This is a finance company… capital /debt is raw material… same applies to HDFC Bank even. They pay interest of Rs 10663.37 cr on operating income of Rs 13729.35 (quarterly).

High debt is part and parcel of finance companies. They can not expand without debt if they have to maintain reasonable ROEs and growth.

Looks like AUM is stagnant at ~4400 Crs as it was last quarter, missing management guidance of 5500 Crs by end of FY. Will be clearer once company comes up with presentation.

GNPA improved to 5% from 9% and around ~180 crs in absolute numbers!! This is huge and way beyond expectations.

1-There is write-off about 179 crores from the book for which company has already provided for by provisioning. The previous quarter had this 179 crores in the book and so it was reflecting as GNPA. Now it is not part of the book so it has been taken out from GNPA.

2- Based on my rough calculation there was recovery of 20 - 40 crores of bad loans during previous quarter. We will get the actual number from company presentation or earnings call.

3- The target of 5500 crores was for overall consolidated book. It includes Taraashna and HFC subsidiary. I think the NPA numbers provided by the company are only for Satin standalone. We will get to know the AUM from the company presentation or earnings call.

4- The results are good and company seem to have almost come out from the Demo impact. However they still have 121 crores of Net NPA on the book.

5- It would be interesting to hear management commentary on current political situation and their view of this situation’s impact on the company in the near future and over the next year. It would also be interesting to find the guidance for AUM for 2018-19. My expectation is that they would be targeting somewhere around 40% growth. This is based on what I heard/read from BFI folks.

More than HFC, I am more excited about Capital First tie-up. Capital First is distributing its products, such as 2-wheeler loans, through Satin. This can be something really big in future. Satin can even start small loans for consumer products in future on it’s own. Potential market is even bigger than Bajaj Finserv.

HF on other hand are longer term duration loans. Given that Satin is entirely dependent on borrowing for liability, it can create AL mismatch situation for company. Even Arman is moving into LAP, 8-10 years duration.

IMO, they should stick to fast moving loans with average maturity of 12-18 months.

I attended Q4-Earnings Call of Satin. Following are my notes Performance in FY18 and Q4-FY18

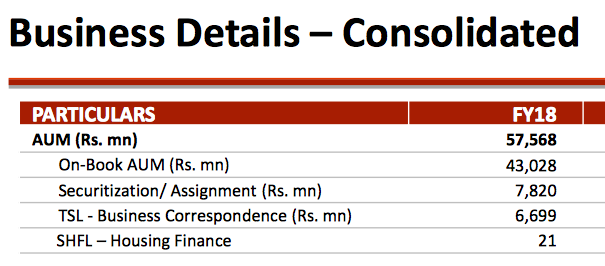

1- Gross AUM grew by 41.6% from 4067 crores in FY-2017 to 5757 crores in FY-2018. MFI lending AUM was 5010 crores registering 40% growth from previous year. MSME, TSL and new Housing Finance AUM together was 747 crores.

2- Collection Efficiency stood at 98% in Q4. Collections also stood at 98% for the loans disbursed after 1st Jan 2017. Collections stood at 99.7% for the loans disbursed to new clients after 1st Jan 2017; this part of the AUM is about 33% of overall AUM. With very little recovery of bad loans from demonetization days in the last quarter the collection efficiency has come down below 100%. Going forward the recovery of left over bad loans from Demonetization should be small.

3- Company is moving towards cashless – 51% of branches have enabled the capability, and 35% of loan disbursed was cashless in Q4. Mr. H P Singh mentioned that cashless disbursement in the current quarter is hitting 50%.

4- There was strong uptick in the loan disbursed in Q4 with average monthly disbursement standing at over 650 crores against 420 crores per month in the previous quarter.

5- Net consolidated profit for Q4 was 44 crores. Networth as on 31st Mar 2018 was 1088 crores and total assets were 5843 crores. Book value per share stood at 222.78.

6- Net NPA stood at 121 crores or 2.90%, and Gross NPA was 216 crores or 5.02%. Please note that these number are consolidated but for on the books AUM. Overall NNPA stood at 130 crores (can be marginally incorrect but this is what I heard).

Subjective Analysis and comments

1- Rural and semi-rural economy has picked up and that is driving growth. Good monsoon would be another trigger.

2- Collaboration with IndusInd for disbursement of loans is working great. MSME loan disbursement to pick up even more speed. HFC loan disbursement would be close to 100 crores in 2018. Main focus of the company would remain micro finance loans.

3- Company is focusing on spreading its wings in east India where MFI penetration is less. WB, Assam and Orissa will drive growth. Company is also planning to have footage in Tripura and Meghalaya.

4- Loan concentration has reduced substantially with UP accounting for lesser than 30%. There is further push to reduce the concentration at district level.

5- Company has made great advances in technology pushing up cashless. A loan can be disbursed in less than 3 minutes and there are feeds available for collection/disbursements every minute.

6- Compared to other MFIs the collection efficiency is still slightly behind because Satin is coming from the most impacted regions of Demonetization. 99% collection efficiency on overall book is not far away and we should reach there in a quarter or two.

7- We would like to keep operational expenditure to about 6.5% despite going for huge branch expansion. We will be able to do it because of automation and technical advancements.

8- Nothing has changed because of Demonetization. The competitive landscape is same and the business opportunity is at least as big as it was earlier.

9- There would be some pressure on the cost of funds but Satin would try to mitigate hit on profitability by better operational performance.

Future outlook

1- AUM growth of more than 40% in FY 2018-19. That would translate into AUM of at least 8060 crores by 31st March 2019. ROA would be maintained above 2.3%.

2- Working with agencies for rating upgrade. There is not much company can do except draw their attention on the performance of the company and capital raised during last year despite all stress. Company is hopeful of an upgrade soon.

3- Company believes that despite a lot of elections coming up it would be able to navigate the situation. Learnings from demonetization and technology would come handy. In the past loan waivers had net positive impact on the collections in UP and Punjab, and so company is not stressed about these waivers announced in other states.

Other notes

I also got opportunity to ask a question to Mr. H P Singh about PAR1 and PAR90 coming down but still collection efficiency trending down in this quarter. Frankly I did not articulate my question well because I was not expecting that I would get a chance based on the past experiences and so I was caught by surprise. Will be better prepared next time. However very detailed and convincing answer was provided by Mr. Singh. He explained that in the last few quarters efficiency was high because of recovery of bad loans from Demonetization days, and that is fading away with only hard bad loans left on the table.

There is a possibility that I would have heard things incorrectly and so what I have stated above are factually incorrect. I am not an analyst and this is not a buy or sell recommendation.

Hi Krishna, I was there on call and Mr. Singh meant this only. You have covered all the points nicely.

I also liked his answer on why company has not provided completely with net NPA of INR 130 crs still on books, when he said that this is a going concern and I would not like to shoot myself in the foot by 1-shot provisioning. He was pretty forthcoming about the situation and also upbeat about the future. I observed same tone from managements of Ujjivan and Arman as well. Let’s hope for turnaround in stock’s fortune as well.

They have already pledged 1/3rd of their holding prior to the new pledge. I don’t know where v stand as total now. Since mid n small cap under lot of pressure, hope going forward it won’t lead to margin call.

Banks taking over micro finance institutions continues with Federal Bank taking the plunge. This comes after the highly publicized BFI takeover by Indusind. On the face of it for a MFI with AUM of 1200 crores the valuation of 700 odd croes looks expensive. But then we do not know other details like AUM growth yoy, asset management, book value and many more things which matter a lot. However just to compare the valuation in the same industry Satin with AUM of more than 5700 crores (as of 31st Mar 2018 which by now would have crossed 6000 crores) has market cap of less than 1600 crores.

However the second one is mysterious (at this point of time). It just says that trading window would be closed from tomorrow till 13th July EOD for the insiders. I am expecting the real news to come tomorrow some time. Not sure what it would be but being an investor in this company I am hoping that it would be something positive. Here is the second notification https://www.bseindia.com/corporates/anndet_new.aspx?newsid=8107cda3-f951-4dac-a8cf-ec6ff0973c89

On consolidated basis

o Gross loan portfolio at Rs. 6025.7 cr – an increase of 42.8% YoY

o During the quarter, a total of 22 new branches were started taking the total

number of branches to 1017 as on Jun‐18.

o Revenue for Q1FY19 Rs. 336 Cr – an increase 32.3% YoY

o Securitization & Assignment portfolio stood at Rs. 800 Cr – an increase of 231% YoY. o Q1FY19 Profit Before Tax at Rs. 41.3 Cr, as against Loss Before Tax at Rs. 128.4 Cr in

Q1FY18.

o Q1FY19 Profit After Tax at Rs. 27.5 Cr, as against Loss After Tax at Rs. 83.8 Cr in q1fy18

Keeping the trend of the past many quarters this time too I attended the ‘Q1 2018-19’ earnings call of Satin. Here are my notes

Factual Statements

1- Gross AUM as on 30th June 2018 was 6025.7 crores. MFI AUM was 5314 crores and non MFI (MSME, BC, HFC) stood at 711.7 crores. Gross AUM grew by 42.77% YoY and 4.67% QoQ. The PAT stood at 27.2 crores resulting in EPS of 5.61 on the diluted equity base 48.5 crores.

2- The company has now more than 3 million clients, It operates in 20 states and has more than 1000 branches. The company is quickly adopting cashless disbursements with 90% of its branches now equipped with it. In Q1 57% of disbursement was cashless compared to 35% in previous quarter.

3- Collection efficiency stood at 98% in Q1. In the previous quarter too it was at the same level. The new clients acquired after 1st Jan 2017 had higher collection efficiency at 99.6%. Collection Efficiency is defined as Collection Efficiency (for a defined period for example in above Q1 2019) = Collection including arrears (ex-prepayments) during the period /Current demand for the same period.

4- There was meaningful improvement in Portfolio At Risk(PAR) numbers. PAR1 improved from 6.7% to 5.9%, PAR30 5.9% to 5.0% and PAR90 (also known as Gross NPA) moved from 4.4% to 3.9%.

5- Absolute non-performing assets were 212 crores. Company has provided provision for 190 crores. So net NPA would be 22 crores or 0.4%.

6- Company has moved its accounting from GAAP to INDAS. There are quite a few changes in the new Accounting Standards. There is no concept of NNPA. The provisioning for the bad loans need to be provided from the day1. In INDAS there is concept of Expected Credit Loss (ECL) which is probability of credit losses over the expected life of the financial asset. The ECL for the company stood at 3.5% against 4.1% in the previous quarter. Per the INDAS company has completely provided for it’s bad loans.

Discussion and forward looking statements

1- Company is still guiding for credit cost to be 1% for the current financial year.

2- Company is still guiding for 40% plus AUM growth and 2.3% plus ROA in the current financial year. Multiple times Mr. H P SIngh stated that they are on track to meet this target.

3- The new clients acquired after 1st Jan 2017 would constitute more than 50% of AUM before the end of current FY. From the current quarter we would start seeing the overall collection efficiency improving from 98%.

4- Company is done with all provisioning. From here on, suppose the AUM would grow by 1000 crores in next few quarters and ECL would be 2.7% then the company would be required to provide additional provision of only 27 crores. This is going to very positively impact the profitability of the company from now onwards.

5- Operational cost would remain around 6% despite company growing in even new geographies.

70% of disbursements are now happening in new territories and 30% in old ones.

6- The IndusInd collaboration is working great and it is picking up nicely. AUM was 47 crores from this business. The capital first thing is not going fast. It is a low key for now.

7- Disbursement is normally low in Q1 and to some extent even in Q2, and then it picks up.

The company is aggressively working on bringing down the credit cost and reducing concentration. UP is now 24% of AUM which was about 40% couple of years ago.

My interpretations

1- The good news is there is almost no bad loan sitting on the books for which provisioning is not done. This is a huge relief.

2- I expect the collection efficiency to slowly inch upwards starting the current quarter and reach 99% by end of this financial year.

3- Improved collection efficiency, controlled operational cost and lower provisioning would push up the profitability. The company should post consolidated PAT north of 160 crores for the the full year FY 18-19. The year-end book value should be around 235 giving net-worth to the company of about 1140 cores.

4- The main risk is excessive obsession with the AUM growth. I would love for the company to have this level of obsession for reducing the credit cost.

5- The second risk is there are many elections coming up and the political drama can cause churn in the operations. Loan waivers definitely create an element of doubt in the minds on borrowers.

6- The third risk (and maybe even opportunity) is company is putting its hands in many things – MFI, MSME, BC, HFC, Vehicle loans etc. While the core business remains same still the diversification dilutes the focus of the management.

I am invested in Satin and so I have ownership bias. I may have misheard things said in the earnings call and so please verify them first-hand before accepting.

thanks for the notes. can u explain me how 190 cr of loan is provisioned for? i can see 45 cr as credit loss, what is that exactly? how is the credit loss expected to be in the coming quarters?