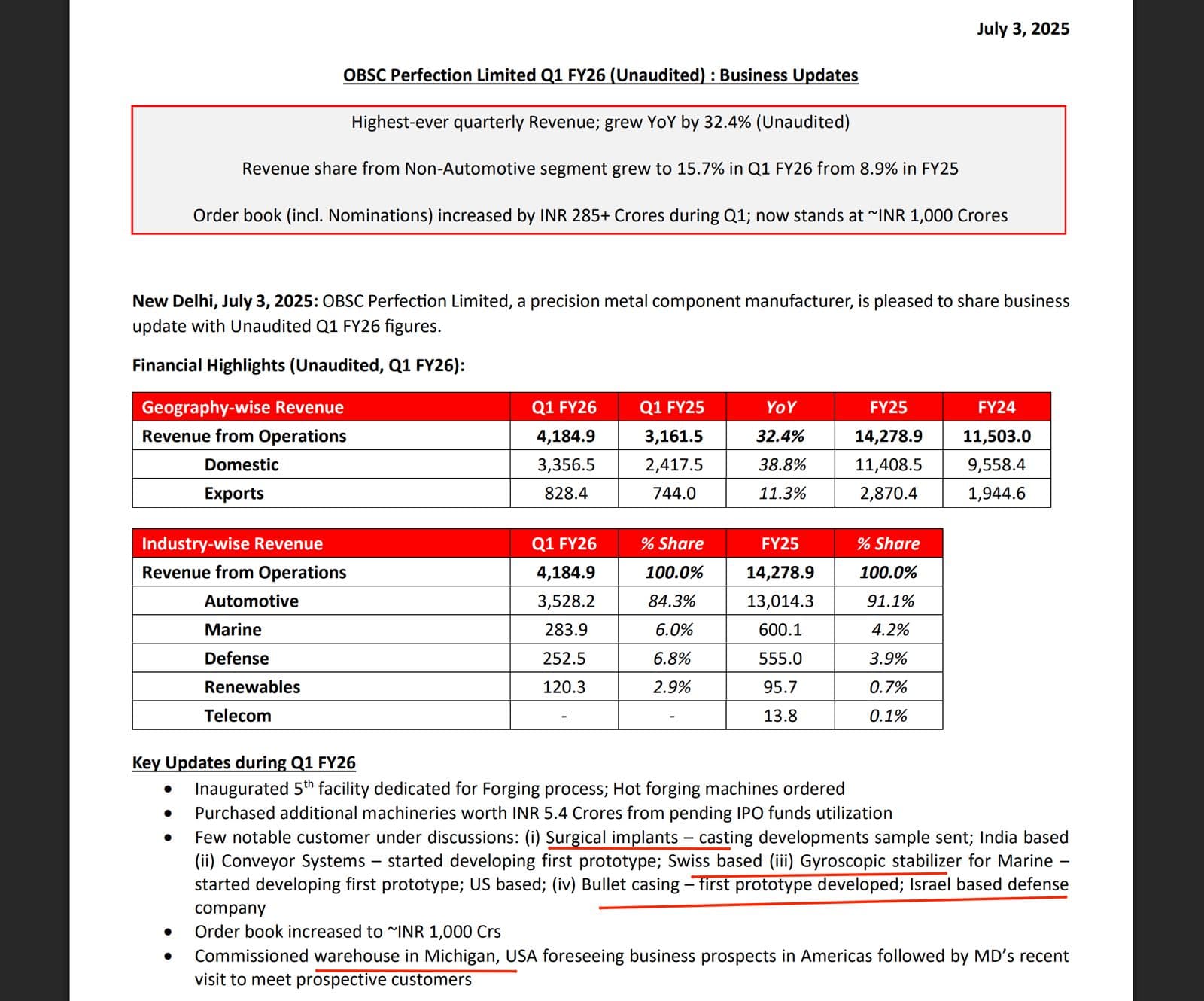

Stallion India Fluorochemicals Ltd : (My notes from recent con-call and other publicly available sources)

Shazad Sheriar RustomJi started this business as a first-generation entrepreneur when he was 22 years old. He has been running and growing it successfully for the past 32 years.

The company is involved in the debulking, blending, and processing of approximately 40 different refrigerant and non-refrigerant gases, holding around a 10% market share in India. The company primarily focuses on after-market sales rather than OEM sales, with 80% of its revenue derived from the higher-margin replacement/after-market channel. This strategy provides resilience during down-cycles. However, HFO and specialty gases will exclusively target the OEM market, as this represents a new and emerging business for the company.

There are few tailwinds in favour of this company

- As it’s into cooling and refrigerant gases used in ACs and cold chains, regulatory transitions from HFC to HFO by 2030. India has its HCFC phase-out scheduled through 2030 for R-22, and will start phasing down HFCs in coming years (freeze by 2028); regulatory change creates a replacement demand cycle that Stallion can ride.

- Semiconductor and electronics manufacturing in India are picking up now and have a good runway for ultra-high purity gases (such as neon, argon, silane, etc. for chip production).

Company has four facilities, and two more are coming up. A new specialty and semiconductor/solar cell gas facility will come up at Mambattu, with a 7,200 MTPA capacity. The capacity for liquid helium processing will be 1,200 metric tonnes per annum.

Company is moving from low-margin hydro-fluoro-carbon to higher-margin hydro-fluoro-olefin. Profit margins are expected to improve by 3-4% in the near term due to new product segments and backward integration. The margin improvement can be seen from FY27 onwards as the new facility is coming up in Q4 of FY26. (Under the Kigali Amendment to the Montreal Protocol, India and other developing countries must start cutting HFC consumption in 2032 and reach an 85% phase-down by 2047).

Guidance :

Expect to grow 35% CAGR top-line for the next three years, with 3-4% margin improvements.

There are some entry barriers to supplying semicon gases due to a multi-year approval process; new entrants will take that much time to get into this business. There is a cyclical upturn right now for the business. HFOs don’t have a down cycle compared to HFCs. Stallion is the largest distributor for Honeywell and Honeywell moving from HFC to HFO. Demand for the product is skewed in some months, so QoQ top-line fluctuations can be seen.

In Flourochems, China has 85% share, RM prices can fluctuate hugely from 100-300%. Company keeps higher inventory to ensure it can navigate the price hikes. Need to watch out for receivables, working capital management, import issues from China and RM fluctuations.

Comparison with peers ( not strictly peers as these are large players with significant economies of scale)

Valuation :

FY25 PAT is 39 Cr. The stock is trading at a trailing PE of 15, which seems to be at a significantly lower valuation than peers in the same industry, though not necessarily the same business. Now that debt is fully reduced, one can expect interest savings flowing to the bottom line. Over a three-year period, if they are able to reach 1000 Cr topline with interest savings and margin expansion, the bottom line could hover between 100-120 Cr, and with some PE rerating, the stock looks to be poised for a significant upside.

DSCL : Invested recently.