I want to write about 8k Miles Software

Market Cap 1500 Cr.

Debt 40 Cr.

PE 65, valuation is expensive,

Main Business

Providing Cloud Solutions to the Global Customers

Managing cloud applications for Global Customers with Global Partners like IBM, Microsoft, CA Technologies etc.

Main Global Customers

MERCK, CISCO, Trimble, GSK, Adidas, Stanford University

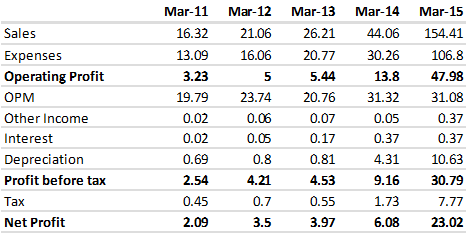

Financials

Main Growth Factors

Companies are finding it easy to go for cloud , rather than investing in IT infrastrcuture.

For companies it is moving fixed cost in variable cost

Total Cloud market is expected to grow to US$ 282 billion ( Source Nasscom Gartner, 2015)

Explosion in Broadband and smart phone penetration with 3G and 4G services

How is 8k places

One of the early movers in the field

has global Customers

Experiences Promoters from the same field,

Disclaimer

I am not expert in the cloud field, so difficult for me to make a recommendation , however will request Value Pickr members to comment on this opportunity

Company has shown almost 10X growth in less than 5 years and still talk about the huge potential it has

Not invested , however planning to make small investment to start with

I doubt whether they can maintain same growth pace in future. Dotcom boom & burst showed that nothing can grow in such absurd pace for long. Before investing you must think of margin of safety. Is there any margin of safety in 8K today if you go wrong. beware of such script as it may be a suckers rally or an operator driven. In market never chase very high growth rate company at an very expensive valuation while its better knows peers like TCS infy are trading in modest PE as U will never know when the growth will stop.

We cannot compare TCS / Infy with 8k miles as 8k miles is boutique / niche firm which focuses only on cloud related services. Companies are currently rapidly moving to cloud as it reduces risk as well as head counts for them. So in terms of growth, we cannot compare TCS like giant’s valuations (which has 100 of offerings and cloud is just one of them) with 8k miles as 8k miles offers only cloud products and services that can go through re-ratings with just few big client additions.

Agree with you on the margin of safety. Usually big firms will be hesitant to work with small IT firms as it will put them as risk. So they will go with companies like persistent, Infy etc. So whether 8k can get into a big league with considerable Fortune 1000/500 companies will determine whether it deserves rich valuations.

Disc: Have small tracking position. Wait and watch mode.

Another point to note is 8k miles has grown out of single product dependency which is Amazon cloud. Now they are also into Microsoft cloud. So we don’t have risk like RS Software.

Still wonder why these guys are not getting to Oracle cloud which is a huge market.

I was not comparing infy Tcs with 8K. I was just referring while infy hcl tech infy are available at reasonable valuation how 8K enjoys such lofty valuation as normally market gives sustained 65 PE to very high quality company like nestle HUL etc.

I don’t expect them to grow 10x but even if they are able to show a growth rate of around 25 percent for another 3 to 4 years, it can be a good case of investment

there customer base is still good and I am sure they would be working on adding more customers

For me the most important point would be the credibility of the promoters

Any update on information on that would be great

They are still a small player and are building up capacity,

Don’t you think acquisitions are small and not very big teams are coming up so integration should not be an issue

The current COO of the company also came while his company was acquired

Any info on promoters from customers

Looks like an excellent company.

Generate 3crs cash from operations, pay no tax,

Acquire businesses worth 36crs, and at the end of year become debt free co after infusing cash from reserves & surpluse.

Just describing the business model. For any cloud provider like Amazon, or Google or Microsoft, 8k provides support for migrating small companies existing servers to cloud. Cloud required for redundancy and scalability related reasons. Migration itself involves assessing number of servers, memory space, what kind of database etc.

Post migration, maintaining the server involves watching it continuously, doing software upgrades and patches, debugging for any issues, application development etc for any new functionalities and finally, building tools etc for analytics.

8k does the above. Though actually its quite far fetched to compare 8k with TCS, but note that largest portion of HCL business is IMS and within that, data center management. You can consider 8k as data center manager for businesses on cloud.

I have done quite some work on this company and would be glad to discuss business further (would refrain from any targets as such, especially at this price)

Thanks a lot for writing

Business seems interesting to me as talking to my friends in the industry, it is becoming clear that most of the companies wants to go on cloud and there is s huge opportunity coming up in this field

My biggest question is that how much of that available opportunity 8k will be able to gain profitability

AOjha

What risks are you seeing in the business model of 8k

@aojha, as you understand the business model of 8k, wanted to have your insights on the following:

What is the kind of customer stickiness in the space where 8K provides cloud data management services and is it repetitive revenue for 8k or one time. Can their customers switch to some other company easily, basically want to understand their strengths in generating revenues consistently.

Their operating margins are near 30% range - can 8k continue to sustain such margins as they scale up and look for new clients and if you can explain this little more as to what makes them command this margin profile.

There does not appear to be listed companies exclusively operating in this space, so what is the kind of competition they face. Any other companies to your knowledge which are developing cloud data capabilities. Are Persistent Systems etc not providing similar services. It’s not very often that you find small companies quoting at 10x sales that 8k does.

Serious investors must ask questions to themselves whether 8k have economic moat. What does it do which the other established IT peers can’t do in near future. As basically it’s doing ims do such high pe justified. As the biggest wealth is created and destroy in pe expansion and pe contraction.

Adding in a few more details from what I have understood about this company till now and trying to map it in my own crude way with the business quality framework suggested by Donald and team:

Strategic Assets

A company which offers services based on cloud platform. It is also diversifying its portfolio based on it cloud expertise to mobile services, identity management, server management etc.

Expertise and tons of experience on cloud makes it a niche player.

Access to businesses which need cloud and hence it is doing backward as well as forward integration across the cloud business value chain.

Access to and partnership with most large cloud providers.

Disproportionate Future

Recent buyouts in healthcare area could help with Obamacare gaining momentum.

What Can Go Wrong?

There are many other companies in the market which “could” offer “similar” services and hence the differentiation could be lost. All Indian IT companies can offer such services, though 8k miles will invariably beat them in quality and efficiency.

Cloud services, at this point in time are more in demand from small SMEs\MSMEs and hence predictability of earnings is suspect. In terms of business development, this approach is diametrically opposite to how large Indian IT companies gain money by “partnering” with larger corporates.

With my limited understanding of their solutions, I believe that they don’t have any specific products that they sell yet and they are still primarily a services provider.

New Products/Innovation/Branding

Niche services in cloud healthcare space

Cloud is a service model in which the client is completely dependent on the cloud provider and hence as an extension on the service provider for cloud too.

This is based on my limited understanding, Will keep adding as I gather more details.

Some questions I haven’t found an answer to yet:

Do they earn by providing services - the usual time and material or fixed bid models, or do they get a share of the profits of the business? Or do they charge based on transactions?

How long have they been serving their oldest client?

Spoke to a CTO/CIO in a listed pharma company, he felt that their service would be of interest to even non-US pharma companies as it may allow for management of compliance, proprietary data, etc. However, although he was on SAP, he did not seem eager to transfer to cloud in a hurry. Conclusion: for him the product was a ‘vitamin’ and not a ‘painkiller’. However this needs further validation with other companies.

Also, need to understand what proportion of their revenues arise as a result of being an Amazon Platinum vendor and what % from Microsoft and others. What is the likelihood of Amazon providing the same services to end users in house and making 8k/others redundant? Who are the other approved vendors of these cloud providers?

As far as management goes, appears to be a technocrat & serial entrepreneur with a track record of building and selling several IT businesses.

@whipsaw - Promoter shareholding has dipped from 66.28% in 12/2014 to 61.96 in 6/2015. Thought this was in the article but I actually saw that elsewhere.

However, I just noticed that the promoter did not sell any shares but his % holding was diluted after issuance of 700,000 shares through warrant conversion by non promoter investors. I was (partially) mistaken - thanks for pointing this out.

Are the promoters planning further dilution? Last AGM had agenda items for (a) raising authorised capital from Rs 15 cr to 20 cr and (b) capital raising option for Rs 500 crore.

Any thoughts from members who are tracking 8k as to what kind of capital structure are they planning for the company and more m&a to come.

Spoke to a CTO/CIO in a listed pharma company, he felt that their service would be of interest to even non-US pharma companies as it may allow for management of compliance, proprietary data, etc. However, although he was on SAP, he did not seem eager to transfer to cloud in a hurry. Conclusion: for him the product was a ‘vitamin’ and not a ‘painkiller’. However this needs further validation with other companies.

In simple terms, cloud impacts OpEx and a normal Data Center impacts the CapEx. Based on the requirements, either of the two strategies could be used. Most CIO\CTOs I have talked to suggest a strategized approach to cloud. A few Indian companies I know actually stopped using cloud as the OpEx was prohibitively expensive for them.

What is the likelihood of Amazon providing the same services to end users in house and making 8k/others redundant?

This IMO is highly unlikely. Most product companies depend on implementation partners for implementing their products. This helps as implementation partners have better local connect with end customers. This is similar to having channel partners to sell your products in a particular area.

Who are the other approved vendors of these cloud providers?

This IMO is the important question. I believe most large Indian IT vendors could also provide these services. What 8k miles will bring to the table is a faster, more efficient and more experienced team. And, the fact that they are building up a suite of solutions which complement the cloud could help their end clients.

Disclaimer: Not Invested, Interested and still learning the business model

I tend to to agree with the article on valuations. It earned around 20cr last financial year as net profit.

Even if you take around 30-40cr as net profit for FY16 (taking the June quarter results as the base), I wonder if a market cap of 1,500cr is justified.

This is a fluid market and things can change rapidly.