4 directors(2 independent n 2 nominee) have resigned.

Embezzlement to the tune of 1.28 cr, in which 34 lakhs been recovered!! Fraud case and amount has come down though.

Audit committee chairman didn’t attended previous AGM!!

CSR amount hasnt been spent for the fiscal.

55% increment to the CEO.

HP Singh doesn’t hold any stake in personal capacity.

Percentage holding mismatch between promoters holding and yearly transaction page.

Impairment losses to the tune of 13.5% of the revenue.

15% of the loans classified as risk.

Subsidiaries are given loan at 1% p.a

SOTP of subsidiaries valuation is less than CMP as per the external valuator.

Company has almost paid 6.3 crore to EPFO for the previous years backlog contribution upon demand I think.

NPA has reduced.

While, they definitely lend to the risky borrowers though I do hope they’re are no kickbacks involved in this lending, which differentiates it from the Yes Bank in a big way.

If you have any other evidence which compares it well with Yes Bank , then do let me know?

Also, I don’t think there promoter has ever got into any wrong doing… Again if you have any articles, then that would be helpful.

Hi Mr Harsh, Thanks for sharing all this info- As I am researching this company myself, can you share the snippets or article from where you have got your information .

On your 2nd point- the Satin promoter has actually trying to reduce their pledge while increase their promoter shareholding i.e. from Mar-19 they have increased their stake from 27.94 to 30.19%. Also, from Jun,19 they have reduced their pledge from 20.80% to 11.79%

Couple of things

Market being so volatile these days, why should anyone subscribe to rights issue at Rs.60? If market corrects we might get it at lesser price in the spot itself? With this, can we extrapolate that rights not subscribing fully?

Since demonetization, i think Management has become conservative on the growth side. But still not out of woods and are being haunted by one or the other like high concentration, floods, riots etc.But being in the unsecured space, NPAs are expected.

With diversifying across the states, pledge getting released, promoter share getting increasing, their decision of subscribing to rights as well indicate there might be light at the end of the tunnel.Going through the concall transcipt, i feel like they are walking the talk. On the one hand, highly concentrated MFIs are quoting at top of the valuations and on the other we are getting this at the fraction of the BookValue. Luckily, none of the institutions booked out losses yet even though they have subscribed at premium to the CMP. Street reactions to the rights as well as the Q1 commentary might give hint at how the future looks like for the company

I am noticing some Satin RE stocks in my Zerodha portfolio. I had satin shares but I did not purchase any right issue separately. Also the last trading price Is 13.5. I’m confused, any idea what it going on here.

Collection efficiency (CE): CE stood at 105% in Mar’21 and Apr’21 saw marginal reduction to 93%, but May’21 has stood particularly challenging with 75% CE because of stringent lockdowns. Even though in last 7 to 10 days CE has somewhat improved, Jun’21 stood better than May’21 but not yet back to pre-COVID levels. The Co. expects better CE trends Jul’21 onwards

Centre meetings: With suspension of centre meetings, door-to-door collections are now happening

Active clients: Satin Credit Care saw active client shrinkage from 30 lakhs to 26 lakhs as at FY21-end. Said that, the Co. has already begun sourcing of new clients.

Delinquency/payments scenario: Early bucket DPD (<30 days) will continue to witness higher PAR whereas 30 plus DPD will not be significant in Jun’21 and therefore wouldn’t add meaningfully to NPAs. While <2% of the customer base has not paid single instalment since Sep’21, 7% have made part payments.

Growth trends: Growth is expected to remain muted in FY22 as focus shifts on maintaining quality of portfolio & digitization of processes.

Assam loan waiver and RBI’s draft proposal on removing MFI’s margin caps, both events should have positive impact on the business. Satin Credit Care has not made any incremental disbursements to states of Assam and West Bengal; it has sufficient ECL provisions in place for this portfolio.

Satin Creditcare Network Limited plans to raise funds by way of issuance of Non-Convertible Debentures upto INR 5,000 Crore. Meeting of the Board of Directors is scheduled to be held on Monday, July 11, 2022.

Consolidated AUM as on 31st Mar’22 is Rs. 7,617 crore Satin Credit care.pdf (284.5 KB)

On 21.12.23

Satin allocated shares to seven institutional investors in a QIP, to raise ~ ₹250 crore.

ICICI Prudential Life: 20% of QIP, ₹50 crore.

Societe Generale - ODI: 16.40%, ₹41 crore.

Bandhan Mutual Fund: 16%, ₹40 crore.

Morgan Stanley Asia: 14%.

Bajaj Allianz Life Insurance: 12%.

Bandhan Small Cap Fund: 10%.

Other funds: Bandhan Multi Cap, Bandhan Financial Services, Ananta Capital Ventures, Ghisallo Master Fund LP also received allocations.

I think This dilution is positve on the story.but havent study who is selling ?

I dont understand the satisn business much, simply based on PE it looks attractive to me, wish to understand more about future prospect of its business.

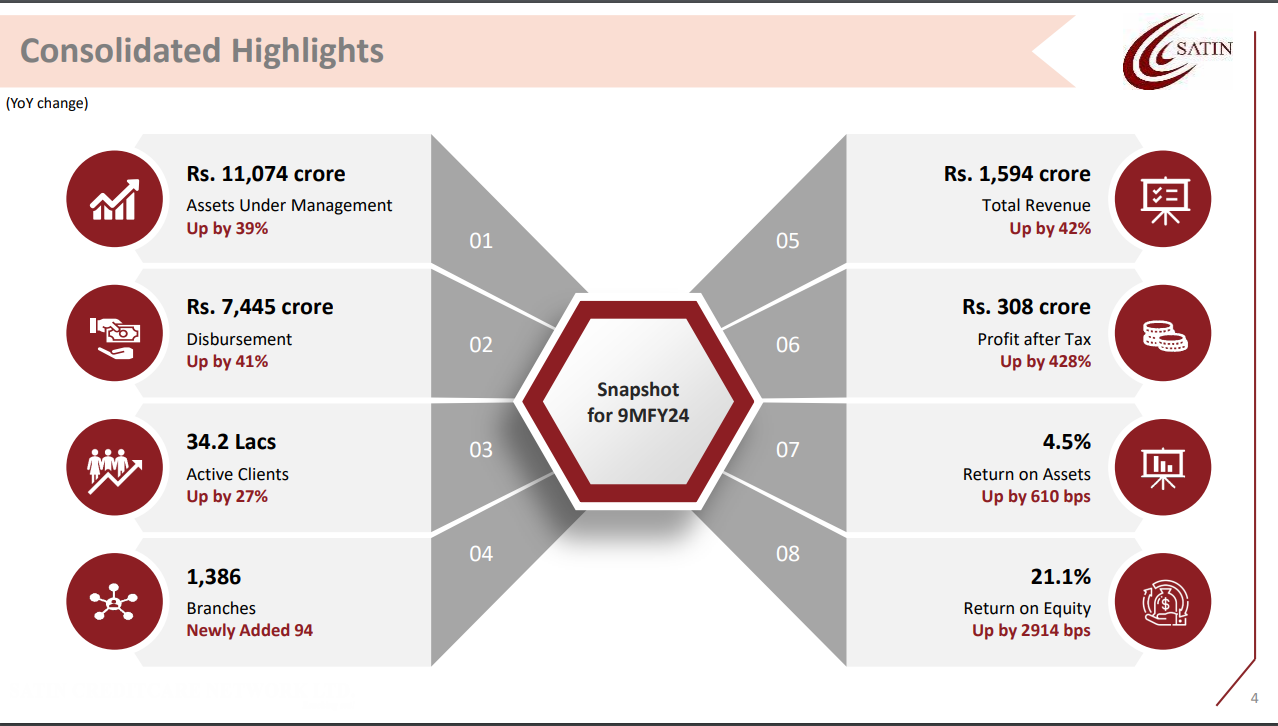

Satin came out with banger Q3 numbers, with RoA and RoE at 4.5% and 21%, a few more quarters of sustained profitability should help re-rate the stock to a minimum of 1.5-2x book (current BV is 205/sh)

Impressed with the management as they cleaned up the book and now are at historic profitability metrics, they not only delivered the projections before FY24 ended.

Satin Management has provided guidance indicating a significant decrease in Return on Assets (ROA) for the current fiscal year compared to the previous one. This is attributed to a slowdown in disbursements and an increase in stressed loans, particularly in Punjab. Should we interpret this as a sign of growth topping out and a deterioration in asset quality? This pattern has occurred multiple times in the past, and it seems the market is already factoring it in. As I’m not an expert in this sector, I would highly appreciate expert view on this matter.

Hi, can you please share on where the management has guided for a significant decrease in RoA? From its latest investor concall, they have guided the RoA to be in the range of 4.25% - 4.75% for FY25. Also, the rate cuts (when and if they happen in this FY should only benefit them). They have also managed to bring their borrowing costs down, the upgrades in credit rating is helping them here.

This indicated ROA figures are significantly lower than current ROA if you look at in percentage terms. Management is observing some stress in Punjab loans. Also slowing down the disbursement in Q1. All these are negative indicators. Q1 numbers may give proper idea of the future territory i think.

Request if you could throw some light on the cleaning up of books…

I only see a huge loss in qtr ended June 2022 assuming that is when a chunk was written off…was there any such exercise more recently?

Satin Creditcare Network has successfully closed its first Pass-Through Certificate (PTC) transaction with HSBC India, valued at INR 119 Cr with a 9.30% coupon rate. This transaction aligns with SCNL’s strategy to expand its funding base and enhance financial inclusion. The Series A1 PTCs were issued on August 30, 2024, with a maturity date of August 12, 2026. The deal involves a par structure where 87.5% of the pool principal is issued, with the remaining 12.5% acting as overcollateralization, and is rated Provisional CRISIL AA+

PE ratio of the stock is still trading around ~5. Any reason for such a low PE ratio to the company ? Is there potential for rerating in next 2-3 years

The sector is undergoing significant stress due to macro as well as company-specific factors. Refer to RBI commentary in this regard - will help set context. Also, the preferred approach to look at lending businesses in general is Price-to-book and not Price-to-earnings, given the asset heavy nature and inherent cyclicality.