Here is the response from Investor relation cell on higher rate debt,

“We have raised some sub-debt for Satin as well as our subsidiary, which is at a higher price than standard debt. The advantages are long term tenure (7 years) and qualification for capital as it is categorized under Tier 2 capital.”

Need to dig deeper for same kind of debt (subordinated debt) raised by other MFIs/NBFC. If anyone has any data request to post here.

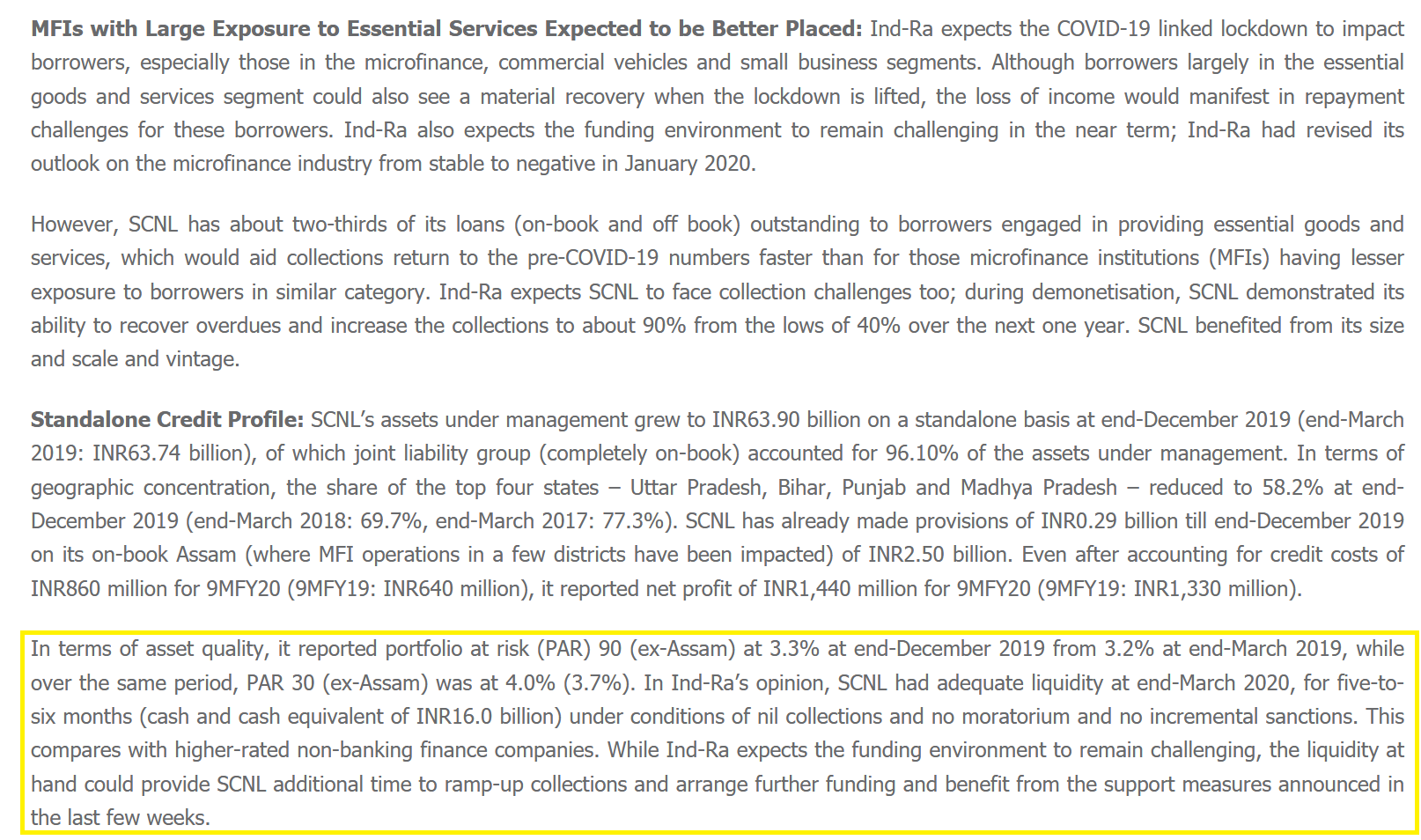

PAR figures which were part of standard presentation for past many quarters go missing from presentation of Q3FY20 .Management was not forthcoming with PAR figures during the con all as well .

Par figures , writeoff ,NPA movement should be a minimum a finance company should compulsory share every time else all is Mumbo jumbo .

Have written to management let’s see what they share .

The stock of Satin has fallen around 70% from it’s peak, however, they talk a lot about doing disbursal online and that they have developed an in-house software .

Do you think it can benefit them - Any views on Satin or some interesting reports to refer?

Though looking at the stock price(0.25 times reported book value) the market seems to be pricing in massive erosion in networth due to spike in defaults.

The market seems to agree with you about survival being difficult,hence the collapse in share price.

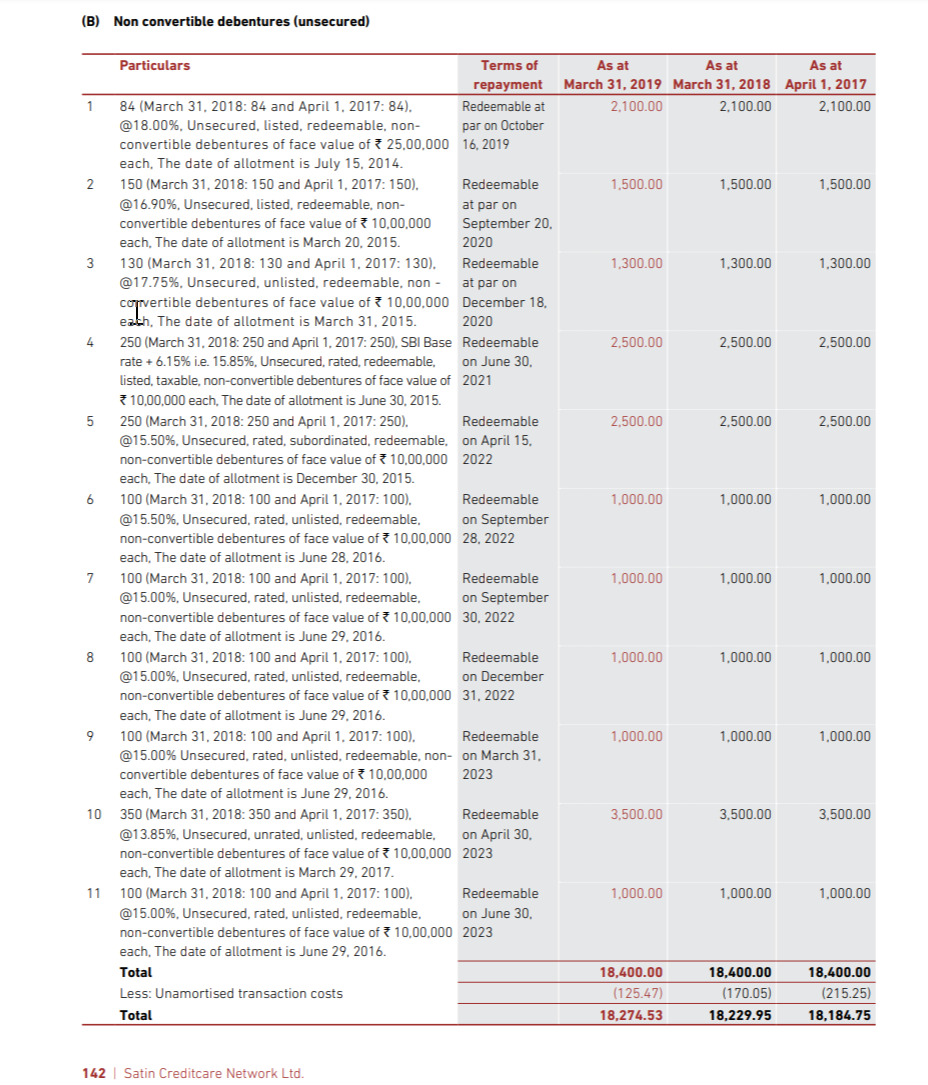

This is interesting because they raised Rs 30 Crores of unsecured debt in December 2019 at 15.5%,the tenure was 7 years and 14 days.

In the subsequent fund raise of unsecured debt done in March 2020 after the covid crisis broke out,they were able to raise money to the tune of 50 Crores at 236 bps lower rate of 13.14%,again the tenure was extremely long at 7 years and 1 month.

Now we can look at this and say that the debt guys are betting that the company will survive at least seven years and the reduction in the company’s borrowing cost means that they feel it is less risky in March 2020 than in December 2019 even after the Covid crisis.

From the company’s point of view,most of their book is short tenure so why would they lock themselves in to this high interest rate for such a long period of seven years?

Overall these 2 issues constitute only about 1-1.5% of their total borrowing.

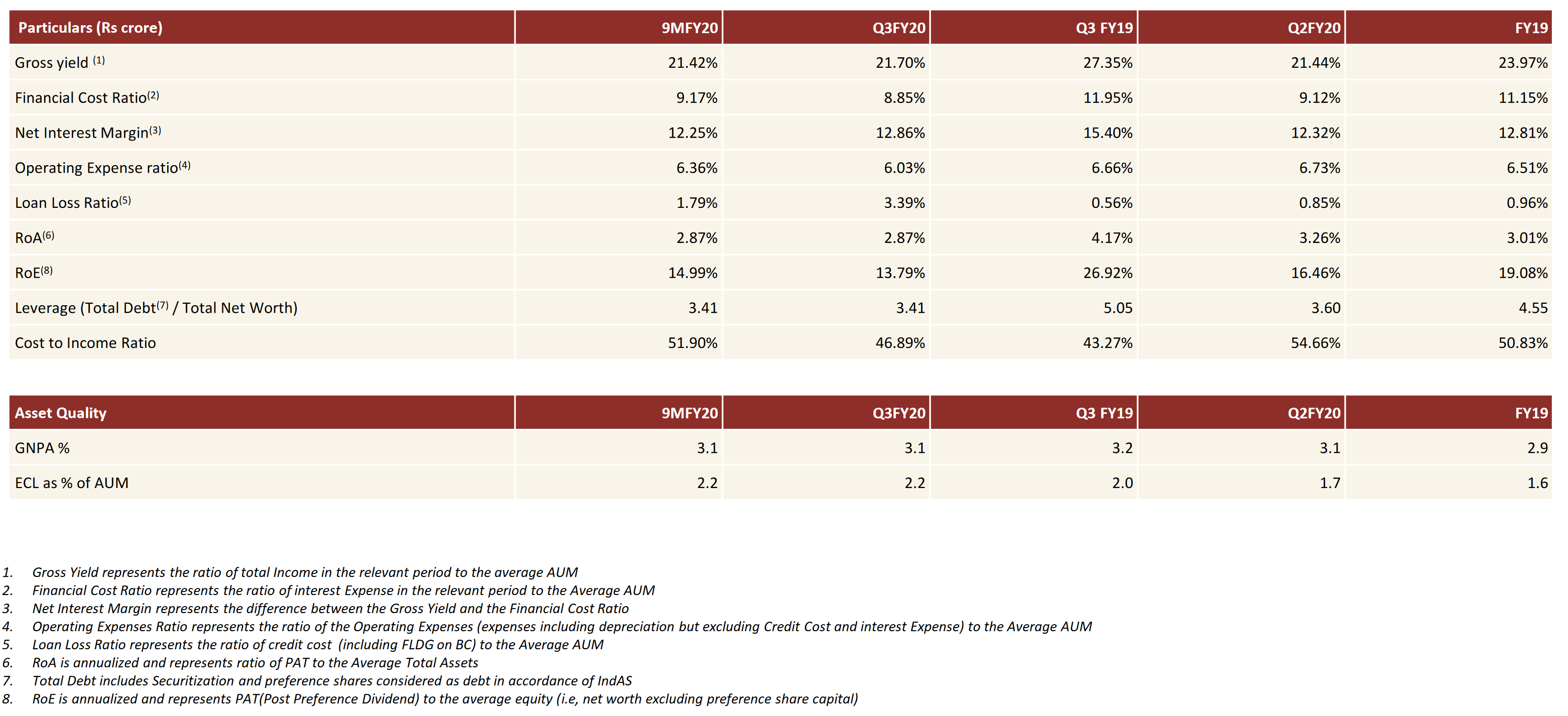

Their portfolio gross yield is about 21% and financial cost is about 8.85% as of Q3.

Finally,I am not recommending this stock as a buy or sell,I am keenly watching developments across companies in the financial space to improve my understanding.

They are increasing the capital base,this will enable the company to raise capital by issuing more shares.

They may be doing this because essentially almost all the microfinance customers are under moratorium and they may need buffers for provisioning and liquidity.

The above interview also is strange,why are they talking about growth in this environment?

Quite an extensive thread this on Satin. I’ve been tracking this company since it was Rs. 120 and now it has dwindled down to Rs. 50, which looks quite an attractive bet with favorable proposition. However, I’ve a found a few niggles which is making me hesitate:

The promoter has pumped in Rs. 100 cr in last 2 years. If they have an alternate source of income, what was the need to pledge their shares and then borrow against it?

The pledges were created when share price was ~Rs. 250-300, and now it is Rs.50. So, will this entail any invocation of pledge or further pledging of shares as top-up?

Company’s Business Correspondent book is heavily tilted towards IndusInd Bank and Yes Bank (75% combined). Could there be any sort of questionable arrangement between them? (I am just being a bit more skeptic!)

Company is assigning 30% of it’s MFI book. Usually, the banks pick up best assets leaving behind inferior ones, so could be we some spike in NPAs going ahead with the stress emerging in the economy?

I’m still looking at the company and trying to find the reasons as to why is it available at 0.2X? What is it that the Street knows and we are missing?

Satin is one company that never recovered from demonetization. Besides frequent dilution and write-offs, they were not able to get NPAs under control. Satin is Yes bank of MFI (that is they lend to most riskiest borrower profile in which Bandhans and Ujjivans could not lend because they thought the borrower is high risk). Their lending rate and borrowing rates clearly reflect it. In a strong market, satin is a risky bet. In a covid-19 world, satin is most probably a write-off which is exactly what is the market is pricing in. High tier 1 capital and ability to write off NPAs or a strong promoter who can provide tier 1 capital is a must for a financial company to survive this downturn. Satin has neither.

I agree with you to an extent. Their high yields on lending clearly highlights the riskiness of its book.But again, my point is that this is an MFI business, unlike corporate where 2-3 bad accounts can wipe off your capital. In this case, you can survive even with 10-12% delinquencies. On capital front, the company is well funded with CAR of 29% and leverage of only 4X. So, my question is- do you think they will see 20-25% kind of slippages? If yes, then not only Satin the entire MFI space should see sharp surge in NPAs, which would possibly mean ‘bye-bye’ to rural story.

So, that is what I want understand, what could be the size of stress? Even at 10% NPA, they will be left with NW of 950 cr and P/BV of 0.3X. Or are you saying there is some fraud in the book and it mght go kaput like DHFL/Yes? If yes, then how is it possible for an MFI.

Just playing a devil’s advocate here. Because if we are wrong, this stock can easily be a five-bagger.

If you want to bet on unbanked and rural story, Bandhan and Ujjivan are much safer stocks. Even these are not risk free.

I can imagine that NPA situation will get quiet bad with many business suffering no revenue for the April quarter and due to the movement of migrant labour, it will be at least another quarter before things can normalise all of which depending on when the lockdown can be lifted. There is no comparative here where people suffered So long with almost zero revenue. Literally survival is the only thing in people’s mind. So repaying instalments on loan would be among the last things in their mind until things get back to normal. I think NPA will be much worse than 10% as demonetization had such levels and this time it’s worse. And even if satin survives, history does not support your 5 bagger Theory as for the last 6 years this stock was a -4 bagger with much stronger economy.

Bandhan at 3.5X still looks expensive especially given its concentration in WB. I think Ujjivan and Equitas could be a bettter bet. My belief is slighty contra to what you siad. Due to reverse migration, the consumption level should go up in rural India and the Govt will have to look after them through MNREGA and stuff. So, the rural businesses, if they do well, then the NPA could be much lower than anticipated.

And your point is valid and even I believe that market is always smarter than us. They have hammered the stock by 90% since 2016. so they are definitely seeing something which I am not able to. Though, I am quite curious as to how the story pans out in next 3-4 quarters. Whether the market gets it right, and if yes, what hanky-panky did the company do, and how.