Little curious, does it mean starting their own e-commerce venture (looks like) or to ride e-commerce boom because I have used groffer in bangalore and heritage retail is one of retailers on grofer’s platform. Is this what they mean by generating 10% of revenue through e-commerce ?

https://www.heritagefreshonline.com/ I hope this answers ur question

1 Like

thanks a lot, was not aware of this.

No problem that’s what this forum is for …to help each other. Anyways, now I m in a dilemma. I really believe in the growth potential of their agri and dairy business but dislike their retailing ambitions, on or offline.

So, waiting to make a decision whether to exit or pile on more…

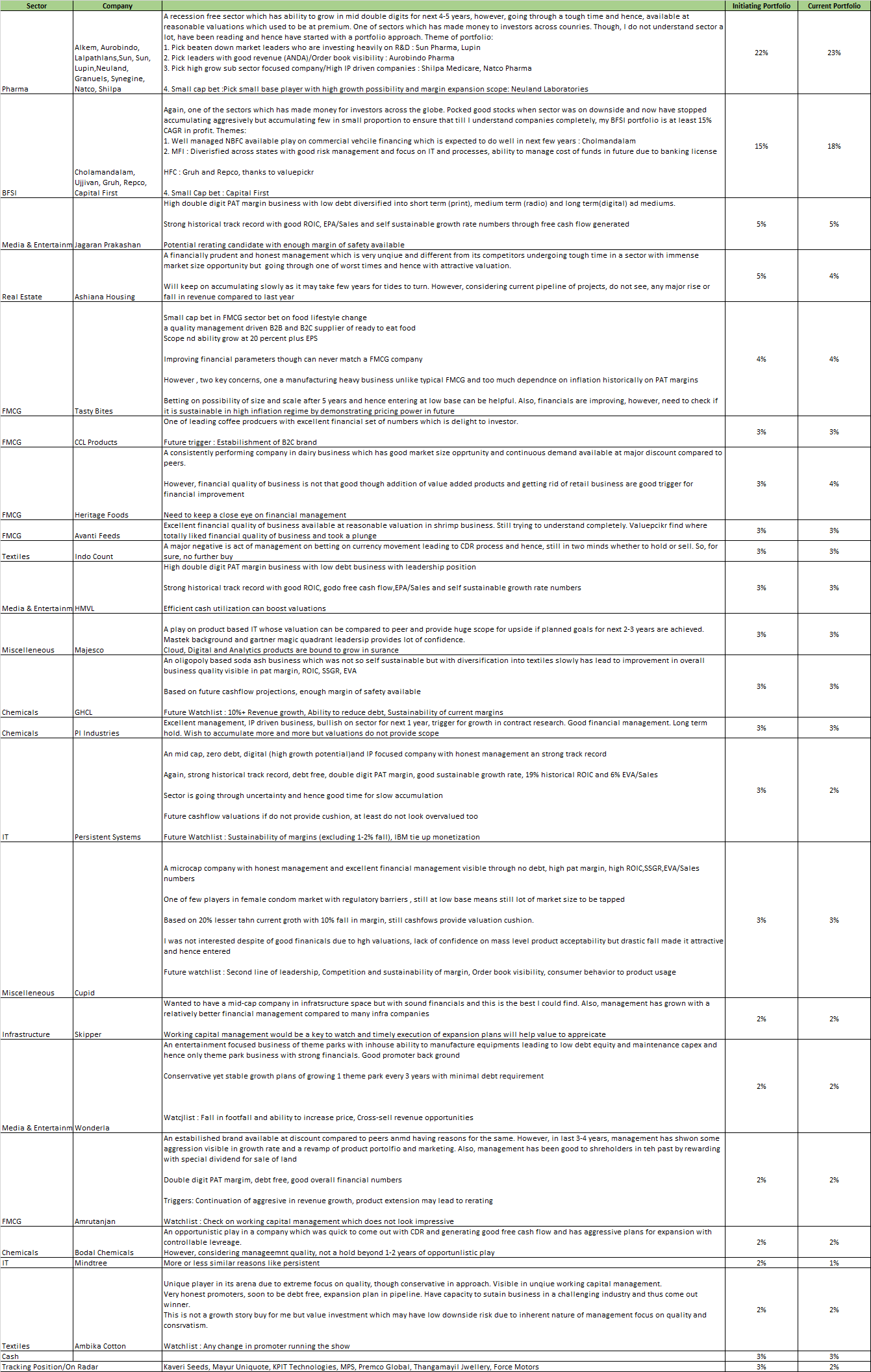

Please double click on image below to zoom and read

Hi All,

Thanks @Advait_6270 @svsrikanth @bhaskarjain for your suggestions. Has helped me to work on portfolio in last 3 months.

Used to have 50+ companies in my portfolio whcih I have been able to bring down to 21

Few points:

-

I need to understand pharma and BFSI sector in detail. Till that time, I will be following a mutual fund approach for these 2 sectors and hence considering each of these 2 sectors as a unqiue stock as I am very much sure of long term wealth creating potential of these two sectors (have been continuously reading so that can understand but it is WIP)

-

The common theme for investments are:

a. Double digit growing businesses with low debt, double digit PAT margins, low debt, stable cash flows, lower need of financial capital to grow with visible cashflows and healthy leverage, ROE, ROIC,SSGR, EPA parameters providing decdent yield and cashflow based valuation comfort

b. Market leaders, Investors delights going through a tough time/sector going through tough time

c. Companies with small base in sectors with immense market size opportunity for identifying multi X bets

Current Portfolio:

Exits/Ideas discarded : Reaons for the same:

- To steep valuation:Cera,Page Industries, Pidilide, Jubiliant food, DFM food

- Lack of conviction on managemnt or ability to grow: Kewal kiran, DCB Bank, 8K Mles, Prozone, Vidhi Dye, Ashapura Intimates

- Not a business which can be rewarding to investor (capital eating/working capital heavy etc.): Indigo, HSIL

- Not fit in mid-cap portfolio : L&T, SBI

- Too much commodity play without any MOAT: Ruchira papers

Watch list/waiting for right price : La Opala, Mayur Unqiuotes, Symphony

Things I have started doing:

- Maintain separate folder for each stock with annual reports, qtr result, research report, concall transcripts and related articles

2 Go through documents mentioned above

-

Build a stock scoring framework

-

Build a valuation framework

-

Read , read and read threads of valuepickr. Its ton of knowledge specially art of valuation and capital allocation therads

-

Read at least 1 investment book every month. Finshed 4 in last 3-4 months from list shared on valuepickr

Note : All of the stocks have been purchased in last 3-6 months

Disclaimer: None of the stocks are for recommendation and these are just my personal views.

Awaiting your suggestions and comments. @hitesh2710 Hitesh jee, as suggested on Kunj’s thread, have tried to document my rationale for purchase. Please provide your valuable feedback.

2 Likes

I cant read what u have put up. I think you would have to put up things in a more clear version so that it becomes easy to read.

Hi @hitesh2710 Hitesh Jee,

Posting investment rationale below:

-

Jagran Prakashan (5% at 178 Rs)

High double digit PAT margin business with low debt diversified into short to medium term (print), medium to long term (radio) and long term(digital) ad mediums. Strong historical track record with good ROIC, EPA/Sales and self sustainable growth rate numbers through free cash flow generated. Potential rerating candidate with enough margin of safety available

based on free cashflow valuation -

Ashiana Housing (5% at 160 Rs)

A financially prudent and honest management which is very unique and different from its competitors undergoing tough time in a sector with immense market size opportunity but going through one of worst times and hence with attractive valuation. Will keep on accumulating slowly as it may take few years for tides to turn. However, considering

current pipeline of projects, do not see, any major rise or fall in revenue compared to last year -

Tasty bites (4% at 2400 Rs)

Small cap bet in FMCG sector bet on food lifestyle change. A quality management driven B2B and B2C mix business for supply of ready to eat food/ingredients. Scope and ability grow at 20 percent plus EPS. Improving financial parameters though can never match a FMCG company. However , two key concerns, one a manufacturing heavy business unlike typical FMCG and too much dependence on inflation historically on PAT margins. Betting on possibility of size and scale after 5 years and hence entering at low base can be helpful. Also, financials are improving, however, need to check if it is sustainable in high inflation regime by demonstrating pricing power and better cost contract management in future -

CCL Products (3% at 262 Rs)

One of leading coffee producers with excellent financial set of numbers which is delight to investor. Improving financial levers. Low cost producer of good quality. Future trigger : Establishment of B2C brand. Reasonably valued at current levels though does not provide enough cushion, from a long term holding perspective , should do good and any fall would be an accumulation opportunity provided assumptions are intact -

Heritage Food (3% at 515 Rs)

A consistently performing company in dairy business which has good market size opportunity and continuous demand available at major discount compared to peers. However, financial quality of business is not of best breed, though addition of value added products and getting rid of retail business are good trigger for financial improvement. margin improvement already happening due to higher mix of value added products. Need to keep a close eye on financial management -

Avanti Feed (3% at 543 Rs)

Excellent financial quality of business available at reasonable valuation in shrimp business. Still trying to understand completely. Valuepcikr find where totally liked financial quality of business and took a plunge -

Indocount (3% at 856 Rs)

One of leading bedsheet exporters with improving financial ratios, falling debt equity, good double digit margins available at at pe of 12. Expansion of production capacity and b2c entry can be triggers. However, 10 years back promoters messed up trying to play with currency and hence still in 2 minds with this stock -

HMVL(3% at 275 Rs)

High double digit PAT margin business with low debt business with leadership position. Strong historical track record with good ROIC, good free cash flow,EPA/Sales and self sustainable growth rate numbers. Efficient cash utilization can boost valuations. Very low downside and major upside opportunity. -

Majesco (3% at 521 Rs)

A play on product based IT whose valuation can be compared to peer and provide huge scope for upside if planned goals for next 2-3 years are achieved. Mastek background and gartner magic quadrant leadership provides lot of confidence. Cloud, Digital and Analytics products are bound to grow in insurance -

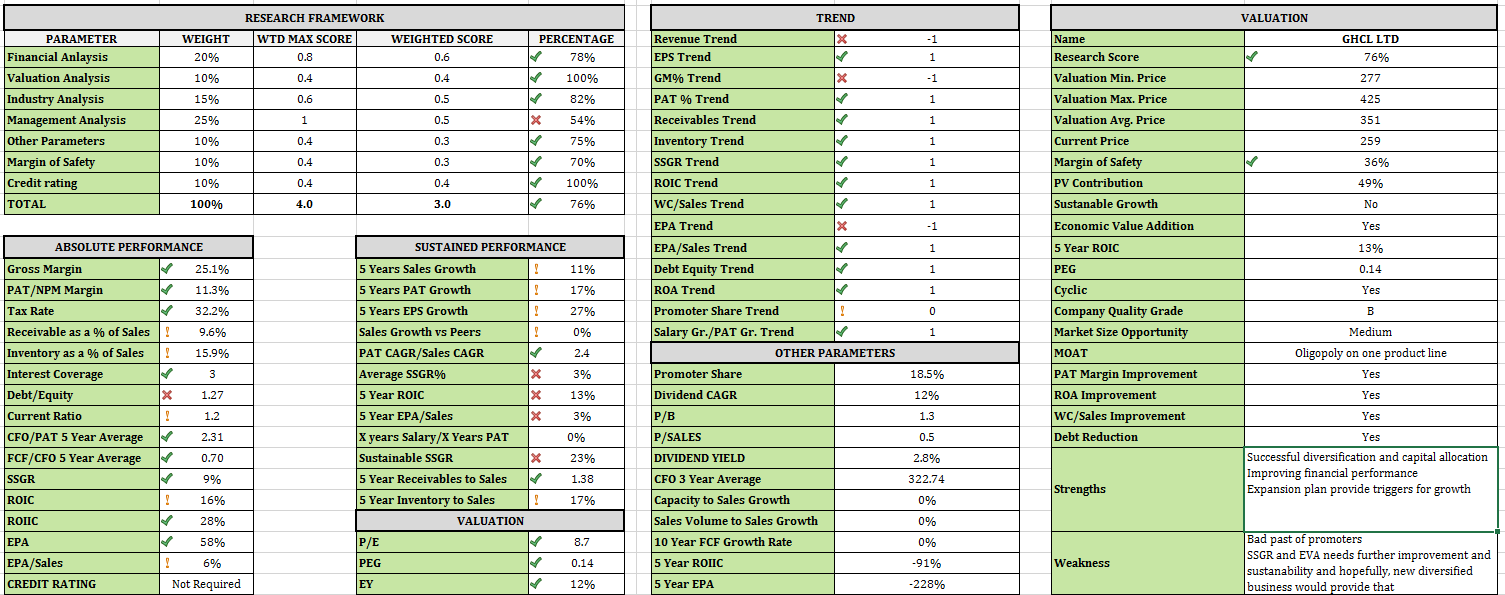

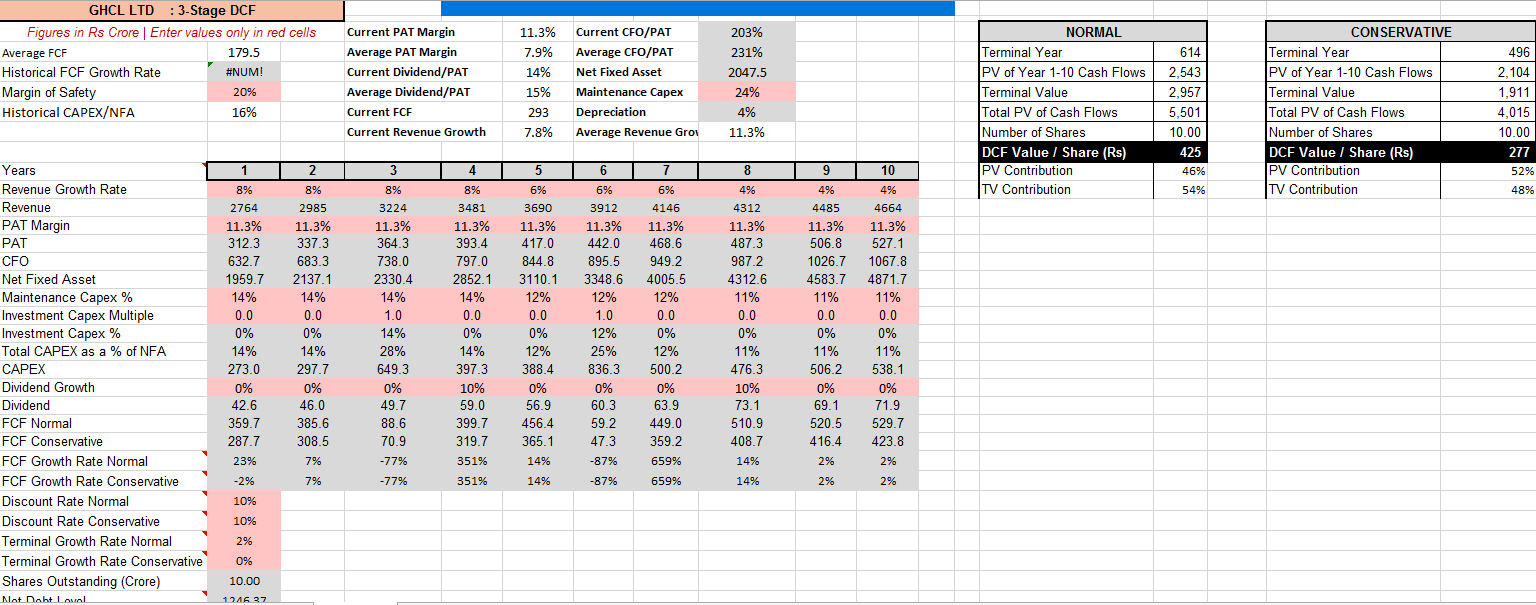

GHCL (3% at 205 Rs):

An oligopoly based soda ash business which was not so self sustainable but with diversification into textiles slowly has lead to improvement in overall business quality visible in pat margin, ROIC, SSGR, EVA. Based on future cash flow projections, enough margin of safety available. Future Watch list : 10%+ Revenue growth, Ability to reduce

debt, Sustainability of current margins -

PI Industries (3% at 680 Rs):

Excellent management, IP driven business, bullish on sector for next 1 year, trigger for growth in contract research. Good financial management. Long term hold. Wish to accumulate more and more but valuations do not provide scope -

Persistent System (3% at 590 Rs)

A mid cap, zero debt, digital (high growth potential)and IP focused company with honest management an strong track record. Again, strong historical track record, debt free, double digit PAT margin, good sustainable growth rate, 19% historical ROIC and 6% EVA/Sales. Sector is going through uncertainty and hence good time for slow accumulation

Future cash-flow valuations if do not provide cushion, at least do not look overvalued too

Future Watch list : Sustainability of margins (excluding 1-2% fall), IBM tie up monetization -

Cupid (3% at 288 Rs):

A micro cap company with honest management and excellent financial management visible through no debt, high pat margin, high ROIC,SSGR,EVA/Sales numbers. One of few players in female condom market with regulatory barriers , still at low base means still lot of market size to be tapped. Based on 20% lesser than current growth with 10% fall in margin, still cashfows provide valuation cushion. I was not interested despite of good financials due to hgh valuations, lack of confidence on mass level product acceptability but drastic fall made it attractive and hence entered

Future watch list : Second line of leadership, Competition and sustainability of margin, Order book visibility, consumer behavior to product usage -

Skipper (2% at 147 Rs):

Wanted to have a mid-cap company in infrastructure space but with sound financials and this is the best I could find. Also, management has grown with a relatively better financial management compared to many infra companies. Working capital management would be a key to watch and timely execution of expansion plans will help value to

appreciate -

Wonderla(2% at 410 Rs):

An entertainment focused business of theme parks with in-house ability to manufacture equipment leading to low debt equity and maintenance capex and hence only theme park business with strong financials. Good promoter back ground. Conservative yet stable growth plans of growing 1 theme park every 3 years with minimal debt requirement. Watcjlist :

Fall in footfall and ability to increase price, Cross-sell revenue opportunities -

Amrutanjan (2% at 430 Rs):

An established brand available at discount compared to peers and having reasons for the same. However, in last 3-4 years, management has shown some aggression visible in growth rate and a revamp of product portfolio and marketing. Also, management has been good to shareholders in the past by rewarding with special dividend for sale of land. Double digit PAT margin, debt free, good overall financial numbers. Triggers: Continuation of aggressive in revenue growth,

product extension may lead to re-rating. Watch list : Check on working capital management which does not look impressive, turnaround of acquired beverage business -

Mindtree (2% at 590 Rs)

More or less similar reasons like persistent -

Ambika Cotton (2% at 812 Rs)

Unique player in its arena due to extreme focus on quality, though conservative in approach. Visible in unique working capital management. Very honest promoters, soon to be debt free, expansion plan in pipeline. Have capacity to sustain business in a challenging industry and thus come out winner. This is not a growth story buy for me but value investment which may have low downside risk due to inherent nature of management focus on quality and conservatism.

Watch list : Any change in promoter running the show -

Pharma Fund (22%): Alkem (20% at 1100), Aurobindo (15% at 770),

Lalpathlans (20% at 900),Sun(10% at 800), Lupin (10% at 1520),Neuland(10% at 900), Granuels, Synegine, Natco, Shilpa (15% all) Since, I am yet to understand the industry completely from domain and valuation perspective, taking a fund based approach as of now. A recession free sector which has ability to grow in mid double digits for next 4-5 years, however, going through a tough time and hence, available at reasonable valuations which used to be at premium. One of sectors which has made money to investors across countries. Though, I do not understand sector a lot, have been reading and hence have started with a portfolio approach. Theme of portfolio:

-

Pick beaten down market leaders who are investing heavily on R&D : Sun Pharma, Lupin

-

Pick leaders with good revenue (ANDA)/Order book visibility : Aurobindo Pharma

-

Pick high grow sub sector focused company/High IP driven companies : Shilpa Medicare, Natco Pharma

-

Small cap bet :Pick small base player with high growth possibility and margin expansion scope: Neuland Laboratories

-

BFSI Fund (15%): Cholamandalam (25% at 750 Rs), Ujjivan (25% at 290 Rs), Gruh (20% at 257 Rs), Repco Home (20% at 663 Rs), Capital First (10% at 557 Rs):

Again, one of the sectors which has made money for investors across the globe. Pocked good stocks when sector was on downside and now have stopped accumulating aggressively but accumulating few in small proportion to ensure that till I understand companies completely, my BFSI portfolio is at least 15% CAGR in profit. Themes: -

Well managed NBFC available play on commercial vehcile financing which is expected to do well in next few years : Cholmandalam

-

MFI : Diversified across states with good risk management and focus on IT and processes, ability to manage cost of funds in future due to banking license

HFC : Gruh and Repco, thanks to valuepickr -

Small Cap bet : Capital First

Once understand valuation, will be more sure of individual stocks

12 Likes

Hi,

Got few messages on valuation approach and hence sharing method used:

Assumptions:

-

Business has consistent CFO and business would continue to operate in the same way as historically until and unless new components are uniquely built in model. (for example, a wonderla expanding 1 park through capex every 3 years is business as usual but wonderla starting a cinema hall can not be factored)

-

Business provides either con-call insights or has history of investment and maintenance capex for guesstimates

-

Historical average and prudent ranges of margins have been considered.

-

For revenue, current/short term future out look considered. In case there is too much difference between 5 year history and current (like no growth), an average of both considered

-

For margin, either current or an average based cyclic behavior n product mix improvement considered (like GHCL)

-

Historical PAT/CFO and CFO/FCF, Dividend history, current dividend, next 2 years of capex plans considered

-

A average scenario based on above and a conservative scenario with 20% margin of safety scenario considered.

-

The arrived price is average of average scenrio and margin of safety scenario.

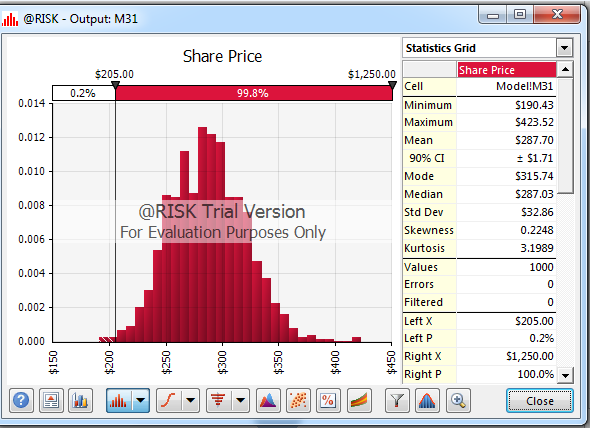

-

Perform a monte-carlo simulation of DCF model so that can get probabilistic scenario of safer price in extreme condition (this is a much scaled up version of scenario analysis)

Where it can not be applied:

- Not applicable to business where too much CFO inconstancy.

- Not applicable to real estate type of business

- Not applicable to ramp up businesses like majesco

What insights i got:

-

Most of business have terminal value (beyond 10 years) contributing to 40-60% of current stock price valuation. Cant agree more with what Prof. Bakshi had said on terminal value contribution.

-

Though many times market punishes a 1% fall in margin by 20% fall in share price but highest impact may come from some other factor. So, this helps to understand for each business 1% fall in which of these levers has highest impact on share price and that needs to be monitored more closely and any fall due to other factors may throw an accumulation opportunity. This will vary business to business

-

Accurate estimate of next 2-3 years of numbers and better understanding of business sustainability(terminal value) will ensure that model is more or less accurate.

-

A monte carlo goes one step ahead of scenario analysis in providing margin of safety , say, if , price with 95% probability is still higher than current price if ranges of values considered are realistic at extremes at least for next 4 years, though, terminal value numbers are most difficult to predict

-

Something is better than nothing, specially for people like me, who has the challenge of investing every month and can not get favorite stock at the same price every time.

Investment approach:

- Scorecard (still work in progress and not yet finalized)

- DCF Valuation

- Monte Carlo Simulation of DCF valuation

Note: None of the views are for any recommendation. The above charts may not be accurate and posted only for demonstration and not for any recommendation. Use of tools demonstrated are for personal usage and not for any commercial purpose.

7 Likes

Good going kumar saurabh.

I personally dont take a 10 year view but am content to have a 2-3-5 year view on companies and take it from there. If I feel that the run way remains or becomes stronger as time goes my conviction keeps on increasing. One also has to be aware of the fact that some companies might be affected by some or other kind of disruption. e.g newspaper companies could be prone to disruption though I feel till the generation that begins the day with a newspaper in the morning is there, the impact will be minimal.

In the list of stocks u have put up u also can add another filter of peer comparision e.g jagran vs db corp or ashiana vs shobha or some similar company, or avanti vs waterbase etc to get an idea where the co stands in peer comparision.

And about having a diversified portfolio I feel there’s nothing wrong provided u have a thesis for holding/buying companies in place. And since I assume that u are having an SIP kind of strategy even buying at slightly higher valuations might not be a matter of concern.

3 Likes

Thanks a lot for your guidance @hitesh2710 Hitesh jee. Frankly, I also rely totally on 3-4 years of market estimates except few companies where ve some guesstimates but then who knows future and completion.to year dcf numbers are just a self guidance on valuation.

Thanks for highlighting importance of comparative analysis. This will add lot of value and currently missing in my template. This would also help to understand and differentiate operating models in sane sector. On my high priority to do list now

Regarding SIP , you are right 10-15 percent here and there for a long term value investor should not matter much if companies are good but the recent run gives me goosebumps , like pi industries has almost doubled where EPs growth is 20-30 pervent which means either it was undervalued or over or may be next 1-2 years r going to be really good which is being factored but just want to be sure while doing SIP on such drastic price movement else happy doing at 10 -15 pervent higher or lower

Heartening to see such dedication to learn!

I was not able to motivate myself to upgrade my knowledge levels as I didn’t have enough money (savings) to invest till few years back. I got the motivation to upgrade only when I was able to make decent savings to invest.

Wish you luck in your investing journey.

Cheers.

1 Like

Portfolio Changes in last 2 months:

Core Portfolio:

Sold : Skipper (better quality of businesses available), Alkem Laboratories (desired price realized) and was not a long term pick

Added Crompton Consumer Electric in core portfolio : Read an article 60s is new 30s for these CEOs. Found a change in mgmt. a new MD with decade of repuation of running world class business, change of board for good, established brand, low capex - high ROCE business, financial metrices better than competitor and trading at 1/3rd discount to competitor. Once market realize potential, can get minor rerated plus total bet on mgmt as 15-20% compounder

Added RBL bank : 1/5th of size of Yes Bank. went through annual reports, presentation. Got a good vibe, opportunity to scale up is there, management looks good.

Added Biocon + Syngeine : Biocon’s biosimilar story looks on track, downside risk of 20%, upside potential can be huge , so, worth risk, still continuing with basket approach in pharm

Accumulated others in core portfolio based on relative valuation attractiveness

Extended Portfolio Entries : Arvind Infrastructure, La Opala, Mirza International, Tata Elxi, Cosmo Films, KitexMayur Uniquotes

Note : These are personal views and not for recommendation. Please do your own due diligence.

2 Likes

Hi Kumar,@suru27

I have checked a few stocks for the last 10 years returns in SIP and all had given 20% plus returns. To generate a 20% return I dont think we need to find new names in business itself. The stock I have checked are as follows and provided all dividends are reinvested .

Period May 2007 to May 2017(some companies are checked from 2008 etc as per available data)

HDFC Bank return is 24%

Bajaj Auto return is 25%

Hero motor return is 20%

VIP industries is 30%

Bajaj Holdings is 25%

Gabriel India is 40%

as you can see barring VIP and Gabriel others are bluechip companies and has given 20% plus returns with good margin of safety for investment. If Its to Generate more than 30 or 35% CAGR i think we should take risk and also as portfolio value rises we should look for stable returns with margin of safety(my view)

Also the stocks like Hero honda, bajaj, hdfc , has still a long runway ahead, Two wheeler penetration is still low, banking is also low, VIP travel is bound to grow and has a good runway and gabriel is again a play on the low penetration of 2 wheelers.

I am not sure if there is any mistake in my calculations.so do your own to verify and if anyone need my excel to recheck i will share it too.

Regards

Vivek

1 Like

Key events in last 2 years of investment journey:

-

Started with a highly diversified portfolio of 50+ stocks spread with max 4% individual allocation as everything was under study. So far, have been able to build a concentrated portfolio which is doing reasonably well

a. The portfolio is not yet in super risk zone as mean PE of portfolio is still between 22-26 both on EPS and CFO basis

b. Has generated 49% XIRR which is not super great (considering the way market has behaved and some of colleagues have generated even higher) -

Portfolio has undergone lot of churn

-

I realized that I want to make money in following ways:

a. Keep accumulating those stocks about which I have high probability of long term conviction

b. I am interested to bet money on value misplaced opportunities where I do not see a long term uniformly sustainable growth but due to headwinds the valuation is highly mispriced and chance to lose money from there is very less (however, this has been done for a selective list of 200 stocks in 6-7 sectors which passes basic quality test. So, this is kind of high confidence arena)

What worked so far:

- Building an investment framework process and following it

- Building multiple tools as a part of framework to speed up analysis process

- Leveraging brexit and demonetization

- Betting heavily on NBFC and real estate sector during demonetization

- Betting on basmati rice cycle (Chamanlal sethi)

- Betting on hotel industry turnaround (SInclairs)

- Bottom up stock picking approach with average up along with conviction

- Holding high conviction stocks despite of under performance given assumptions and story was/is intact

- Buying IT heavily when no one was buying (took it as building cash position as found evry low downside and good upside, ended up making decent money and converting some into long term holding)

- Quickly getting rId of mistakes

What did not worked so far:

- Started pharma exposure with a basket approach but miss-timed it and over exposed portfolio and hence had to book losses partially to re-balance

- Mistakes of investing in some of wrong stocks (covered below)

- Mistakes of not investing in some of right stocks with high allocation (covered below)

So, what all happened in last 2 years in terms of stock activity:

Totally took short/mid/long term position in 145 stocks during last 2 years

Neither good nor bad but mere exclusions post study on various grounds

Discarded stories:

a. Not comfortable with management/business quality/accounting/long term sustainability of business model/lack of confidence and conviction: 8kmiles,Man Infra, Lakshmi Vilas Bank,Kaveri Seeds,

Aurobindo Pharma, Omkar chemicals, Indo count, Kitex, Eldeco Housing, Tiger Logistics, Advance Enzyme,Sheemaroo, Jubiliant food, Specialty Restaurants, Vidhi, JKumar Infra, Sharda Cropchem, Capital First

b. Not comfortable with valuation and could not accumulate in one go and finally had to sell off to build a concentrated portfiolio: Bajaj Finance, Eicher Motors, Gruh Finance, Bosch, La Opala,

c. Found a better peer; Oracle Financial, HCL Technology, Fiem

Misses

Mistakes where had to book losses and exit::

a. Where desired story did not play as per expectation within given time: Majesco, Intellect Design Arena, Hindustan Media Ventures, Cosmo Films, GHCL,Jagaran Prakashan

b. Portfolio allocation went wrong trying to be a contrarian and realized opportunity loss is too high: Sun pharma

c. Mistakes as lost opportunity or exited too early or exited due to minor negatives: Bajaj Finance, Eicher Motors, Gruh finance, Motilal Oswal Financial Services, Natco Pharma, Biocon, Vinati Organics

d. Error in judgement of risk levers: Wonderla

e. Could not build enough conviction despite some effort (though made money, could not convert into long term holding): PI Industries, Avanati Feeds

Hits

-

Quality plays which have given decent return (exited due to valuation discomfort/target price achieved, may enter again based on valuation attractiveness and margin of safety): Amruntanjan, Tasty bytes, Heritage food, PI Industries, Maruti

-

Value Gap plays: Vardhman Textiles, Samprg Piston, Balaji Amines, Mirza International, Sonata Software, TCPL Packaging, Mayur Uniquoters,Arvind Infrastructure, Prozone , REC, PSU Banks, Hexware, Ruchira Paper,Bodal Chemical, Shree Pushkar Chemicals, Sudharshan Chemical

-

Medium/Long term holdings which have so far fared as per expectation on business performance (and in some price performance

) or value gap play playing so far : Repro, Manappuram, Ashiana, Persistent, NESCO, Piramal, Edelweiss, kolte Patil, Ambika, Crompton, Tata Elxi

) or value gap play playing so far : Repro, Manappuram, Ashiana, Persistent, NESCO, Piramal, Edelweiss, kolte Patil, Ambika, Crompton, Tata Elxi

Current Portfolio:

- Repro India (11% at Rs 441) of portfolio : Trimmed down from 20% due to over-run and over-expose

- Manapuram Finance (11% at Rs 92)

- Ashiana Houasing (6% at Rs 174)

- Persistent (6% at Rs 610)

- Edelweiss (5% at Rs 123)

- Piramal Enterprises (5% at Rs 2470)

- NESCO (5% at Rs 490)

- Ambika Cotton (5% at 1020)

- Crompton Greaves (5% at Rs 164)

- Kolte Patil (5% at Rs 136)

- CCL Products (4% at Rs 288)

- Tata Elxi (4% at Rs 677)

- Lupin (3% at Rs 990)

- Sinclairs Hotel (3% at Rs 308)

- Chamanlal Sethi (3% at Rs 96)

- Cholamandalam (3% at Rs 1123)

Total 84% in 16 companies

Small Exposure Portfolio

- Ujjivan Finance (1.5% at Rs 330)

- Accelya Kale (1.5% at Rs 1324)

- Cyient (1.5% at Rs 512)

- Cupid (1.5% at 298)

- Ajanta Pharma (1.5% at Rs 1194)

- Shilpa Medicare (1% at Rs 603)

- Premco Global (1% at Rs 441)

- Aries Agro (1% at Rs 227)

- Century Ply (1% at Rs 253)

- Alstom (1% at Rs 670)

- Technolelectric (1% at Rs 322)

- Neuland Labs (1% at Rs 940)

Watchlist (1.5%): Canfin Homes (Rs 482), Zee Learn (Rs 45), Hindustant Copper (Rs 98), Thyrocare (Rs 674), Allcargo (Rs 177)

Other Watch-list without holding: Narayana Hrudalay, Max India, Fortis, Wonderla, TVS Srichakra, AIA

Performance of portfolio so far as last 2 years XIRR returns : 49%

23 Likes

Looking at how you evolved in the past two years - you did a wonderful job. How much effort have you put in, in terms of average time spent per week on creating such a framework, keeping track of news, potential new entries, etc ?

3 Likes

I am sure your learning has compounded much much more than whatever your peers might have learnt during this period. Even your returns are very nice in absolute sense, so rejoice. In a bull market everyone looks like a hero but the real test which separates the men from the boys happens during the sideways/bear markets.

All the best and keep do update this thread from time to time, so that we get to be your co-passengers in your journey.

2 Likes

Everyday 2-3 hours you can say . So, let me summarize what all I have done in last 2 years

-

Have gone through all VP threads on investment framework and companies falling in watchlist zone . Special mention to threads like on capital allocation etc. They are worth reading multiple times

-

Read 10-15 investment books to get flavor of different investment philosophies

-

Partially or entirely read some of the blogs like by proof bakshi, Dr Malik, Rohit Chauhan ,anil, Jana etc.lot of knowledge. Helps in avoiding to try to reinvent the wheel

-

Built 3-4 tools with 2 years of effort and still work in progress

A. Various personalized screeners ( key is to understand right metric for right situation ). For example, expansion based opportunities might be very different from supply constrained side opportunity. This is a continuous learning curve .

B. Excel tool for 1st level company analysis

C. Excel tool for competitive analysis ( this does not give answers but helps to ask right questions around the ecosystem )

D. A complete stock market data crunching tool to identify patterns of behavior ( beyond Excel ,leveraging professional knowledge of tech,analytics ). Beta version in progress

E. Quantified investment algos to identify patterns of opportunities. This is work in progress with encouraging result and is on my priority list for 2018 -

Read 200+ annual reports ,20+ industry research reports and related documents , concall transcripts , interviews of companies of interest

-

Started attending quarterly conference calls in some of companies where I need to track closely .

Please note that I have been in market since 2006 but took an intentional complete break from individual stock investing between 2013 to 2015 due to professional reasons and had to restart everything from scratch in 2016Jan. So, it was not a fresh start and I was able to carry lot of old learnings which were more around what not to do and fortunately last 2 years have been towards adding what to do

29 Likes

Totally agree, the real test of investment style needs at least 10 years of time. I am intentionally avoiding the word portfolio quality because partial churn of portfolio could be another investment style considering a 10 year period and indiviual areas omf competence. Let’s see how life unfolds. Would be glad to share and learn.

This forum has given so much learning which can’t be measured in monetary worth and is beyond stock investments . I still remember when I thought of getting back to stocks ,the first thing I did was to open mailbox to click on link for VP which Donald had sent during 2011 when many of us shifted from TED. Going through all posts was as good as covering journey from 2012 to 15 which I missed. Many thanks to all contributing investors @Donald @hitesh2710 @desaidhwanil @ayushmit ,yogesh sane and @vivek_mashrani and special thanks to @ayushmit to democratize stock analysis as without screener.in , lot of tools built over that would not have been possible.

8 Likes

Dear @suru27,

I hold CAPF considering the management as passionate with dream to grow the company. Would you please able to articulate why you added CAPF in this list ? That would help me to review my investment thesis to see if it continue to stand.

Also Shemaroo is another company in my watch list(not invested so far). so like to hear views on that as well.

Hi James. Thanks for writing. Please find my responses below:

Sheemaroo:

-

I understood the complexity of accounting principles in this business and realized that for me it is difficult to find out accounting malpractices if promoter does.So, indirectly need to be dependent on promoter to some extent. Though, Dwanil jee’s response in this regard was encouraging, I could not make up my mind

-

The second and bigger issue was that I could not convince myself on the business model under a disruptive technological environment and hence could not conclude on a terminal value to business. Shemaroo generates IRR on second wave of copyrights on content. Now, this is a skill set which they have developed over years. However, I feel, with the amazons and netflix of the world coming, they would be in a better position to identify the true potential of older content and may kill this market for sheemaroo (House of cards was a pure result of customer viewership analytics leading to a profitable segmentation exercise justifying ROI). So, I see 5 years down the line amazons and netflix diectly dealing with original content creator dealing for second generation content. I do not see what kind of advantage sheemaroo will have over tech aggregators to do the same. This is just a hypothesis and may or may not play out. However, considering such risks in a highly disruptive environment (M&E is one of most disruptive businesses tech wise), i am unable to valuate the business and hence decided to stay out.

Capital First:

- In BFSI, I am not an expert and hence i try to stay with tested companies.

- Also, it is very difficult to identify black holes in financial statements in advance. Lending is easy but recovery difficult. So, I am more bothered about quality of lending in finance than quantity of growth

- Considering the above, I am more interested in companies who have shown historical examples of conservatism and asset quality with growth as second priority

- The below link will give some clues on why I did not like Capital First : Indian Microfinance Sector and the companies in the sector

Look for post no 335 by Yogesh Sane

- I would like to wait for few years and see how Capital first evolves. When in doubt, I am willing to pass and stay with more conservative approach in BFSI

3 Likes