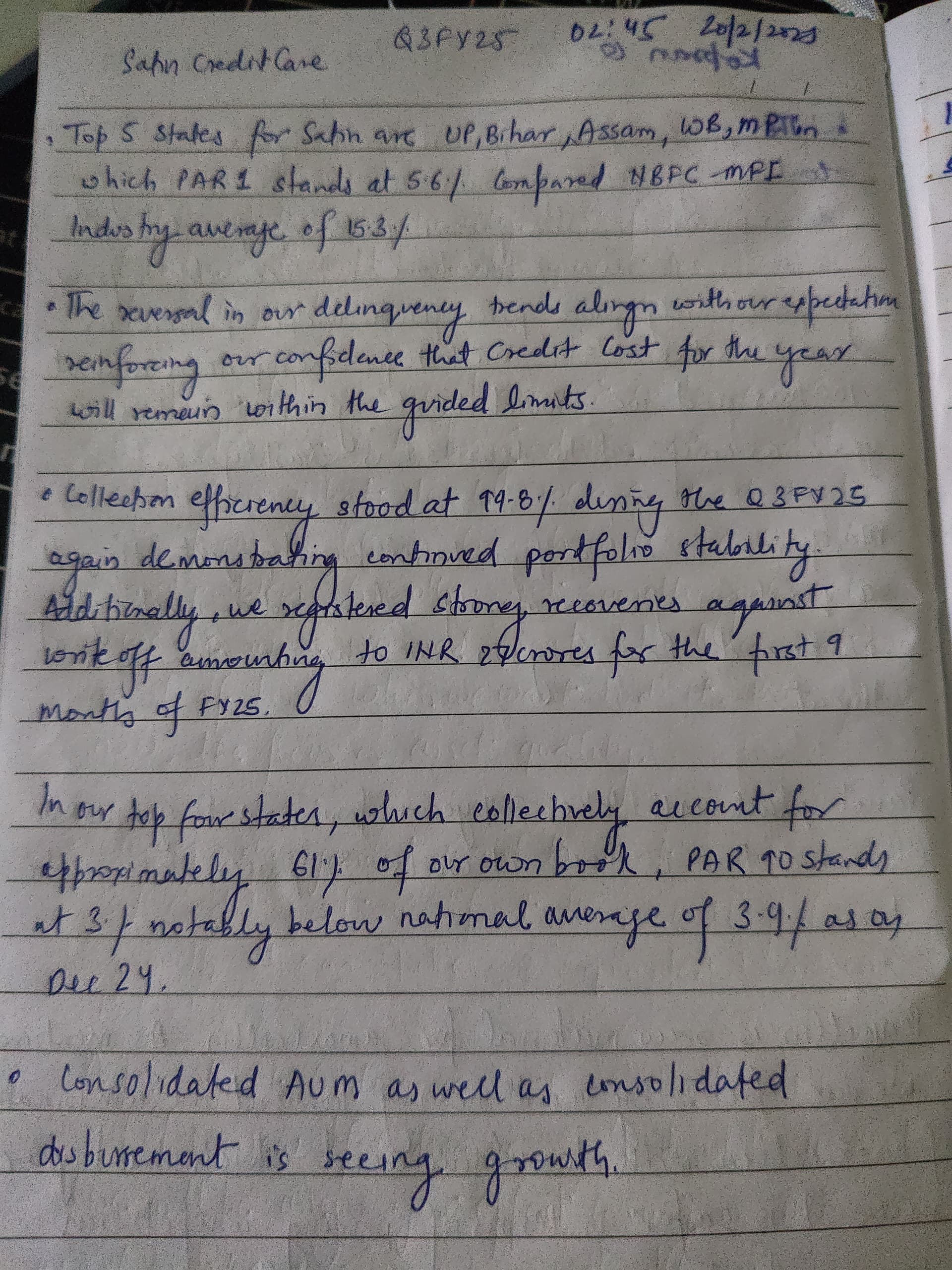

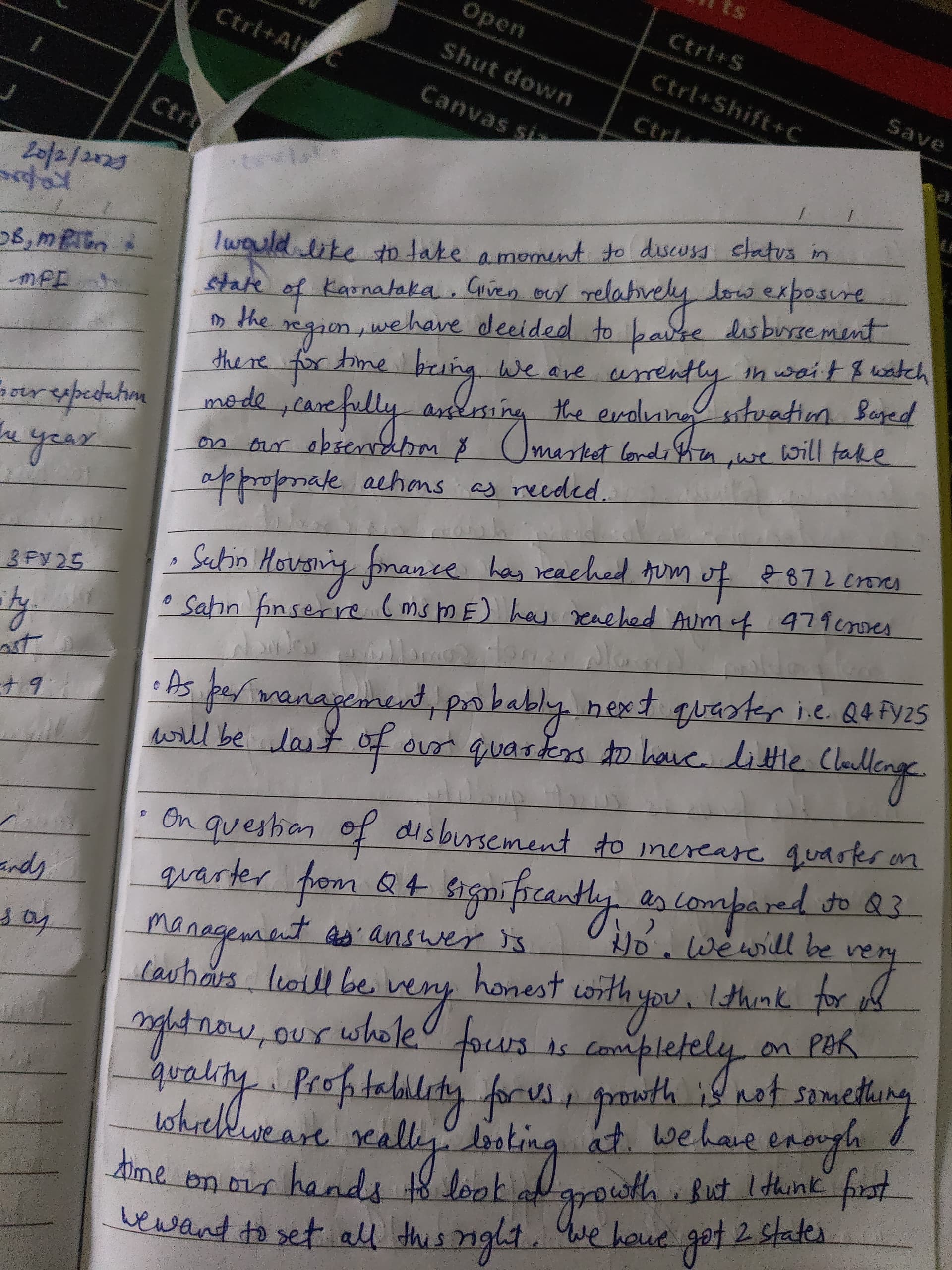

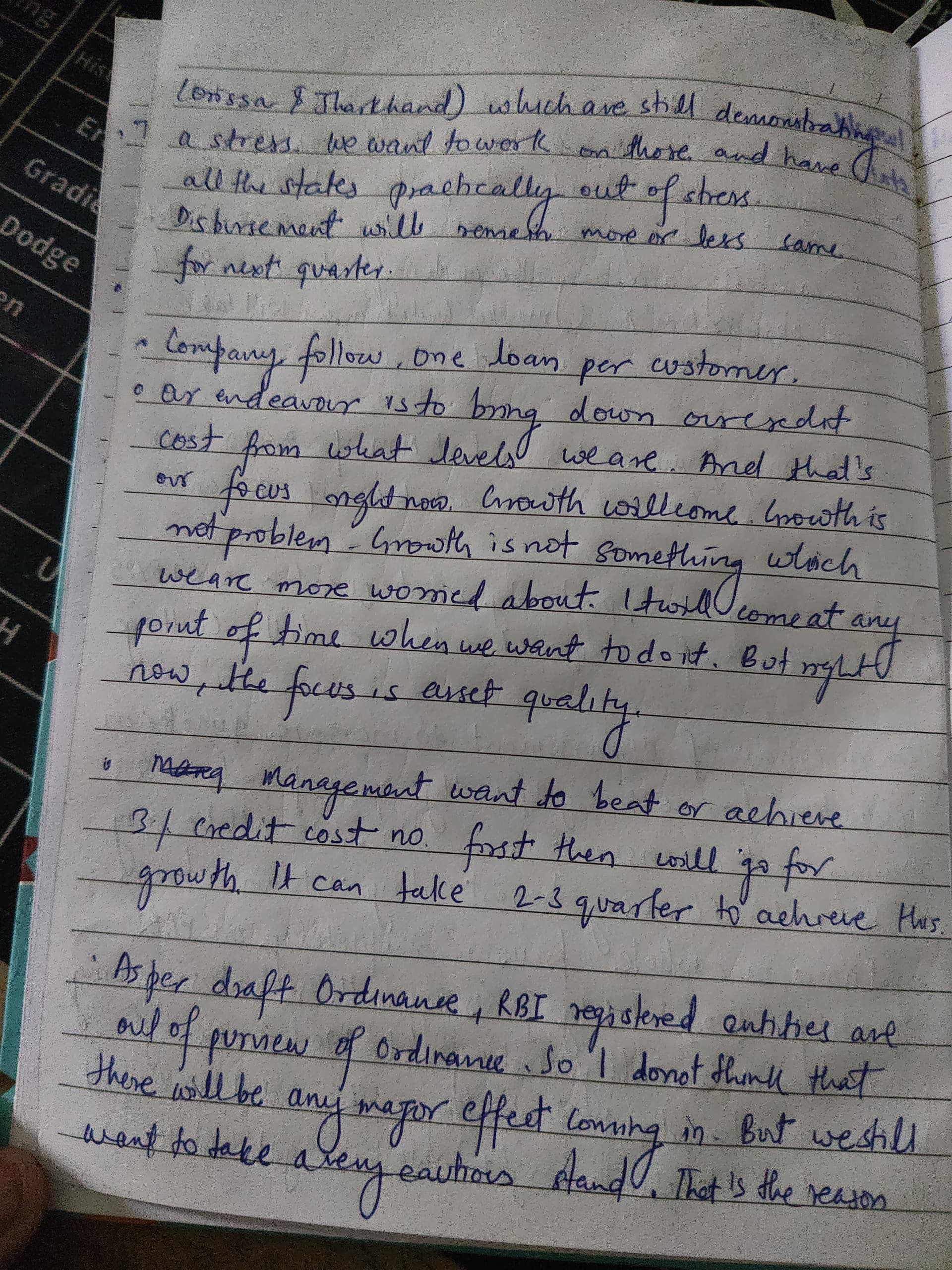

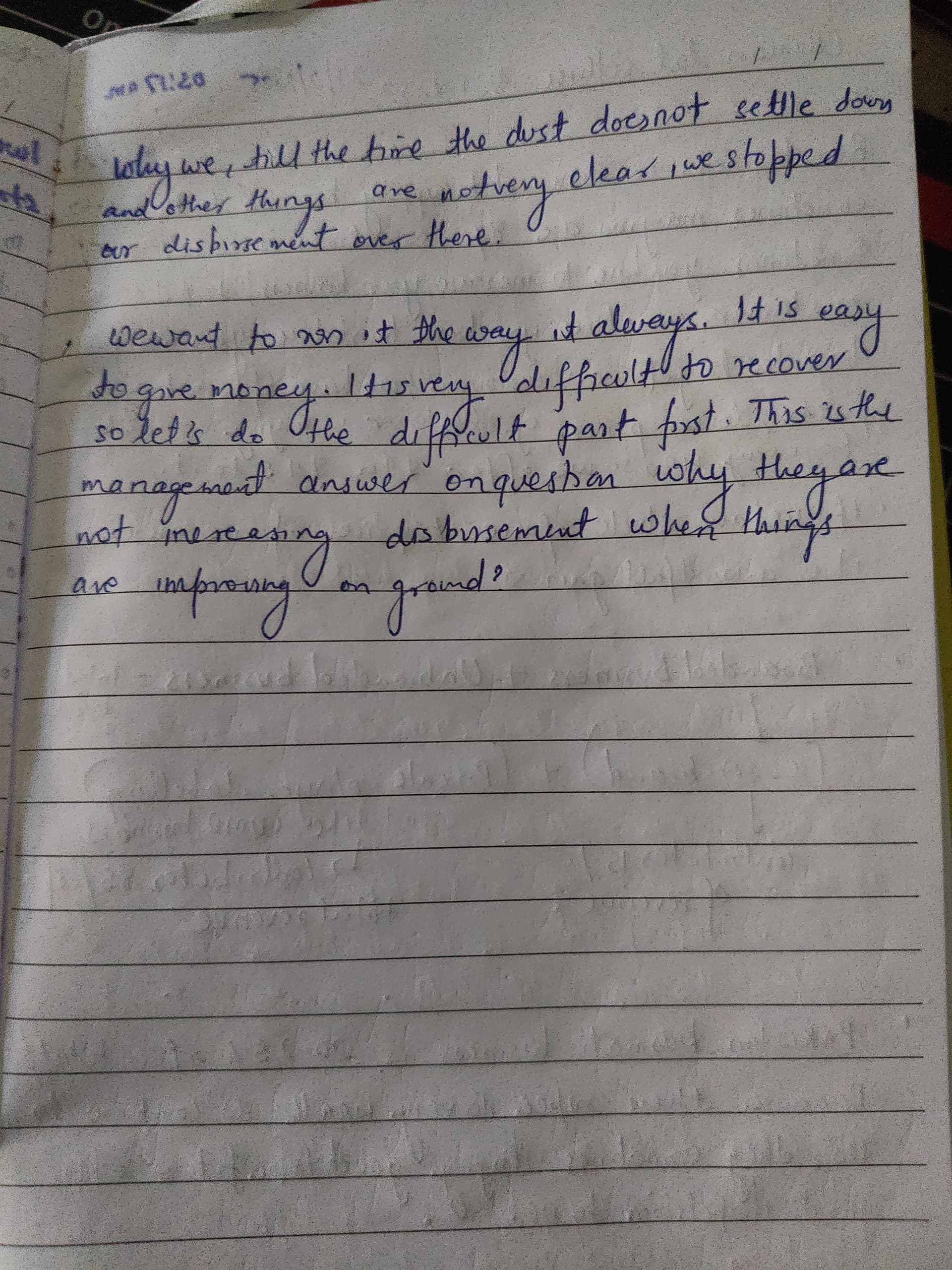

Why I like Satin:

Background:Satin, Credit Access Grameen, Manappuram (For Ashirwaad ), IIFL (For Samasta) and Spandana Spoorty, Fusion Microfinance are a few of the NBFC MFIs I track. There are more in the market. ( viz Muthoot Microfin), that I do not track.

Microfinance, as understood by me, is a collections game. If you collect well, you have lower credit cost. This leads to more profits, higher book value etc. And the best way to avoid NPAs is to source well. The better MFIs, therefore have systems in place that avoid loans that may turn into NPAs.

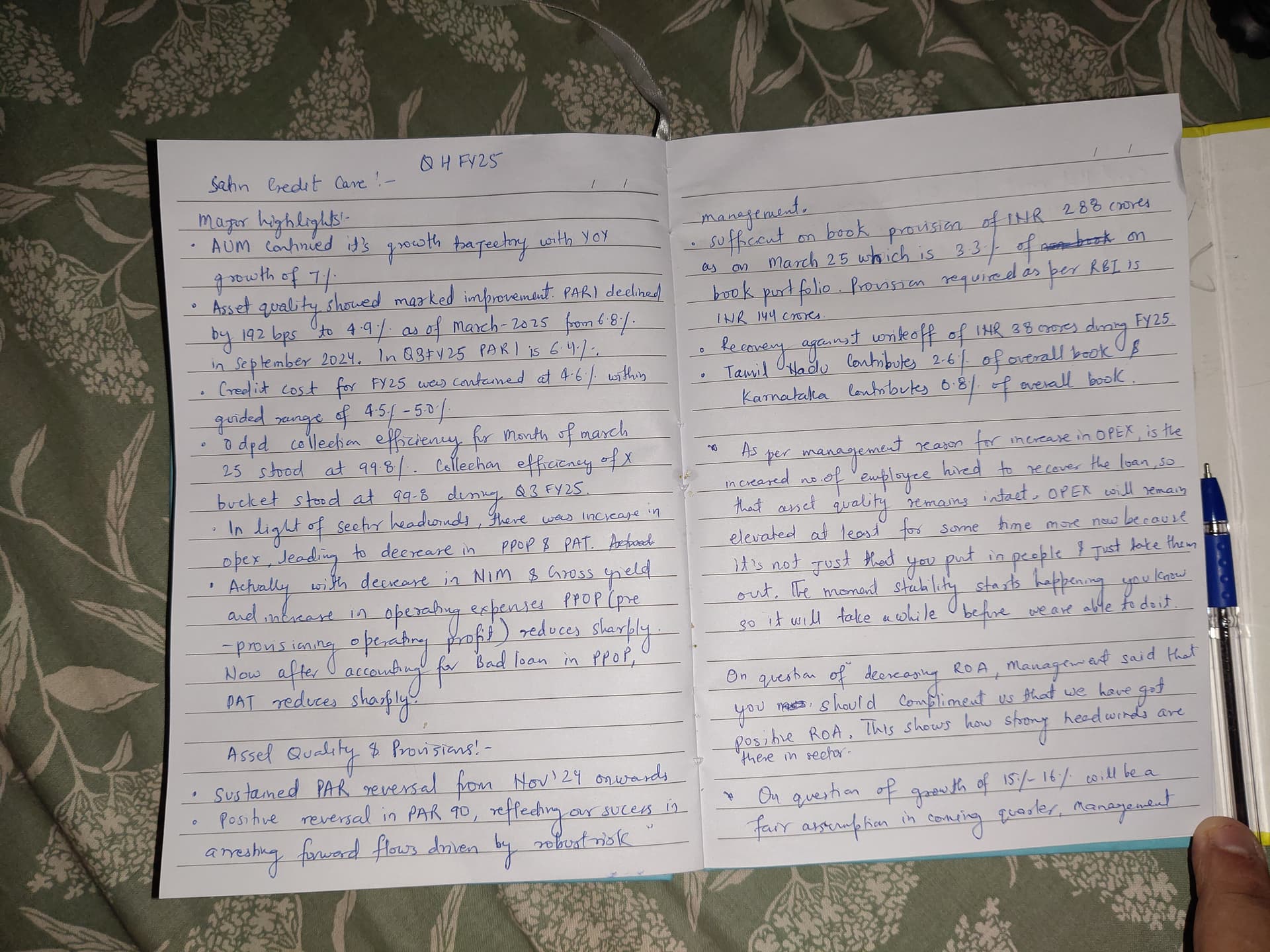

Reason 1: What I can make out is that Satin has the best credit cost numbers, not only on Q3 results but previous Q2 and Q1 also.

Reason 2: Further, it is trading at significant discount to its book value.

Reason 3: The MFI shares are beaten down currently owing to the stress in the sector. However, I believe that the MFIs will eventually recover from the stress and valuations will accordingly move upwards. And the better run MFIs will deliver superior returns.

Disclosure: My personal views. Not a buy or sell recommendation.

Disclaimer: Holding and bought today again. Will share concall notes shortly.In my opinion, it is quite undervalued in comparison to Arman and Credit. What is comforting is improving asset quality with very good collection efficiency. Credit cost also remains as per management guidance. Biggest holding in MFI space with Arman and credit access. I may be wrong in my understanding. Kindly take this with pinch of salt.

PAR 90 is peaked out, due to continuous effort by management, the heat of same is felt on increasing Opex which is need of hour to have good asset quality.Things still look haunted looking at pre-covid times what happens at loan book. Market is knowing this and that’s why discounting it.

Looking at Manappuram MFI Asirwad & Muthoot microfin,till now they have done very good job. I am fearing a lot in putting my hard earn money as they are not as renowned as Credit access and Arman. I am taking calculated risk here. My average buying price is 152.25. lower buying price will cover any margin for error and provide much needed margins of safety.

Let see where it ends. Will track business very closely.