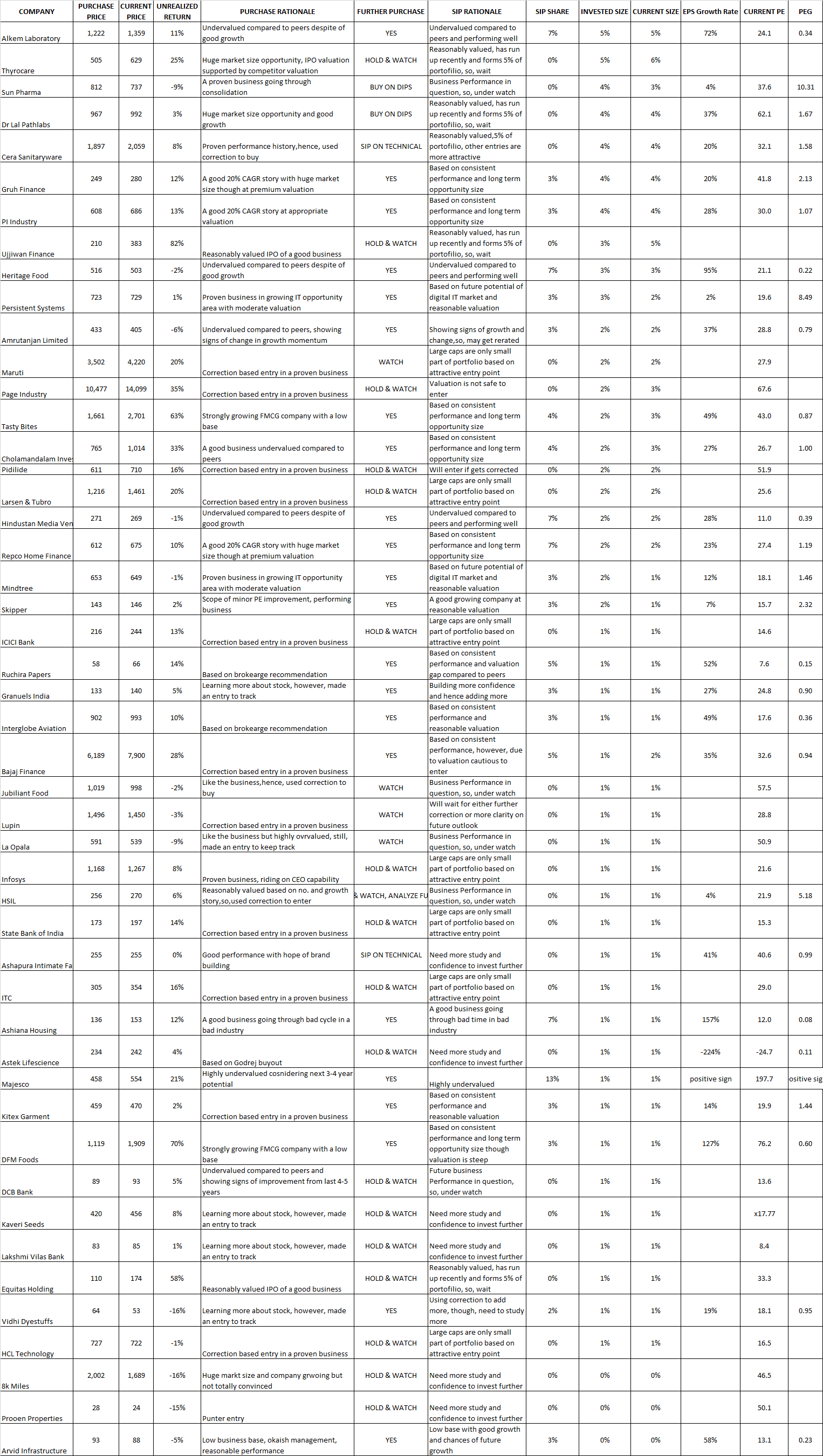

Hi All,

Have been invested in direct equities for past 6 months using market correction as entry point. With rising confidence, building a portfolio for 10 years. Though have picked up lot of stocks, idea is to get some quantity to keep tracking them and study more about them to build further conviction. However, would like to see list of 49 stocks reducing to 20-25 in next one year.

Would need your guidance, suggestion and feedback on my SIP/regular investment rationale, plans and how to consolidate, point out stocks which do not make sense and other valuable suggestions:

SIP Share : Distribution of Capital for next 3 months of SIP

Invested Size : Invested Portfolio Distribution

Current Size : Current Portfolio Distribution

It is possible to view the portfolio with some difficulty. But @suru27, 47-49 stocks at individual level is too much, its more than a mutual fund scheme. IMHO, even 20-25 is on a higher side, if you plan to properly track the stocks.

I dont know how you identify a stock. Suggest you to go thru the depth of discussion provided in many of stock stories in this forum. It is the collective brilliance of the vibrant forum members who dive deep, look for the red flags, green shoots & what not and provide a holistic view of a company. It has been a personal experience to read, opine, discuss, contribute and learn. Can you dig so deep for each of the stocks? Well, you must not be doing anything else then (business/job etc) for living .

Reasons I would like to have 20-25 stocks in portfolio:

Not comfortable having too concentrated portfolio of 8-10 (based on past experiences, may be , I am not able to build that level of conviction)

Can do SIP (do not have large bulk amount to put and hence building portfolio sslowly). So, the problem with having too few stocks is if some of them run up too fast and I am not comfortable buying as SIP, then, I do not know where to invest. So, kitty is little big to keep getting opportunity among this basket

I would like to track these 20 stocks on regular basis and if performance in-line, then, not much digging deep but if things go wrong, then, will take a deeper look for hold or exit decision

Now, penning down thoughts behind buying these stocks.

I Understand Business and comfortable to do SIP based on current valuations (18):

Ideally, there are 18 stocks which I have read in some detail and would continue doing SIP

Alkem Laboratories

Majesco

Hindustan Media Ventures

Heritage Food

Cera Saniatryware

PI Industries

Mindtree

DFM Food

Amrutanjan

10.Persistent System

11.Skipper

12.Kitex Garment

13.Interglobe Aviation

14.Gruh Finance

15.Cholamandalam Investment

16.Tasty Bites

17.Repoco Home Finance

18.Ashiana Housing

I Understand Business, purchased in past but not comfortable to do SIP based on current valuations(4):

Page Industries

Thyrocare (working further to comapre with lalpath labs and move to 3)

Dr. Lalpath Lbas

Bajaj Finance

Scripts which have gone wrong and not doing well and in hold stage (3):

Sun Pharma

Jubiliant Foodworks

HSIL (Can move this money to cera)

One Time Purchases: I purchased this as a one time purchase as risk reward ratio due to price correction looks very favorable (8): These are mostly large cap stocks purchased at price points where chances of loss were low,so, I intend to just hold them as it is without further addition or offloading for next few years (On this a 10-15% return with a low beta expectation, in long run this would be hardly 10% of my portfolio)

ITC

L&T

Maruti

SBI

ICICI

Lupin

HCL Technology

Infosys

IPO Valuation was attractive and hence invested

(One time

Equitas Holding

Ujjivan Finance

I purchased in small quantity to build further conviction for entry or exit (out of sight is out of mind for me)/buy with right valuation (10). May be as I already have 18 stocks in my SIP list, i should sell these and exit completely until I get questions/insights on why some of those 18 stocks do not make sense and these stocks at current valuation are better and can replace some of the 18 stocks in my SIP list

La Opala

Ashapuram Intimate

8k Miles

Lakshmi Vilas Bank

DCB

Kaveri Seeds

Vidhi Dyestuff

Granuels

Ruchira Papers

Astec Lifesciences

Now awaiting your and other seniors comments, specifically to those 18 stocks I have mentioned at the top.

I understand looks like a complicated and confusing portfolio, hence, looking for help to simplify

Please do a rating on all the stocks on a scale of 1 to 5…for following parameters 1. Growth till now 2. Management quality 3. Size of opportunity for growth 4. Current valuation … the rating will help to eliminate a few stocks and focus on stocks which u feel better

I think you are on the right track and need to build your conviction yourself. No need for confirmation from any “seniors” – only you are responsible for your money and strategy. You say you have started investing in direct equities in the last 6 months but based on your responses and portfolio, it seems you have been tracking markets and know enough about portfolio sizing, entry points, valuations etc

Most important thing to keep in mind is the promoter quality so there are a couple of companies in your portfolio which look speculative to me. Do study past actions of the promoters and think if they are friendly towards minority shareholders, are not crooks etc

I would just ask you to do the following:

create a separate physical folder for each of your investments and note down why you have invested in a company – is it attractive valuation,future growth, any catalysts you foresee etc

keep updating with related news articles, quarterly earnings reports, management interviews, your thoughts on how you see the company progressing, whether you would buy the company at cmp if given an option…

when in doubt or when stock falls, go back to your notes and read them

As long as you can keep learning in the markets, not make any stupid speculative decisions, keep learning from your mistakes and have a long term bias – you are set on a path of success.

All the best.

Skipper has been doing pretty good in its business and also has a promising orders in hand, which are capable enough to take the company to better valuations.

Pls refer to the attachment for some clues.Skipper .pdf (408.9 KB)

Thanks for that info @krpwn1516. I think what is lacking for is company is brand positioning. Look at what astral did. I think a strong brand ambassador and good or can do wonders for this company, i.e. in the PVC segment

Thanks. Point noted and now a maintain folder for stocks with reqd. doc. Yes, I was in the market but due to shift in career, had to be completely out of market and reply more on mutual funds. however, as I have bandwidth available now, rebuilding my portfolio with a small % allocated to equity which I am slowly increasing.

The historical performance analysis is almost automated. Now, I am looking to use technology to automate quarterly tracking of these companies.

The reason for investing in skipper are following:

Financially, one of the most well maintained company in list of infrastructure pack

Strong historical growth in revenue and profitability

Available at discount compared to no. 1 player despite of maintaining comparative healthy financials

Visibility in growth areas based on management guidance and historical execution capacity

Management’s intent to reduce debt while expanding revenue and profitability

Improvement in key financial ratios

Key concern areas:

Based on last 3 years trend, increase in accounts receivable is 26% higher than growth in sales

Cautionary stand on current liabilities and related parameters

Granules, I have taken a marginal entry based on preliminary understanding of good basics, however, yet to take a long term decision based on future study. That is the approach I am following when I see an interesting company and currently sum of all such companies are less than 10% of portfolio and none of them more than 1% of my portfolio individually

Though I never tracked any of these companies, kwality and arvind never came to my radar because of few rules which I follow for stock selection . One of them is low debt or signs/possibility of intent to reduce debt. Kwality and Arvind were always out because of this reason. It is more of a personal choice to avoid risk.however , in dairy , I am invested in heritage though I understand current andhra telangana split can have major negative impact . Still, I believe this one of the reasonably placed bet any relatively attractive valuation in dairy space . Positive triggers are : continued growth in value added dairy products, signs of turnaround in retail business, jv in pipeline for value added business, successful expansion in other states though difficult due to local dairy brand factor, chances of catching up to peers in ,. Concerns : political risk affecting growth in core geographies , extended retail business breakdown

Hi @suru27 , yes I agree, hence my scepticism to enter Arvind, despite believe i growth prospects,

Regarding Heritage, I have a very small stake. I entered primarily due to low valuations and stamp of approval from Vijay Kedia

But of late, I have had my doubts, some based on the points u pointed out and on a very peculiar stance of Heritage. They say they want to hive off their retail segment eventually, yet they continue to expand very aggressively and rapidly. This strategy sounds very absurd to me. Why would you pour more money to expand a loss making entity just to sell it off?

Also, you were mentioning something about a JV, could you please shed some light on that?

Can you throw light on hive off retail business in case it was communicated by management. The JV stuff is mentioned in con call transcripts though they have not disclosed details.

.

.