Hello sir. Can you please have a look at Committed Cargo?

It doesn’t have a thread of it’s own!

Thanks and very nice write up.

1.Is there any fire incident happened in the company history?

2. Any value addition products started from HFO

1 Like

Hi Anushka,

I had a glance at it, Its a low margin business. Has run up a lot and looks expensive. Anything interesting happening in Committed cargo ? Since they have not done con-calls could not find much data on this.

1 Like

Hi Krishna,

Its a recent IPO, I have not seen any recent filing regarding fire incidents, but its a likely risk we have to watch out for. We have to wait for any new filing from Stallion or the next next con-call to know about HFO progress.

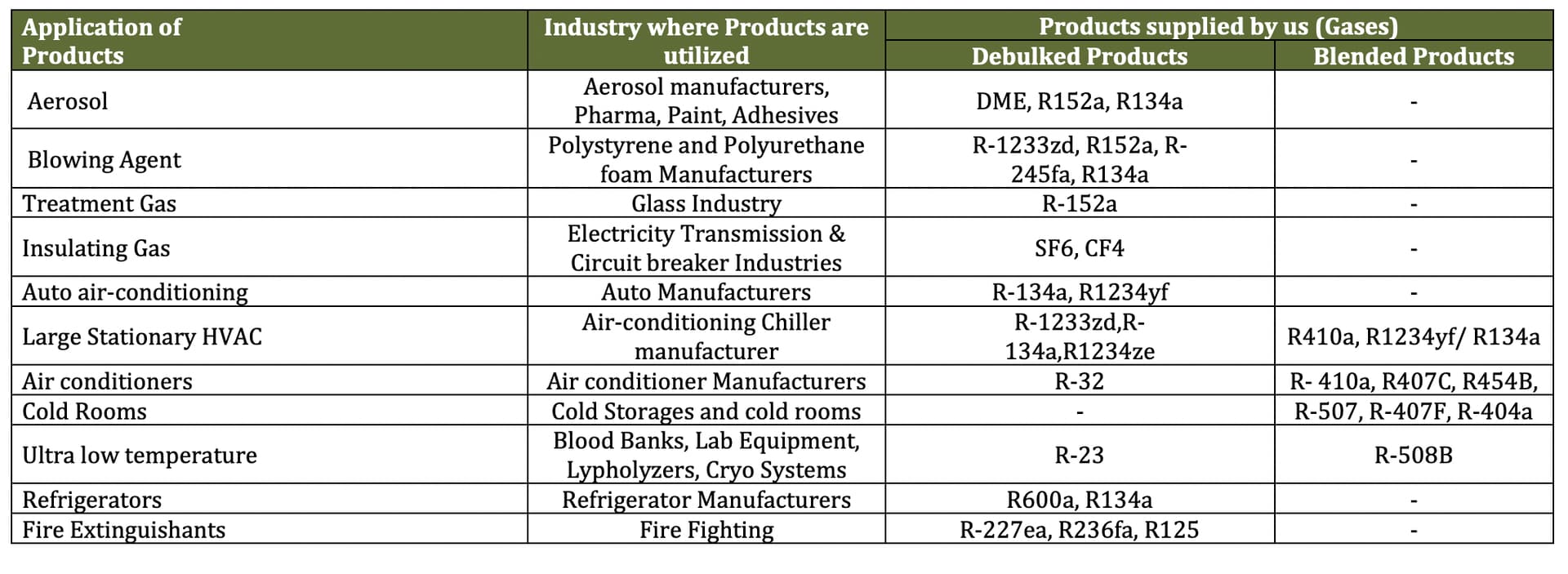

Reg the fire hazard risk, I wanted to understand how this might impact Stallion. Below is the table with list of gasses and fire hazard profile.

Stallion works majorly with Low-risk A1 gases , but its growth will come from HFO-1234yf, R-32 blends and the small-pack hydrocarbons which are in the A2L–A3 bands. This is expected to fetch higher margins and possible low moat as handling this is not easy , but will also raise the compliance costs, training needs and higher risk of fire hazards.

| ASHRAE | Industry safety class | Stallion supplies these gasses | End usage os the gasses | Fire risk impact |

|---|---|---|---|---|

| A1 | Non-flammable gas for SF₆ / CF₄ | R-410A • R-407C • R-404A • R-134a • SF₆ • CF₄ | Room- & VRF A/C (R-410A) • Retrofit chillers (R-407C) • Cold-room refrigeration (R-404A) • Auto & domestic fridges (R-134a) • Switch-gear insulation (SF₆) • Semiconductor etching (CF₄) | Will not ignite under normal pressure & temperature. Fire risk comes mainly from stored-pressure cylinders, not from the gas itself. |

| A2 | Lower-flammability, Low-toxicity | R-32 • R-1234yf | Next-gen room A/C & heat-pumps (R-32) • New-model car A/C (R-1234yf) | Needs a strong spark + confined mix of gas/air to burn; flame front spreads slowly. Extra leak-detection & ventilation are required, but systems can still be serviced in typical workshops. |

| A3 | Flammable | R-152a | Aerosol propellant, foam-blowing agent, some HFO blends | Ignites more readily than A2L gases; service areas must be strictly spark-free and well-ventilated. |

| A4 | high flammability | R-600a (isobutane) • R-290 (propane) | Domestic & bottle coolers (R-600a) • Hydrocarbon heat-pumps & low-temp freezers (R-290) | Catches fire easily and burns fast; charged volume is therefore tightly limited (≤ 150 g in most fridges). Technicians need explosion-proof tools and strict charge-size rules. |

3 Likes

@satishwe have you looked at Accent Microcell Ltd.?

Company manufactures Pharma Excipients - Micro Crystalline Cellulose (MCC) which is a binding agent. They are also moving into specialty products like CMC/SMCC which have nearly twice the realizations (MCC - INR 250-300/kg; CMC/SMCC - INR 550-650/kg). (competitor - Sigachi Industries)

Additionally, company is also undergoing a capex (current capacity: 9.2K MT for MCC, capex for specialty block: 2.8K MT by Oct’25 & additional bulk MCC capex - 12K MT by June’26) effectively a ~150% increase in capacity. Same is being funded by IPO proceeds + right issue.

Financials summary: Mcap: 650 cr, Rev: 265 cr/ PAT: 33 cr, PE: 19x, debt free, CFO/EBITDA ~0.5x.

Modelling in 60% utilization of the 12K MT plant, & 75% of the 2.8K plant by FY28 (considering company has been running at ~100% capacity for the last 3 years, so faster ramp up), we are looking at INR 575 cr revenue / EBITDA - 18-20% (uptick due to premium product mix) and PAT of 70-75 cr, which translates to 100-125% absolute PAT growth.

Considering PEG of 1x, the company looks to be interesting, considering it delivers on the capex and the ramp-up.

Would love to hear your thoughts on the same.

2 Likes

Hi Satish, thanks for the reply!

Did good this year as compared to earlier earnings. FII’s have come in this quarter, which boosts my conviction a little more.

I am invested from 126 levels (a 2x for me already), so was just looking for someone more experienced with SMEs to have a look.

2 Likes

Hi Vidhyut,

I am not tracking this one right now, used to hold some stocks last year. I dnt understand if they have any specific moat hence left it. But with competitor Sigachi in trouble due to recent Fire accident , this stock has started to run up a bit.

3 Likes

Hi Satish, do you track Creative Graphics? They have leadership in flexographic printing plates and recently forayed into pharma packaging. Guiding for 100% growth. Could you take a look?

Hi Varun,

At first glance it looks good. I dont track this one yet, so cannot tell more for now. Will revert if i track this.

2 Likes

Hi Satish,

Are you tracking parmeshwar metal?

Hi Arjeet,

I am not tracking Parmeshwar Metal. First glance seems like a commodity business with no differentiating factor. The Raw Material costs are 97%, and margins are at 1%. Feel very tough to make high returns in such commodity stocks.

4 Likes

Hi Satish,

Have you analyzed Osel Devices? It has recently received license to manufacture Philips brand devices in India! Looking interestijg from technical point as well.

Thanks in advance

Hi Amrit,

I do track this one, need to see how well this Phillips partnership will work out, as globally I am not sure if Phillips phones are doing well. Last year they had -ve cash flows and Numbers dont seem good for the past year for cash conversion cycle, working capital needs are not great. Right now its in the watchlist for me.

4 Likes

@satishwe Now we have a separate thread for this company. Should we not move all related news at one place? Thanks

4 Likes

Satish ji is Pulz a listed player of 100 cr from Mumbai in same space and does cinema hall acoustic work and recording studios

@Naveen_Bhatia Pulz is not in sound proofing, its into speakers and sound systems.

1 Like

Your take on result @satishwe

Q1 FY 26 highlights -

Revenues - 110 Cr, up 51 pc from Q1 FY 25 - 73.2 Cr , 152 Cr Q4 25

EBITDA - 14.3 Cr, up 16 pc Q1 FY 25 12.4 Cr, 18.7 Cr FY Q4 25

Margins - 13pc vs 17 pc Q1 FY 25, 12pc FY Q4 25

PAT - 10.4 Cr, up 19 pc from Q4 FY 25 8.42 Cr , 13.3 Cr FY Q4 25

Concall scheduled on 12 Aug

1 Like

Top line looks great with 50% yoy growth, need to check on the concall on margins compression.

3 Likes