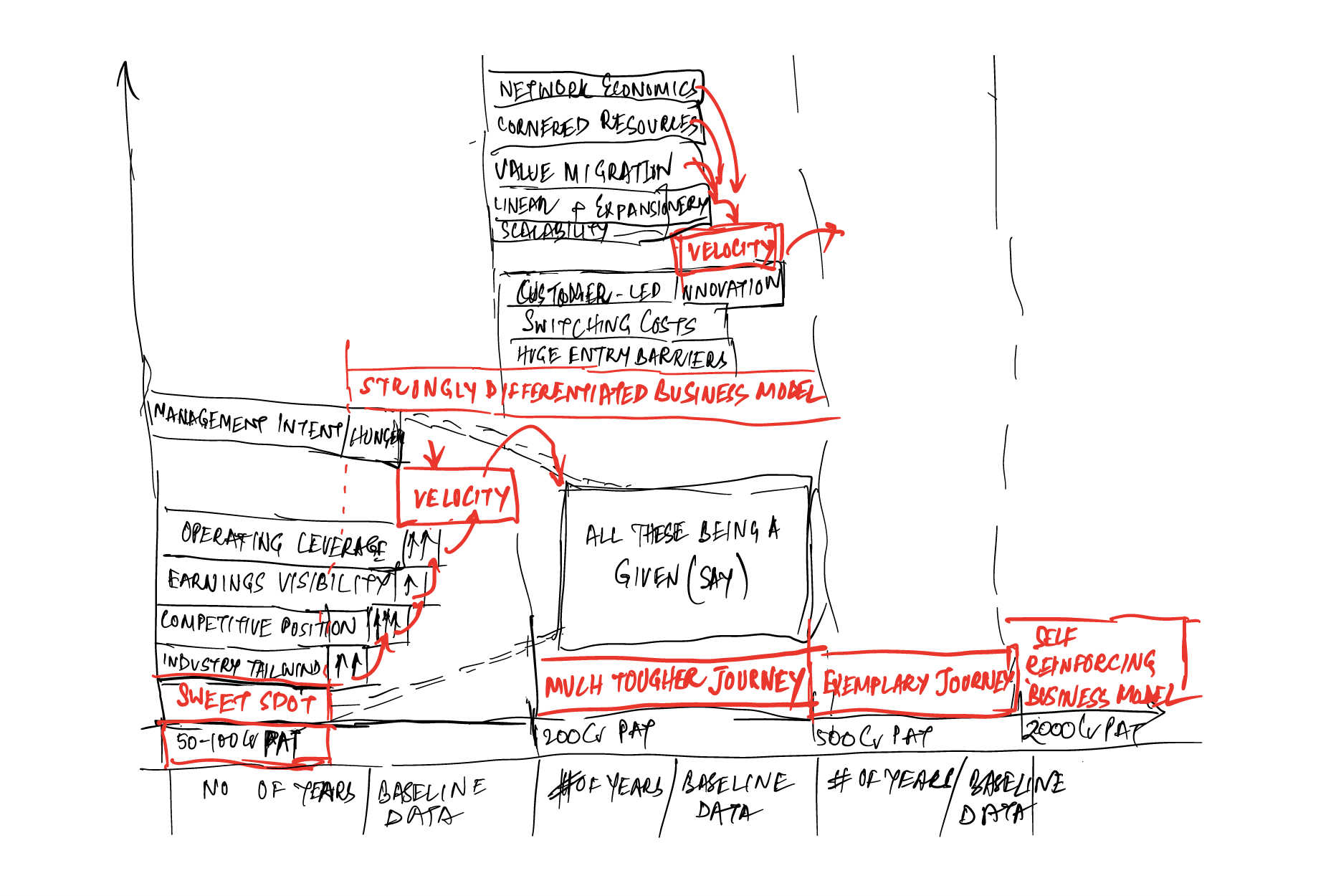

SCALABILITY THINKING #3 : Easy-Peasy in Hindsight

(most would counter legitimately), but can’t we be a little more prescient; a little more sure-footed, in our ability to Foresee !!

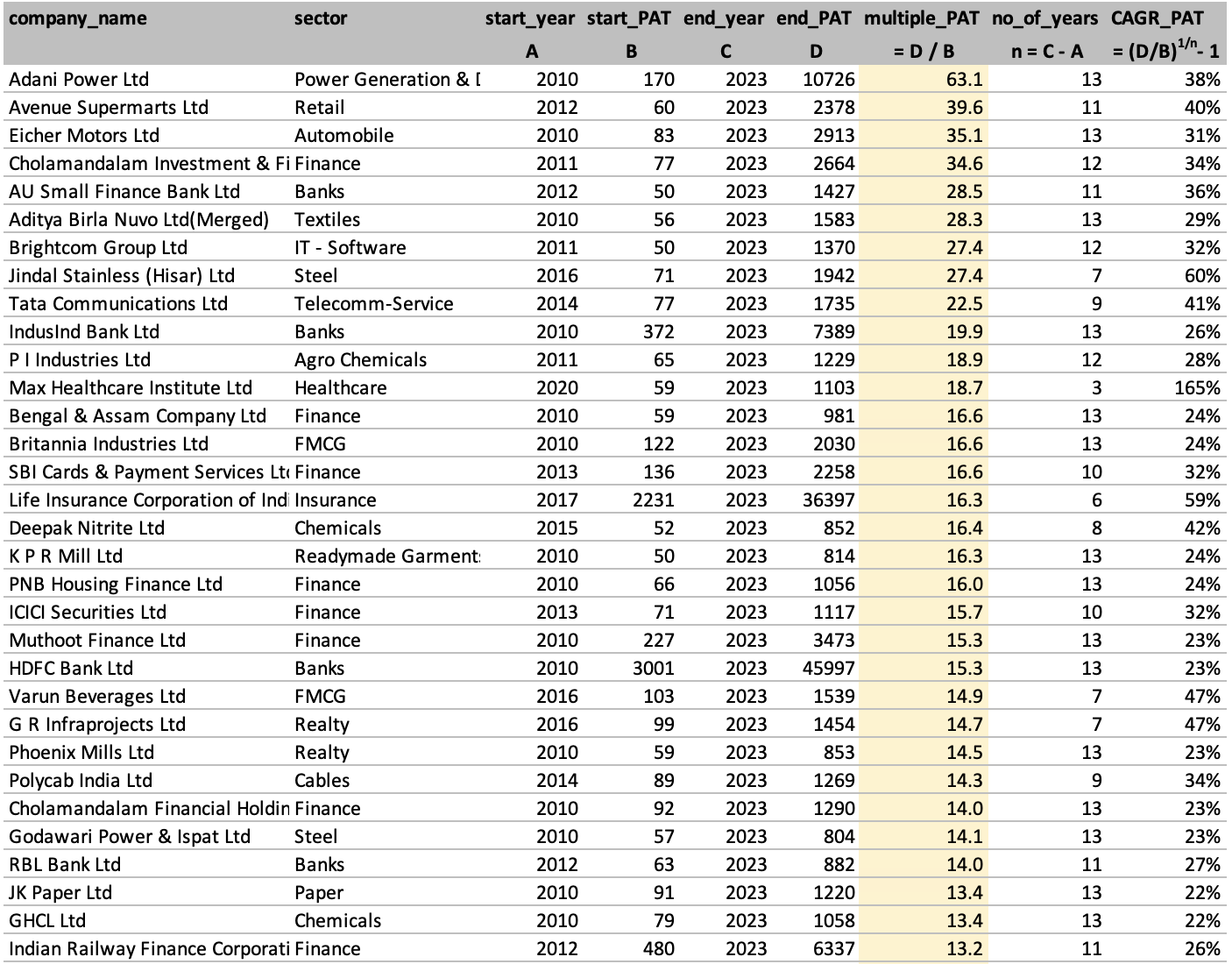

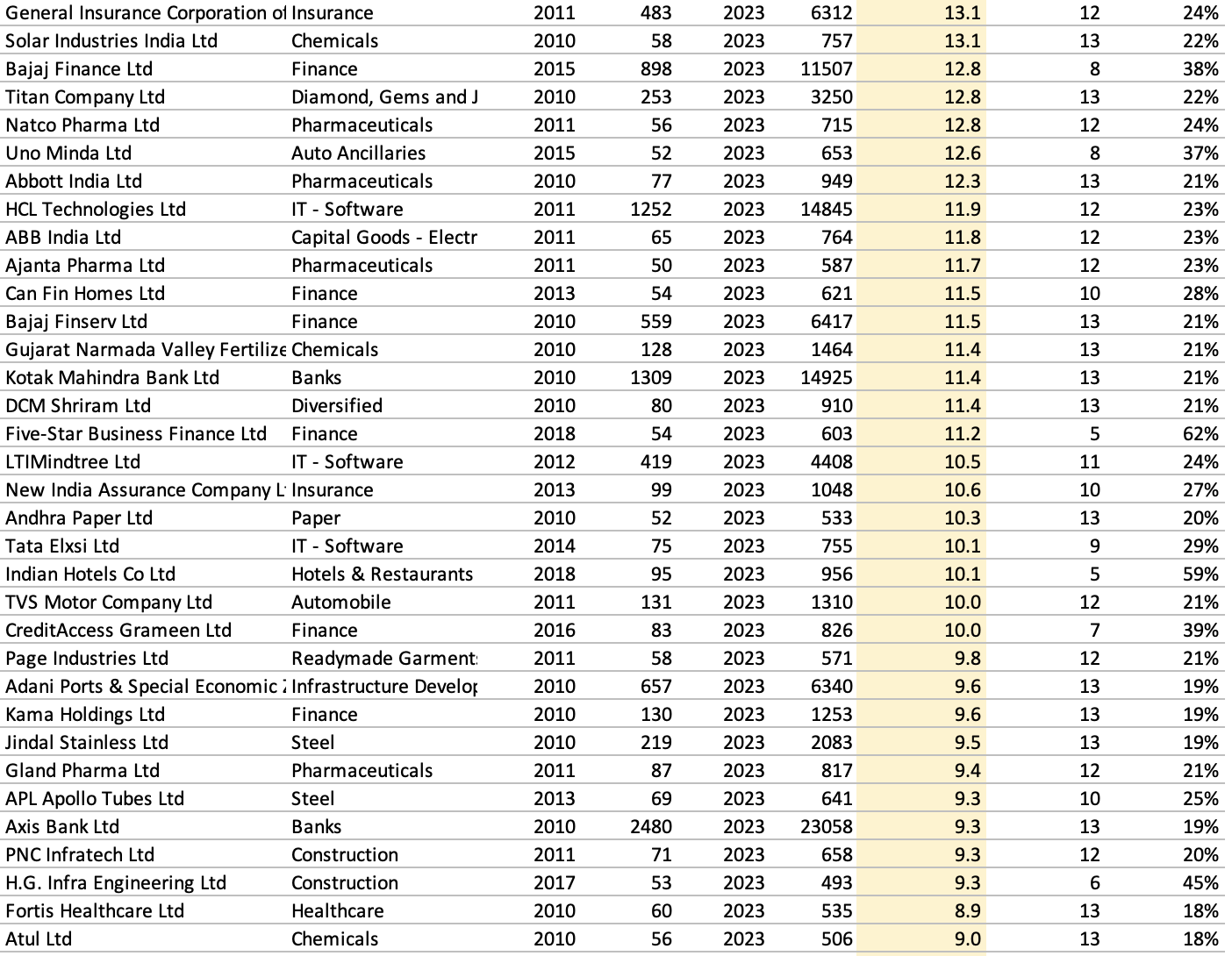

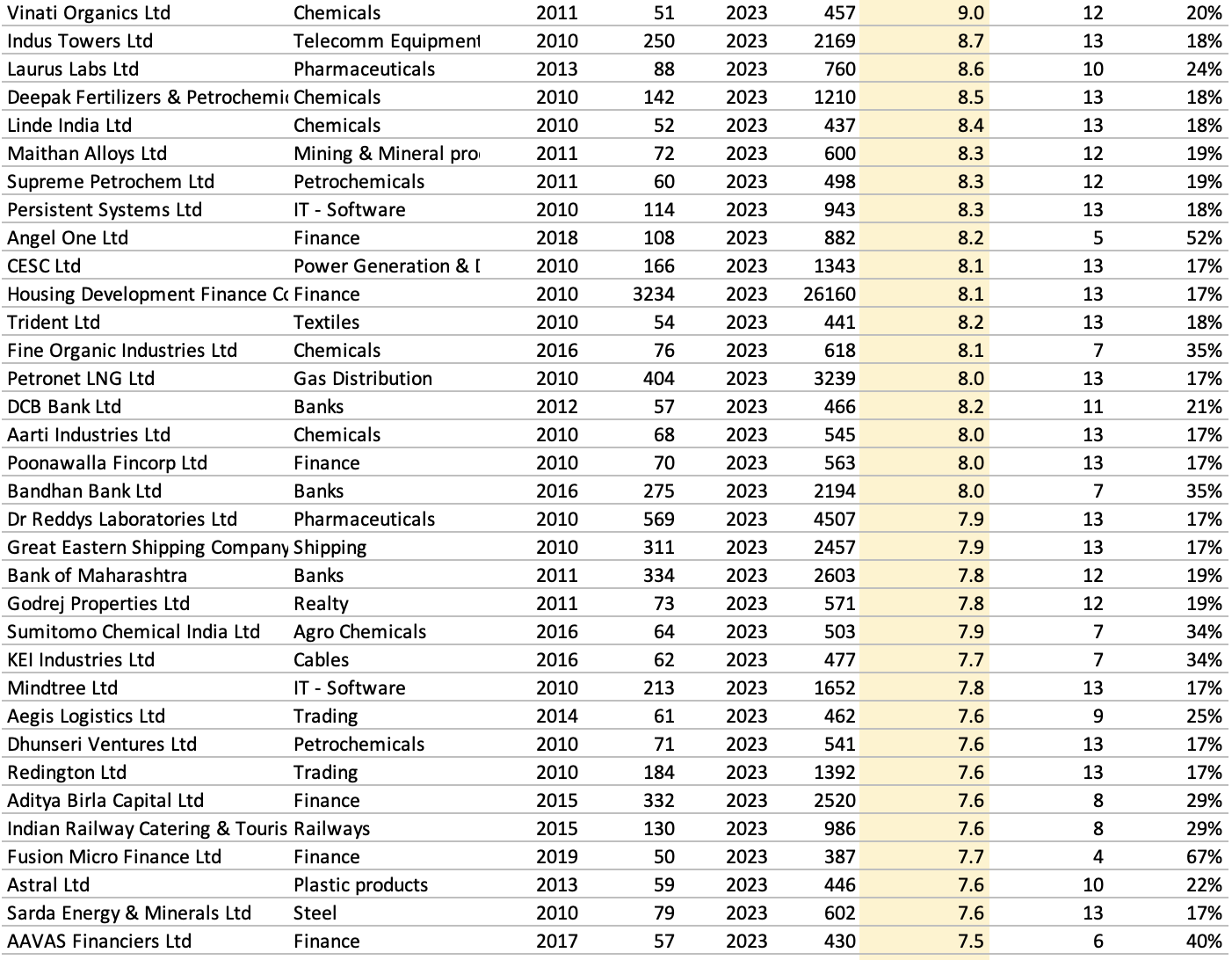

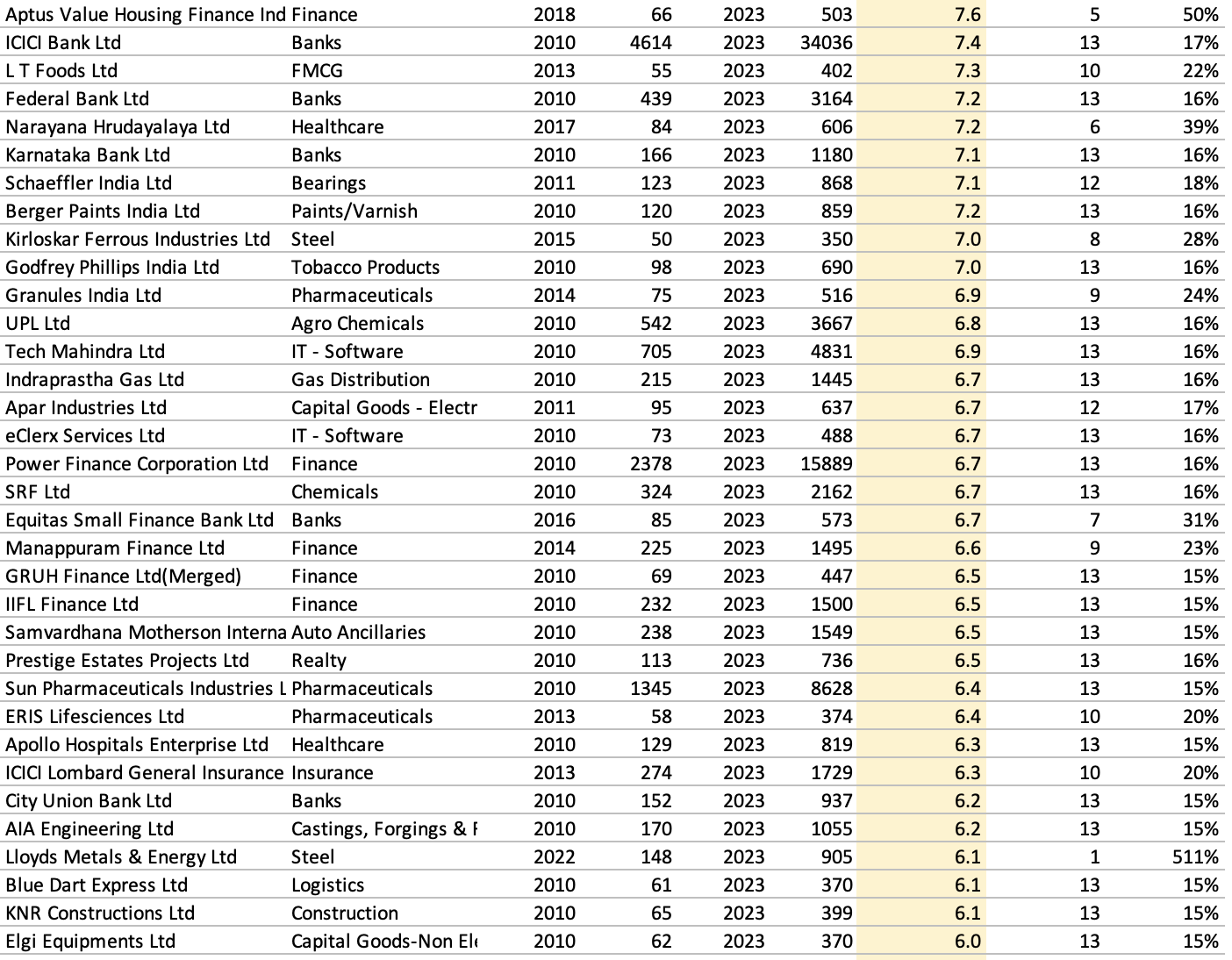

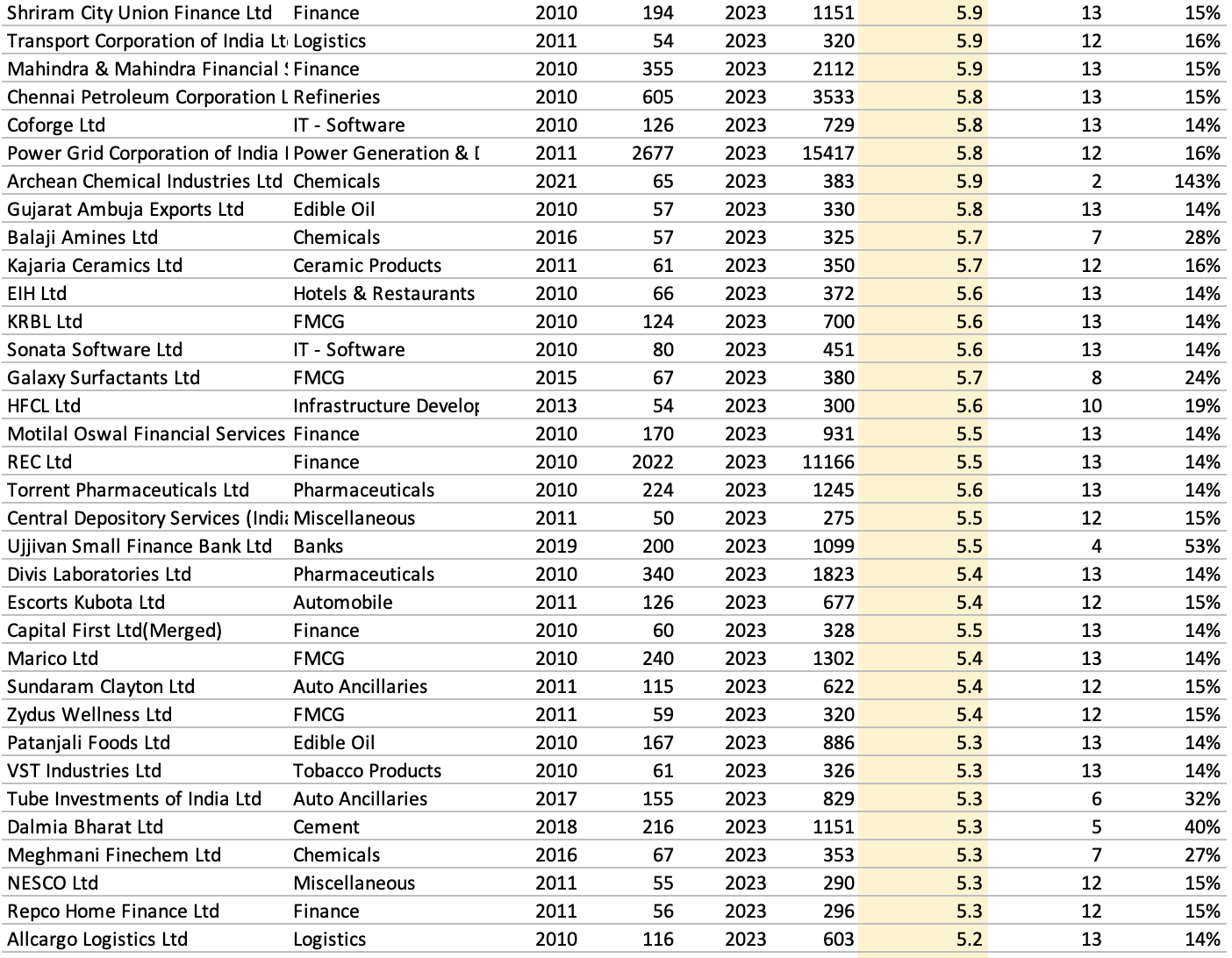

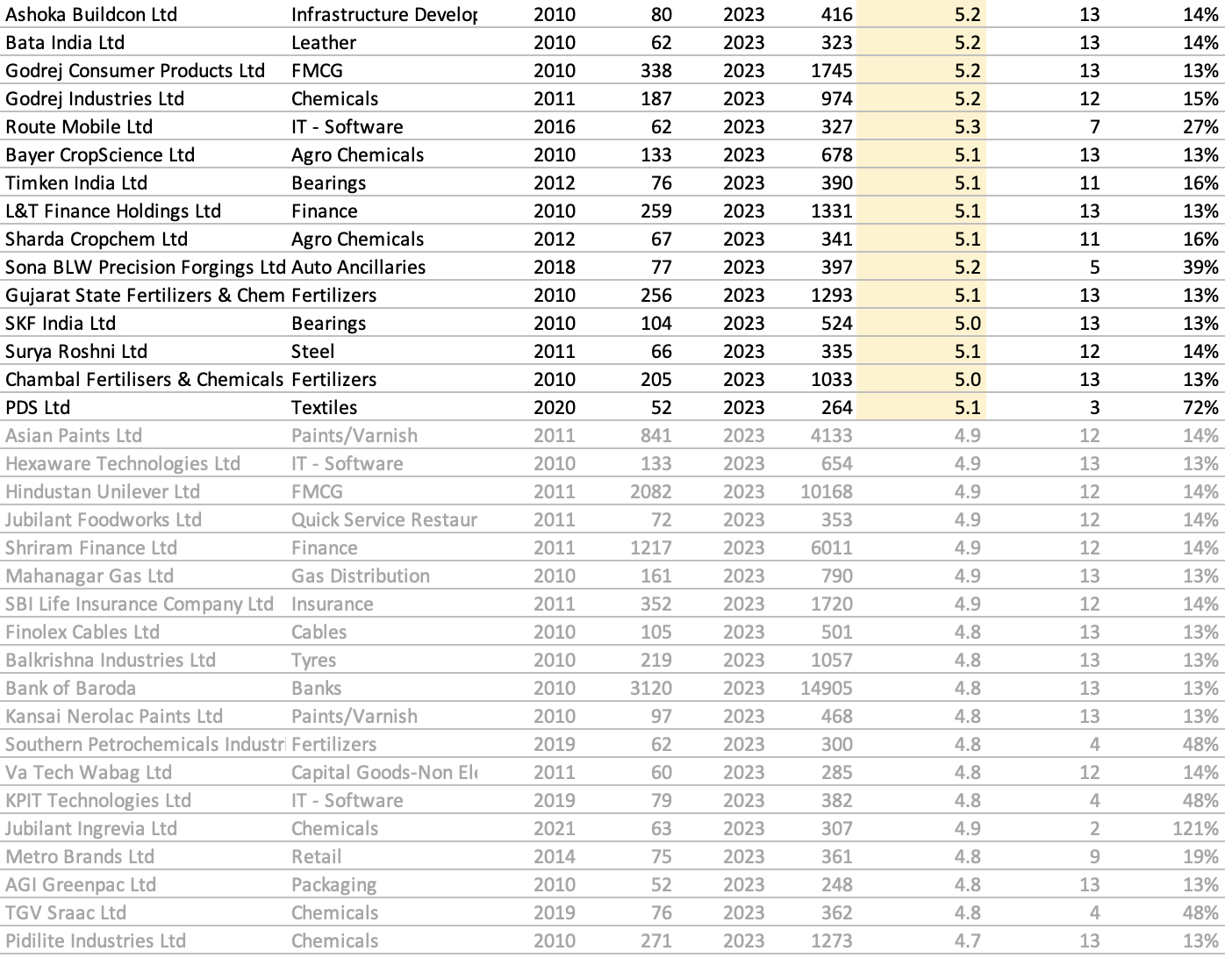

And this is where the whole conversations with my Mentors started getting REAL and INTERESTING. Meaning - I was able to transfer my excitement - almost everyone was getting it (as to where I was headed) - when I supplied the Commentary with the above picture. What was that Commentary.

Sure-Footed Patterns:

(All Senior Practitioners/Fund Managers I have interacted based on #2 agree there is a probable method to the madness lying there - for us to get a firmer grip on; at least 3 have offered to do more crunching and slicing/dicing of the data set of say last 15 years; and in the coming days will hopefully ADD more MEAT to this (sort of) intuitive discussion flow

All things being equal - let’s say 5 businesses have passed my (our) thresholds, are there parameters that SWING THE NEEDLE the MOST and this give me a better handle on investment decision-making/allocations strategy?

We now bet, there is (and in this pre-set order, too perhaps) (Sticking our necks out again  )

)

- If there is strong Industry Tailwind, AND

- The business is improving its Competitive Position (gaining market share), AND

- There is evidence of Operating Leverage at Play (coming in), AND

- We have a great sense of Management INTENT/HUNGER (where do they want to take the business), AND

- We can clearly see Value Migration happening within 2-3 years

- No of variables that can go wrong

More often than NOT (again given all things being equal- all selected business passing all/most of our thresholds) the business that scores higher (qualitatively and quantitatively) on these, the ODDS of success are higher.

We hope to be able expand on these with combined collaborative power, as we delve more through our own example sets. Each case will be different perhaps. Every Industry like say IT or Finance will bring its own nuances; Processing/Manufacturing bring on a different set? A multiplicity fo factors at play, and we make bold to come back to you with more simple, powerful and abstracted patterns as the above 5 that in our intuitive understanding - swings the needle the most!

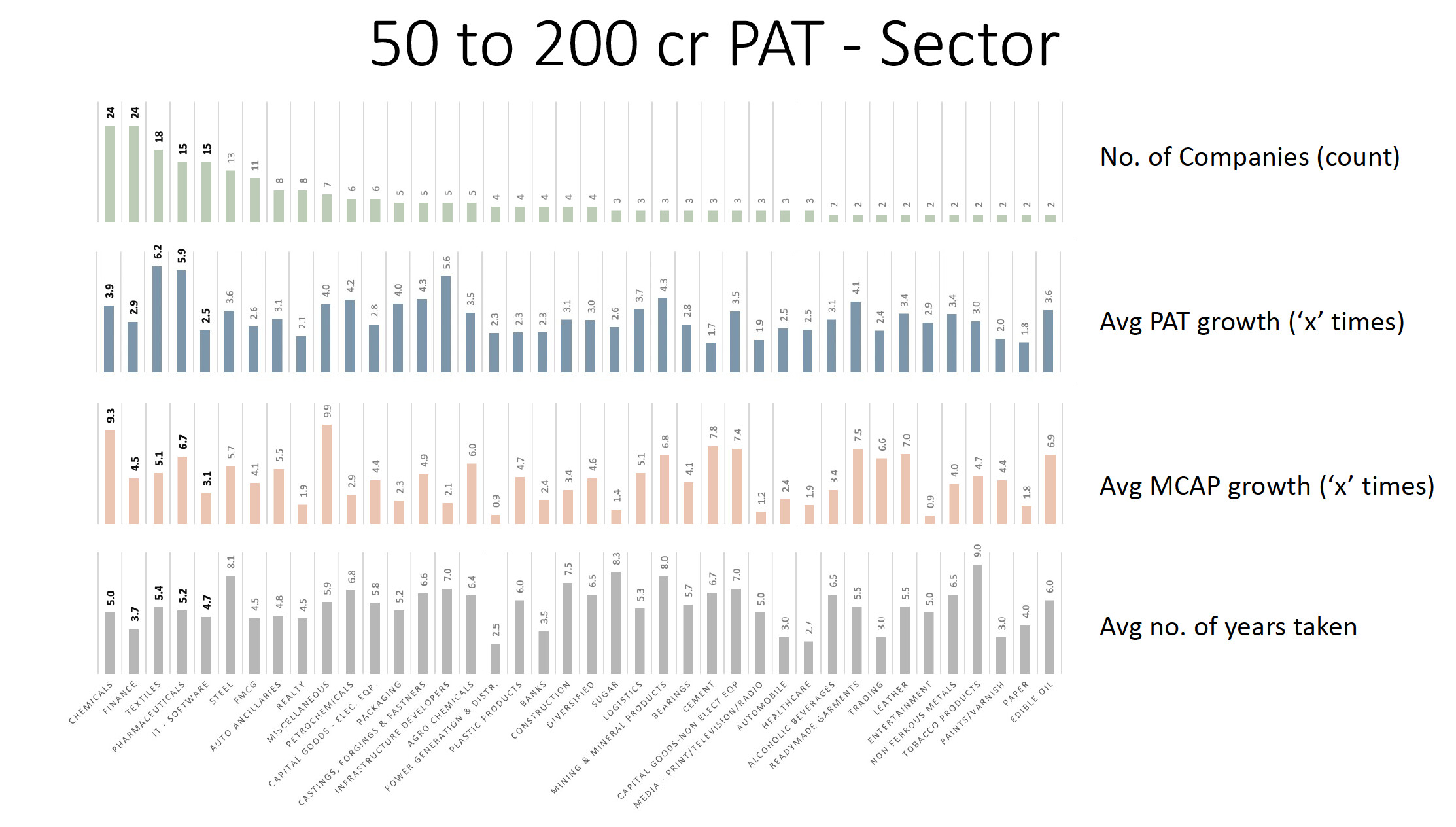

As we progress to slicing and dicing and playing with the rich data-set, we should find that

a) Scaling up from 50-100-200 Cr is far easier

b) #No of businesses crossing these thresholds will be larger by far, than

c) 200-500 Cr is another beast altogether - tougher and many more factors probably play definitive role

d) Management INTENT is probably V Important from here on (probably most decisive factor?)

e) Needless to say higher PAT levels from 500 Cr to 1000 to 2000 Cr gets tougher and tougher and the numbers shrink too

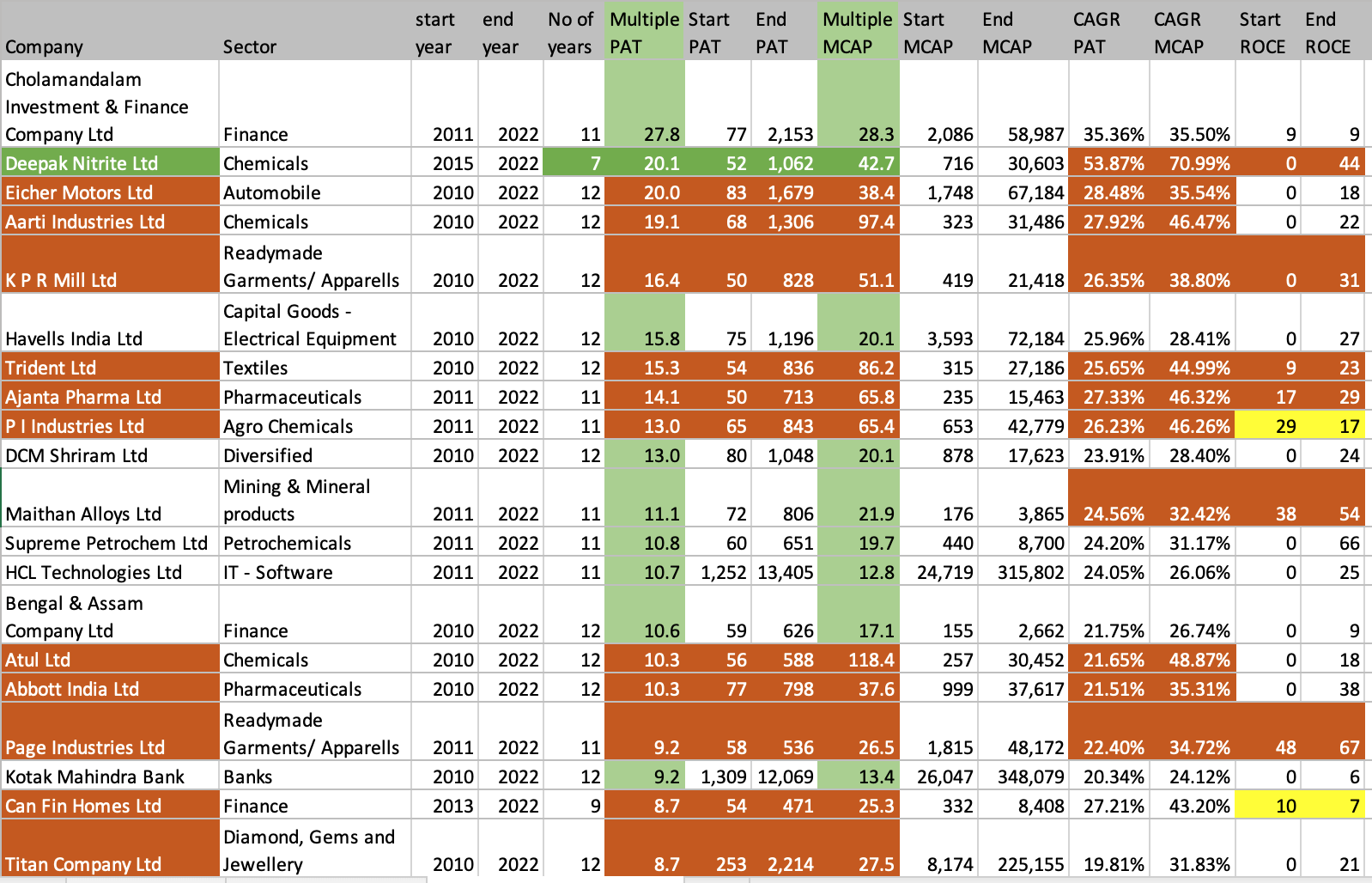

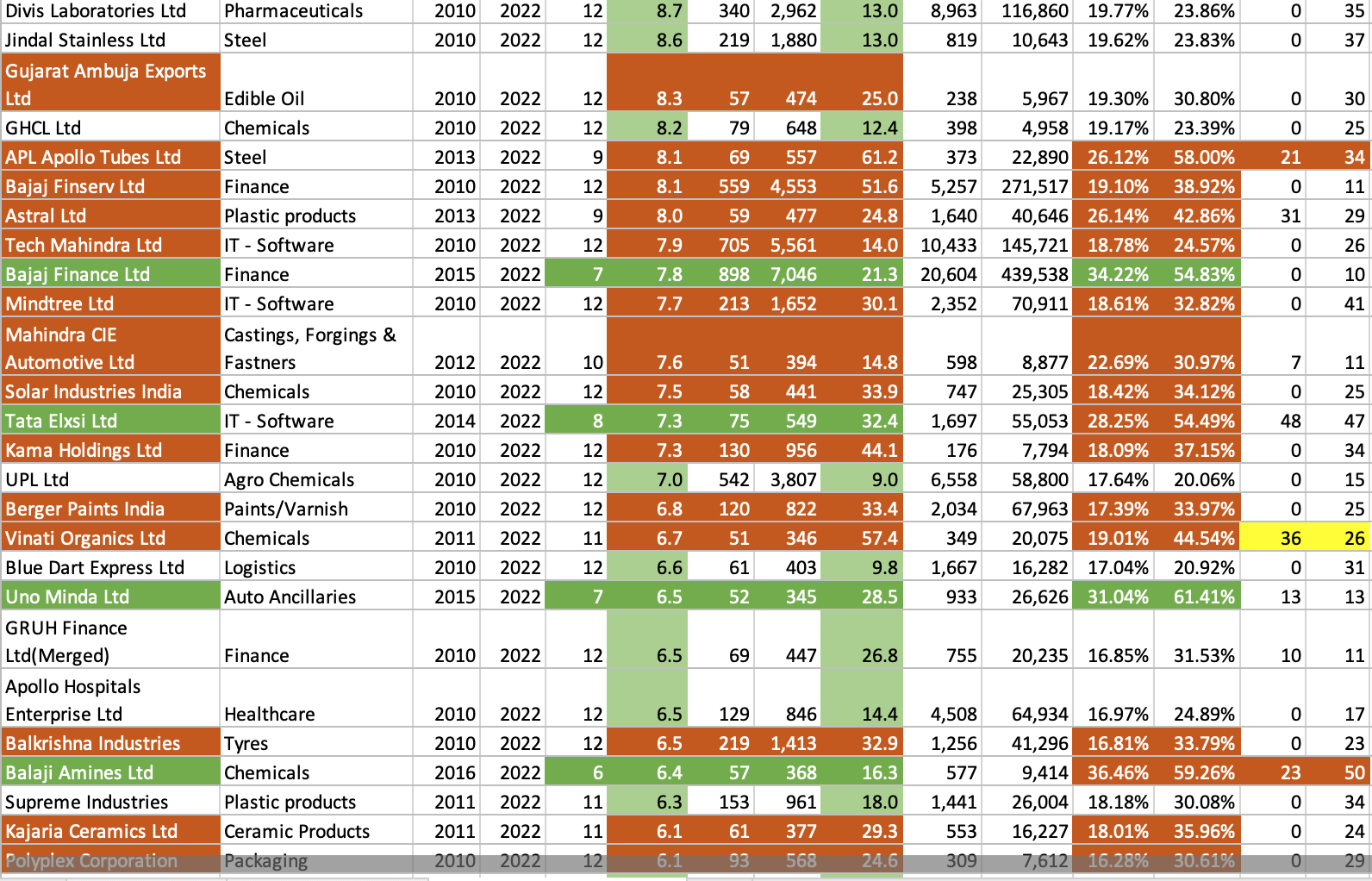

From my current set of examples - I can probably say with confidence that a Shivalik Bimetals (~75 Cr PAT), HBL Power (~100 Cr) and an Usha Martin (~350 Cr) will have a relatively easier time than say a Gujarat Fluorochem (~1300 Cr) to consistently keep scaling up from here for next say 3-5 years.

Gujarat Fluorochem has done exceedingly well in a complex playing field where far too many things change dynamically will probably cross 2000 Cr easily but for it to scale form 2000 Cr to 4000 Cr - we will need to frame the right questions to breakdown - what will GFL Mgmt need to aspire for/invest/and execute v well to cross that ? And seek the answers for that from Management as well as our grounds-up research.

What are your examples from your data-sets, and how can we go about thinking better and breaking down scalability thinking for your businesses of interest??