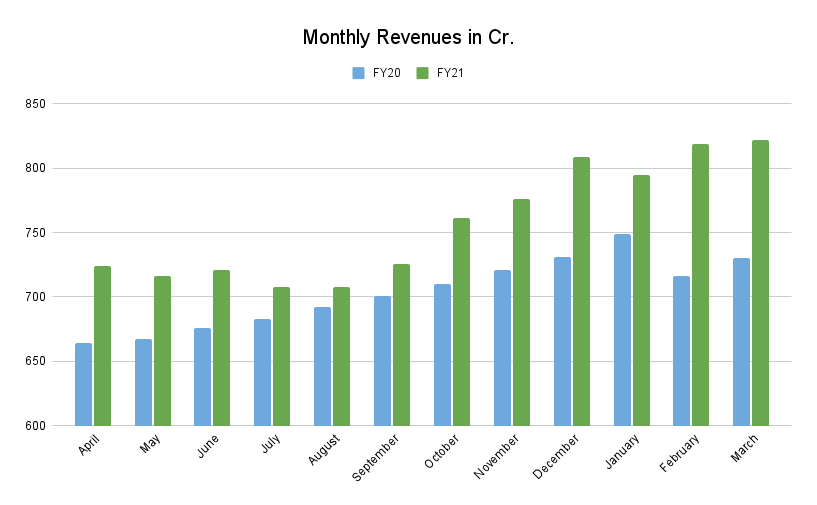

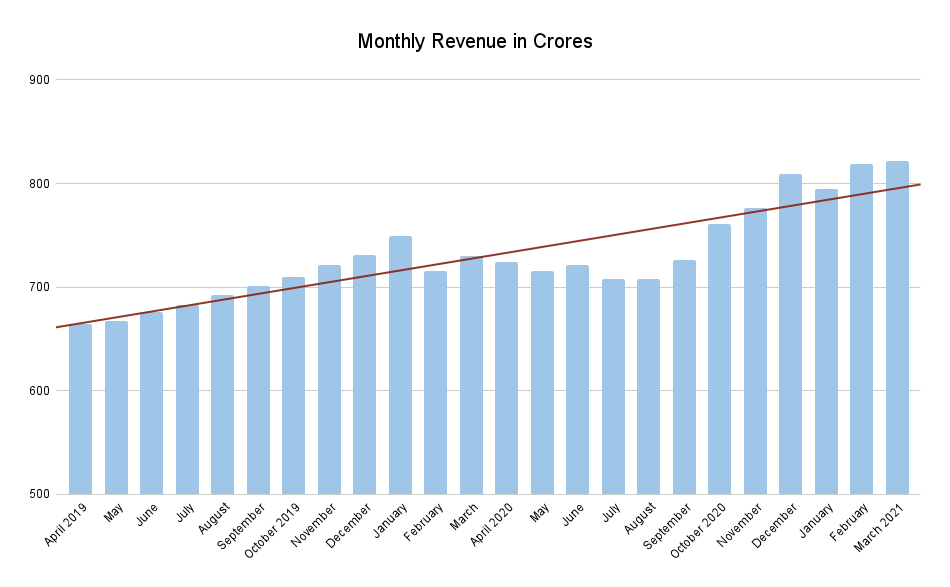

They then gave the monthly revenue breakup for the last two years, and I love detailed disclosures. Before you look at this, think for a second whether you expect them to be seasonal/cyclical in any way.

The Q&A was bizarre, and they definitely need to screen the questions taken going forward. There was someone who asked more than 10 questions, and 8 of them were downright insane. This ranged from asking SIS to employ his legal services to asking for sweet boxes for all shareholders as the AGM was virtual and they missed out on the opportunity for free coffee and snacks.

How has your supply chain been affected by Covid? (covered extensively before, answer rehashed).

What will be the growth triggers in FY22?

Demand resilience and supply side resilience has been demonstrated. To get back to 15-20% growth rates, we need to see how the economy picks up and whether there is a third wave. Have had a decent start to Q1FY22, April and May were resilient. After experiencing FY21, we are better prepared to take on FY22.

Reiterated:

What is the capacity utilisation figure for the month of May/June 2021? (What an insane question to ask a security services provider…)

How many employees did you sack due to covid, what was the salary cut?

We have not sacked a single employee and haven’t cut the salary of any employee at any level. Gave increments to frontline employees in October last year, no increments to corporate management.

Sounds great: they’re being really generous towards frontline employees. Page 58 on the annual report removes some of this shine.

Once again, we are not a manufacturing company, we have no factories. Humbly welcome you, and all shareholders to our training academy in Jharkhand after the pandemic.

The entire AGM was worth listening to for the following question alone.

The exceptional items are basically government grants. The beauty of essential service operators / large employers is that both in India and Australia, job creation / employment is a priority data point for all government policies. Governments came forth to give large employers like us subsidies to prevent job cuts. We expect to grow 2-2.5x GDP growth as essential services provider. Every time you build 1 new hotel, mall, metro, manufacturing site, healthcare facility, we get 5 business deals out of it: security guards, CCTV, facility management staff, pest control, ATM replenishment.

The beauty is when economy contracts, our demand does not shrink. You have the benefits of a defensive + consumer business all in one.

The specifics of the exceptional items also came from the SIS Henderson Holdings subsidiary. A shareholder having 40% stake in it was supposed to sell it to us for X dollars, and we had accounted for it. Due to Covid, the shareholder wanted a much faster exit, and we were able to bring down the price to X/K dollars, paying much less for the 40% of shares.

This reminds me a lot of the Cera Sanitaryware thesis of every new home needs two new toilets.

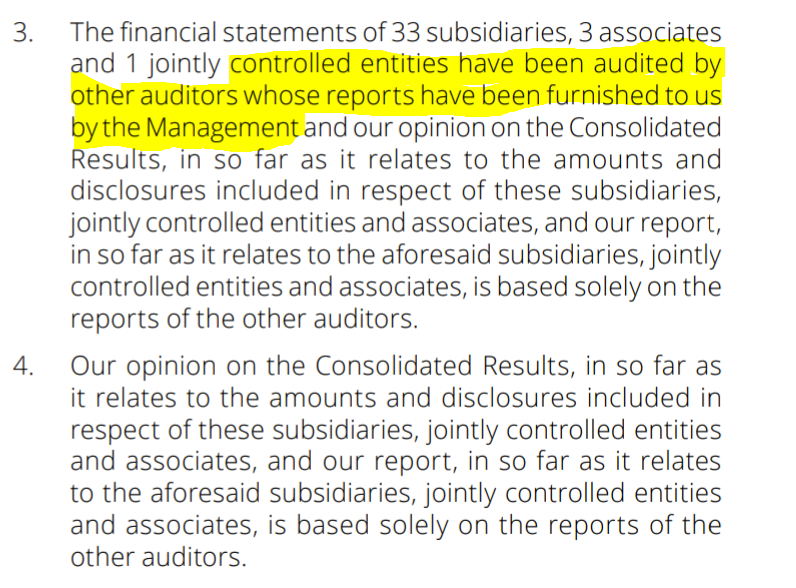

To address some of the queries regarding unaudited subsidiaries higher up on this thread, note page 162 of the annual report.

33 subsidiaries still haven’t been audited by the primary auditor. However, it isn’t as bad as I initially thought:

I have written to the management, asking if the audited reports on the 33 subsidiaries can be released to shareholders. The annual report says that they needed other auditors as the subsidiaries fall under international tax regimes.

Will post about the annual report soon, there are some very nice deals lined up.

Disclosure: Invested

hello everyone , can someone helps to understand debt level,is growth funded by debt?

thanks in advance

invested

discl:not sebi register

Seems to be paid article, not opening for me. Can you share key points please?

Very bullish on SIS but the company isn’t sharing transcripts for last few quarters,which isn’t expected from a transparent management and before that haven’t been in continuity. Don’t know how long before the streak breaks

Search on youtube, all earning calls are happening regularly.

Can you share your investment thesis as to why you are so bullish on this? Some of the points I was unsure about are listed below

i think you must read consolidators book , sis is gaining market share .

My key reasons are:

Simple asset light business, diversified across services offered and country it operates in.

Having 3 main revenue streams and 4 countries to operate in helps hedge the company risks of being over dependent on single source and facilitates in creating economies of scale . Timid growth in one of them can be countered by other verticals. 15 to 20 % growth achievable in normal circumstances in foreseable future.

Even after being the largest player in Security Solutions and second largest in FM the market share is only 6-7%. A huge market size waiting to be tapped. As India enters the next growth phase, more businesses will provide the opportunity.

Good Inorganic growth(acquisition and joint ventures) track record with Henderson, Uniq, SLV, Terminix, prosegur, SXP,MSSSecurity ,DTS .All these M&A have upticked the top line and bottom line and increased the geographical reach.

Inelastic Demand: when the businesses around the world were completely shut and opening up slowly due to covid waves SIS still grew(7%) and sectors like FM recovered to the pre covid levels in Q3 itself. Company has maintained its goodwill and contracts among its clientele in tough business scenarios.

Stopped the cash logistics services in some ATMs contract where the margins were being affected leading to inefficiency (Good management step, to discontinue verticals hindering the business )

Bought it at fair Valuations(430 levels). Solid balance sheet, Good return ratios and consistently increasing cash flows. Debt used in buyouts has been decreasing substantially.

Company aggressive and ambitious in increasing sales team for acquiring new clients. Research and development has also been happening for FM and security verticals. Technological assistance will help SIS to deploy less personnel. EBITDA levels may even reach 20% for FM for specific contracts

Good pay, employee satisfaction and holistic culture imbibed, in a sector dominated by unorganized players. Was a part of top 50 firms to work for in India by GPTW.

Management commentary: Personally liked the annual reports , not over ambitious in setting goals, and future plans. Vision 2020 was almost executed on most fronts. Expecting to double its market share till 2025.

Competition and Employees:

SIS holds a dominant position in all the country it operates in all three businesses (cash logistics ,security, fm). There is no big entry to barrier, but I believe Learning costs which it incurs cannot be mirrored on a large scale by small players.as the industry changes is a major tailwind. GOI in upcoming quarters is gonna come up with Wage and Labor laws, Which is gonna benefit organized players like SIS. Company’s CEO in an interview informed that all SIS contracts are based on back to back pass through arrangement so if wages increase by whatever % they increase their contract costs and pass on the costs . This labour and wage laws enactment will also begin the paradigm shift from unorganized to organized sector .

Another major advantage that Sis has its quality of its services offered. From being in top 10 players in FM in 2015 to second biggest player in FY2021and holding a dominant position in cash logistics ,company has grown both inorganically and vv. Upon researching about the reviews of SIS came across an instance of a residential building ending its contract with sis due to high cost however the new company was not able to deliver the needful so SIS was again deployed to the task. Can conclude SIS has sort of distinguished itself from the mediocre players even if it charges a premium . Companies and residential buildings don’t compromise on that part. So they do enjoy a brand advantage which will only get better.

Employee cost: SIS Ebitda margins have been in correlation with global peers(6%). The business sis operates in is not of boasting high margins but the less capital deployed helps it in achieving stable RoCe of near around 20%. Post Covid coupled with strained margins numerous small players will find it hard to compete with cash rich SIS which has been consistently investing in its resources and technology to improve customer experience. With digitalization can see reducing their costs on various fronts

Australian business. The Australian business suffered a de growth due to lockdowns and covid wave in Q2 and margins collapsed due to vaccination programs, increasing training and sales costs. However I believe it is transitionary and last few quarters of the Australian market show that. The roce of Australian market has been 70 %(claimed)

Political Connections: Though it has been highlighted before in this thread ,it is surely a thing to take note of but I don’t see any big red flags as of now. No major developments has been made till now.

PS: Views may be biased

So my issue is not with the margin but decreasing margin. Earlier the company use to have ~10% margin but is now dropped to 6%

wouldn’t this increase the employee cost as these new laws are generally employee friendly and they might add up the compliance cost? and hence, that would benefit the unorganized sector?

Debt has reduced but still not low. It has the interest coverage of 3-4 which I think is adequate but looking at the financials it appears that the growth is on the pretext of the debt (inorganic growth) and not organic growth of any of the streams (except the security camera division but it’s a small %age of the total revenue) so to achieve 20-30% of growth they might have to keep acquiring companies leading to debt never leaving the balance sheet. Any views on this?

Also small point I noted, their receivable days are also increasing. Can you share some points to show that management is capable and competent as you said?

On margins: Do not think there was ever 10% margins for the business adjusted for one offs etc. The company has always guided for 6% kind of band - this is a plain vanilla body shop business, and there cannot be any decent margin improvement. Growth will be the main driver.

Employee cost increase is good for them. They take a specific margin from the client, and increasing employee cost increases their absolute EBITDA while keep margins stable.

The way this sector grows is through acquisitions. It has been same globally too. The smaller players are subscale and companies add scale and margins through acquiring them. You can think of diagnostics chains like Dr Lal, Metropolis etc also growing like this - this will continue, one has to be comfortable with this notion or avoid.

Receivable days has been in a band, it keeps increasing or decreasing based on macro conditions and relationship building, but does not shoot overall levels. In general trajectory will be on the increasing side, as F&M business has higher receivable days, and as the proportion increases, the receivable days will increase.

Management capability is in the market share gains they have seen in both security and F&M business. If you compare how companies have grown in the security and F&M segments (most are unlisted), then SIS has outstripped everyone by a decent margin.

Standalone revenue growth of SIS.

(EBITDA margins have always been in 6-7%. refer ARs)

It would be unfair to say that growth is only inorganic when it has been growing near about 20% on standalone basis since 2012. M&A have provided much needed safety net to expand and target different geographies.

Worth noting that these M&A have added huge value to the business considering M&A can go horribly wrong .I am quite comfortable if company is finding good opportunities to grow, increasing customers and cutting out its competition thereby creating synergies. SIS is lookin to create a niche in these services as well and is widening the gap between it and other players.