Segmental Revenues are as follows:

‒ Security Solutions India: Rs. 858 Crs in Q1FY21 vs Rs 808 Crs in Q1 FY20

‒ Security Solutions International: Rs. 1020 Crs in Q1FY21 vs Rs 913 Crs in Q1 FY20

‒ Facilities Management: Rs. 293 Crs in Q1FY21 vs Rs 290 Crs in Q1 FY20

Cash Conversion - The company demonstrated very strong cash conversion with OCF/

EBITDA at 81% in Q1FY21.

Business Updates:

-

India Security Solutions Business: SIS role as an essential services provider was reinforced during the toughest quarter ever faced, as we ended Q1FY21 at YoY growth of 6.1%. All our branch offices continued to be operational during the lockdown period and we ensured business continuity for all our customers with minimal disruption. Similarly, despite aggressive and cautionary provisions, our EBITDA margin was stable at 5.4%. We continue to be cautiously optimistic for the rest of the year - market share gains will be the focus for the year on the back of cross sales initiatives and launch of new solutions.

-

International Security Solutions Business: The International business has been the

standout vertical this quarter with revenues of Rs 1020 Cr which is a YoY increase of 11.7%. The growth in the international markets was aided by strong, proactive economic and medical response to Covid resulting in minimal disruption to the business climate. The EBITDA margin for the international business was 5.9%, despite conservative provisioning and deferring recognition of certain government grants.

-

Facility Management: The Facility Management segment was impacted to some extent due to the extended lockdowns in big urban cities in India. The revenues for the segment saw a 1% increase YoY. Going forward, the FM segment is likely to see increased operating expenditure, higher quality standards and more intensive cleaning requirements. We believe that this is going to lead to significant changes in industry dynamics and greater formalisation. We have launched new solutions in the areas of disinfection, deep cleaning, sanitisation and production support which will help us greatly in increasing wallet share with customers.

-

Cash Logistics: The Cash Logistics segment continues on its steady path of portfolio rationalisation and margin improvement. Despite the ATM pricing reset getting delayed due to the pressures on the banking sector, our other segments of retail cash management and cash in transit continued to show strong operating metrics. The segment delivered a 68.4% YoY growth in EBITDA in Q1FY21, despite a 9.8% YoY decline in revenues (on account of closure of unprofitable routes and contracts). We believe that our focussed operations will continue to stand us in good stead in the coming quarters.

Commenting on the performance, Mr. Rituraj Kishore Sinha, Group Managing Director said, “The Covid pandemic and lockdowns have reinforced the essential need for our services, which are a business continuity imperative for a safe workplace and society. The Q1 results establish that our industry is less impacted and will recover quicker than many other sectors. Covid will also accelerate market share consolidation as customer focus is shifting towards expertise, reliability and market leaders. Given near term uncertainties, we continue to remain cautiously optimistic and will undertake prudent provisioning policies to factor for unforeseen surprises.”

Q1FY21 webinar notes Might have missed few points as the line was not clear

I dont think many cos came with kind of results like us

2 factors 1) essential service 2) execution of HR payroll

Our pricing power was highlighted. No negotiations by customers

GM stable. no negotiation. Vendor change / customer attrition at all time low

SG&A saving of 40cr possible. 20cr of it will not be permanent. Some is due to less travel.

International business has balanced volatility of india. For long time people saw it as a drag but COVID showed the importance of having a counter balance part. 40% revenue from Australia, NZ and Singapore. Key driver was that these countries dont use police or para military for lets say COVID facilities. Non-core police functions being outsourced to security services cos. India will also get to such model after a long lag

Understand the difference bw staffing and services. We have 100% revenue from services, zero from staffing. COVID will bring out the diff. Urge to look at results of ISS global, G4 global, Securitas. None reported pressure on revenue/margins. Today you cant run a office without a security guard checking temp, mask compliance. Facility management is a business continuity imperitive. Services are needed more than ever

During Apr-June we secured 1600 new orders. Only marginal drop in revenue

WFH trend- No clue of the impact. But some interesting things- in last 150 yrs railways shut down. Railway as it re-opens they have to ensure sanitation. If and when they re-open, the spend on hygiene and access control will be higher than ever before. Similarly for IT, they are super consious of employee safety. Even for 1/3rd employees the precautions are high. Spends on cleaning of cafeterias etc is 3x. Even if half of IT workforce comes back, the spends would go much higher.

Security and Facility management are needed even more.

Most schools, companies, railway stations etc will have Assembly line setups like boarding flights. One guy does sanitization, one checks bags etc, one checks temperature

In next 6-9 months, which part of business will be most difficult? SIS has survived the impact. Looking fwd for a V shaped recovery. 100 day plan of 1st response to COVID-

-

keep our offices operational. Our employee reporting during this time was 98.3%

-

Gross margin impact. In Q1 we had hardly any GM change. EBITDA fell because of prudential provision. Carrying 80JJ credit which gives Tax buffer.

-

Cash flow management- In 2 of the 3 months, we collected more than normal. OCF/EBITDA high indicates that

-

Not allowing sales engine to shut down…approached 32k clients in last 100 days.

-

Digital transformation- new IT platform. Will come out better prepared

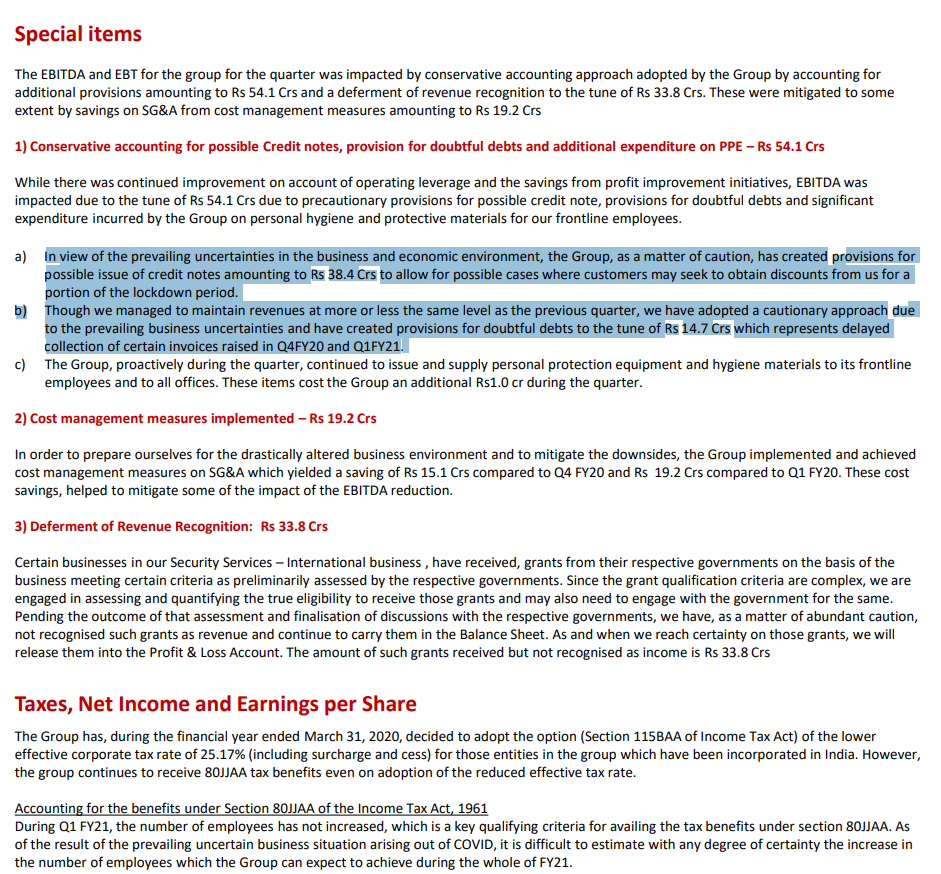

Coming 1-2 months can be impacted for our customers. We took very very prudential stand and provided 54cr. NOT at all linked to pressure on collections. We provisioned because we dont know how next 9 months will go. If things go well, this amount can flow back to EBITDA. 38cr is reduction from revenue. 15-16 cr is on account of affiliates, which is in other expenses.

2 big trends that will lead to organic consolidation in this space. Bigger than GST reforms or labor reforms.

-

When all customers are looking to cut other costs, they want to increase spending towards safety and hygiene. Factory/ movie theater/ schools should not shut down due to safety concerns. How much it translates to us remains to be seen.

-

Customer procurement focus was cost. Now they want reliability and quality, ready to pay more to market leaders.

Want our revenue to go back to 2% m-o-m growth.

Inorganic as and when it comes in 12-24 months. Net debt/EBITDA excl lease liability is 1.1x. Slower growth as opportunity to get balance sheet even better than 1.1x. Then we will be geared for an acquisition. People are paying us sooner than before because of the essential nature. DSOs slipped 5-6% but WC intensity will reduce. Debt has gone down by 30cr in Q1. We are comfortable. Avg borrowing cost is 7%. Not worried about leverage.

Govt focus on job creation, labor reforms. We have potential to create entry level jobs, which is priority of govt. We are very bullish about labor reforms. Will be looking to hire more.